APAC Processed Meat Market Size 2024-2028

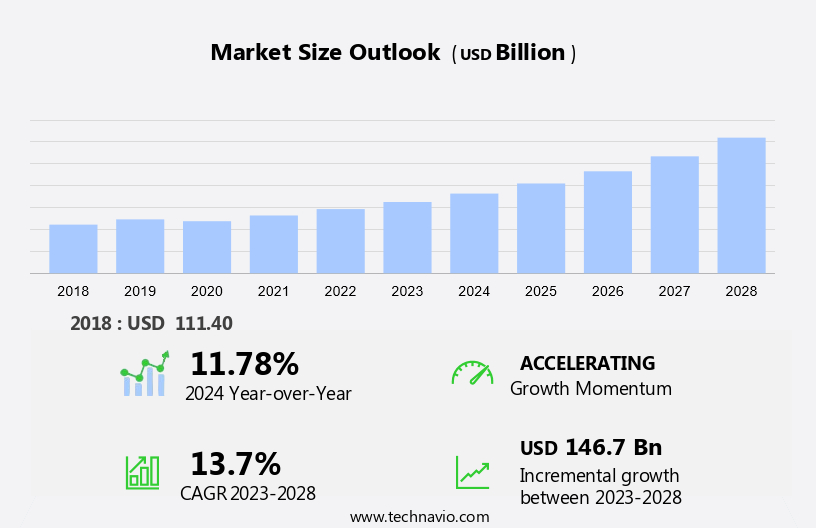

The APAC processed meat market size is forecast to increase by USD 146.7 billion at a CAGR of 13.7% between 2023 and 2028. The market is experiencing significant growth due to the increasing preference for convenience foods and packaging innovations. However, the market faces challenges from health concerns, particularly those related to red meat and processed meats, which have been linked to an increased risk of cancer. The fresh meat sector, including poultry and eggs, is gaining popularity as a healthier alternative. The poultry sector, in particular, is witnessing a surge in demand due to its integration into Westernized culture and the popularity of Mediterranean cuisines. Despite these trends, microbial contamination remains a concern for the processed meat industry, necessitating stringent regulations and safety measures. To mitigate these challenges, companies are focusing on product innovation and improving food safety standards to cater to the evolving consumer preferences and regulatory requirements.

The processed meat market in APAC is witnessing significant growth due to various factors. The region's population is increasingly adopting protein-rich diets, leading to a rise in demand for meat products. This trend is particularly prominent among the millennial demographic. Food processing technologies, including high-pressure processing and freezing techniques, are gaining popularity in the APAC processed meat market. These methods help enhance the shelf life of meat products, making them an attractive option for both retail and institutional sectors. The retail sector is a major contributor to the growth of the market.

The availability of a wide range of packaged food products, including processed meat and beverages, has made it convenient for consumers to incorporate protein-rich foods into their diets. The institutional sector, including schools, hospitals, and offices, is another significant market for processed meat in APAC. The convenience and affordability of ready-to-eat food products make them a popular choice for this sector. The food service industry, including quick-service restaurants and cafes, is also driving the demand for processed meat in APAC. The fast-paced lifestyles of consumers in the region have led to an increase in the consumption of convenient and flavorful meat products.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2017-2022 for the following segments.

