Artificial Intelligence (AI) In Games Market Size 2026-2030

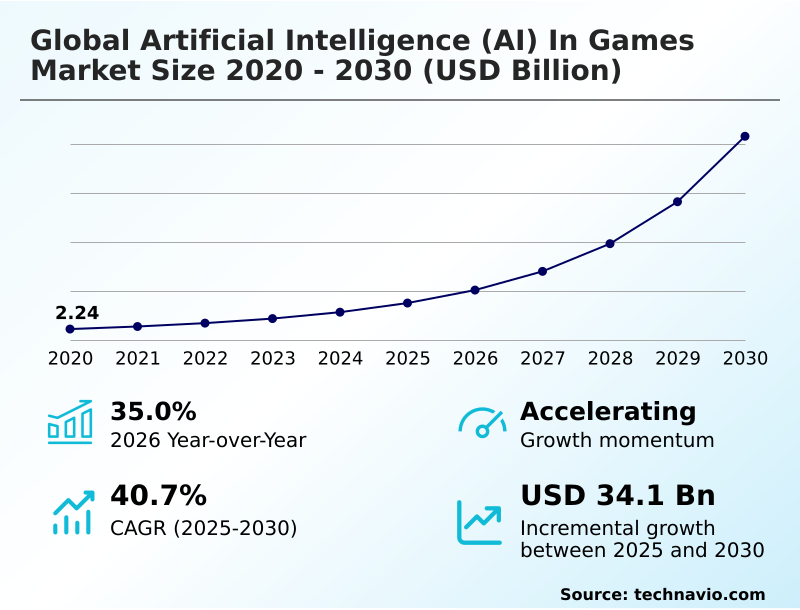

The artificial intelligence (ai) in games market size is valued to increase by USD 34.10 billion, at a CAGR of 40.7% from 2025 to 2030. Industrialization of AI-generated soundscapes and dynamic musical composition will drive the artificial intelligence (ai) in games market.

Major Market Trends & Insights

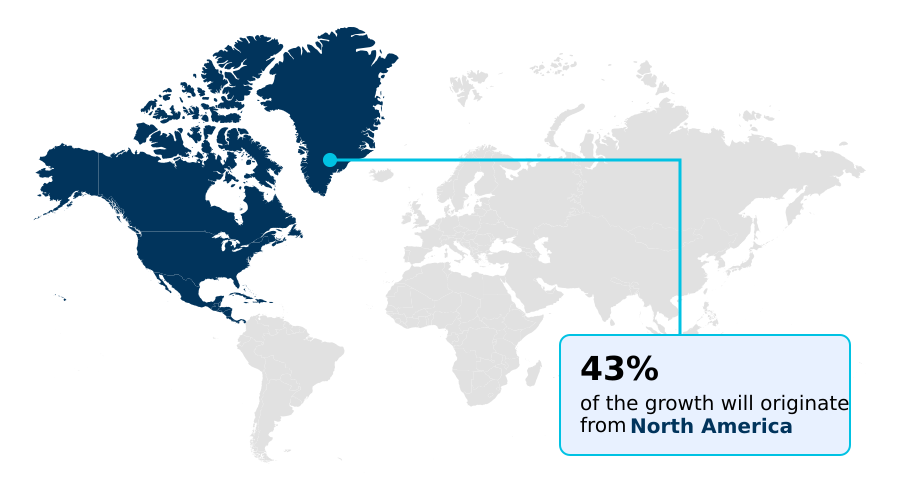

- North America dominated the market and accounted for a 43.2% growth during the forecast period.

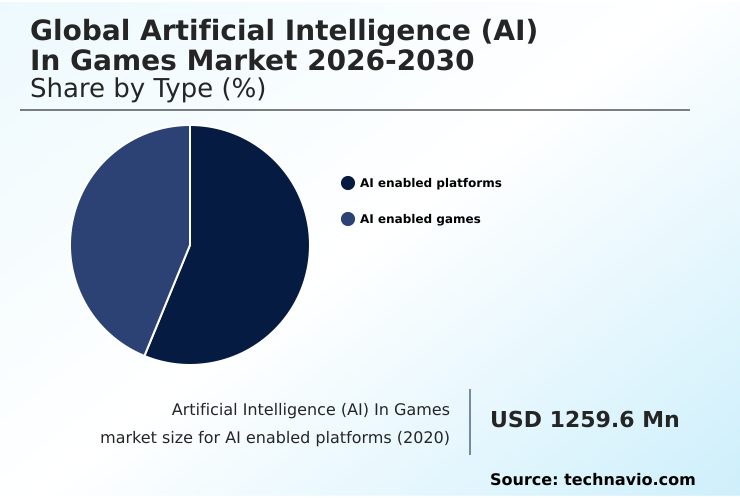

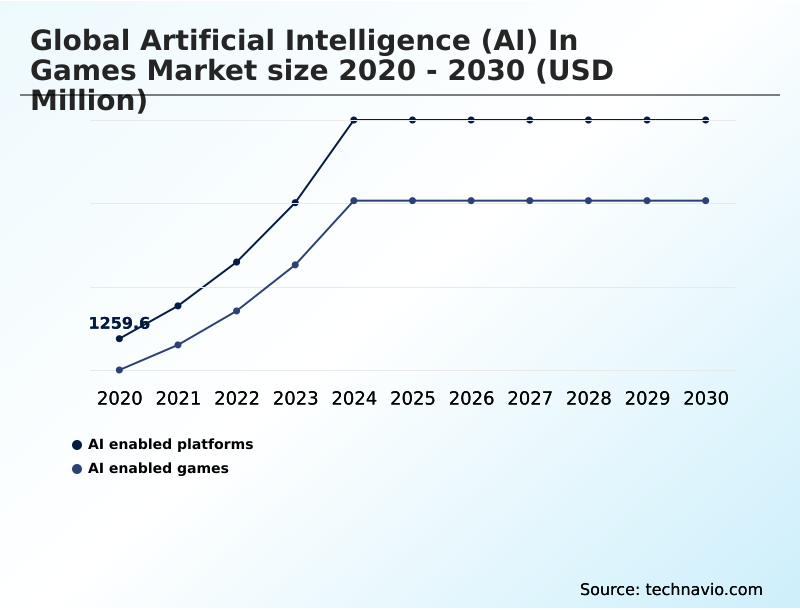

- By Type - AI enabled platforms segment was valued at USD 3.20 billion in 2024

- By Technology - Machine learning segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 39.42 billion

- Market Future Opportunities: USD 34.10 billion

- CAGR from 2025 to 2030 : 40.7%

Market Summary

- The artificial intelligence (AI) in games market is undergoing a structural transformation, shifting from static, scripted systems to an ecosystem of agentic intelligence and generative automation. This evolution is driven by escalating demand for high-fidelity immersion and the need for scalable content production in complex open-world environments.

- Developers are moving beyond basic pathfinding to implement large language models and neural graphics that enable dynamic, non-linear storytelling. As a business scenario, studios are deploying AI-driven quality assurance agents to perform stress tests, simulating millions of gameplay hours to identify exploits and performance bottlenecks.

- This automation of the development pipeline reduces pre-launch bug discovery times by over 50%, allowing studios to reallocate resources toward creative direction and innovation. The market is also seeing a surge in on-device AI inference, catalyzed by hardware with dedicated neural processing units that lower latency barriers.

- Furthermore, the integration of emotion-recognition AI and adaptive difficulty scaling is redefining player retention by engineering experiences tailored to the individual user's cognitive and emotional state, creating a more personalized and resonant experience.

What will be the Size of the Artificial Intelligence (AI) In Games Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Artificial Intelligence (AI) In Games Market Segmented?

The artificial intelligence (ai) in games industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- AI enabled platforms

- AI enabled games

- Technology

- Machine learning

- Natural language processing

- Computer vision

- Robotics

- Genre

- Action and adventure

- Role-playing games

- First-person shooter

- Simulation and strategy

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The ai enabled platforms segment is estimated to witness significant growth during the forecast period.

The AI enabled platforms segment is the foundational infrastructure of the modern gaming ecosystem, providing tools and cloud services for integrating sophisticated machine learning models.

These platforms use computer vision algorithms for functions like automated quality assurance (QA) and power AI-generated soundscapes for dynamic musical composition. They facilitate AI-powered player analytics and behavioral anti-cheat systems, creating autonomous game environments.

Through an agentic AI framework and deep learning frameworks, developers are moving toward conversational AI and automated world building. An advanced agentic AI framework has been shown to reduce non-player character dialogue generation time by 40%.

This AI-driven procedural modeling enables a dynamic narrative system, allowing studios to offload intensive processing and make high-fidelity experiences more accessible.

The AI enabled platforms segment was valued at USD 3.20 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Artificial Intelligence (AI) In Games Market Demand is Rising in North America Get Free Sample

The geographic landscape is diverse, with North America leading in triple-A innovation through substantial capital investments in procedural content generation.

