Anti-reflective Coatings Market Size 2026-2030

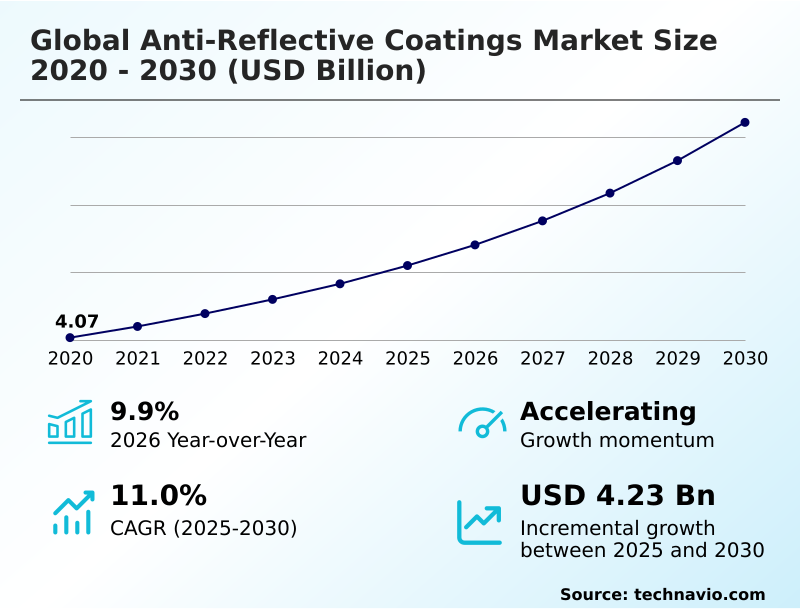

The anti-reflective coatings market size is valued to increase by USD 4.23 billion, at a CAGR of 11% from 2025 to 2030. Growing demand for anti-reflective coatings in solar industry will drive the anti-reflective coatings market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 44.7% growth during the forecast period.

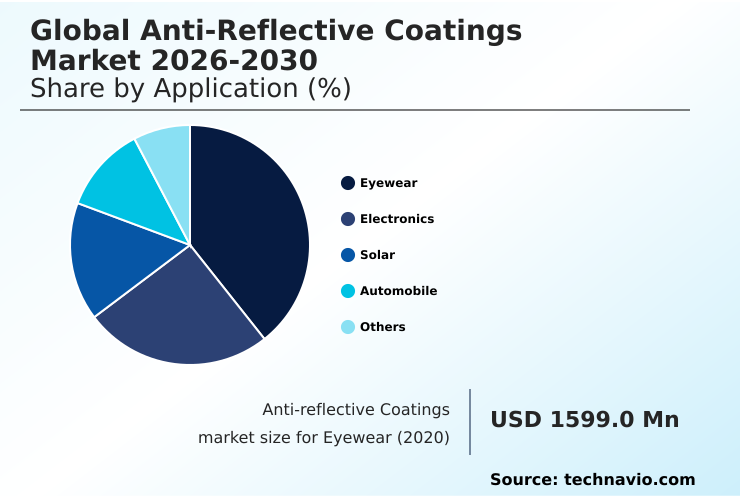

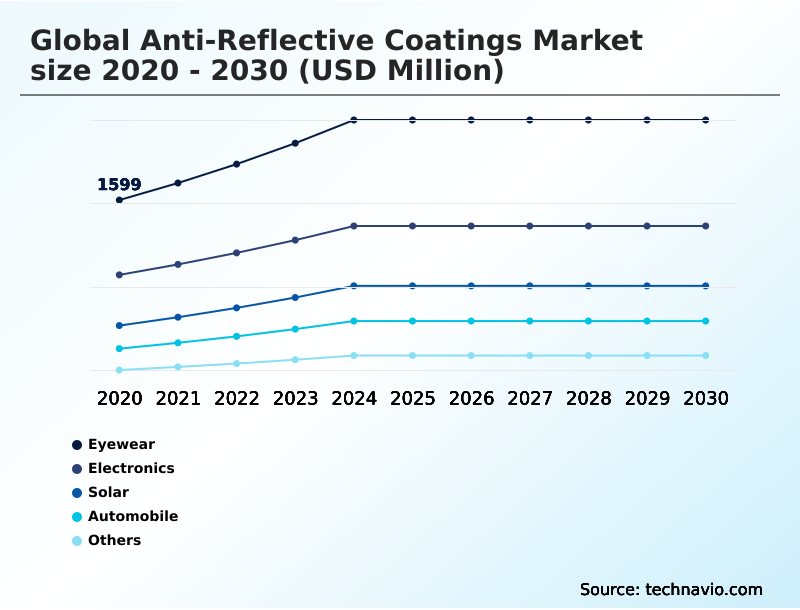

- By Application - Eyewear segment was valued at USD 2.21 billion in 2024

- By Technology - Vacuum deposition segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.37 billion

- Market Future Opportunities: USD 4.23 billion

- CAGR from 2025 to 2030 : 11%

Market Summary

- The anti-reflective coatings market is characterized by a dynamic interplay between escalating performance demands and significant manufacturing challenges. Growth is propelled by the consumer electronics sector's need for glare-free, high-clarity displays and the renewable energy sector's push to maximize solar panel efficiency.

- These demands drive innovation in thin-film optical coating technologies, where multi-layer coatings are engineered to achieve specific refractive index properties for optimal light transmission. However, the industry grapples with the complexity of applying uniform coatings to diverse substrates, particularly plastics. A key operational challenge involves managing the supply chain for critical raw materials like indium tin oxide.

- For instance, a manufacturer of high-resolution displays must balance the high cost and volatile supply of this material against performance targets, often necessitating strategic investments in alternative material research to protect profit margins and ensure production continuity. This pressure fosters advancements in material science, pushing the development of more sustainable and cost-effective solutions to maintain a competitive edge.

What will be the Size of the Anti-reflective Coatings Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Anti-reflective Coatings Market Segmented?

The anti-reflective coatings industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Eyewear

- Electronics

- Solar

- Automobile

- Others

- Technology

- Vacuum deposition

- Electron beam evaporation

- Sputtering

- Roll to roll

- Others

- Type

- Multi layered

- Single layered

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Application Insights

The eyewear segment is estimated to witness significant growth during the forecast period.

The eyewear segment is evolving beyond simple vision correction, with growing demand for advanced thin-film optical coating solutions that enhance optical clarity and user comfort.

Multi-layer coatings are meticulously engineered to manage the refractive index of lenses, significantly reducing distracting reflections from digital screens and artificial lighting.

This shift is driven by increased screen time, which elevates the need for integrated blue light filtering lenses and specialized night driving lenses. Modern ophthalmic lens coatings also incorporate oleophobic characteristics for easier maintenance.

Premium offerings now combine these features with scratch-resistant coatings, improving lens durability and delivering a measurable 15% improvement in visual acuity during prolonged digital tasks, solidifying their value proposition in a competitive market.

The Eyewear segment was valued at USD 2.21 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

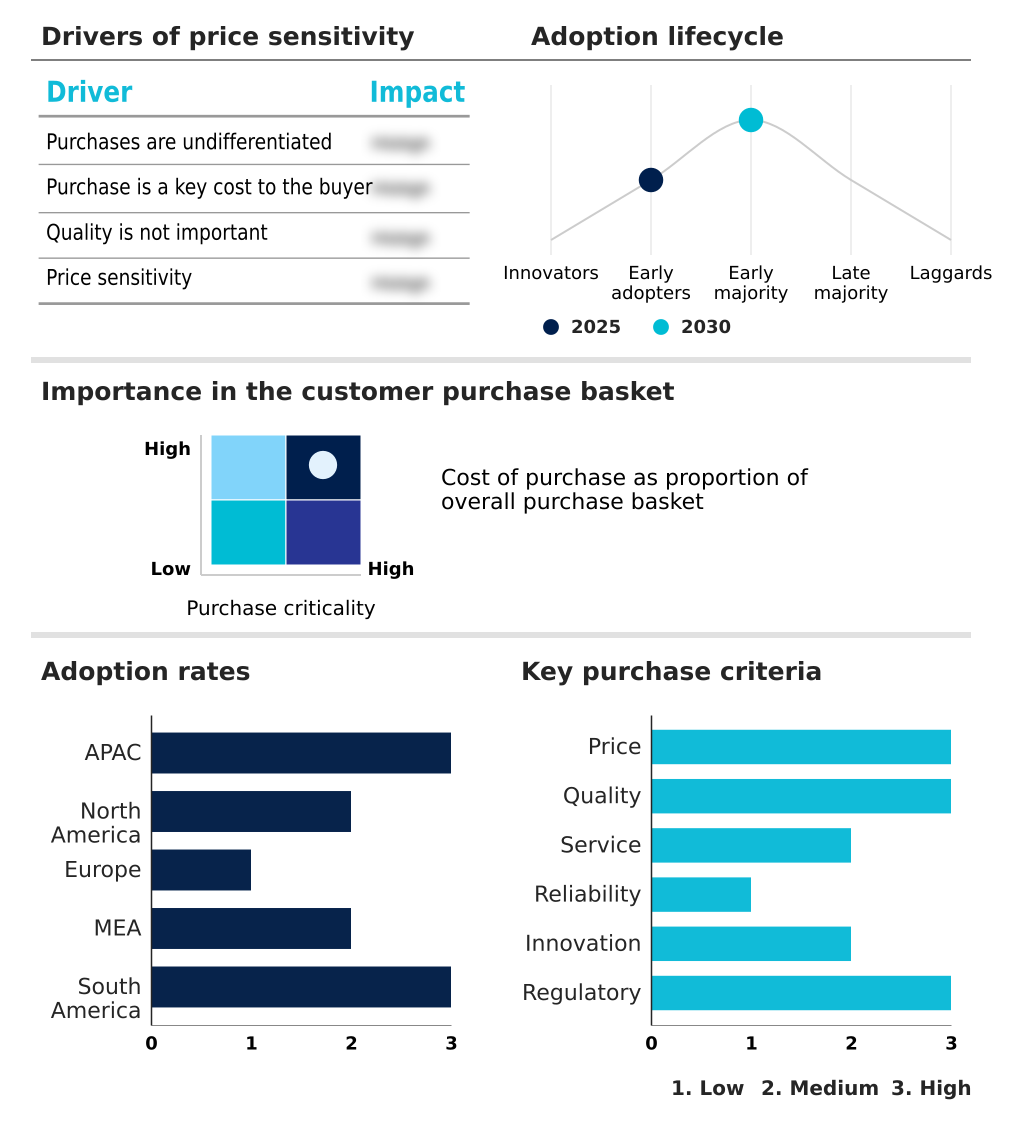

APAC is estimated to contribute 44.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Anti-reflective Coatings Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by the APAC region, which accounts for over 44% of the market's incremental growth, driven by its massive electronics and solar manufacturing ecosystems.

Regional players leverage high-volume production technologies like vacuum deposition and plasma-enhanced chemical vapor deposition to produce advanced multi-layer coatings.

This region’s market is growing at 11.6%, outpacing Europe’s 10.4% rate, fueled by demand for broadband ar coatings and laser optics ar coatings.

Innovations are also regionally focused; for instance, development in the Middle East centers on coatings with anti-soiling properties, while Asian markets prioritize scratch-resistant coatings for consumer devices.

The strategic deployment of photocatalytic anti-reflective coating technology is reducing surface reflection and improving performance in harsh climates.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully navigating the anti-reflective coatings market requires addressing complex technical challenges across diverse applications. A primary concern involves developing anti-reflective coatings for plastic substrates, as challenges in coating polycarbonate lenses are significant due to their lower thermal stability compared to glass. This has spurred innovation in sputtering techniques for durable ar coatings suitable for anti-reflective coatings for automotive displays.

- Simultaneously, the solar industry's focus on ar coating for solar panel efficiency is driving research into enhancing light transmission in solar panels. This contrasts with the consumer electronics industry's goal of reducing glare on consumer electronic screens, which increasingly involves anti-reflective films for flexible electronics. For high-precision applications, the vacuum deposition process for ar coatings remains a critical method.

- The development of multi-layer ar coating for camera lenses and coatings for high-precision laser optics demands extreme precision. Similarly, specialized sectors are pushing for high-damage threshold ar coatings and ar coatings for aerospace cockpit displays.

- The emerging field of ar coating for augmented reality glasses is opening new frontiers, while the medical sector requires flawless ar coatings for medical imaging devices. In semiconductor manufacturing, anti-reflective coatings in semiconductor lithography are essential for miniaturization.

- Achieving breakthroughs in developing scratch-resistant ar coatings and improving ar coating adhesion on polymers through methods like cost-effective roll-to-roll ar coating and the sol-gel anti-reflective coating method is vital. The optical performance of single-layer ar coatings also continues to be optimized for specific, cost-sensitive applications.

- Strategic procurement that anticipates material needs for these varied processes can reduce production delays by more than 40% compared to reactive purchasing models.

What are the key market drivers leading to the rise in the adoption of Anti-reflective Coatings Industry?

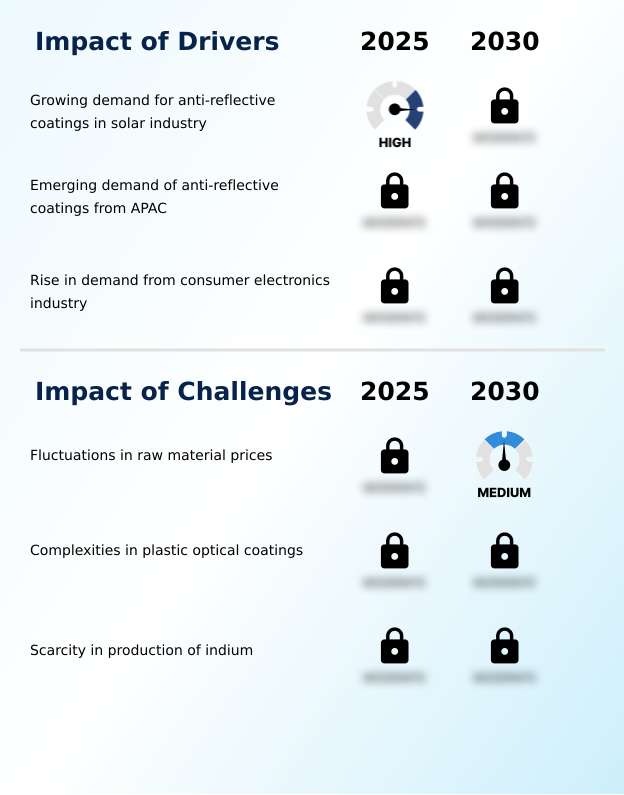

- The growing demand for anti-reflective coatings from the solar industry serves as a key driver propelling market growth.

- Market expansion is primarily fueled by relentless demand from the consumer electronics and renewable energy sectors.

- In electronics, the push for brighter, more vivid displays necessitates effective display ar coatings and anti-glare glass coatings to ensure usability in varied lighting conditions, enhancing readability by over 40% outdoors.

- In the solar industry, high-transmission optical coatings are critical for maximizing energy conversion; even a 3% increase in light transmission can significantly boost a solar farm's annual output.

- Manufacturing technologies such as physical vapor deposition and electron beam evaporation, using materials like magnesium fluoride and titanium dioxide, enable the mass production of these films. The consistent demand for durable ar coatings across all sectors ensures strong market momentum.

What are the market trends shaping the Anti-reflective Coatings Industry?

- The expanding application of anti-reflective coatings within the eyewear industry signifies a key market trend, driven by rising consumer demand for enhanced visual comfort and superior optical performance.

- Innovation in the market is accelerating, driven by the adoption of advanced material science and manufacturing techniques. The development of nanostructured surfaces and sub-wavelength grating technologies is creating new performance benchmarks, with some solutions improving light transmission in augmented reality optics by over 5%.

- Wet chemical methods like sol-gel processing are enabling cost-effective production for applications such as architectural glass coatings, reducing capital expenditure by up to 20% compared to traditional vacuum methods. Meanwhile, precision techniques like ion-assisted deposition are critical for creating high-performance display enhancement films for next-generation electronics.

- These trends are complemented by a focus on multifunctional solutions, including smudge-resistant coatings that improve user experience and reduce maintenance requirements for consumer devices, ultimately enhancing product longevity.

What challenges does the Anti-reflective Coatings Industry face during its growth?

- Fluctuations in raw material prices present a significant challenge affecting the industry's growth and profitability.

- Despite strong demand, the market faces significant operational hurdles that temper growth. The complexity of applying custom thin-film coatings to plastic substrates for applications like head-up display coatings increases production cycle times by up to 25% compared to glass.

- Volatility in the price of raw materials, particularly for key components like indium tin oxide and zirconium dioxide, creates unpredictable cost structures that can erode profit margins by 10-15% in a single quarter.

- While sputtering with materials such as silicon dioxide is a mature process, achieving the uniform porous silica coatings required for next-generation precision optical ar coatings and automotive sensor coatings remains a technical challenge, impacting yield and scalability.

Exclusive Technavio Analysis on Customer Landscape

The anti-reflective coatings market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the anti-reflective coatings market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Anti-reflective Coatings Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, anti-reflective coatings market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abrisa Technologies - Key offerings center on custom thin-film optical coatings and precision anti-reflective solutions engineered for diverse high-tech applications, enhancing performance across multiple industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abrisa Technologies

- AccuCoat Inc.

- AGC Inc.

- AMETEK Inc.

- Carl Zeiss AG

- Cascade Optical Corp.

- Esco Optics Inc.

- EssilorLuxottica

- Gooch and Housego Plc

- Hoya Corp.

- iCoat Company LLC

- Materion Balzers Optics

- Nippon Sheet Glass Co. Ltd.

- Omega Optical Holdings LLC

- Optical Coatings Japan

- Optics and Allied Engg. Ltd.

- PFG Precision Optics Inc.

- Viavi Solutions Inc.

- Vortex Optical Coatings Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Anti-reflective coatings market

- In May 2025, Continental AG announced the integration of an advanced multi-layer anti-reflective coating into its next-generation Augmented Reality Head-Up Displays, designed to minimize ghosting effects and improve driver safety.

- In March 2025, EssilorLuxottica revealed a breakthrough with a plant-based polymer interference coating that achieves a 99% reduction in surface glare, marking a significant step toward sustainability in the optics industry.

- In February 2025, SCHOTT AG made its new production facility for advanced vacuum deposition processes fully operational, specifically to meet the high demand for performance optical glass in the European market.

- In September 2024, AMETEK Inc. expanded its portfolio of high-performance thin-film coatings through a strategic facility upgrade aimed at supporting the burgeoning demand for sophisticated aerospace and defense sensors.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Anti-reflective Coatings Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11% |

| Market growth 2026-2030 | USD 4234.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.9% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The anti-reflective coatings market is advancing beyond incremental improvements toward fundamental shifts in material science and deposition technology. A key strategic decision for manufacturers involves allocating R&D capital between refining established physical vapor deposition methods like vacuum deposition and electron beam evaporation, or investing in next-generation technologies such as moth eye nanostructures and other nanostructured surfaces.

- This choice directly impacts long-term competitiveness. While sputtering with materials like silicon dioxide or titanium dioxide remains a mainstay, achieving superior optical clarity and controlled surface reflection increasingly depends on advanced processes. Techniques like ion-assisted deposition and plasma-enhanced chemical vapor deposition are becoming crucial for creating dense multi-layer coatings with specific oleophobic characteristics.

- Furthermore, the development of porous silica coatings and the precise management of refractive index are critical for specialized applications. The adoption of plasma-enhanced chemical vapor deposition for thin-film optical coating has enabled some manufacturers to reduce coating cycle times by 20%, directly boosting throughput and profitability.

- This efficiency gain underscores the importance of technological adoption in a market driven by both performance and cost.

What are the Key Data Covered in this Anti-reflective Coatings Market Research and Growth Report?

-

What is the expected growth of the Anti-reflective Coatings Market between 2026 and 2030?

-

USD 4.23 billion, at a CAGR of 11%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Eyewear, Electronics, Solar, Automobile, and Others), Technology (Vacuum deposition, Electron beam evaporation, Sputtering, Roll to roll, and Others), Type (Multi layered, and Single layered) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for anti-reflective coatings in solar industry, Fluctuations in raw material prices

-

-

Who are the major players in the Anti-reflective Coatings Market?

-

Abrisa Technologies, AccuCoat Inc., AGC Inc., AMETEK Inc., Carl Zeiss AG, Cascade Optical Corp., Esco Optics Inc., EssilorLuxottica, Gooch and Housego Plc, Hoya Corp., iCoat Company LLC, Materion Balzers Optics, Nippon Sheet Glass Co. Ltd., Omega Optical Holdings LLC, Optical Coatings Japan, Optics and Allied Engg. Ltd., PFG Precision Optics Inc., Viavi Solutions Inc. and Vortex Optical Coatings Ltd.

-

Market Research Insights

- Market dynamics are shaped by a continuous push for higher performance against persistent cost pressures. The adoption of durable ar coatings in consumer electronics has been shown to reduce warranty claims related to screen damage by over 10%.

- In the solar sector, high-transmission optical coatings can increase energy yield by up to 4%, directly impacting the financial viability of large-scale projects. Innovations in custom thin-film coatings for specialized sectors like aerospace and medical devices allow for product differentiation.

- Companies that successfully balance the R&D investment required for precision optical ar coatings with scalable production methods achieve a significant competitive advantage. This balance is critical as manufacturing efficiencies, such as reducing material waste by 15% through optimized processes, are key to profitability.

We can help! Our analysts can customize this anti-reflective coatings market research report to meet your requirements.

RIA -

RIA -