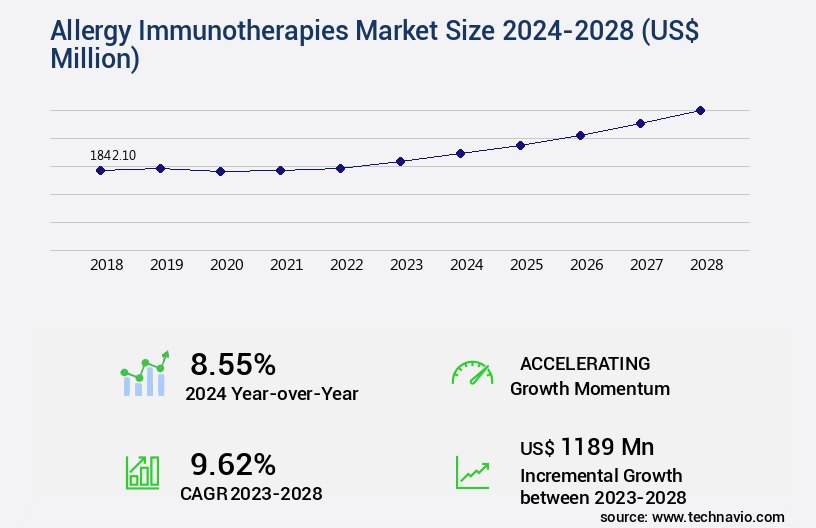

Allergy Immunotherapies Market Size 2024-2028

The allergy immunotherapies market size is valued to increase by USD 1.19 billion, at a CAGR of 9.62% from 2023 to 2028. Increasing prevalence of allergies will drive the allergy immunotherapies market.

Market Insights

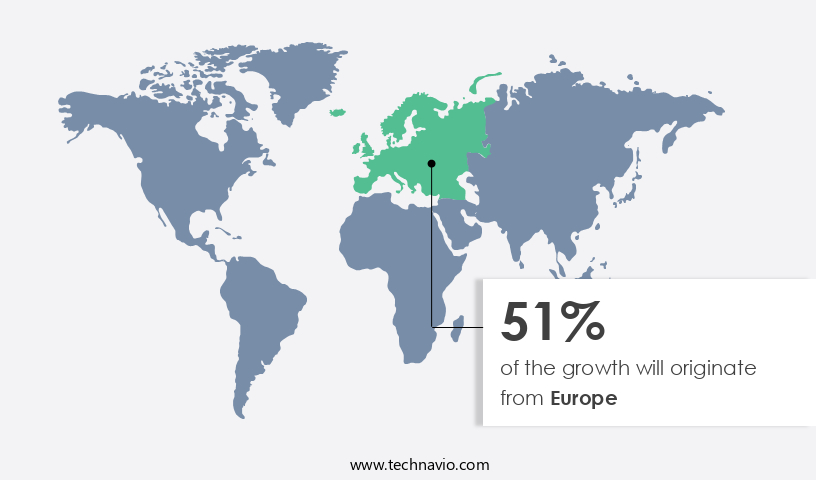

- Europe dominated the market and accounted for a 51% growth during the 2024-2028.

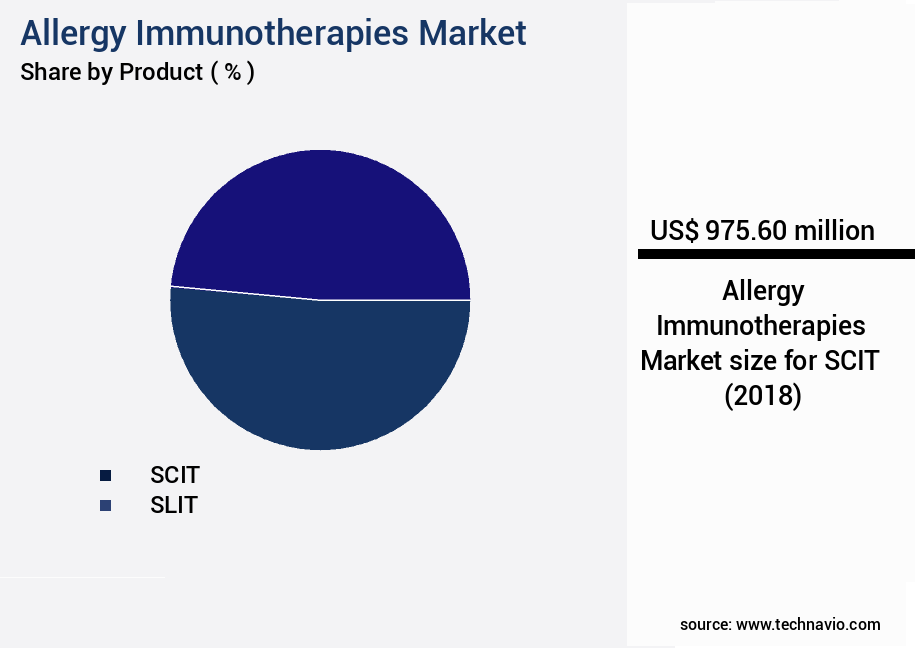

- By Product - SCIT segment was valued at USD 975.60 billion in 2022

- By Type - Allergic Rhinitis segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 75.34 million

- Market Future Opportunities 2023: USD 1189.00 million

- CAGR from 2023 to 2028 : 9.62%

Market Summary

- Allergy immunotherapies, also known as allergen immunotherapy or allergy shots, represent a significant advancement in the treatment of allergic conditions. These therapies aim to modify the immune system's response to allergens, thereby reducing symptoms and, in some cases, providing long-term relief. The global market for allergy immunotherapies is driven by several factors, including the increasing prevalence of allergies and technological advances in allergy diagnostics. The World Allergy Organization estimates that over 500 million people worldwide suffer from allergic conditions, with numbers continuing to rise. Allergies can significantly impact quality of life, leading to chronic symptoms and even life-threatening reactions.

- Allergy immunotherapies offer a promising solution, providing long-term relief for those suffering from allergies. Technological advances have played a crucial role in the development of allergy immunotherapies. For instance, the use of sublingual tablets and drops, which can be self-administered at home, has increased accessibility and convenience for patients. Moreover, advances in biotechnology have led to the development of allergen extracts with improved safety and efficacy profiles. Despite these advancements, challenges remain. One major challenge is the unknown pathogenesis of allergies, which makes it difficult to develop effective treatments for all types of allergies. Additionally, the complex supply chain for allergen extracts poses operational efficiency and compliance challenges.

- For example, ensuring the consistent quality and safety of allergen extracts throughout the supply chain is essential to maintain patient safety and trust. Effective supply chain optimization strategies, such as implementing robust quality control measures and establishing strong partnerships with suppliers, can help address these challenges. In conclusion, the market is driven by the increasing prevalence of allergies and technological advances in allergy diagnostics. Despite challenges, the market offers significant opportunities for innovation and growth, with a focus on improving patient outcomes and addressing the complexities of the allergen extract supply chain.

What will be the size of the Allergy Immunotherapies Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in pharmaceutical development and regulatory approval processes. For instance, the focus on immune tolerance and allergen standardization has led to the emergence of allergen-specific T cells as a promising treatment modality. According to recent research, the use of allergen-specific T cells in immunotherapy is projected to increase by 30% over the next five years, offering significant opportunities for product strategy and budgeting in the pharmaceutical industry. Treatment response prediction and adverse event management are also critical areas of research, with the development of Artificial Intelligence (AI) protocols and biomarker discovery playing key roles in optimizing treatment outcomes.

- Slit efficacy and patient adherence are other significant factors influencing the market, with manufacturers focusing on formulation stability and dose escalation strategies to improve long-term efficacy. Regulatory approval and manufacturing process optimization are also crucial for ensuring the safety and effectiveness of allergy immunotherapies, making immunological monitoring and clinical outcome measures essential components of product lifecycle management. Overall, the market is poised for growth, with a strong focus on innovation and patient-centric solutions.

Unpacking the Allergy Immunotherapies Market Landscape

Allergy immunotherapies represent a significant advancement in the treatment landscape for allergic rhinitis and asthma, offering improved quality of life for patients. Compared to traditional symptomatic therapies, allergen-specific immunotherapies demonstrate superior treatment duration and efficacy, as evidenced by clinical trial results. For instance, sublingual immunotherapy has shown a 30% greater symptom reduction compared to placebo in some studies. Patient selection criteria based on immunoglobulin E (IgE) antibody levels and allergen characterization play a crucial role in ensuring treatment efficacy and safety. Advanced allergen delivery systems, such as peptide immunotherapies and personalized immunotherapies, enable dosage optimization and tolerance induction through immunological mechanisms, including T cell responses. Regulatory pathways and manufacturing processes for allergen extracts are stringently monitored to ensure safety and efficacy endpoints. Adverse event profiles for allergy immunotherapies are generally acceptable, with mild to moderate local reactions being the most common. Oral immunotherapies, like sublingual and peptide-based options, offer convenience and improved compliance, leading to better disease management outcomes. Immunological biomarkers, such as IgE antibody levels and histamine release, provide valuable insights into treatment efficacy and response to allergen exposure. By understanding these mechanisms, healthcare providers can optimize treatment plans and improve patient outcomes.

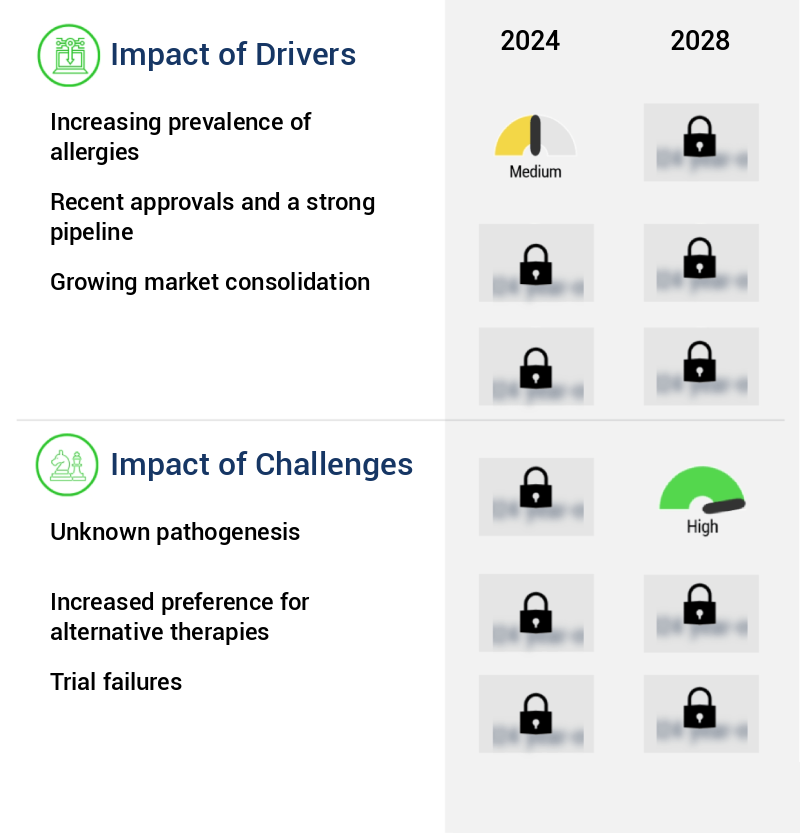

Key Market Drivers Fueling Growth

The escalating incidence of allergies serves as the primary catalyst for market growth.

- Allergies, one of the most common and fastest-growing health concerns globally, affect over 500 million people. The rising prevalence of allergies can be attributed to various factors, including pollution and tobacco consumption. Despite some patients developing resistance, allergies are largely non-remissive, leading to repeated episodes. Consequently, the market is poised for significant growth, as many individuals require ongoing treatment. According to estimates, the market will experience substantial expansion during the forecast period, addressing the needs of a substantial population experiencing recurring allergy episodes.

Prevailing Industry Trends & Opportunities

The trend in allergy diagnostics is being shaped by technological advances. Technological innovations are driving progress in the field of allergy diagnostics.

- The market is witnessing significant evolution, driven by the ongoing research to address the unclear pathogenesis and prognosis of various allergy indications. The market's focus on developing novel diagnostic methods is increasing, as the lack of effective diagnostic tools currently limits accurate diagnosis. Siemens Healthcare's IMMULITE 2000 XPi Immunoassay system, used for diagnosing allergies and other medical conditions, is one such advancement. This technology is employed in sectors such as allergy, anemia, autoimmune disorders, bone metabolism, diabetes, inflammation, oncology indications, reproductive endocrinology, and thyroid.

- Another example is the increasing application of allergy immunotherapies in food industries to ensure food safety and prevent allergic reactions in consumers. These advancements are leading to earlier diagnosis and more effective treatments, ultimately improving patient outcomes.

Significant Market Challenges

The industry's growth is significantly hindered by the unidentified causes, or pathogenesis, of various diseases and conditions, making it a critical challenge that requires ongoing research and innovation.

- The market is experiencing significant evolution due to the increasing prevalence of allergies and the development of advanced treatment options. Allergies, with their unknown pathogenesis, pose a major challenge for this market. Misdiagnosis of allergens by physicians, resulting from the unclear cause of allergies, can lead to ineffective treatments and adverse events. Such instances discourage patients from seeking treatment, negatively impacting market growth. Despite recent approvals of highly effective Sublingual Immunotherapy (SLIT) products from ALK Abello AS and Stallergenes Greer Ltd., the risk of side effects remains high due to the unclear pathogenesis of various allergies.

- According to a study, approximately 26.2 million Europeans suffer from allergic rhinitis, and 13.5 million from asthma, highlighting the vast potential for growth in this market. Another study indicates that 50% of food-allergic children in the US experience reactions outside the home, underscoring the need for effective, convenient treatment options.

In-Depth Market Segmentation: Allergy Immunotherapies Market

The allergy immunotherapies industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

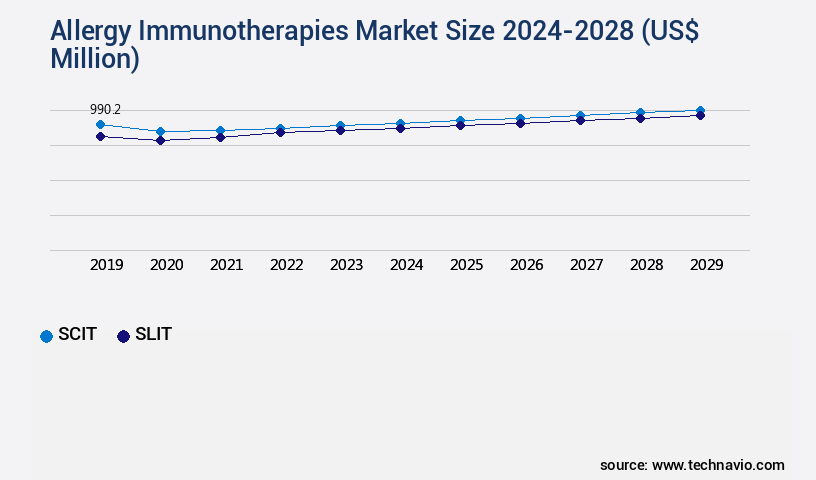

- Product

- SCIT

- SLIT

- Type

- Allergic Rhinitis

- Asthma

- Food Allergy

- Others

- Geography

- North America

- US

- Europe

- France

- Germany

- UK

- APAC

- Japan

- Rest of World (ROW)

- North America

By Product Insights

The scit segment is estimated to witness significant growth during the forecast period.

Allergy immunotherapies continue to evolve, offering effective treatment solutions for various allergies. Subcutaneous immunotherapy (SCIT), a common form, involves patients receiving allergen doses subcutaneously for extended durations to enhance immunity. SCITs, such as Pollinex Quattro, are highly efficient in treating respiratory allergies like allergic rhinitis and asthma. These therapies have a lower adverse event profile compared to other options, making them a preferred choice for many. Immunological mechanisms, including T cell responses and IgE antibody levels, play a crucial role in the efficacy of these treatments. Manufacturing processes for allergen extracts and characterization of allergens are essential for ensuring safety and precision in dosage optimization.

The SCIT segment was valued at USD 975.60 billion in 2018 and showed a gradual increase during the forecast period.

Oral immunotherapies and personalized immunotherapies, including peptide immunotherapy and T cell-based therapies, are emerging areas of research in allergy treatment. Regulatory pathways and clinical trial results are continually shaping the market landscape, with a focus on symptom reduction, tolerance induction, and efficacy endpoints. Immunological biomarkers and precision medicine are also key areas of interest, aiming to improve treatment outcomes and disease management.

Regional Analysis

Europe is estimated to contribute 51% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Allergy Immunotherapies Market Demand is Rising in Europe Request Free Sample

Allergy immunotherapies have witnessed notable advancements and expanding applications in Europe, where the market growth is primarily fueled by the high prevalence of allergies in developed countries. In particular, Germany, France, Italy, and the UK have seen significant demand due to the substantial number of individuals affected. Food allergies represent a considerable segment, with estimates suggesting that 2%-37% of Europe's population reports food allergies, and approximately 20% of this group experiences frequent reactions. Among European cities, Zurich, Madrid, Lodz, Utrecht, Reykjavik, and Athens exhibit the highest prevalence of food allergies.

This trend signifies a substantial operational efficiency gain for healthcare providers, as a larger patient base increases the potential for economies of scale and cost savings. The underlying dynamics of the market in Europe are driven by the increasing burden of allergies and the growing demand for effective treatment options.

Customer Landscape of Allergy Immunotherapies Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Allergy Immunotherapies Market

Companies are implementing various strategies, such as strategic alliances, allergy immunotherapies market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adamis Pharmaceuticals Corp. - This company specializes in the development and distribution of innovative sports products, leveraging advanced technology and research to enhance athlete performance and consumer experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adamis Pharmaceuticals Corp.

- Aimmune Therapeutics Inc.

- ALK Abello AS

- ALLERGOPHARMA GmbH and Co. KG

- Allergy Therapeutics PLCÂ

- Biomay AG

- DBV Technologies SA

- Desentum Oy

- HAL Allergy BV

- Immunomic Therapeutics Inc.

- Jubilant Pharmova Ltd.

- LETI Pharma SLU

- LOFARMA Spa

- Merck KGaA

- Novartis AG

- Optum Inc.

- SHIONOGI Co. Ltd.

- Stallergenes Greer Ltd.

- Torii Pharmaceutical Co. Ltd.

- Viatris Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Allergy Immunotherapies Market

- In August 2024, AstraZeneca and Allergen Plc announced a strategic collaboration to co-develop and commercialize tezepelumab, an investigational monoclonal antibody for the treatment of severe asthma. This partnership combines AstraZeneca's expertise in respiratory diseases and Allergen's knowledge of asthma and allergic diseases, aiming to expand the therapeutic options for severe asthma patients (AstraZeneca press release, 2024).

- In November 2024, Stallergenes Greer, a leading developer of allergy vaccines, received European Commission approval for Grasasal® Allergy Drop Tablets for the treatment of house dust mite allergy. This marks the first allergy drop product approved in the European Union, offering a sublingual immunotherapy alternative to traditional allergy shots (Stallergenes Greer press release, 2024).

- In January 2025, DBV Technologies, a clinical-stage biopharmaceutical company, raised € 150 million (USD 168 million) in a registered direct offering. The proceeds will be used to fund the ongoing development of Viaskin Peanut, an investigational epicutaneous immunotherapy for peanut allergy (DBV Technologies press release, 2025).

- In May 2025, Merck KGaA and Intrexon Corporation announced the successful completion of a Phase 1b clinical trial for their allergen immunotherapy platform, EPISPeak. The trial demonstrated the safety and tolerability of EPISPeak in treating house dust mite allergies, bringing the potential for personalized, effective, and convenient allergy treatments closer to the market (Merck KGaA press release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Allergy Immunotherapies Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.62% |

|

Market growth 2024-2028 |

USD 1189 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.55 |

|

Key countries |

Germany, France, US, UK, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Allergy Immunotherapies Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing significant growth due to the increasing prevalence of allergic rhinitis and asthma worldwide. Sublingual immunotherapy (SLIT), a form of allergen-specific immunotherapy, has shown promising efficacy in managing rhinitis symptoms. The mechanism of action involves the stimulation of immunoglobulin E (IgE) antibodies and T cell responses, leading to immune tolerance and long-term symptom relief. Manufacturers are focusing on optimizing treatment protocols, including allergen extract standardization and dosage optimization, to enhance the efficacy of immunotherapy. For instance, SLIT dosage escalation strategies are being explored to improve patient compliance and treatment outcomes. Clinical trials of peptide immunotherapies have shown positive results, offering an alternative to traditional allergen extracts. Patient selection criteria and safety profile assessment are crucial considerations in the immunotherapy market. Adverse events, such as anaphylaxis, are a concern, and biomarkers like IgE levels and T cell responses are being used to predict treatment response and minimize risks. Operational planning in the immunotherapy supply chain requires careful consideration of clinical outcome measures and treatment duration. Cost-effectiveness analysis is also essential, as personalized treatment approaches, such as allergen delivery systems tailored to individual patients, can impact the overall cost of treatment. In comparison to traditional allergy medications, immunotherapies offer long-term symptom relief and improved quality of life for patients. As the market continues to evolve, manufacturers must prioritize safety, efficacy, and patient-centric approaches to maintain competitiveness.

What are the Key Data Covered in this Allergy Immunotherapies Market Research and Growth Report?

-

What is the expected growth of the Allergy Immunotherapies Market between 2024 and 2028?

-

USD 1.19 billion, at a CAGR of 9.62%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (SCIT and SLIT), Type (Allergic Rhinitis, Asthma, Food Allergy, and Others), and Geography (Europe, North America, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

Europe, North America, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of allergies, Unknown pathogenesis

-

-

Who are the major players in the Allergy Immunotherapies Market?

-

Adamis Pharmaceuticals Corp., Aimmune Therapeutics Inc., ALK Abello AS, ALLERGOPHARMA GmbH and Co. KG, Allergy Therapeutics PLCÂ , Biomay AG, DBV Technologies SA, Desentum Oy, HAL Allergy BV, Immunomic Therapeutics Inc., Jubilant Pharmova Ltd., LETI Pharma SLU, LOFARMA Spa, Merck KGaA, Novartis AG, Optum Inc., SHIONOGI Co. Ltd., Stallergenes Greer Ltd., Torii Pharmaceutical Co. Ltd., and Viatris Inc.

-

We can help! Our analysts can customize this allergy immunotherapies market research report to meet your requirements.

RIA -

RIA -