- Application

- Commercial

- Residential

- Product

- Frozen

- Chilled

- Canned

- Geography

- APAC

- China

- India

- Japan

- APAC

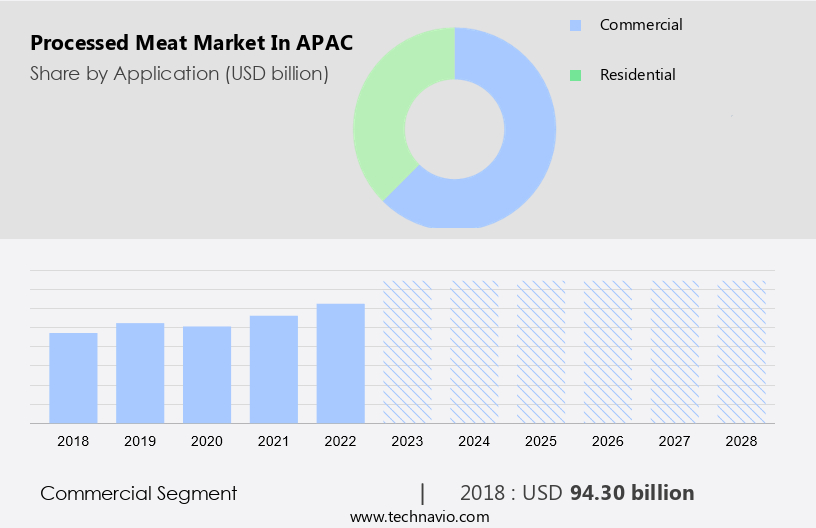

By Application Insights

The Commercial segment is estimated to witness significant growth during the forecast period.In the Asia Pacific (APAC) region, the processed meat market caters significantly to the commercial sector. This segment comprises establishments such as restaurants, fast-food chains, hotels, catering services, and food service suppliers. The convenience, consistent flavor, and customer preference for quick, ready-to-eat meals fuel the demand for processed meats in this sector. Processed meat products widely used in the commercial sector include burger patties, pizza toppings, and breakfast items like bacon and sausages. Fast-food chains in APAC rely heavily on processed meat, particularly beef and chicken patties, to create their signature burgers. Popular pizza toppings consist of processed meats such as pepperoni, sausage, and ham.

Hotels offer a variety of processed meat options, including bacon and sausages, as part of their breakfast and brunch buffets. To maintain the shelf life and ensure the freshness of these products, freezing techniques are extensively used in the processed meat industry. Retail sales and online platforms are crucial channels for the distribution of processed meat products. Consumers increasingly seek healthier meat options, leading to the development of reduced-fat, reduced-sodium, and additive-free processed meat products. Premium meat options, such as organic and grass-fed, also hold a growing share in the market.

Get a glance at the market share of various segments Request Free Sample

The Commercial segment accounted for USD 0.00 billion in 2017 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

APAC Processed Meat Market Driver

Increasing demand for convenience foods is the key driver of the market. Processed meat products, including salami, bacon, and various packaged offerings, have gained significant popularity in Asia Pacific (APAC) due to their umami taste and convenience. The rise in disposable income and changing lifestyles have fueled the demand for these foods. companies catering to this market offer processed meat in various forms, such as chilled, frozen, and canned, to meet diverse consumer preferences. To expand their reach, manufacturers are partnering with local meat producers, distributors, and technology providers through joint ventures and collaborations. These strategic alliances enable them to offer a wider range of organic meat products, which are increasingly preferred by health-conscious consumers.

Organic animal husbandry practices and the use of natural curing agents, such as nitrites and nitrates, are becoming essential in the production of processed meat to cater to evolving consumer preferences. The convenience of processed meat products, coupled with their versatility for use in various dishes through glazing and braising techniques, continues to attract consumers in APAC. The market for processed meat is expected to grow steadily due to these factors and the increasing penetration of e-commerce platforms, making these products easily accessible to consumers at their doorsteps.

APAC Processed Meat Market Trends

Growing emphasis on packaging innovations is the upcoming trend in the market. In the APAC processed meat market, companies employ innovative packaging solutions to gain a competitive edge. These packaging strategies not only attract consumers but also extend the product's shelf life and durability. Innovative packaging technologies, such as modified atmosphere packaging (MAP), vacuum packaging, and vacuum skin packaging, are increasingly being adopted. For example, Tyson Foods Inc. Employs vacuum packing for various fresh and frozen meat offerings. Air-permeable packages remain popular, but advanced packaging technologies offer enhanced freshness retention, discoloration prevention, and microbial control. These advancements are crucial as the processed meat industry continues to evolve, ensuring consumer satisfaction and product longevity.

APAC Processed Meat Market Challenge

Health hazards associated with processed meat is a key challenge affecting the market growth. Processed meat consumption in APAC is facing challenges due to health concerns. The World Health Organization's International Agency for Research on Cancer has classified red meat and processed meat as carcinogenic to humans. This revelation has led to growing awareness about the health risks, causing consumers to reconsider their meat consumption. Instead, there is a trend towards healthier and plant-based alternatives. Microbial contamination is another issue plaguing the processed meat industry. Celery powder, a common additive, has been identified as a potential source of contamination. This issue has raised concerns about food safety, further limiting the appeal of processed meats.

In contrast, fresh meat and poultry meat continue to be popular choices. The poultry sector is witnessing growth due to its perceived health benefits. Eggs are another alternative to processed meat that are gaining popularity in the region. The Westernized culture and Mediterranean cuisines that heavily feature processed meats are losing ground to healthier eating habits. As consumers become more conscious of their health, the demand for processed meats is expected to decrease. In conclusion, the market is facing challenges due to health concerns and food safety issues. Consumers are shifting towards healthier alternatives, and the trend is expected to continue.

The processed meat industry needs to adapt to these changing consumer preferences to remain competitive.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Al Aali Exports Pvt. Ltd. - In the Asia Pacific region, our company provides a diverse range of processed meat products, including buffalo carcasses, buffalo veal meat, offals, and mutton. These offerings cater to various market segments and consumer preferences.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Al Aali Exports Pvt. Ltd.

- Al Kabeer Exports Pvt. Ltd.

- Allanasons Pvt. Ltd.

- BRF SA

- Cargill Inc.

- Charoen Pokphand Foods PCL

- FRESHTOHOME FOODS Pvt. Ltd.

- IB Group

- Itoham Foods Inc.

- JBS SA

- Mirha Exports Pvt. Ltd.

- MK Overseas Pvt. Ltd.

- NH Foods Ltd.

- Prabhat Poultry Pvt. Ltd.

- Suguna Foods Pvt. Ltd.

- Suzannes Food

- The Meat Products of India Ltd.

- Tyson Foods Inc.

- VH Group

- VISSAN

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

In the Asia Pacific region, the processed meat market is witnessing significant growth due to the increasing adoption of protein-rich diets and the convenience offered by processed meat products. With dietary habits shifting towards more convenient and quick meal options, the retail sector, institutional sector, and food service industry are witnessing an uptick in demand for processed meat. Food processing technologies such as high-pressure processing and freezing techniques are being employed to enhance the shelf life of these products, making them more accessible to consumers. Retail sales of processed meat are booming, with both online platforms and traditional grocery stores witnessing robust growth.

Health-conscious consumers are seeking out healthier meat options, leading to the development of reduced fat, sodium, and additive-free processed meat products. Premium meat options, including sausages, ham, and bacon, are also gaining popularity, particularly in the millennial demographic. The processed meat market in the Asia Pacific region includes a wide range of products, from fresh processed meat to raw fermented and raw cooked meat, pre-cooked meat, cured meat, dried meat, chilled meat, frozen meat, and canned meat. Processing technologies such as salting, curing, smoking, and glazing are used to enhance the nutritional value and umami taste of these meat products.

Despite the health concerns associated with processed meats, particularly red meat and poultry meat, the market is expected to continue its growth trajectory due to the region's Westernized culture and the popularity of Mediterranean cuisines, which feature flavored meat products, herbs, marinades, and seasonings. However, concerns over microbial contamination and cancer risks remain, particularly in the poultry sector, which is also a significant contributor to the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

142 |

|

Base year |

2023 |

|

Historic period |

2017-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.7% |

|

Market growth 2024-2028 |

USD 146.7 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

11.78 |

|

Key companies profiled |

Al Aali Exports Pvt. Ltd., Al Kabeer Exports Pvt. Ltd., Allanasons Pvt. Ltd., BRF SA, Cargill Inc., Charoen Pokphand Foods PCL, FRESHTOHOME FOODS Pvt. Ltd., IB Group, Itoham Foods Inc., JBS SA, Mirha Exports Pvt. Ltd., MK Overseas Pvt. Ltd., NH Foods Ltd., Prabhat Poultry Pvt. Ltd., Suguna Foods Pvt. Ltd., Suzannes Food, The Meat Products of India Ltd., Tyson Foods Inc., VH Group, and VISSAN |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles,market forecast , fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -