Agroscience Market Size and Trends

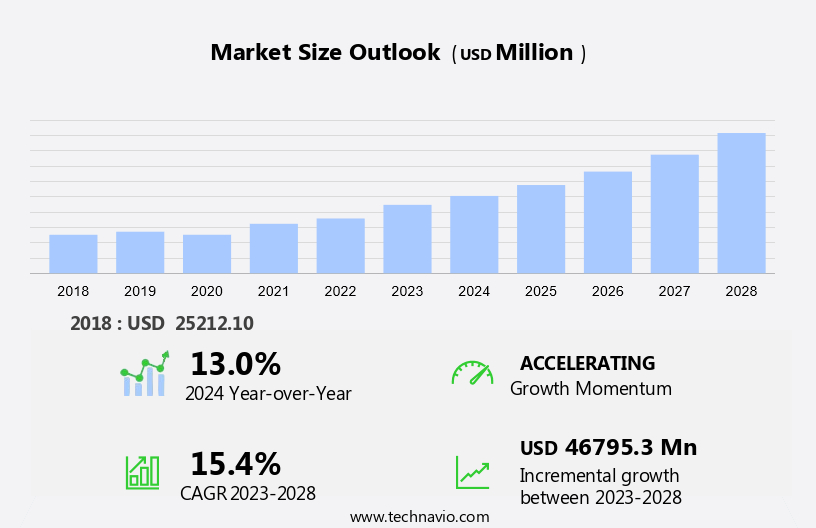

The agroscience market size is forecast to increase by USD 46.80 billion, at a CAGR of 15.4% between 2023 and 2028. The market is experiencing significant growth due to various factors. Shrinking arable land and the need for sustainable agricultural practices are driving the demand for innovative farming methods. Conventional farming continues to dominate, but organic farming and hydroponic or aeroponic systems are gaining popularity among farmers, commercial growers, retailers, farmers, home gardeners, and professional landscapers. Technological improvements are leading to more efficient methods of agriculture, enabling increased food and fiber production. However, challenges persist in plant breeding, requiring ongoing research and development. This market analysis report provides a comprehensive examination of these trends and challenges, offering valuable insights for stakeholders in the market. The report's professional tone and adherence to formal business writing standards make it an essential resource for decision-makers seeking to navigate the complexities of the market.

The market plays a vital role in addressing the increasing food demand and ensuring sustainable farming practices. With the global population projected to reach 9.7 billion by 2050, the need for advanced agricultural solutions becomes increasingly important. Agroscience encompasses various sectors, including field crops, fruits and vegetables, fibre production, and horticulture. Climate change poses a significant challenge to food production, necessitating the adoption of precision agriculture. This farming approach leverages big data and IoT devices to optimize crop yields, reduce waste, and minimize environmental impact. Precision agriculture incorporates techniques such as soil sampling, satellite imagery, and weather forecasting to enhance crop production systems. Biotechnology products, including genetically modified crops (GM seeds), biopesticides, and fertilizers, contribute significantly to the market. GM seeds offer resistance to herbicides and insects, ensuring higher crop yields and reduced reliance on chemical inputs.

Biopesticides, derived from natural sources, provide effective pest control while minimizing environmental impact. Fertilizers, enriched with active ingredients, improve soil health and nutritional profiles, leading to healthier crops and increased productivity. Agronomy and soil science are essential components of the market. Agronomy focuses on optimizing crop production through scientific management practices, while soil science aims to improve soil health and fertility. Biostimulants, including acid-based and extract-based products, promote plant growth and enhance crop yields by improving soil structure and nutrient availability. The market is driven by the need for sustainable food production and fibre production. Crop protection is a critical aspect of sustainable farming, ensuring that crops remain healthy and productive despite environmental challenges. Crop genetics plays a significant role in developing new varieties with desirable traits, such as disease resistance and improved nutritional profiles. The market is continually evolving, with ongoing research and development in areas such as biotechnology, precision agriculture, and crop protection. As the world population grows and climate change continues to impact food production, the importance of the market in ensuring a sustainable and productive food supply becomes increasingly evident.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Product

- Genetically modified seeds

- Biopesticides

- Biostimulants

- Geography

- North America

- Canada

- Mexico

- US

- APAC

- China

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- North America

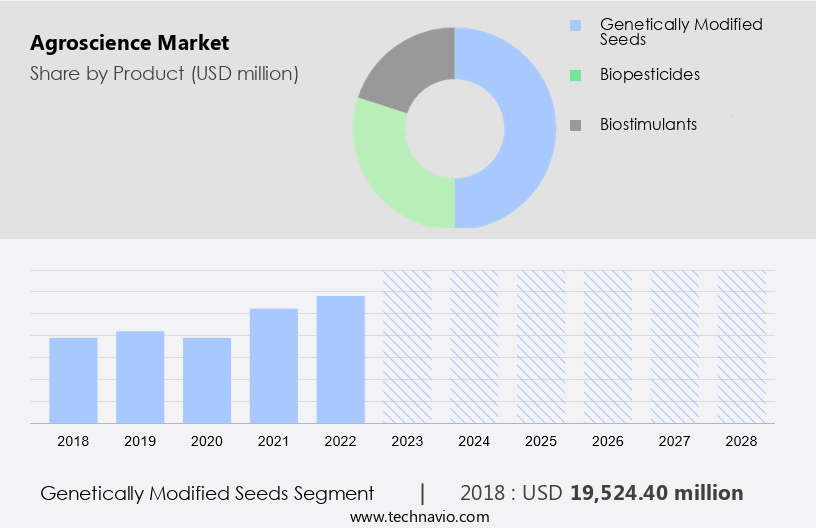

By Product Insights

The genetically modified seeds segment is estimated to witness significant growth during the forecast period. The market has witnessed substantial growth, particularly in the sector of Cereals and Grains, driven by the adoption of advanced agricultural techniques. Genetically modified seeds have revolutionized crop production by incorporating specific traits, such as herbicide tolerance and pest resistance, through the direct manipulation of their DNA. This innovation has been instrumental in addressing the challenges of conventional farming, organic farming, hydroponic, and aeroponic systems, catering to the needs of retailers, farmers, commercial growers, home gardeners, and professional landscapers.

Get a glance at the market share of various segments Download the PDF Sample

The genetically modified seeds segment was valued at USD 19.52 billion in 2018. Genetically modified seeds were the leading segment of the market and their dominance is expected to persist throughout the forecast period. The shrinking arable land and the increasing global population necessitate the need for sustainable agricultural practices and higher food production and fiber production. By 2050, food consumption is projected to rise by 59% to 98%. In this context, genetically modified seeds offer a viable solution to meet the growing demand for food security while minimizing the environmental impact. Agronomy plays a crucial role in optimizing the potential of these seeds, ensuring their successful implementation and maximizing their benefits.

Regional Analysis

For more insights on the market share of various regions Download PDF Sample now!

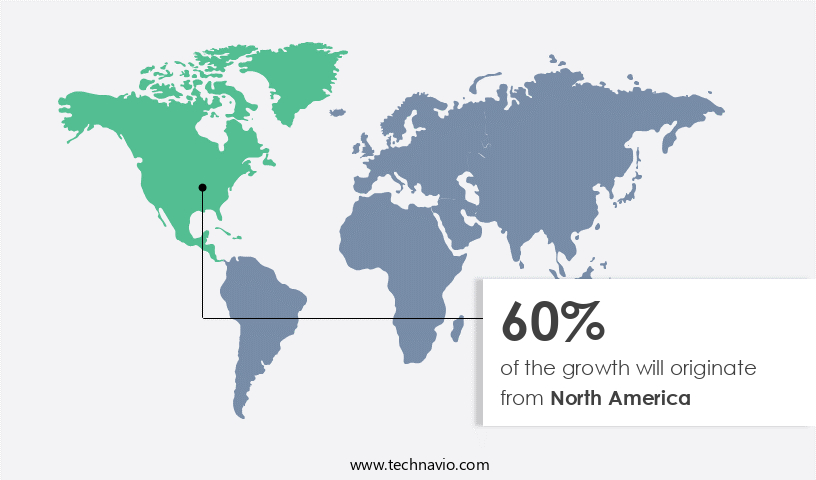

North America is estimated to contribute 60% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The market in North America is projected to lead the global market due to advancements in precision farming and biotechnology. The US, being the market leader in this region, is witnessing significant growth in the production of enzymes using gene technology and the development of acid-based biostimulants. Technological innovations in the agricultural sector, such as smart machinery, robotics, AI, and machine learning, are driving agricultural productivity in the US and Canada. Additionally, the increasing food demand and regulations limiting pesticide usage are fueling the demand for biological control products to manage pests like thrips and whiteflies. The Market in North America is poised for growth during the forecast period.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Agroscience Market Driver

Shrinking arable land is notably driving market growth. The market is experiencing significant growth due to the decreasing size of arable land worldwide. This trend is linked to a decline in total factor productivity (TFP), leading to increased demand for genetically modified seeds, biopesticides, and other solutions to preserve crop productivity on existing farmland. For example, the global arable land area has been decreasing at a substantial rate, primarily due to urbanization. TFP is a crucial measure of agricultural productivity that takes into account the total capital, labor, material resources, and land used in agricultural production, as well as livestock and crop output. As the availability of arable land shrinks, the need for advanced agricultural technologies, such as crop genetics, soil health management, precision agriculture, and bio-based alternatives, becomes increasingly important for sustainable food production in the face of food demand growth and climate change challenges.

The integration of big data, IoT devices, and artificial intelligence (AI) in agriculture is also playing a significant role in enhancing agricultural productivity and efficiency. Key players in the market include companies focusing on crop protection, crop genetics, and nutritional profiles, among others. The market is expected to continue growing as farmers and agricultural businesses seek innovative solutions to address the challenges of feeding a growing population while minimizing the environmental impact of agriculture. Thus, such factors are driving the growth of the market during the forecast period.

Agroscience Market Trends

Technological improvements leading to efficient methods of agriculture is the key trend in the market. Agroscience plays a crucial role in addressing the increasing food demand amidst the declining arable land. Advanced farming practices, such as sustainable agriculture, are being adopted to enhance crop yields and mitigate the effects of climate change. Precision agriculture, biopesticides, genetically modified crops, seeds, crop protection products, fertilizers, and biotechnology products are some of the key areas driving innovation in Agroscience. New breeding techniques, including Cisgenesis, Intragenesis, Targeted mutagenesis, and various short-term recombinant DNA techniques, are revolutionizing agriculture. These techniques enable the transfer of desirable traits, improve crop resilience, and increase yields.

RNA-induced DNA methylation gene silencing, reverse breeding, and grafting a non-GM scion onto the GM rootstock are other emerging techniques that hold significant potential. The application of these advanced techniques in field crops, fruits and vegetables, ornamentals, and turf is essential to ensure food security and maintain agricultural productivity. By adopting these innovative solutions, Agroscience is poised to overcome the challenges of feeding a growing population while preserving the environment. Thus, such trends will shape the growth of the market during the forecast period.

Agroscience Market Challenge

Challenges associated with plant breeding is the major challenge that affects the growth of the market. Agroscience is a critical field focusing on improving agricultural productivity and sustainability. One of its key solutions is plant breeding, which enables farmers to develop high-yielding, climate-resilient crops. However, plant breeding faces numerous challenges. Increased CO2 concentration and the greenhouse effect, along with rising temperatures, bring about more frequent extreme weather conditions, such as heatwaves, typhoons, and forest fires, negatively impacting crop growth. Even seemingly minor annual climate variations can have drastic consequences if a threshold is crossed, leaving essential crops unable to adapt.

Additionally, crop diseases and nutritional deficiencies pose significant challenges. To address these issues, agroscience employs advanced technologies like genome editing, precision agriculture, and smart farming. These technologies enhance nutrient content, post-harvest shelf life, and resource optimization, while promoting soil health management and employing microbial solutions. Furthermore, big data analytics and biologicals play a crucial role in enhancing agricultural practices and mitigating the impact of climate change. Hence, the above factors will impede the growth of the market during the forecast period

Exclusive Customer Landscape

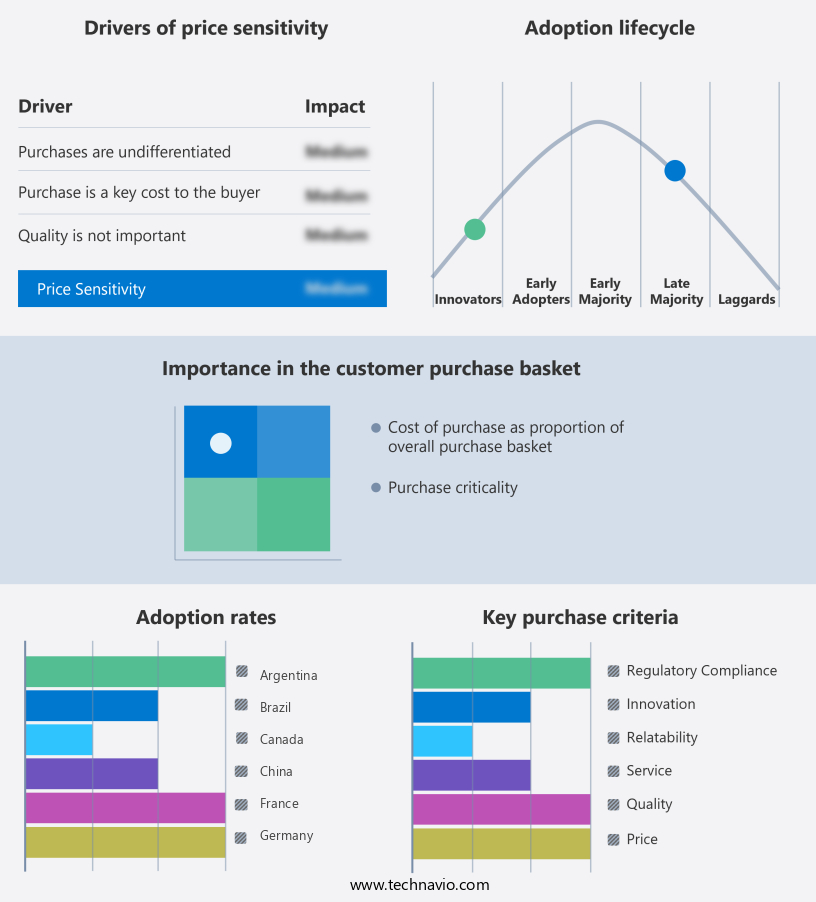

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AgBiTech Pty Ltd. - The company offers agroscience such as biological pest control solutions, focusing on environmentally friendly methods to manage agricultural pests through the use of beneficial insects and microbial products.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADAMA Ltd.

- Agrinos AS

- Andermatt Group AG

- Arysta LifeScience Corp.

- BASF SE

- Bayer AG

- Biostadt India Ltd.

- BioWorks Inc.

- Corteva Inc.

- FMC Corp.

- Koppert

- Novozymes AS

- Nufarm Ltd.

- Nutrien Ltd.

- Stoller Group

- Sumitomo Chemical Co. Ltd.

- Syngenta Crop Protection AG

- VALAGRO Spa

- Valent BioSciences LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market is witnessing significant growth due to the increasing food demand and the need for sustainable farming practices. With climate change posing a major challenge to agricultural productivity, precision agriculture and biotechnology are playing a crucial role in enhancing crop yields. Biopesticides, genetically modified crops, seeds, fertilizers, and biotechnology products are some of the key offerings in the market. Sustainable agricultural practices such as organic farming, hydroponics, and aeroponics are gaining popularity among farmers, commercial growers, retailers, home gardeners, professional landscapers, and consumers. The focus on food security and consumer health is driving the demand for sustainable food production, which in turn is fueling the growth of the market.

Digital agriculture, precision farming, and biotechnology are revolutionizing agriculture by providing solutions for climate-smart agriculture, vertical farming, smart machinery, robotics, and artificial intelligence. The use of big data, IoT devices, and AI in agriculture is enabling farmers to optimize resources, manage soil health, and control crop diseases and nutritional deficiencies. The market is also witnessing the development of biological control products, biostimulants, and microbial solutions to address crop diseases and nutrient content. The market is expected to grow further with the adoption of CRISPR-Cas9 and genome editing technologies for creating climate-resilient crops and enhancing nutritional profiles and post-harvest shelf life.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.4% |

|

Market Growth 2024-2028 |

USD 46.80 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

13.0 |

|

Regional analysis |

North America, APAC, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 60% |

|

Key countries |

US, China, Brazil, India, Canada, Germany, UK, Mexico, Argentina, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ADAMA Ltd., AgBiTech Pty Ltd., Agrinos AS, Andermatt Group AG, Arysta LifeScience Corp., BASF SE, Bayer AG, Biostadt India Ltd., BioWorks Inc., Corteva Inc., FMC Corp., Koppert, Novozymes AS, Nufarm Ltd., Nutrien Ltd., Stoller Group, Sumitomo Chemical Co. Ltd., Syngenta Crop Protection AG, VALAGRO Spa, and Valent BioSciences LLC |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for market forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -