Api Security Management Platforms Market Size and Growth Forecast 2026-2030

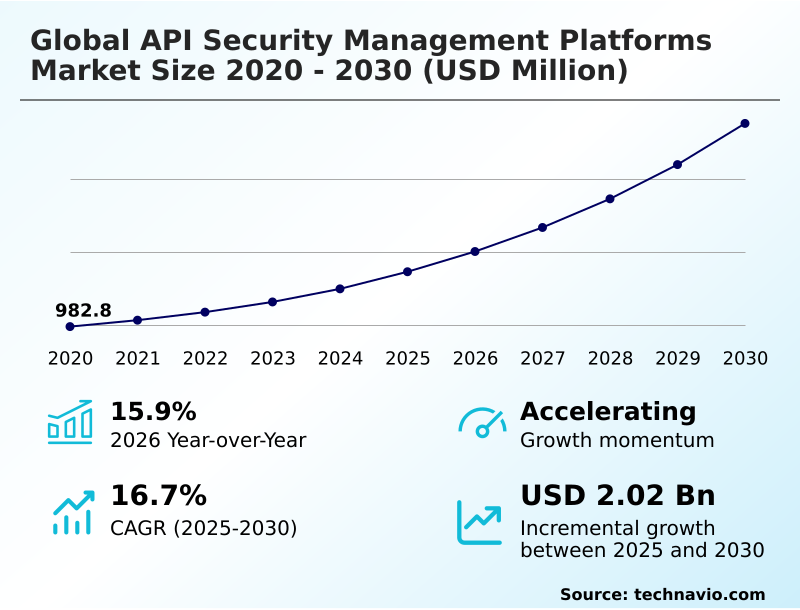

The Api Security Management Platforms Market size was valued at USD 1.73 billion in 2025 growing at a CAGR of 16.7% during the forecast period 2026-2030.

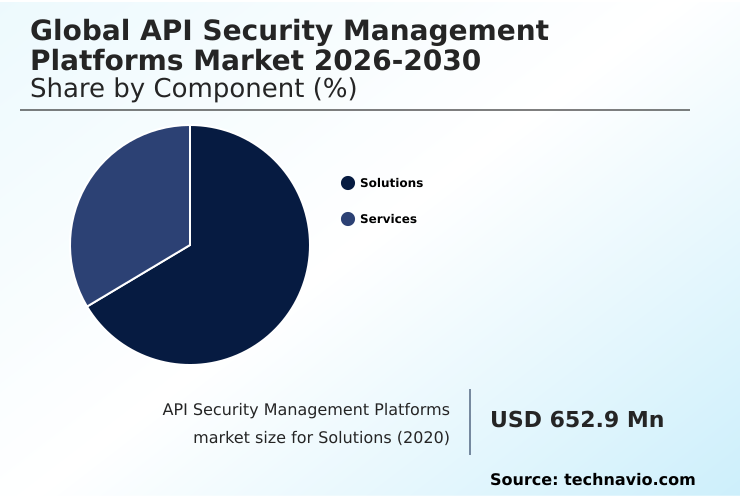

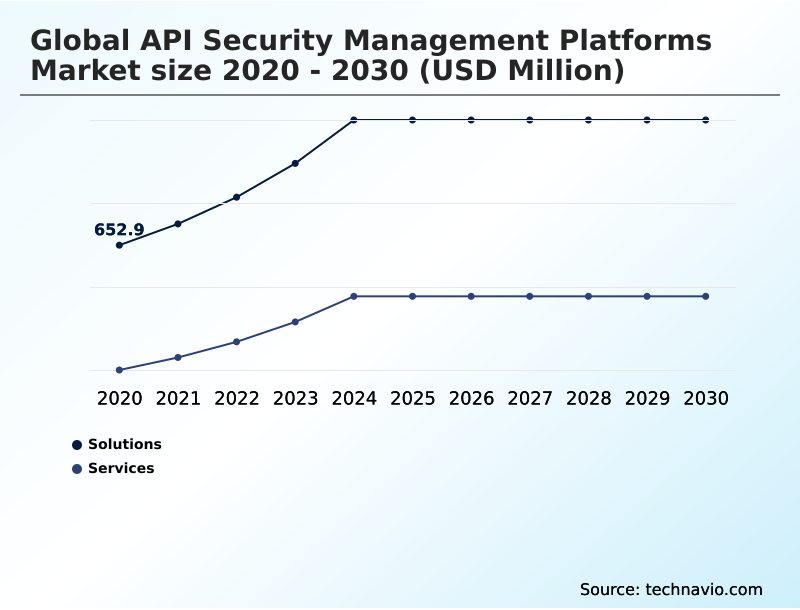

North America accounts for 36.1% of incremental growth during the forecast period. The Solutions segment by Component was valued at USD 976.9 million in 2024, while the Cloud-based segment holds the largest revenue share by Deployment.

