Enjoy complimentary customisation on priority with our Enterprise License!

The Aluminum Scrap Recycling Market size is estimated to increase by USD 2.99 billion, growing at a CAGR of 8.9% between 2022 and 2027. The surge in aluminum usage within the automotive sector emerges as a pivotal catalyst propelling market expansion. With the industry gravitating towards aluminum due to its advantageous attributes, such as bolstering fuel efficiency, curbing emissions, and elevating vehicle performance, the demand for this versatile metal escalates. Its widespread integration throughout vehicle manufacturing, spanning from high-end automobiles to mass-market models, augments durability and safety while concurrently trimming weight and fortifying resilience against dents. This shift underscores a transformative trend reshaping automotive engineering paradigms, where aluminum emerges as a cornerstone material driving innovation and sustainability across the automotive landscape.

To learn more about this report, Request Free Sample

It refers to the process in which scrap is recycled for reuse in a range of applications and products. The process of recycling involves remelting to produce secondary aluminum.

In the market, the surge in demand for sustainable practices and resource conservation drives growth. Aluminum scrap recycling market players like Guidetti, Glencore, and China Metal Recycling lead the charge in recycling scrap aluminum, contributing to reduced environmental impact and resource depletion. However, challenges such as efficient sorting, purifying, and solidifying processes persist, requiring continuous innovation. Trends like advancements in sorting technology and collaboration among industry players further shape the landscape, paving the way for enhanced efficiency and profitability in aluminum scrap recycling.

The surge in aluminum utilization within the automotive sector emerges as a pivotal force energizing market expansion. With the automobile industry increasingly favoring aluminum, propelled by its advantageous traits in enhancing fuel efficiency, curbing emissions, and augmenting overall vehicle performance, the demand for this versatile metal escalates. Its incorporation across vehicle manufacturing, spanning from high-end automobiles to mass-produced models, amplifies durability and safety while concurrently reducing weight and bolstering resistance against dents.

Furthermore, automakers are actively embracing secondary aluminum to address environmental concerns associated with global warming, leveraging innovative techniques such as solid-state recycling and LIBS. Government initiatives aimed at promoting electric vehicles manifested through subsidies in key markets like India and Germany, add further impetus to the demand. Notably, expansions by automotive giants like Toyota, evidenced by investments in U.S. production facilities, are poised to intensify demand dynamics throughout the forecast horizon.

Advancements in furnaces used is a key trend shaping the market. The global market has seen improvements in the type of furnaces used for melting. These advanced furnaces are tailored to the type, quality, and condition of the scrap being recycled. One such furnace is the tilting barrel furnace, which is used for melting foundry castings, scrap die castings, and trimmings from the casting process.

Another type is the multi-chamber furnace, designed to address the physical properties of the being recycled. These advancements in furnace technology are expected to enhance the efficiency of the process, driving the growth of the global in the forecast period.

Environmental issues related to recycling is a major challenge hindering the market growth. While recycling requires only 5% of the energy needed for primary production, it comes with environmental challenges. The recycling process produces toxic chemicals released into the air and generates a hazardous waste called dross. Proper containment of dross is necessary to prevent groundwater contamination.

Moreover, the process involves energy-intensive machines running on fossil fuels, contributing to air pollution with toxic gases and particulate matter. Inhaling these pollutants can lead to health issues. The lack of advanced technologies for dross recovery also hinders the market. These environmental concerns pose a threat during the forecast period.

The market research report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Customer Landscape

In the dynamic realm of market, segmentation is essential for effectively addressing the diverse facets of this thriving industry. From harnessing the abundant resource of Earth's crust to leveraging the innate properties of aluminum (Al) such as malleability and ductility, key players like Guidetti, Glencore, and China Metal Recycling spearhead innovation in recycling processes. With a focus on reclaiming valuable scrap aluminum, these companies employ cutting-edge technologies in sorting and purifying, facilitated by entities like IMS Metal Management and Tomra Sorting Solutions. Embracing sustainability, Edoma Recycling and Uusakoski contribute to environmental preservation by solidifying efforts in nonferrous metal recycling. Moreover, collaboration across Group 13 of the periodic table underscores concerted efforts in advancing aluminum scrap recycling, while the integration of silicon enhances material properties for diverse applications. Amidst this landscape, the convergence of minerals, flora, and animals underscores a holistic approach towards resource conservation and circular economy principles within the aluminum scrap recycling domain.

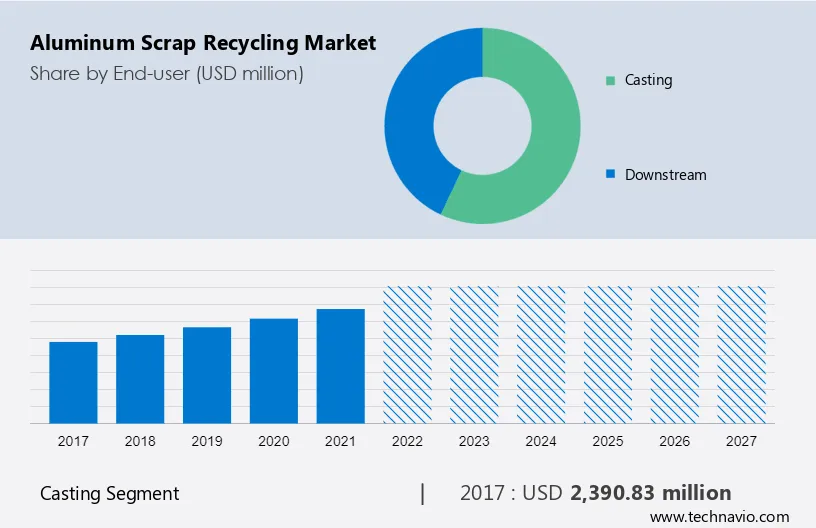

The casting segment is expected to experience significant growth in the forecast period. Casting is widely used in industries like automotive, aerospace, construction, and consumer goods for producing ingots and slabs. Technological advancements in melting and alloying techniques have further improved the casting process, enabling the production of high-quality cast products using recycled scrap. The segment's growth is driven by the easy availability as raw material, a growing focus on sustainability, and compliance with environmental regulations. It can be obtained in-house from various sources like billets, rolling slabs, frozen spilled ingots, and foundry alloy ingots.

Get a glance at the market contribution of various segments View the PDF Sample

The casting segment was the largest segment and was valued at USD 2.4 billion in 2017. However, the segment is facing challenges due to the closure of smelting plants because of unfavorable market conditions. However, companies are focusing on tackling these issues by implementing new technologies and investing significant amounts into R&D. Hence such factors are expected to propel segment growth during the forecast period.

The market based upon the type segment is categorized as old scrap and new scrap.

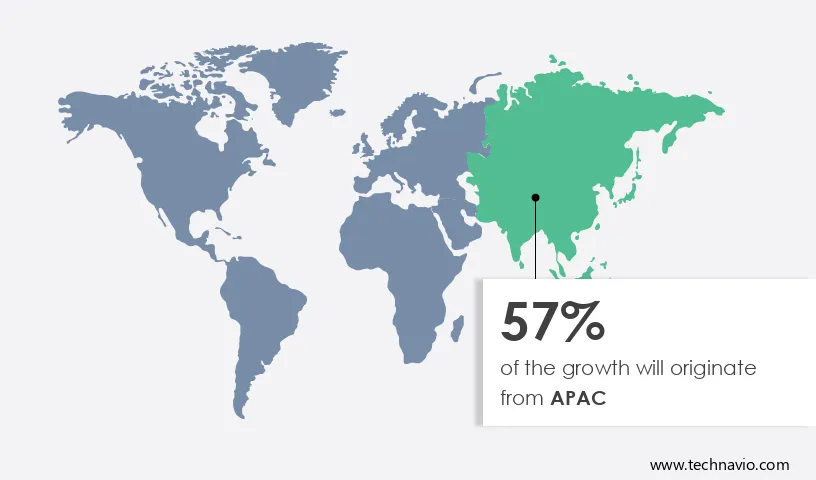

APAC is estimated to contribute 57% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

The APAC region offers significant opportunities in the global market, particularly in secondary smelting, with countries like Hong Kong, Thailand, South Korea, Japan, and Malaysia contributing to the secondary smelting capacity globally. China dominates the casting market in the region, driven by growth in the construction and automobile industries. China's ban on bauxite imports increased the demand. Several countries in the region are imposing new standards, boosting the demand. India's packaging segment is the largest consumer, driven by rising disposable income and demand for beverage cans and foils. In Japan, the demand from the automobile industry and green car incentives will fuel market growth.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Steel Dynamics Inc.- The company offers aluminum scrap recycling product and services such as Non ferrous metals, ferrous metals, aluminum, alloys and alloy wheels, and heavy machinery.

The research report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including Alcoa Corp., CASS Inc., Chiho Renewable Development Ltd., Commercial Metals Co., Constellium SE, Crestwood Metal Corp., European Metal Recycling Ltd., Hindalco Industries Ltd., Koch Enterprises Inc., Kuusakoski Oy, Metal Exchange Corp., Nucor Corp., Real Alloy, RETHMANN SE and Co. KG, Rio Tinto Ltd., Sims Ltd., Steel Dynamics Inc., Triple M Metal LP, Ye Chiu Metal Recycling China Ltd., and Norsk Hydro ASA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market is driven by a confluence of factors, from the demand for sustainable practices to the intrinsic properties of aluminum itself, including corrosion resistance. Industries spanning from retailing to consumer durables and electronics rely on recycled aluminum for products like railcars, marine vessels, and airplanes, benefiting from its resilience against corrosion. However, challenges like supply chain disruptions and labor shortages necessitate innovative solutions. Aluminum recycling practices have evolved to encompass diverse sources such as demolition of buildings and urbanization, mitigating dependence on finite natural resources and alleviating supply chain interruptions. Moreover, advancements in mining techniques and sensor technology enhance efficiency in scrap metal recycling yards, ensuring a sustainable waste stream and facilitating the production of recycled alumina and aluminium ingots.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.9% |

|

Market growth 2023-2027 |

USD 2.99 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

8.54 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 57% |

|

Key countries |

US, China, India, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Alcoa Corp., CASS Inc., Chiho Renewable Development Ltd., Commercial Metals Co., Constellium SE, Crestwood Metal Corp., European Metal Recycling Ltd., Hindalco Industries Ltd., Koch Enterprises Inc., Kuusakoski Oy, Metal Exchange Corp., Nucor Corp., Real Alloy, RETHMANN SE and Co. KG, Rio Tinto Ltd., Sims Ltd., Steel Dynamics Inc., Triple M Metal LP, Ye Chiu Metal Recycling China Ltd., and Norsk Hydro ASA |

|

Market dynamics |

Parent market growth analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the market forecast period. |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by End-user

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.