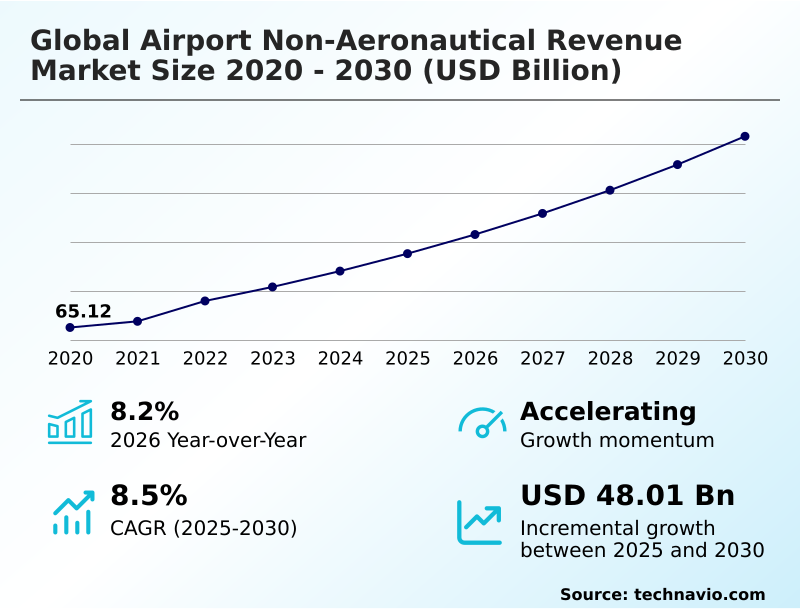

Airport Non-aeronautical Revenue Market Size 2026-2030

The airport non-aeronautical revenue market size is valued to increase by USD 48.01 billion, at a CAGR of 8.5% from 2025 to 2030. Rising passenger traffic and global connectivity will drive the airport non-aeronautical revenue market.

Major Market Trends & Insights

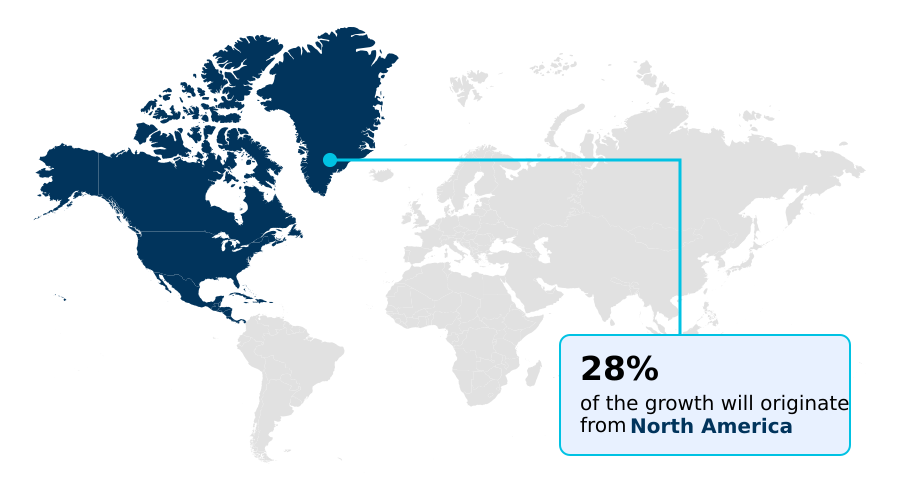

- North America dominated the market and accounted for a 28.4% growth during the forecast period.

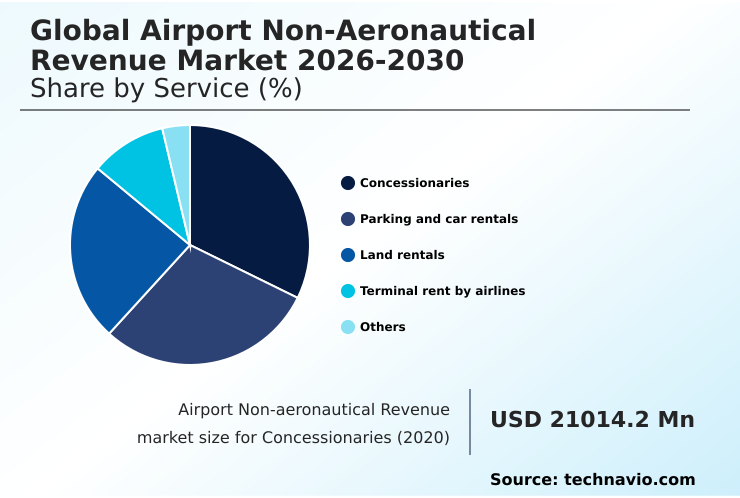

- By Service - Concessionaries segment was valued at USD 28.54 billion in 2024

- By Business Segment - Commercial development segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 78.21 billion

- Market Future Opportunities: USD 48.01 billion

- CAGR from 2025 to 2030 : 8.5%

Market Summary

- The airport non-aeronautical revenue market is undergoing a fundamental transformation, evolving from a focus on operational efficiency to a strategy centered on commercial optimization. This shift is propelled by the need to diversify income beyond traditional aviation charges. Key drivers include rising global passenger volumes and the strategic premiumization of services, which turns terminals into destinations.

- Trends such as digitalization are reshaping the passenger experience, with operators leveraging data analytics and omnichannel platforms to enhance engagement and capture greater spend. For instance, an operator facing declining discretionary purchases might use real-time analytics to adjust its retail mix and launch targeted promotions for food and beverage outlets, protecting concession revenue.

- However, the market faces challenges from economic volatility impacting consumer spending and the high capital investment required for digital transformation. Success hinges on creating a seamless, high-value commercial environment that maximizes revenue from every stage of the passenger journey, from smart parking systems to experiential duty-free retail.

What will be the Size of the Airport Non-aeronautical Revenue Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Airport Non-aeronautical Revenue Market Segmented?

The airport non-aeronautical revenue industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

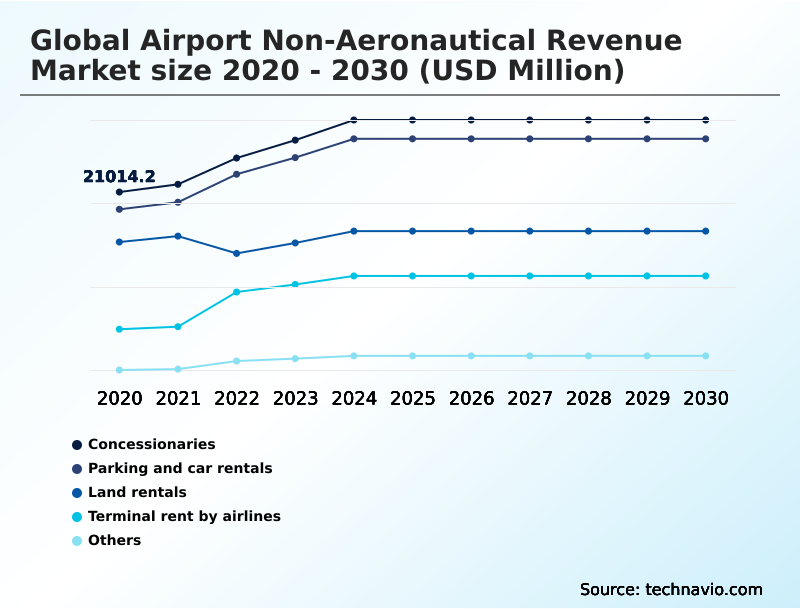

- Service

- Concessionaries

- Parking and car rentals

- Land rentals

- Terminal rent by airlines

- Others

- Business segment

- Commercial development

- Advertising

- Type

- Large airports

- Medium airports

- Small airports

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Service Insights

The concessionaries segment is estimated to witness significant growth during the forecast period.

The concessionaries segment is central to airport commercial management, generating substantial income from duty-free retail and food and beverage concessions.

A successful premiumization strategy is key to maximizing airport retail, with a focus on experiential luxury to enhance the passenger-centric retail journey.

This approach significantly boosts non-aviation revenue growth, with some operators reporting a 31% surge in income from premium airport hospitality services alone.

Such performance, which maximizes passenger dwell time monetization, underscores the segment's critical role in overall airport financial performance, demonstrating a clear shift from transit functionality to comprehensive commercial destination.

The Concessionaries segment was valued at USD 28.54 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 28.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Airport Non-aeronautical Revenue Market Demand is Rising in North America Get Free Sample

The geographic landscape is dynamic, with North America leading incremental growth, projected to contribute over 28% of the total, driven by modernization and the optimization of smart parking systems.

APAC follows closely, accounting for nearly 28% of the opportunity, fueled by demand for premium airside retail and robust real estate leasing activities.

Operators in Europe focus on maximizing ancillary revenue streams by securing strong airport concession agreements for high-value retail. In the Middle East, the focus on premium services is boosting VIP services income.

Across all regions, optimizing terminal space and enhancing airport ancillary services through effective airport parking management are critical strategies for growth.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Operators are now focused on holistic strategies for increasing non-aeronautical revenue, moving beyond isolated initiatives. The impact of e-commerce on airport retail has forced a re-evaluation of in-terminal sales, highlighting the critical role of technology in airport commercial services. To compete, airports are integrating digital platforms for passenger shopping, which enhances the customer experience and provides valuable data.

- The roi of digital transformation in airports is becoming clearer, as leveraging big data for airport retail personalization can lift conversion rates by double-digit percentages, far exceeding gains from traditional promotions. This focus extends to premiumization trends in airport lounges and optimizing food and beverage offerings in terminals.

- Concurrently, the long-term airport city and aerotropolis model benefits are being realized through the future of airport real estate development and maximizing advertising income in airports. However, challenges in managing airport concession contracts persist. Evaluating commercial performance of airport terminals now requires sophisticated non-aeronautical revenue per passenger metrics.

- This includes addressing the impact of ride-sharing on airport ground transport revenue and exploring how to improve airport parking revenue through smart, convenient solutions. The emphasis on sustainability in airport commercial operations is also influencing decisions, as the customer experience impact on non-aeronautical spend becomes a key performance indicator.

What are the key market drivers leading to the rise in the adoption of Airport Non-aeronautical Revenue Industry?

- Sustained growth in passenger traffic, coupled with expanding global connectivity, serves as the primary driver for the market.

- Sustained growth in passenger volumes is a primary driver, directly increasing non-aeronautical income sources and opportunities for passenger dwell time monetization. This allows for greater airport commercial development and commercial portfolio diversification.

- Operators are leveraging traffic to increase concession revenue and overall passenger spend through enhanced offerings. For example, a 3.4% rise in passenger movements can directly support initiatives for improving passenger spend.

- Furthermore, a focus on premium services like lounge access monetization can yield disproportionate returns, with some operators seeing a 31% income surge in this area alone. Advanced airport retail analytics are crucial for identifying and capitalizing on these high-margin opportunities.

What are the market trends shaping the Airport Non-aeronautical Revenue Industry?

- A key market trend is the expansion of the airport city and aerotropolis model. This strategic development transforms airports into self-sustaining economic zones with integrated commercial functions.

- Key market trends include the expansion of the aerotropolis development model and the adoption of omnichannel retail. The airport city concept is evolving through strategic airport real estate strategy, transforming airport land into integrated airport business parks. Simultaneously, the digital airport experience is being redefined with digital commerce platforms that enable click-and-collect services, improving passenger journey mapping and convenience.

- The success of this integrated approach is evident, with some new retail concepts driving segment revenue up by over 12%. Effective airport retail design and strong airport concession agreements are foundational to capitalizing on these shifts.

What challenges does the Airport Non-aeronautical Revenue Industry face during its growth?

- Economic pressures and related shifts in consumer spending behavior present a key challenge to the industry's growth trajectory.

- Economic volatility poses a significant challenge, impacting discretionary spending on landside services and in-terminal purchases, which affects non-flight related income. Operators face pressure on ground transportation fees and car rental concessions from new mobility solutions. The digital shift challenges traditional airport advertising models, with some hubs seeing retail revenue grow by only 2.5% while noting weakness in legacy advertising.

- This necessitates new terminal commercial planning and innovative airport services to maintain the value of terminal real estate. For commercial airport operations to remain profitable, they must adapt to these pressures on key streams like advertising revenue.

Exclusive Technavio Analysis on Customer Landscape

The airport non-aeronautical revenue market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the airport non-aeronautical revenue market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Airport Non-aeronautical Revenue Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, airport non-aeronautical revenue market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aena S.M.E. SA - Offers a diversified portfolio of non-aeronautical revenue streams, including premier duty-free retail and integrated commercial services to enhance airport profitability and passenger experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aena S.M.E. SA

- Aeroports de Paris SA

- Airports of Thailand PCL

- Changi Airport Group Pte. Ltd.

- Copenhagen Airports AS

- Dubai Airports Co.

- Flughafen Munchen GmbH

- Flughafen Zurich AG

- Fraport AG

- GMR Airports Infrastructure Ltd.

- Heathrow Airport Holdings Ltd.

- IGA Istanbul Airport

- Japan Airport Terminal Co. Ltd.

- Korea Airports Corp.

- Malaysia Airports Holdings

- Royal Schiphol Group N.V.

- Sydney Airport Corp. Ltd.

- Vancouver Airport Authority

- Vinci SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Airport non-aeronautical revenue market

- In August 2025, Corporacion America Airports reported its consolidated revenues for the second quarter grew 18.9%, driven by a 22% rise in commercial revenues that outpaced aeronautical segment growth.

- In July 2025, GMR Airports concluded the acquisition of a 70% stake in a logistics park entity to strengthen its airport-based industrial and warehousing portfolio as part of its aerotropolis strategy.

- In May 2025, GMR Airports reported a consolidated loss for the fourth quarter of its 2024 fiscal year, citing that a delayed tariff order from the regulatory authority significantly impacted its financial performance.

- In March 2025, Changi Airport Group reported that its concession revenue growth remained subdued despite reaching a record 68.4 million passenger movements, citing global economic uncertainties impacting consumer spending.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Airport Non-aeronautical Revenue Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.5% |

| Market growth 2026-2030 | USD 48005.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.2% |

| Key countries | China, Japan, India, Australia, Singapore, Indonesia, US, Canada, Mexico, UK, Germany, France, Spain, Italy, The Netherlands, UAE, Saudi Arabia, Qatar, South Africa, Egypt, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The strategic importance of non-aeronautical revenue has intensified, compelling a shift toward comprehensive commercial portfolio diversification. Operators are focused on maximizing income from every asset, including terminal real estate and landside services. The premiumization strategy is central, involving investments in experiential luxury offerings to generate VIP services income.

- A key area is optimizing airside retail, particularly duty-free retail and food and beverage concessions, where one operator recently achieved a 23% revenue rise. The airport city concept and broader aerotropolis development are gaining traction, supported by real estate leasing. Digital transformation is also critical, enabling omnichannel retail through digital commerce platforms and facilitating click-and-collect services.

- This extends to operations, with smart parking systems enhancing revenue from ground transportation fees and car rental concessions. Ultimately, these ancillary revenue streams, including advertising revenue and lounge access monetization, are vital for increasing overall passenger spend and creating a passenger-centric retail environment.

What are the Key Data Covered in this Airport Non-aeronautical Revenue Market Research and Growth Report?

-

What is the expected growth of the Airport Non-aeronautical Revenue Market between 2026 and 2030?

-

USD 48.01 billion, at a CAGR of 8.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Service (Concessionaries, Parking and car rentals, Land rentals, Terminal rent by airlines, and Others), Business Segment (Commercial development, and Advertising), Type (Large airports, Medium airports, and Small airports) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising passenger traffic and global connectivity, Economic pressure and consumer spending shifts

-

-

Who are the major players in the Airport Non-aeronautical Revenue Market?

-

Aena S.M.E. SA, Aeroports de Paris SA, Airports of Thailand PCL, Changi Airport Group Pte. Ltd., Copenhagen Airports AS, Dubai Airports Co., Flughafen Munchen GmbH, Flughafen Zurich AG, Fraport AG, GMR Airports Infrastructure Ltd., Heathrow Airport Holdings Ltd., IGA Istanbul Airport, Japan Airport Terminal Co. Ltd., Korea Airports Corp., Malaysia Airports Holdings, Royal Schiphol Group N.V., Sydney Airport Corp. Ltd., Vancouver Airport Authority and Vinci SA

-

Market Research Insights

- The market's dynamics are shifting toward airport commercial development, with operators focusing on innovative airport services to drive profitability. Strategic airport commercial planning is essential, as some operators achieve commercial revenue growth of 11% that significantly outpaces passenger traffic increases. Success in non-aviation revenue growth is increasingly tied to optimizing terminal space and enhancing the digital airport experience.

- For instance, a focus on premium services can lead to a 31% surge in income from that segment, demonstrating the high ROI of targeted airport hospitality services. This data-driven approach to passenger journey mapping and improving passenger spend is central to maintaining financial resilience.

We can help! Our analysts can customize this airport non-aeronautical revenue market research report to meet your requirements.

RIA -

RIA -