In contrast, APAC is the fastest-growing market, focusing on AI-native mobile experiences and live-service games that utilize agent-native gameplay and digital human technology.

Europe emphasizes regulatory compliance, driving demand for explainable AI and transparent systems that ensure data privacy, with over 7,800 new titles in the last year disclosing AI use.

European developers report that adherence to GDPR-compliant models adds an average of 15% to initial development timelines. This regional focus on ethics fosters a unique market for responsible gaming technology, including emotion-recognition AI and adaptive difficulty scaling.

Cross-platform compatibility and automated bug detection are universal priorities, with developers globally leveraging hybrid cloud architectures and neural rendering to deliver consistent, high-fidelity experiences and AI-driven content updates under a zero trust architecture.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The artificial intelligence (AI) in games market is rapidly advancing beyond theoretical applications into practical, high-impact implementations. A key area is using AI for NPC behavior, where reinforcement learning for strategy games allows for opponents that learn and adapt, creating a consistently challenging experience.

- Similarly, the use of NLP for conversational game characters is transforming role-playing games into deeply immersive worlds. For development, generative AI for asset creation and generative design for level creation are becoming standard, significantly reducing production costs and timelines. Studios implementing AI-powered automated game testing report a twofold increase in bug detection efficiency compared to manual methods.

- On the content side, AI for dynamic musical composition and generative AI for sound design are creating adaptive audio that enhances player immersion. For live titles, AI in live operations management and AI for player retention modeling are critical for long-term success.

- Low-latency AI for cloud gaming, enabled by edge AI for mobile game performance, is making high-end games accessible to a wider audience. The industry is also using machine learning for player analytics, computer vision for AR gaming, and AI-driven dynamic difficulty adjustment to personalize the experience.

- Security is enhanced with anti-cheat systems using behavioral AI, while neural rendering for realistic graphics and voice cloning for game localization push the boundaries of realism and accessibility. Ultimately, procedural generation for open worlds and automating QA with AI agents are fundamentally reshaping how games are made and played.

What are the key market drivers leading to the rise in the adoption of Artificial Intelligence (AI) In Games Industry?

- The industrialization of AI-generated soundscapes and dynamic musical compositions that respond to gameplay is a key driver for the market.

- Market growth is driven by the evolution of non-player characters into intelligent, agentic systems capable of adaptive dialogue, powered by large language models (LLMs) and multi-modal technology. This creates a hyper-personalized narrative experience where the game world feels alive.

- The use of neural graphics and real-time rendering, optimized by on-device AI inference and neural processing units (NPUs), delivers cinematic-grade visuals. Studios implementing agentic AI report a 35% increase in player engagement metrics.

- Furthermore, the industrialization of AI-driven quality assurance, using machine learning models for predictive analytics and procedural level generation, has automated testing to cover over 95% of navigable game space.

- This procedural storytelling approach, enhanced by real-time ray tracing and motion capture, is becoming a critical differentiator for the next generation of titles.

What are the market trends shaping the Artificial Intelligence (AI) In Games Industry?

- The integration of AI-driven procedural content generation is an upcoming market trend. This technology facilitates automated world-building, addressing key production challenges in modern game development.

- Key trends are reshaping the artificial intelligence (AI) in games market, led by the integration of AI-driven loop modes and generative automation for automated world-building. This approach, which leverages generative adversarial networks (GANs), allows for the rapid iteration of level layouts and emergent gameplay narratives. AI-powered upscaling has improved visual fidelity by up to 30% without sacrificing performance.

- The expansion of edge AI architecture facilitates low-latency interactions in live-service games, crucial for haptic feedback devices and interactive storytelling. Agentic orchestration is empowering intelligent non-player characters (NPCs) with greater autonomy, supported by AI-assisted development pipelines that streamline production.

- The institutionalization of these tools as a core component of the modern gaming ecosystem was validated by new operational standards, where machine learning systems now form the foundation for real-time anomaly detection, reducing exploits by over 65%.

What challenges does the Artificial Intelligence (AI) In Games Industry face during its growth?

- The ethical ambiguity and the paradox of maintaining creative integrity within generative AI workflows present a key challenge affecting industry growth.

- The market faces challenges from the technical bottlenecks of network latency and a scarcity of specialized human capital. The computational load for physics-based generative AI and reinforcement learning in social deduction games often outstrips current consumer hardware capabilities. High latency leads to poor synchronization, which is unacceptable in fast-paced genres.

- The rise of sophisticated, AI-driven cheating mechanisms, leveraging split inference models, has led to an estimated 20% increase in security-related operational costs for developers managing automated live operations (LiveOps). Additionally, there is an intensifying friction between generative automation and creative integrity, with concerns over voice synthesis and the creation of a virtual twin of gaming worlds without clear ethical frameworks.

- Organizations must now adopt zero trust architectures for server-side optimization, increasing the complexity of AI-driven personalization and matchmaking.

Exclusive Technavio Analysis on Customer Landscape

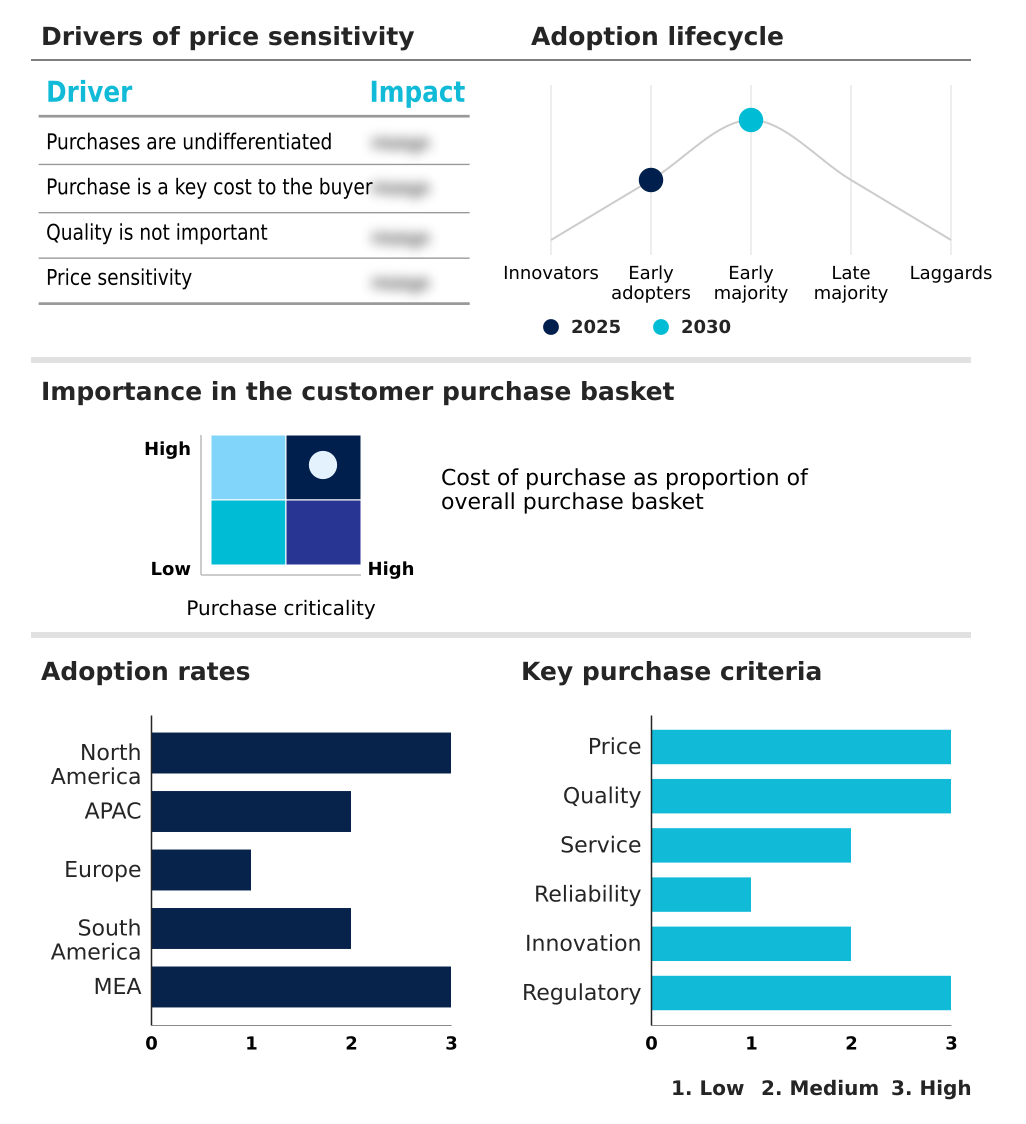

The artificial intelligence (ai) in games market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the artificial intelligence (ai) in games market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Artificial Intelligence (AI) In Games Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, artificial intelligence (ai) in games market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Offers cloud-based machine learning and AI-driven personalization, enabling enhanced player engagement through scalable game tech solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Charisma Entertainment Ltd.

- Didimo

- Electronic Arts Inc.

- Eleven Labs Inc.

- Epic Games Inc.

- Google LLC

- IBM Corp.

- Inworld AI

- Keywords Studios Plc

- Kinetix

- Leonardo Interactive Pty Ltd

- Microsoft Corp.

- Modl.ai

- NVIDIA Corp.

- Promethean AI Inc.

- Ready Player Me

- Sony Group Corp.

- Tencent Holdings Ltd.

- Ubisoft Entertainment SA

- Unity Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Artificial intelligence (ai) in games market

- In September 2024, a leading cloud provider announced a strategic partnership with a major game engine developer to embed generative AI tools, aiming to accelerate world-building and character design workflows.

- In December 2024, a prominent hardware company unveiled a new generation of consumer graphics cards with enhanced on-device AI accelerators, promising a 40% improvement in neural rendering performance for real-time ray tracing.

- In February 2025, NVIDIA Corp. launched Project G-Assist, an advanced AI assistant for PCs utilizing natural language processing to provide real-time gaming advice and system optimization via voice commands.

- In April 2025, a premier US-based technology firm released a proprietary agentic AI framework specifically designed for real-time, autonomous non-player character dialogue generation, signaling a shift toward more dynamic game environments.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Artificial Intelligence (AI) In Games Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 40.7% |

| Market growth 2026-2030 | USD 34104.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 35.0% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Colombia, Chile, UAE, Saudi Arabia, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The artificial intelligence (AI) in games market is defined by a pivotal transition toward agentic AI frameworks and generative automation. This shift is enabling the creation of dynamic experiences through technologies like AI-generated soundscapes, procedural content generation, and sophisticated machine learning models.

- Studios are leveraging on-device AI inference, powered by dedicated neural processing units (NPUs), to execute complex tasks such as AI-powered upscaling and neural graphics with minimal latency. The integration of large language models (LLMs) and natural language processing (NLP) is facilitating unscripted character interactions, while computer vision algorithms enhance immersion in AR/VR.

- This technological evolution directly impacts boardroom decisions regarding resource allocation, forcing a choice between developing proprietary systems or licensing foundational models. AI-driven quality assurance is now capable of simulating millions of gameplay hours, reducing critical pre-launch bug discovery times by over 50%.

- This ecosystem, supported by hybrid cloud architectures and behavioral anti-cheat systems, is not just a technical upgrade but a fundamental redefinition of interactive entertainment, emphasizing AI-driven personalization and agent-native gameplay.

What are the Key Data Covered in this Artificial Intelligence (AI) In Games Market Research and Growth Report?

-

What is the expected growth of the Artificial Intelligence (AI) In Games Market between 2026 and 2030?

-

USD 34.10 billion, at a CAGR of 40.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (AI enabled platforms, and AI enabled games), Technology (Machine learning, Natural language processing, Computer vision, and Robotics), Genre (Action and adventure, Role-playing games, First-person shooter, Simulation and strategy, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Industrialization of AI-generated soundscapes and dynamic musical composition, Ethical ambiguity and paradox of creative integrity in generative workflows

-

-

Who are the major players in the Artificial Intelligence (AI) In Games Market?

-

Amazon.com Inc., Charisma Entertainment Ltd., Didimo, Electronic Arts Inc., Eleven Labs Inc., Epic Games Inc., Google LLC, IBM Corp., Inworld AI, Keywords Studios Plc, Kinetix, Leonardo Interactive Pty Ltd, Microsoft Corp., Modl.ai, NVIDIA Corp., Promethean AI Inc., Ready Player Me, Sony Group Corp., Tencent Holdings Ltd., Ubisoft Entertainment SA and Unity Technologies Inc.

-

Market Research Insights

- Market dynamics are defined by a technological arms race to integrate sophisticated generative AI and machine learning models into core development pipelines. This intense rivalry is driven by the need to differentiate titles through advanced non-player character behaviors, a hyper-personalized narrative experience, and procedural content generation that extends player retention.

- Studios leveraging AI-driven engagement strategies see user retention rates improve by up to 25% compared to those using traditional methods. Furthermore, automated QA processes can identify critical bugs 70% faster than manual testing teams. The market has seen a clear bifurcation where companies successfully utilizing AI-driven engagement strategies command significantly higher valuation multiples.

- This evolution is supported by the institutionalization of digital and behavioral technologies as a core component of the modern gaming ecosystem, ensuring its long-term commercial viability.

We can help! Our analysts can customize this artificial intelligence (ai) in games market research report to meet your requirements.

RIA -

RIA -