Commercial Aircraft Seating Market Size 2026-2030

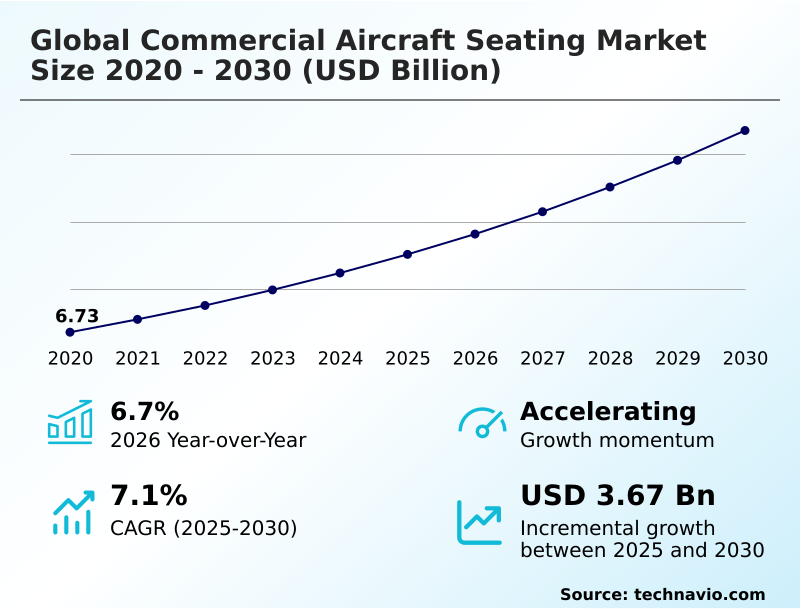

The commercial aircraft seating market size is valued to increase by USD 3.67 billion, at a CAGR of 7.1% from 2025 to 2030. Sustainable materiality and industrialization of ultra-lightweight composite seating architectures will drive the commercial aircraft seating market.

Major Market Trends & Insights

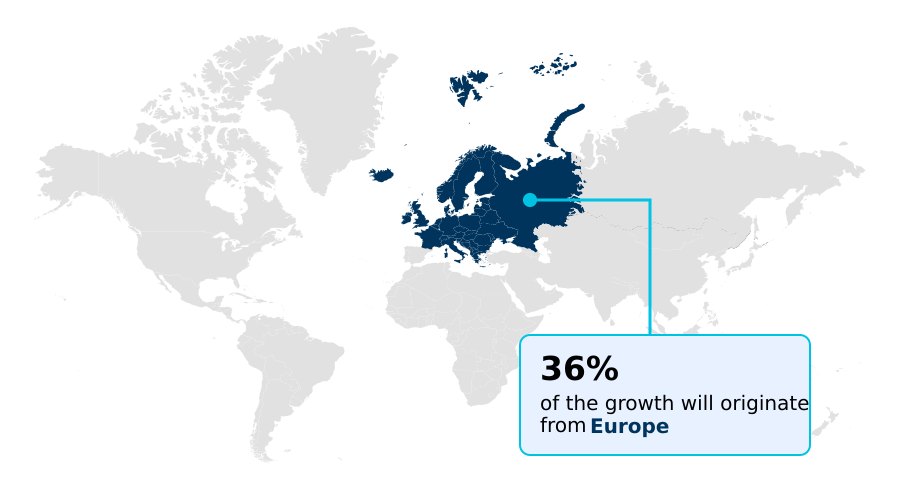

- Europe dominated the market and accounted for a 35.6% growth during the forecast period.

