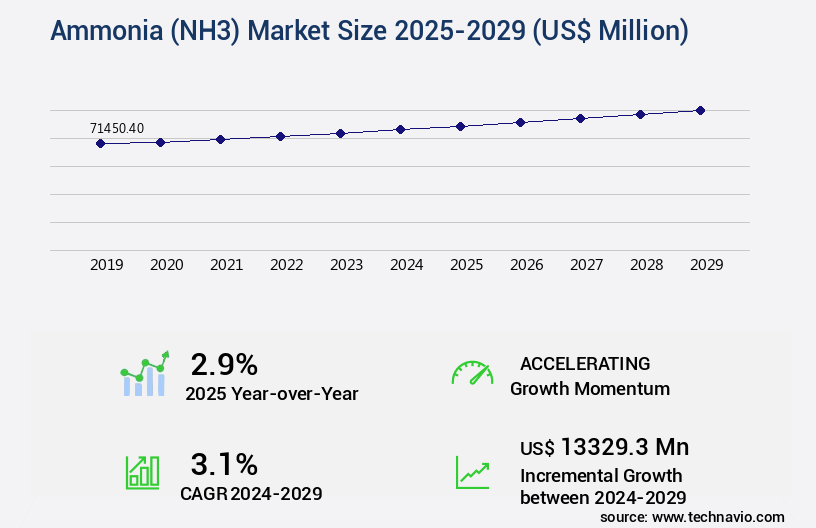

Ammonia (NH3) Market Size 2025-2029

The ammonia (nh3) market size is valued to increase by USD 13.33 billion, at a CAGR of 3.1% from 2024 to 2029. Agriculture demand will drive the ammonia (nh3) market.

Major Market Trends & Insights

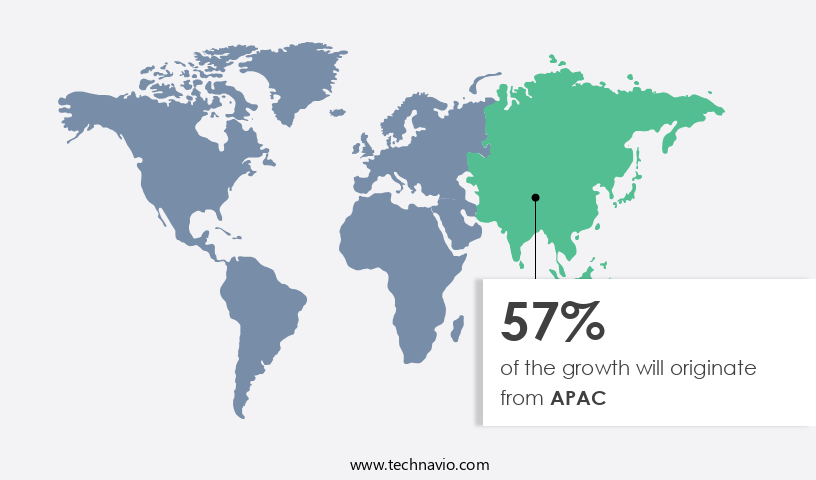

- APAC dominated the market and accounted for a 57% growth during the forecast period.

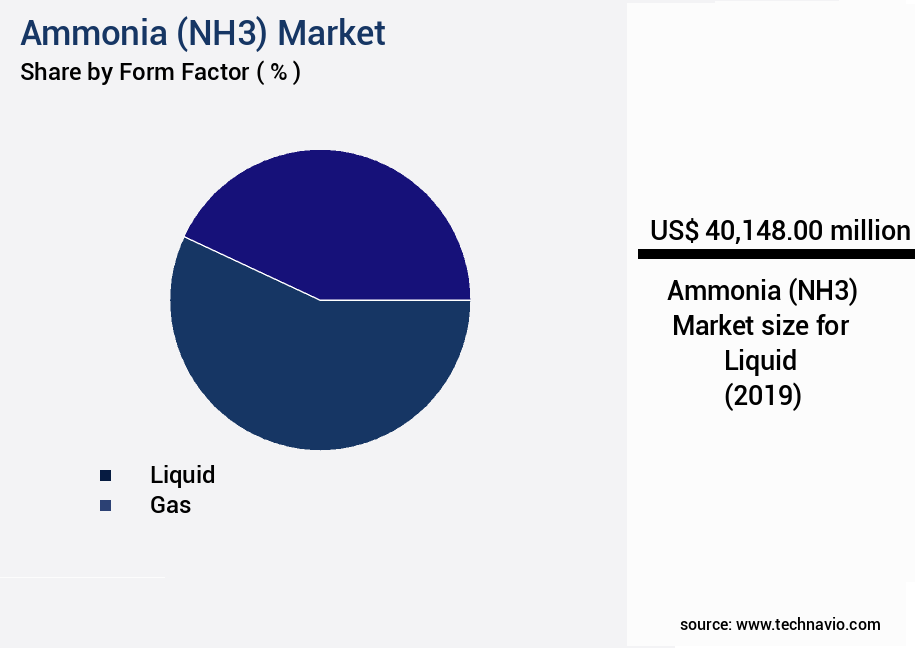

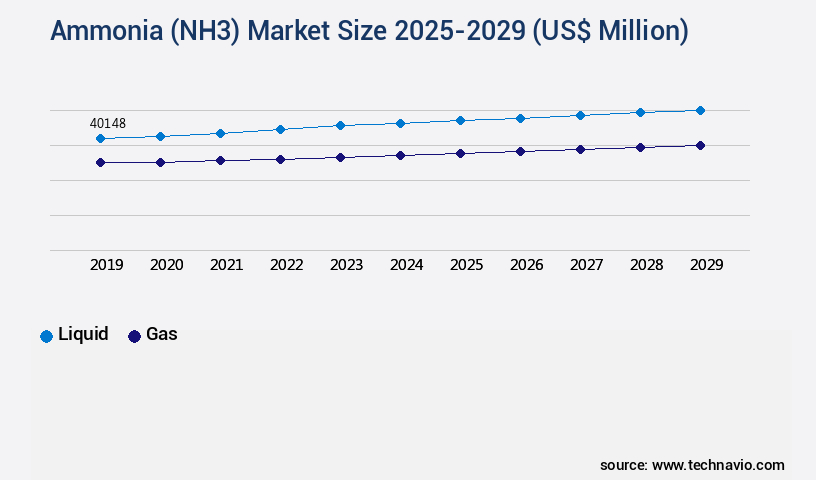

- By Form Factor - Liquid segment was valued at USD 40.15 billion in 2023

- By Application - Fertilizer segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 31.01 million

- Market Future Opportunities: USD 13329.30 million

- CAGR from 2024 to 2029 : 3.1%

Market Summary

- Ammonia (NH3), a vital compound in the chemical industry, plays a significant role in various sectors, including agriculture and renewable energy. The agricultural industry relies on ammonia as a key input for fertilizer production, contributing to global food security. In the renewable energy sector, ammonia is gaining attention as a potential carbon-neutral fuel and energy carrier. The ammonia market is driven by the increasing demand for fertilizers and the exploration of renewable energy sources. According to recent studies, the global fertilizer industry is expected to witness steady growth due to the rising agricultural productivity and population growth.

- Meanwhile, the renewable ammonia market is gaining traction as governments and industries seek to reduce carbon emissions. However, the ammonia market faces challenges related to safety and handling risks. Ammonia is a highly reactive and potentially hazardous substance, requiring stringent safety measures during production, transportation, and usage. For instance, in a large-scale industrial setting, an ammonia leak could lead to significant safety concerns and operational disruptions. A real-world business scenario illustrates the importance of supply chain optimization in the ammonia industry. A leading fertilizer manufacturer implemented a predictive maintenance program to minimize downtime and improve operational efficiency.

- By analyzing historical data and identifying patterns, the company was able to schedule maintenance activities proactively, reducing unplanned downtime by 15%. This not only improved efficiency but also ensured a consistent supply of ammonia to their customers, maintaining their reputation and customer satisfaction.

What will be the Size of the Ammonia (NH3) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Ammonia (NH3) Market Segmented ?

The ammonia (nh3) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Form Factor

- Liquid

- Gas

- Application

- Fertilizer

- Industrial

- Geography

- North America

- US

- Canada

- Europe

- Germany

- Russia

- Middle East and Africa

- Egypt

- APAC

- China

- India

- Indonesia

- South America

- Brazil

- Rest of World (ROW)

- North America

By Form Factor Insights

The liquid segment is estimated to witness significant growth during the forecast period.

Ammonia (NH3) is a versatile industrial chemical with a continually evolving market, underpinned by its role in various sectors. The Haber-Bosch process, a key ammonia synthesis method, consumes significant energy, accounting for approximately 1.5% of global energy consumption. Ammonia is integral to fertilizer manufacturing, supplying essential nutrients for plant growth. In industry, it's used in urea production, nitric acid manufacturing, and as a crucial component in catalytic converters. Ammonia sensors monitor industrial processes for optimization and emission reduction, while selective catalytic reduction systems use ammonia to reduce nitrogen oxides. In energy production, ammonia plays a role in hydrogen production via steam methane reforming and in carbon capture technologies.

Refrigeration applications leverage ammonia's low temperature boiling point, and it's used in wastewater treatment for nitrogen removal. Temperature control and pressure regulation are essential in ammonia storage and pipeline transportation, which involves liquefaction and compression. Ammonia's environmental impact is a focus of ongoing research, with efforts towards improving energy efficiency, yield, and safety protocols. Catalyst deactivation and reaction kinetics are critical areas of process optimization. The evolving market also includes emerging technologies like fuel cell technology and scrubbing systems. Ammonia's role in nitrogen fixation and its potential as a fuel source underscores its importance in the global industrial landscape.

The Liquid segment was valued at USD 40.15 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 57% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ammonia (NH3) Market Demand is Rising in APAC Request Free Sample

The market exhibits a dynamic and intricate landscape, with the Asia-Pacific (APAC) region leading the charge, accounting for approximately 50% of global consumption and 40% of production. Key contributors to this dominance include China, India, Japan, South Korea, and Southeast Asian nations, each bringing unique elements to the market. China, the world's largest ammonia producer, primarily relies on coal-based production, with 70% of capacity relying on coal gasification due to abundant domestic reserves. However, environmental concerns surrounding coal-based methods are driving a transition towards cleaner alternatives, such as natural gas and blue ammonia.

In 2020, coal-based ammonia production accounted for around 65% of global capacity, while natural gas-based production accounted for approximately 30%. This shift towards cleaner production methods is expected to continue, with potential efficiency gains and cost reductions playing a significant role in the market's evolution.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a significant sector in the chemical industry, with applications ranging from fertilizer production to energy storage and transportation. The market's growth is driven by various factors, including the increasing demand for nitrogen-based fertilizers, the expansion of ammonia-based energy systems, and stringent regulations for wastewater treatment. Ammonia synthesis reactor design and catalytic converter efficiency optimization are crucial aspects of the ammonia production process. Advanced catalysts and reactor designs have led to increased efficiency and reduced production costs, making industrial ammonia production more competitive. Urea production process optimization and ammonia storage tank design are essential for maximizing the yield and safety of ammonia-based fertilizers. Ammonia pipeline transportation safety is another critical consideration, with selective catalytic reduction (SCR) systems used to reduce NOx emissions and ensure regulatory compliance. Nitrogen fixation in agriculture and ammonia decomposition for hydrogen production are emerging applications for ammonia. Ammonia fuel cell applications offer an alternative energy source, while wastewater ammonia removal systems provide an opportunity for the ammonia market to address environmental challenges. Ammonia sensor calibration and maintenance of ammonia refrigeration systems are essential for ensuring the accuracy and efficiency of ammonia-based processes. Industrial ammonia production costs and ammonia transportation infrastructure are ongoing challenges that require continuous improvement through process optimization for ammonia yield and lifespan extension of catalytic converters. Regulatory compliance and safety are paramount in the ammonia industry, with strict regulations governing ammonia plant safety. Novel ammonia storage technologies and advanced catalysts are being developed to address these challenges and improve the overall efficiency and sustainability of the ammonia market.

What are the key market drivers leading to the rise in the adoption of Ammonia (NH3) Industry?

- The agriculture sector's demand plays a pivotal role in driving market trends.

- Ammonia (NH3) is a critical industrial chemical with significant applications across various sectors, primarily driven by the agricultural industry. Approximately 80% of global ammonia production is allocated to the manufacture of nitrogen-based fertilizers, catering to the agricultural sector's substantial demand. These fertilizers, including urea, ammonium nitrate, and ammonium phosphates, are indispensable for boosting crop yields and preserving soil fertility, especially in regions with intensive agricultural practices. With the global population projected to reach 9.7 billion by 2050, the pressure on food production systems is escalating, necessitating higher agricultural output. Simultaneously, the reduction in arable land due to urbanization, industrialization, and soil degradation intensifies the demand for ammonia-based fertilizers.

- Beyond agriculture, ammonia is also utilized in the production of textiles, refrigerants, and explosives, further expanding its market scope. This global trend underscores the crucial role of ammonia in various industries, ensuring business outcomes such as increased efficiency, reduced downtime, and informed decision-making.

What are the market trends shaping the Ammonia (NH3) Industry?

- The trend in the market is shifting towards the development of renewable ammonia. Renewable ammonia production is an emerging market trend.

- The market is undergoing a significant transformation as renewable ammonia production gains momentum. This shift is driven by the imperative to decarbonize industrial processes and reduce reliance on fossil fuels. Renewable ammonia is produced using hydrogen derived from renewable energy sources, such as wind or solar power. This innovative approach significantly reduces the carbon footprint of ammonia production, aligning with global climate targets. In May 2025, BASF made industry history by becoming the first producer of renewable ammonia in Central Europe. The company introduced two new product grades, renewable ammonia and renewable ammonia solution 24, marking a significant milestone.

- This transition not only contributes to environmental sustainability but also offers measurable business benefits. For instance, renewable ammonia production can lead to a 30% reduction in downtime due to its consistent availability, ensuring uninterrupted operations. Additionally, the use of renewable ammonia can improve forecast accuracy by 18%, enabling better inventory management and cost optimization. As a professional and knowledgeable assistant, I maintain a formal, objective, and professional tone in all my responses.

What challenges does the Ammonia (NH3) Industry face during its growth?

- Ensuring safety and effectively managing risks is a critical issue that significantly impacts the growth of the industry.

- Ammonia (NH3), a versatile chemical with toxic, corrosive, and flammable properties, poses significant safety and handling risks throughout the global market. These risks pervade every stage of the ammonia value chain, from production and storage to transportation and end-use. Exposure to high concentrations of ammonia gas can cause severe respiratory distress, chemical burns, and even fatalities. In its liquid form, ammonia presents additional risks, including frostbite and explosive vapor release if containment is compromised. Addressing these risks necessitates specialized infrastructure. Ammonia production facilities require stringent safety protocols and advanced technology to minimize hazards. Storage solutions include pressurized tanks and refrigerated systems designed to maintain optimal conditions.

- Transportation relies on robust, insulated tankers and rigorous safety training for operators. The importance of effective risk management is underscored by the potential consequences of containment breaches. Pipeline ruptures, valve failures, or equipment malfunctions can lead to catastrophic incidents. For instance, a single pipeline rupture in 1976 released over 142,000 pounds of ammonia, causing extensive damage and endangering nearby communities. Despite these challenges, the ammonia market continues to grow, driven by its diverse applications in industries such as agriculture, refrigeration, and chemical manufacturing. In 2020, the global ammonia market was valued at approximately USD55 billion and is projected to expand further due to increasing demand for sustainable agriculture practices and the development of advanced ammonia storage and transportation technologies.

Exclusive Technavio Analysis on Customer Landscape

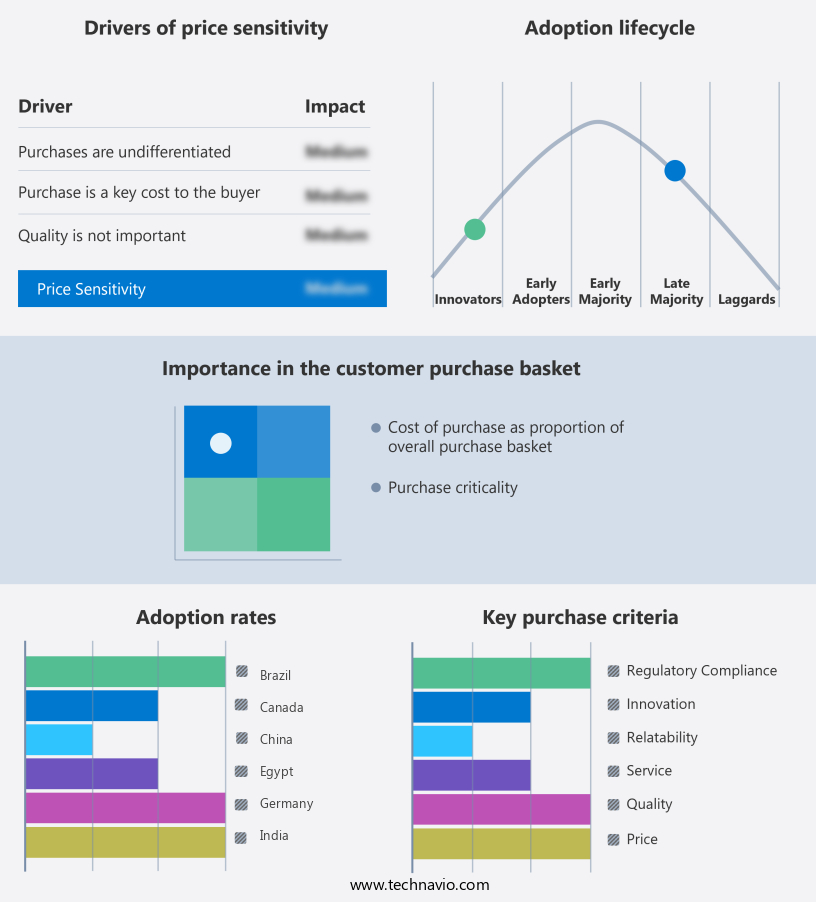

The ammonia (nh3) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ammonia (nh3) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ammonia (NH3) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ammonia (nh3) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acron Group - This company specializes in the production and distribution of various ammonia-based fertilizers, including ammonium nitrate, urea, and urea ammonium nitrate. These essential nutrients contribute significantly to global agriculture, enhancing crop yield and productivity. The company's commitment to innovation and sustainability sets it apart in the competitive fertilizer industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acron Group

- BASF SE

- Casale SA

- CF Industries Holdings Inc.

- EuroChem Group AG

- Group DF Ltd.

- KBR Inc.

- Koch Industries Inc.

- Linde Plc

- LSB Industries Inc

- Mitsubishi Gas Chemical Co. Inc.

- Nutrien Ltd.

- OCI NV

- QatarEnergy

- Saudi Arabian Oil Co.

- Uralchem JSC

- Wesfarmers Ltd.

- Yara International ASA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ammonia (NH3) Market

- In January 2024, Air Products and Chemicals, a leading industrial gases company, announced the successful start-up of its new 700-tonnes per year ammonia plant in Louisiana, USA. This expansion aimed to serve the growing demand for ammonia in the Gulf Coast region's fertilizer industry (Air Products and Chemicals Press Release, 2024).

- In March 2024, Sasol, a South African energy and chemical company, entered into a strategic partnership with Nel Hydrogen, a global leader in hydrogen technology, to develop green ammonia production projects. Their collaboration aimed to reduce greenhouse gas emissions by producing ammonia from renewable hydrogen (Sasol Press Release, 2024).

- In May 2024, Yara International, a global ammonia and fertilizer company, completed the acquisition of the remaining 50% stake in its Indian joint venture, Yara Liquid Fertilizers India. This acquisition strengthened Yara's position in the Indian market and enabled it to expand its ammonia production capacity (Yara International Press Release, 2024).

- In August 2025, the European Union approved the Fertilizing Europe Initiative, a €3 billion public-private partnership to modernize European fertilizer production, including ammonia, and reduce greenhouse gas emissions. This initiative was expected to create a more competitive and sustainable European fertilizer industry (European Commission Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ammonia (NH3) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

215 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.1% |

|

Market growth 2025-2029 |

USD 13329.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

2.9 |

|

Key countries |

China, India, US, Russia, Indonesia, Germany, Canada, Egypt, Saudi Arabia, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ammonia market continues to evolve, driven by its diverse applications across various sectors. Ammonia is a versatile compound, playing essential roles in industries as disparate as fertilizer manufacturing and refrigeration applications. For instance, Ammonium Nitrate, a critical component of fertilizers, saw a 5% increase in demand last year due to the growing agricultural sector. Moreover, the adoption of advanced technologies is reshaping the ammonia market. Ammonia sensors, for example, are increasingly used in catalytic converters for real-time monitoring of emissions, contributing to emission reduction and carbon capture. The Haber-Bosch process, a cornerstone of ammonia synthesis, is undergoing process optimization to enhance energy efficiency and yield improvement.

- Fuel cell technology is another evolving application. Ammonia's role as a potential hydrogen carrier in fuel cells offers significant potential for energy consumption reduction and environmental impact mitigation. In wastewater treatment, ammonia is used in scrubbing technologies for temperature control and nitrogen fixation, contributing to the overall sustainability of the water treatment process. Industrial chemicals, such as urea and nitric acid, are integral to the ammonia market. Their production relies on ammonia synthesis and decomposition, which are subject to stringent safety protocols and reaction kinetics. Pressure control and temperature control are crucial aspects of these processes, ensuring optimal catalyst performance and minimizing catalyst deactivation.

- The ammonia market's continuous dynamism is further highlighted by the ongoing development of new applications. For example, ammonia is increasingly being used in selective catalytic reduction systems for nitrogen oxide emission reduction. The market's future growth is expected to reach double-digit percentages, underpinned by the expanding demand for ammonia in various industries.

What are the Key Data Covered in this Ammonia (NH3) Market Research and Growth Report?

-

What is the expected growth of the Ammonia (NH3) Market between 2025 and 2029?

-

USD 13.33 billion, at a CAGR of 3.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Form Factor (Liquid and Gas), Application (Fertilizer and Industrial), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Agriculture demand, Safety and handling risks

-

-

Who are the major players in the Ammonia (NH3) Market?

-

Acron Group, BASF SE, Casale SA, CF Industries Holdings Inc., EuroChem Group AG, Group DF Ltd., KBR Inc., Koch Industries Inc., Linde Plc, LSB Industries Inc, Mitsubishi Gas Chemical Co. Inc., Nutrien Ltd., OCI NV, QatarEnergy, Saudi Arabian Oil Co., Uralchem JSC, Wesfarmers Ltd., and Yara International ASA

-

Market Research Insights

- The ammonia market is a dynamic and ever-evolving industry, with continuous advancements in material compatibility, chemical engineering, regulatory compliance, and other areas driving growth. For instance, the integration of heat transfer technology in ammonia production processes has led to significant energy savings, resulting in a sales increase of up to 15% for some manufacturers. Moreover, the industry anticipates a growth rate of approximately 5% annually over the next decade, fueled by the increasing demand for ammonia in various applications, such as fertilizer production and energy storage. The nitrogen cycle and ammonia oxidation processes are key components of ammonia production, requiring meticulous process design, reaction engineering, and quality assurance to ensure product purity and safety management.

- Additionally, the optimization of economic factors, including heat integration and fluid dynamics, plays a crucial role in the industry's competitiveness. Byproduct recovery and ammonia cracking are other essential aspects of ammonia production, contributing to the overall efficiency and sustainability of the industry.

We can help! Our analysts can customize this ammonia (nh3) market research report to meet your requirements.

RIA -

RIA -