Ambulatory Surgical Centers Market Size 2026-2030

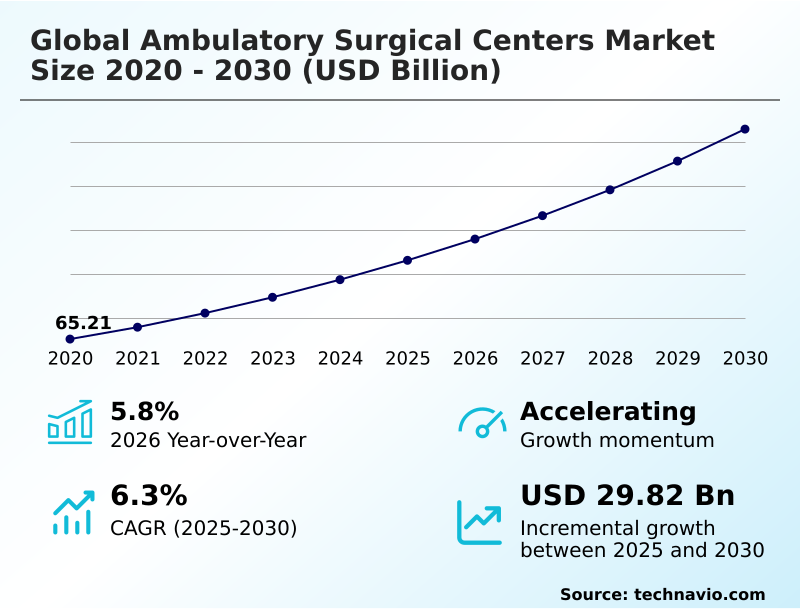

The ambulatory surgical centers market size is valued to increase by USD 29.82 billion, at a CAGR of 6.3% from 2025 to 2030. Regulatory support and acceleration of value-based payment models will drive the ambulatory surgical centers market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 50.4% growth during the forecast period.

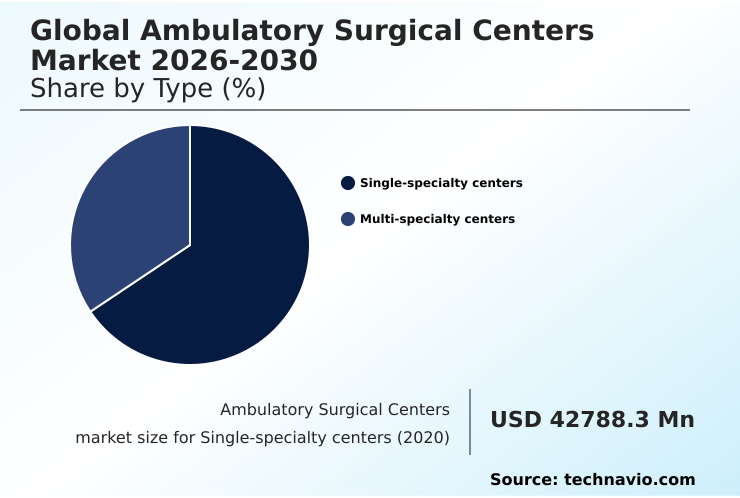

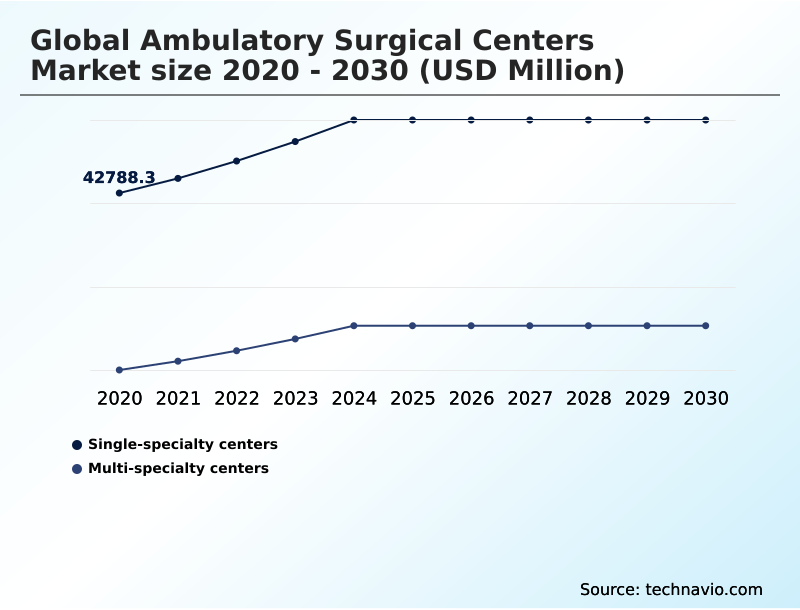

- By Type - Single-specialty centers segment was valued at USD 51.19 billion in 2024

- By Modality - Hospital-affiliated ASCs segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 47.72 billion

- Market Future Opportunities: USD 29.82 billion

- CAGR from 2025 to 2030 : 6.3%

Market Summary

- The ambulatory surgical centers market is undergoing a structural transformation, driven by a concerted push toward value-based care and cost containment. Advancements in minimally invasive surgical techniques, coupled with enhanced anesthetic protocols, are enabling the migration of high-acuity procedures like total joint replacements and cardiovascular interventions from hospitals to outpatient settings.

- This shift is supported by payers who incentivize the use of ambulatory surgical centers due to their lower cost structure. As a result, the competitive landscape is defined by aggressive consolidation, with private equity firms and large corporate operators acquiring independent, physician-owned centers to build scalable platforms.

- For instance, a mid-sized operator faces the strategic decision of whether to invest heavily in a new robotic surgery platform to attract top orthopedic surgeons or to seek a partnership with a larger health system. This decision directly impacts their ability to negotiate favorable payer contracts and manage the increasing administrative burden of regulatory compliance.

- However, the industry's expansion is constrained by a chronic shortage of specialized clinical labor and wage inflation, which compresses margins and threatens operational continuity. Navigating these dynamics requires a focus on operational efficiency and strategic physician alignment models to ensure long-term viability.

What will be the Size of the Ambulatory Surgical Centers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Ambulatory Surgical Centers Market Segmented?

The ambulatory surgical centers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Single-specialty centers

- Multi-specialty centers

- Modality

- Hospital-affiliated ASCs

- Freestanding ASCs

- Service

- Treatment

- Diagnosis

- Service type

- Otolaryngology

- Endoscopy

- Obstetrics or gynecology

- Dental

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By Type Insights

The single-specialty centers segment is estimated to witness significant growth during the forecast period.

The single-specialty center segment is driven by high-volume disciplines like ophthalmology and gastroenterology, designed for maximum efficiency in outpatient surgical care. These facilities leverage standardized workflows for specific outpatient procedures, enabling streamlined surgical scheduling optimization and superior payer contract negotiation.

By focusing on narrow specialty service lines, they achieve high repetition, which is critical for mastering minimally invasive surgery techniques and refining anesthetic protocols.

This model offers physicians significant control over the surgical environment, a key factor in their migration from hospital employment. Consolidation is rampant as management services organizations aggregate these centers to form scalable platforms.

These platforms are better equipped to handle stringent quality reporting requirements and invest in technologies like robotic-assisted surgery, improving outcomes in same-day surgery by over 15% in certain complex cases.

The Single-specialty centers segment was valued at USD 51.19 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 50.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ambulatory Surgical Centers Market Demand is Rising in North America Get Free Sample

The geographic landscape of the ambulatory surgical centers market is led by North America, which accounts for over 50% of the incremental growth, driven by favorable site-neutral payments and bundled payment initiatives.

In this region, a sophisticated ambulatory care strategy focuses on de novo facility construction in suburban areas.

In contrast, Europe is adopting value-based care models to manage public healthcare backlogs, with an emphasis on enhanced recovery after surgery protocols to improve efficiency.

Asian markets are experiencing the fastest expansion, with private chains implementing hub-and-spoke models that reduce facility overhead by up to 30% compared to tertiary hospitals.

Across all regions, effective outpatient facility management and robust revenue cycle management systems are crucial for navigating regulatory complexities and ensuring high clinical safety standards amid intense physician recruitment and retention competition.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the ambulatory surgical centers market hinges on a careful analysis of several interconnected factors. A key consideration is the cost comparison hospital versus asc, which consistently shows that outpatient settings offer significant savings, a fact that underpins payer strategies. The private equity impact on asc operations is profound, accelerating consolidation and providing capital for key investments.

- This includes the robotic surgery adoption in ascs, a critical move for attracting top surgeons and enabling the orthopedic surgery migration to ascs. Concurrently, the growth of cardiovascular procedures in outpatient setting opens new high-margin service lines. However, operators must navigate significant headwinds. Managing asc workforce shortages has become a primary operational focus, directly impacting profitability.

- Supply chain challenges for ascs can lead to case cancellations, necessitating resilient procurement strategies. Furthermore, evolving regulatory changes for asc procedures require constant vigilance to maintain compliance.

- Ultimately, the success of different ownership structures is evaluated by patient outcomes in freestanding ascs versus integrated models, with many turning to asc joint venture models benefits to align hospital and physician interests, which has proven to increase case volume by more than 15% in some partnerships.

What are the key market drivers leading to the rise in the adoption of Ambulatory Surgical Centers Industry?

- Regulatory support and the acceleration of value-based payment models serve as a key driver for the ambulatory surgical centers market.

- A primary driver is aggressive private equity investment, which fuels the expansion of corporate operator networks and the professionalization of outpatient surgery facilities through the management services organization model.

- This capital influx facilitates surgical technology adoption, with centers investing in robotics achieving over 15% improvement in clinical outcome improvement for complex cases. These platforms enable significant healthcare cost reduction, performing procedures at costs 40-50% lower than hospitals.

- Physician equity models are instrumental in aligning incentives, boosting productivity and attracting talent to manage a rising case mix complexity.

- Effective post-operative care coordination and precise outpatient procedure coding are critical for maximizing reimbursement and ensuring financial viability in this consolidating landscape.

What are the market trends shaping the Ambulatory Surgical Centers Industry?

- A dominant market trend is the acceleration of cardiovascular procedure migration, which is shifting complex interventions from traditional hospitals to specialized outpatient settings.

- A dominant trend is the acceleration of high-acuity case migration into outpatient settings, particularly within high-volume surgical specialties like cardiology and orthopedics. Advanced medical device integration and clinical pathway standardization have enabled facilities to safely increase surgical case volume, with some centers reporting a 25% increase in complex procedures year-over-year.

- This shift is compelling physician-owned centers to pursue physician partnership syndication to fund technology acquisitions. Ambulatory care platforms are crucial for managing new outpatient reimbursement models and complex regulatory compliance frameworks. Maintaining high patient satisfaction metrics is now a key performance indicator, directly impacting reimbursement in over 30% of new value-based contracts and driving adherence to strict accreditation standards.

What challenges does the Ambulatory Surgical Centers Industry face during its growth?

- The intensification of workforce shortages and related wage inflation poses a significant challenge to the growth of the ambulatory surgical centers industry.

- A major challenge is navigating volatile procedure reimbursement policies and the high upfront capital equipment expenditure required for ambulatory service line growth. The ongoing healthcare infrastructure shift necessitates robust cost-containment strategies as margin pressures intensify; labor costs alone have risen by over 10% in competitive markets.

- Ambulatory network expansion is further complicated by stringent surgical center accreditation rules and the need for sophisticated regulatory change management. While healthcare joint ventures can mitigate financial risk, achieving profitability on elective surgical procedures under value-based purchasing models remains difficult.

- This environment forces operators to focus on outpatient setting optimization to ensure that investments in surgical hub development deliver a sustainable return amid market uncertainties.

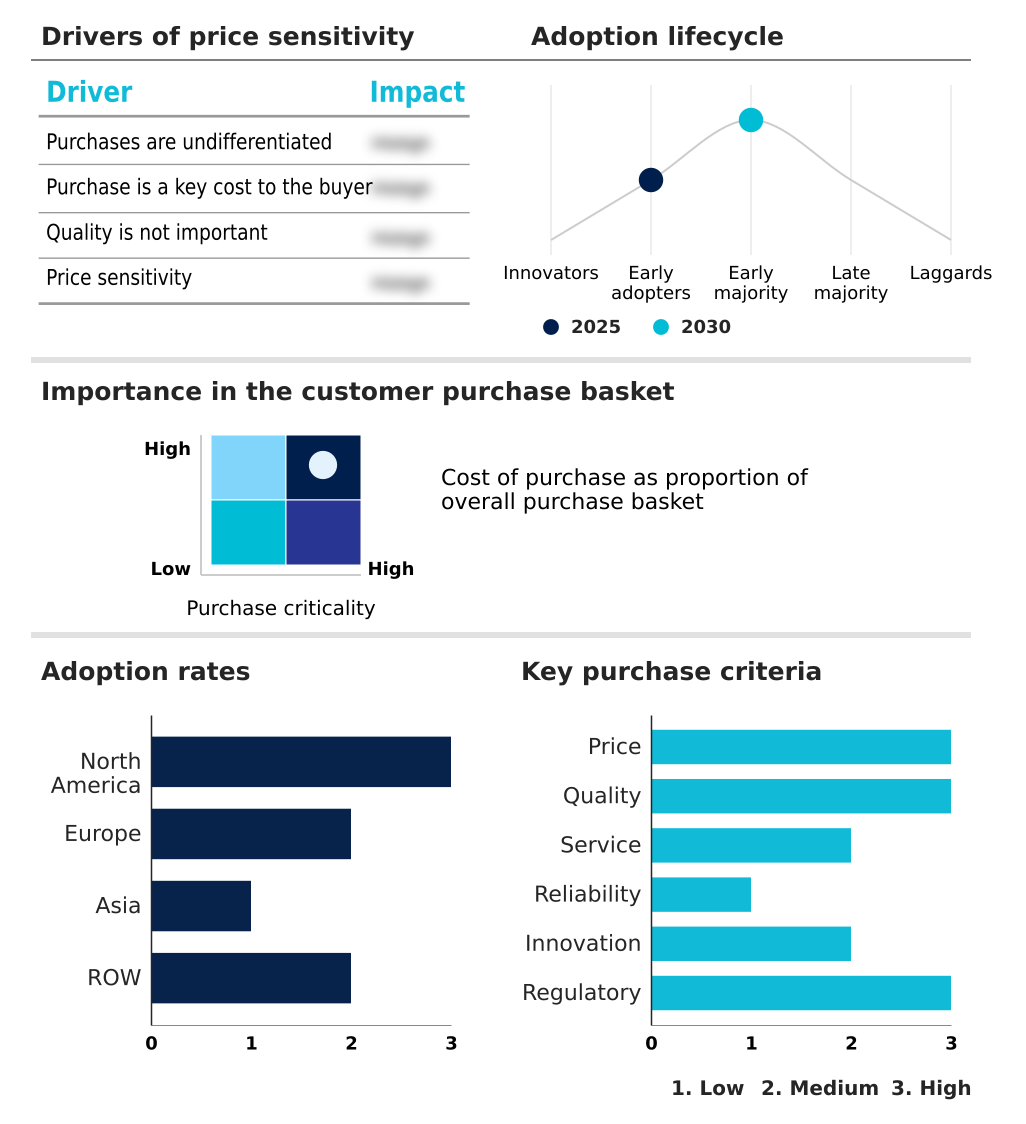

Exclusive Technavio Analysis on Customer Landscape

The ambulatory surgical centers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ambulatory surgical centers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ambulatory Surgical Centers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ambulatory surgical centers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Align Surgical Associates Inc. - Delivers strategic and operational management for ambulatory surgical centers, enabling high-quality, same-day surgical care and enhanced patient experiences.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Align Surgical Associates Inc.

- Ambulatory Surgery Center

- American Vision Partners

- AMSURG Corp.

- Azura Vascular Care

- Becton Dickinson and Co.

- Boston Scientific Corp.

- HCA Healthcare Inc.

- IOR Partners

- Medtronic Plc

- NueHealth

- Regent Surgical Health

- SCA health

- Stryker Corp.

- Surgery Partners Inc.

- Tenet Healthcare Corp.

- Unifeye Vision Partners

- University Hospitals

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ambulatory surgical centers market

- In February 2025, Tenet Healthcare earmarked approximately $450 million in capital for ambulatory surgical center mergers and acquisitions, signaling a corporate pivot toward expanding its outpatient sector.

- In March 2025, United Surgical Partners International inaugurated a state-of-the-art cardiovascular ambulatory surgery center in Phoenix, Arizona, designed to handle complex interventions like pacemaker implantations and stenting.

- In April 2025, Intuitive Surgical announced the commercial availability of its da Vinci 5 surgical system, featuring software upgrades for outpatient efficiency, leading to increased adoption in high-acuity robotic cases.

- In September 2025, Webster Equity Partners announced the merger of three regional eye care practices to form Retina and Eye Surgery Partners, a national platform that includes twelve ambulatory surgical centers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ambulatory Surgical Centers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 29817.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.8% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ambulatory surgical centers market is defined by the rapid migration of high-acuity case migration from inpatient settings, driven by advancements in minimally invasive surgery and refined anesthetic protocols. This shift necessitates a focus on impeccable clinical safety standards and accreditation standards to ensure positive outcomes for same-day surgery.

- Operationally, success depends on sophisticated revenue cycle management and effective payer contract negotiation to navigate site-neutral payments and bundled payment initiatives. Corporate operator networks and physician-owned centers alike are leveraging management services organization structures and physician alignment models to thrive.

- The boardroom focus is on capital equipment expenditure, particularly for robotic-assisted surgery, which has been shown to reduce procedural variability by over 20%. As the industry pursues de novo facility construction and ambulatory network expansion, maintaining high patient satisfaction metrics within value-based care models is paramount.

- This evolving healthcare infrastructure shift requires strategic cost-containment strategies to manage the economics of elective surgical procedures and complex surgical procedure coding, while optimizing surgical case volume through enhanced recovery after surgery protocols and securing supply chain procurement.

What are the Key Data Covered in this Ambulatory Surgical Centers Market Research and Growth Report?

-

What is the expected growth of the Ambulatory Surgical Centers Market between 2026 and 2030?

-

USD 29.82 billion, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Single-specialty centers, and Multi-specialty centers), Modality (Hospital-affiliated ASCs, and Freestanding ASCs), Service (Treatment, and Diagnosis), Service Type (Otolaryngology, Endoscopy, Obstetrics or gynecology, Dental, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Regulatory support and acceleration of value-based payment models, Intensification of workforce shortages and wage inflation

-

-

Who are the major players in the Ambulatory Surgical Centers Market?

-

Align Surgical Associates Inc., Ambulatory Surgery Center, American Vision Partners, AMSURG Corp., Azura Vascular Care, Becton Dickinson and Co., Boston Scientific Corp., HCA Healthcare Inc., IOR Partners, Medtronic Plc, NueHealth, Regent Surgical Health, SCA health, Stryker Corp., Surgery Partners Inc., Tenet Healthcare Corp., Unifeye Vision Partners and University Hospitals

-

Market Research Insights

- The ambulatory care strategy is increasingly focused on care continuum integration and achieving superior operational efficiency metrics. This strategic shift is delivering measurable results, with integrated ambulatory care platforms demonstrating up to a 40-50% cost reduction compared to traditional hospital outpatient departments for similar procedures.

- Health system partnerships are pivotal, allowing for streamlined patient referral pathways and improved surgical scheduling optimization, which has been shown to boost facility throughput by over 15%.

- As high-volume surgical specialties continue to migrate to the outpatient setting, a focus on patient experience enhancement and robust quality reporting requirements becomes critical for maintaining competitive advantage and securing favorable outpatient reimbursement models.

We can help! Our analysts can customize this ambulatory surgical centers market research report to meet your requirements.

RIA -

RIA -