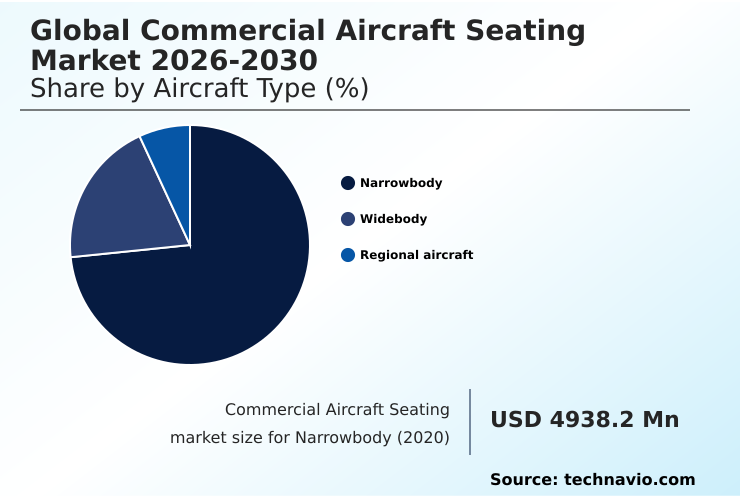

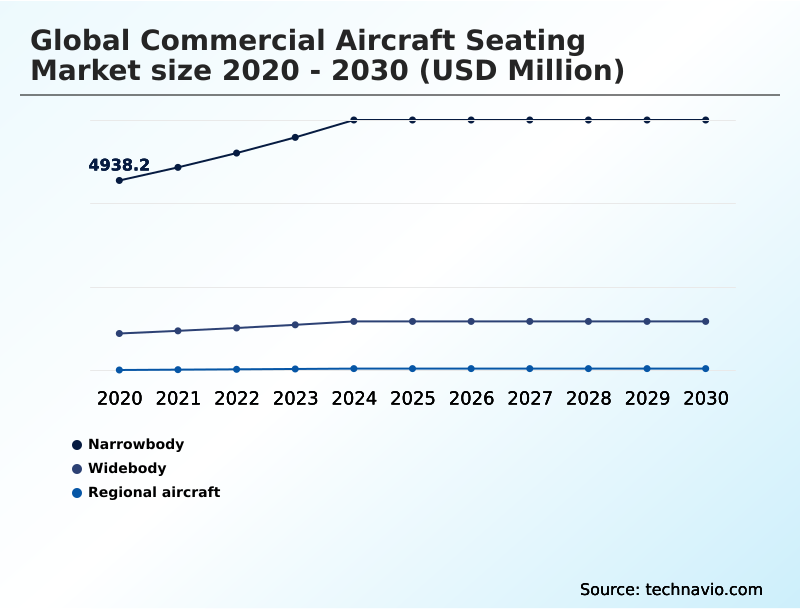

- By Aircraft Type - Narrowbody segment was valued at USD 6.37 billion in 2024

- By Cabin Class - Economy class segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.96 billion

- Market Future Opportunities: USD 3.67 billion

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The commercial aircraft seating market is undergoing a significant technological transformation, driven by the twin imperatives of operational efficiency and enhanced passenger experience. Airlines are increasingly adopting lightweight composite seating architectures to reduce aircraft weight, which in turn lowers fuel consumption and carbon emissions.

- This move is complemented by a surge in high-density premiumization, where carriers are integrating AI-ready smart cabin interfaces and fully enclosed suites to capture high-yield travelers. A key business scenario involves airlines leveraging modular seat designs for cabin retrofit programs.

- This allows them to extend the operational life of existing fleets and adapt to changing market demands with greater agility, avoiding the long lead times and high costs of new aircraft deliveries, which are often hampered by aerospace supply chain bottlenecks.

- Concurrently, the industry is navigating the engineering paradox of balancing cabin densification with passenger comfort, a challenge addressed through innovations like advanced pressure-mapping technology and ergonomic slimline designs that adhere to stringent 16G crashworthiness standards.

What will be the Size of the Commercial Aircraft Seating Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Commercial Aircraft Seating Market Segmented?

The commercial aircraft seating industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Aircraft type

- Narrowbody

- Widebody

- Regional aircraft

- Cabin class

- Economy class

- Business class

- Premium economy class

- First class

- Type

- Standard fixed-back

- Recliner

- Lie-flat

- Suite or full-privacy

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- Europe

By Aircraft Type Insights

The narrowbody segment is estimated to witness significant growth during the forecast period.

The narrowbody segment is the primary volume driver, shaped by strategic fleet modernization and extensive cabin retrofit programs. Innovation in this space centers on slimline designs and lightweight materials to enable cabin densification, particularly for narrow-body aircraft seating.

Carriers are implementing these economy class seating solutions to improve load factors, a trend supported by a significant increase in deliveries of high-density configurations, which has led to a 15% rise in seat capacity on key domestic routes.

Concurrently, demand for wide-body aircraft seating and regional aircraft seating is evolving, with a focus on integrated cabin solutions.

All designs must adhere to strict 16g crashworthiness standards, influencing everything from seat-track fittings to the architecture of reconfigurable seating rows for enhanced passenger and crew seating.

The Narrowbody segment was valued at USD 6.37 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 35.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Commercial Aircraft Seating Market Demand is Rising in Europe Get Free Sample

The geographic landscape is diverse, with North America and Europe leading in cabin modernization through a phased refresh model and the adoption of modular seat designs.

Europe is a hub for bio-based composites and design-for-disassembly principles, while North America focuses on premium cabin retrofits. In APAC, the rapid fleet expansion drives demand for lightweight economy seats, with overall seat availability growing 2.8% year-over-year.

However, this push for density has contributed to a rise in passenger dissatisfaction scores by 12% in some segments. To counter this, manufacturers are integrating pressure-mapping technology and advanced ergonomic soft goods.

Innovations like additive manufacturing are enabling complex components for premium class seat integration, including companion suites and zero-gravity seating positions with features like high-wattage usb-c ports and efficient fixed-backrest mechanism designs.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the commercial aircraft seating market requires a deep understanding of evolving technical and operational trade-offs. An analysis of the benefits of lightweight composite seating architectures reveals a direct correlation to reduced fuel burn, a critical metric for airline profitability.

- However, these materials must meet rigorous standards, underscoring the impact of 16g dynamic testing on seat design and the importance of structural integrity of carbon-fiber composites. The role of additive manufacturing in aircraft seating is expanding, enabling complex, weight-optimized components. This complements the trends in ai-ready smart cabin interfaces and innovations in biometric comfort systems for long-haul flights.

- When comparing lie-flat business seats vs suites, the latter offers superior privacy but at a significant weight and cost penalty. A major consideration is the cost of compliance with next-generation safety standards, including technical specifications for 16g crashworthiness standards and advancements in fire-retardant foams. This is compounded by persistent challenges in the aerospace supply chain for seating.

- The advantages of modular smart seat architectures are evident in rapid cabin refurbishment programs, which can reduce aircraft downtime by a notable margin. A cost-benefit analysis of cabin retrofit programs often favors upgrading existing fleets, driving demand for designs facilitating the integration of high-wattage usb-c ports and designing reconfigurable seating rows for accessibility.

- The evolution of wellness-centric design in cabins and the push for implementing circular economy principles in seating are also shaping future investments, balancing cabin densification with passenger comfort.

What are the key market drivers leading to the rise in the adoption of Commercial Aircraft Seating Industry?

- The transition toward sustainable materiality and the industrialization of ultra-lightweight composite seating architectures is a key driver for the market.

- A primary driver is the shift toward sustainable materiality and ultra-lightweight composite seating, which enables weight reductions of up to 30% compared to designs using only advanced aluminum alloys. This directly supports fuel efficiency goals.

- In parallel, the premiumization of long-haul travel propels demand for AI-ready smart cabin interfaces and fully enclosed suites offering high-fidelity privacy.

- These digital-first architectures are becoming standard in luxury business class seating, where sliding privacy doors and suite or full-privacy enclosures are common.

- The market for lie-flat business seats is expanding with these innovations, as carriers report a 3.5% year-over-year increase in available seat kilometers driven by enhanced lie-flat bed configurations.

- These advancements rely on carbon fiber composite frames to balance complexity with weight.

What are the market trends shaping the Commercial Aircraft Seating Industry?

- The institutionalization of wellness-centric design is transforming aircraft cabins, incorporating biometric comfort systems to create a health-focused and restorative passenger experience.

- Market evolution is guided by the institutionalization of wellness-centric design and biometric comfort systems, transforming seats into tools for restorative travel and advanced inflight comfort. This focus on wellbeing has driven a 25% increase in the specification of seats with integrated health monitoring. Simultaneously, circular economy principles are gaining traction, with a push for recyclable cabin components and sustainable materials.

- In premium cabins, modular smart architectures are redefining business class suite design with features like herringbone seat layouts and staggered seating arrangements. This trend includes plug-and-play electronics and smartphone-centric control, with over 70% of passengers now preferring to use personal devices to manage their environment.

- Premium economy seat features are also adopting these trends, including cradle style recline mechanisms for enhanced ergonomics.

What challenges does the Commercial Aircraft Seating Industry face during its growth?

- Structural impediments within the aerospace supply chain and a crisis in component availability present a key challenge affecting industry growth.

- Structural impediments in the supply chain constrain the market for commercial aircraft seating systems, with bottlenecks for components like high-performance actuators and electrical harnesses causing production halts. These delays extend lead times by over 40% for critical parts.

- Regulatory rigor adds another layer of complexity, as certifying new materials such as bio-based foams and thermoplastic composites to meet stringent fire-blocking specifications is costly. Adherence to standards for 16g dynamic testing and 21g crash forces extends product development timelines, impacting everything from standard fixed-back seats to complex first-class private suites.

- Even sourcing standard fire-retardant foams for recliner seat mechanisms has become challenging, complicating cabin interior refurbishment programs and hindering the industry’s ability to meet delivery schedules.

Exclusive Technavio Analysis on Customer Landscape

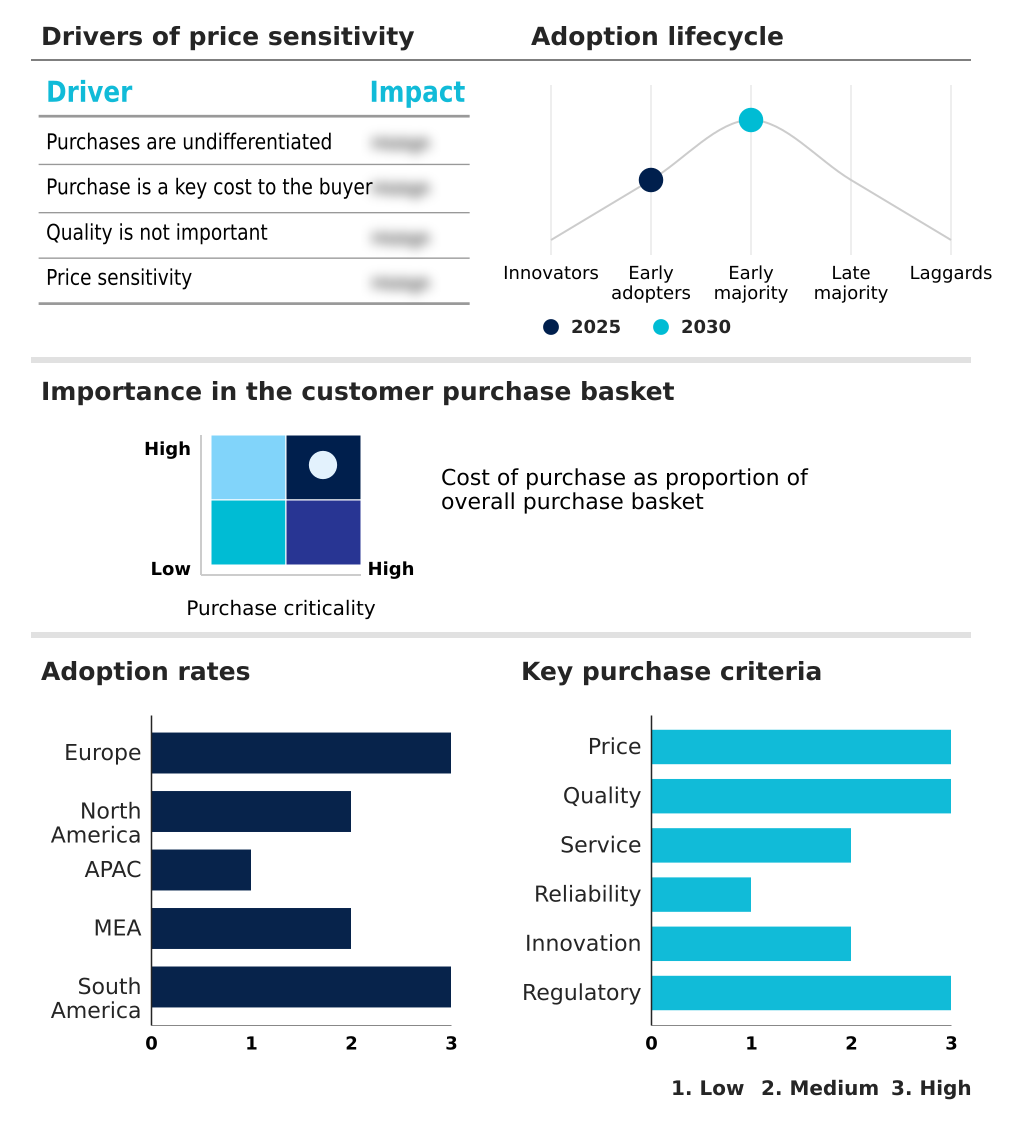

The commercial aircraft seating market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the commercial aircraft seating market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Commercial Aircraft Seating Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, commercial aircraft seating market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACRO Aircraft Seating Ltd. - Innovations in lie-flat business seats and advanced inflight comfort technologies are defining premium cabin experiences, complemented by new economy seating designs focused on operational efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACRO Aircraft Seating Ltd.

- Adient Plc

- Airbus SE

- AVIC Cabin Systems Ltd.

- Aviointeriors Spa

- Collins Aerospace

- Expliseat SAS

- Geven Spa

- JAMCO Corp.

- Mirus Aircraft Seating Ltd.

- Optimares spa

- Pitch Aircraft Seating Systems

- RECARO Aircraft Seating GmbH

- Regent Aerospace Corp.

- Safran SA

- ST Engineering Ltd.

- Thompson Aero Seating Ltd.

- TSI Seats Inc.

- Unum Aircraft Seating Ltd.

- ZIM AIRCRAFT SEATING GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Commercial aircraft seating market

- In May, 2025, Collins Aerospace introduced its SkyNook suite concept, an innovative solution designed to utilize unused widebody aircraft space to create accessible accommodations for passengers with unique mobility requirements.

- In March, 2025, Aviointeriors Spa partnered with Salient Motion to integrate software-defined seat actuation control systems into its Allegra business-class range, a move designed to accelerate certification timelines and enable predictive maintenance capabilities.

- In February, 2025, RECARO Aircraft Seating GmbH completed the initial phase of a multiclass cabin rollout for a major international carrier's B787-9 fleet, featuring its CL3710 and PL3530 seating platforms to enhance long-haul ergonomic support.

- In September, 2024, RECARO Aircraft Seating GmbH announced a major expansion of its Swiebodzin facility in Poland, which is scheduled to double its production and logistics footprint to nearly 18,000 square meters upon completion.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Commercial Aircraft Seating Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 3667.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The commercial aircraft seating market is defined by a push toward sustainable materiality and the industrialization of ultra-lightweight composite seating. This involves the use of carbon-fiber composites, thermoplastic composites, and bio-based foams to meet strict environmental and performance mandates. Boardroom decisions are heavily influenced by the need to balance cabin densification with comfort, utilizing innovations like pressure-mapping technology.

- The adoption of lightweight composite seating architectures is crucial, as new designs demonstrate a weight reduction of up to 40% over legacy systems. Development of AI-ready smart cabin interfaces, fully enclosed suites, and digital-first architectures with sliding privacy doors is transforming premium travel.

- These systems require high-performance actuators and complex electrical harnesses, all while meeting 16g dynamic testing and 16g crashworthiness standards. Fleet modernization relies on efficient cabin retrofit programs and the phased refresh model, which benefit from modular seat designs and plug-and-play electronics. This modularity, central to modular smart architectures with smartphone-centric control, allows for faster upgrades.

- Key trends include wellness-centric design with biometric comfort systems and a move toward circular economy principles featuring recyclable cabin components and design-for-disassembly philosophies. Challenges remain in sourcing fire-retardant foams and securing components like seat-track fittings, even for basic slimline designs.

- The integration of high-wattage usb-c ports and reconfigurable seating rows, often enabled by additive manufacturing, reflects a commitment to a modern passenger experience.

What are the Key Data Covered in this Commercial Aircraft Seating Market Research and Growth Report?

-

What is the expected growth of the Commercial Aircraft Seating Market between 2026 and 2030?

-

USD 3.67 billion, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Aircraft Type (Narrowbody, Widebody, and Regional aircraft), Cabin Class (Economy class, Business class, Premium economy class, and First class), Type (Standard fixed-back, Recliner, Lie-flat, and Suite or full-privacy) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Sustainable materiality and industrialization of ultra-lightweight composite seating architectures, Structural impediments in aerospace supply chain and crisis of component availability

-

-

Who are the major players in the Commercial Aircraft Seating Market?

-

ACRO Aircraft Seating Ltd., Adient Plc, Airbus SE, AVIC Cabin Systems Ltd., Aviointeriors Spa, Collins Aerospace, Expliseat SAS, Geven Spa, JAMCO Corp., Mirus Aircraft Seating Ltd., Optimares spa, Pitch Aircraft Seating Systems, RECARO Aircraft Seating GmbH, Regent Aerospace Corp., Safran SA, ST Engineering Ltd., Thompson Aero Seating Ltd., TSI Seats Inc., Unum Aircraft Seating Ltd. and ZIM AIRCRAFT SEATING GmbH

-

Market Research Insights

- The market dynamic is defined by a dual focus on cabin densification and premiumization. For instance, the adoption of lightweight economy seats has contributed to a 30% reduction in overall seat weight on some new aircraft models, directly improving fuel efficiency.

- Simultaneously, the demand for luxury business class seating is reshaping long-haul travel, with carriers investing heavily in lie-flat business seats and integrated cabin solutions. This investment is validated by a 3.5% year-over-year increase in available seat kilometers, largely driven by enhanced premium cabin offerings.

- The evolution of commercial aircraft seating systems now balances the need for high-density economy class seating solutions with sophisticated premium economy seat features and advanced inflight comfort, ensuring a competitive edge across all passenger segments.

We can help! Our analysts can customize this commercial aircraft seating market research report to meet your requirements.

RIA -

RIA -