The market is projected to grow by USD 2.77 billion from 2020 to 2030, with USD 2.02 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Api Security Management Platforms Market Overview

The API security management platforms market is defined by a fundamental shift toward protecting the connective interfaces of modern software, with a year-over-year growth of 15.9% underscoring its importance. As North America contributes over 36% of the incremental growth, enterprises are heavily investing in platforms that provide deep visibility and automated protection. For instance, a financial institution implementing an open banking strategy under PSD2 regulations deploys a dedicated api security gateway to enforce strict api authentication and authorization for all third-party connections. This zero trust api security approach prevents sensitive data exposure and ensures compliance, with behavioral analytics engines monitoring for anomalous patterns indicative of credential stuffing or broken object level authorization attacks. This strategic focus on securing the data exchange layer is now a cornerstone of enterprise risk management, moving beyond simple perimeter defenses to address the granular nature of application-to-application communication.

Drivers, Trends, and Challenges in the Api Security Management Platforms Market

The growth trajectory for API security management platforms is significantly influenced by the increasing complexity of digital ecosystems and the financial repercussions of security failures. The cost of an API security breach extends beyond immediate remediation, encompassing regulatory fines, customer churn, and long-term brand damage, making proactive security a critical investment.

Organizations are evaluating unified api protection platform benefits, which consolidate discovery, testing, and runtime defense into a single console. A key development is the use of ai for api security threat detection, where machine learning models analyze traffic to identify and block sophisticated attacks in real time.

For instance, a major e-commerce platform leverages these tools for protecting apis from automated bot attacks that attempt inventory hoarding or credential stuffing, ensuring compliance with PCI DSS. Integrating api security in ci/cd pipeline is another critical focus, enabling developers to remediate vulnerabilities early. However, multi-cloud api security challenges, such as inconsistent policy enforcement and lack of visibility, persist.

The debate over api security vs web application firewall efficacy continues, though specialized platforms demonstrate superior performance in detecting logic-based attacks.

As the market evolves, understanding graphql vs rest api security issues becomes essential for tailoring defenses, while the demand for transparent api security management solutions pricing grows, especially among small and medium enterprises seeking scalable protection for assets like api security for iot devices.

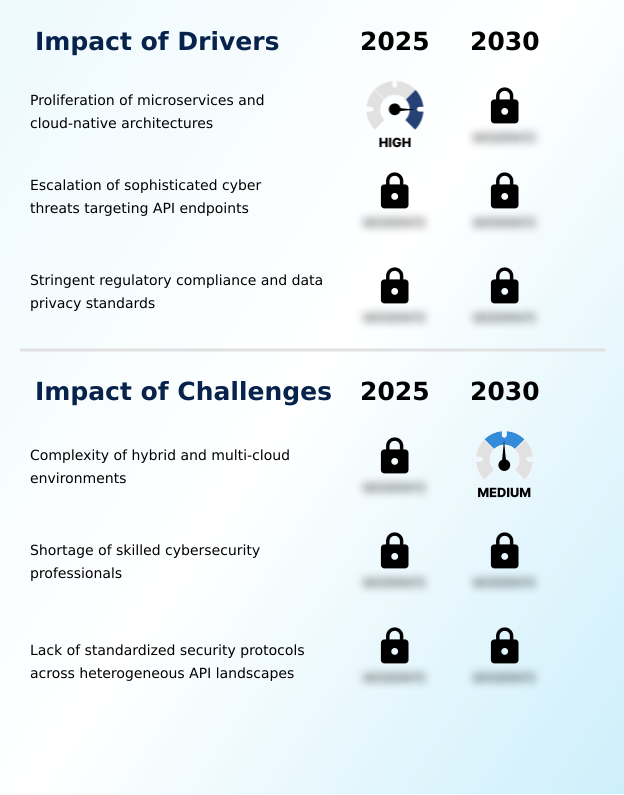

Primary Growth Driver: The rapid proliferation of microservices and cloud-native architectures is a primary market driver, expanding the digital attack surface and necessitating specialized security controls.

The market's expansion, marked by a 15.9% year-over-year growth rate, is fundamentally driven by two interconnected factors: architectural evolution and a rising threat landscape.

The widespread adoption of microservices security principles has deconstructed monolithic applications, creating thousands of new API endpoints that require specialized protection.

This explosion of interfaces necessitates robust api discovery and inventory management to identify and secure all potential entry points, including unmanaged or shadow APIs. Simultaneously, attackers are increasingly targeting vulnerabilities outlined in frameworks like the owasp api security top 10.

This requires enterprises to invest in platforms that offer advanced api threat protection and automated remediation capabilities to defend against logic-based attacks that traditional firewalls often miss.

Emerging Market Trend: The proliferation of artificial intelligence and machine learning is a defining market trend, enabling advanced capabilities in automated threat remediation and behavioral analysis.

Key market trends are converging around automation and intelligence to counter sophisticated threats. The integration of ai for api security is central to this shift, enabling platforms to move beyond static rules to proactive, behavioral-based threat detection. This is particularly crucial as organizations adopt complex microservices architectures, which are projected to drive the market's 15.9% year-over-year growth.

The consolidation of security functions into unified web application and api protection (waap) platforms is another significant development, providing a single management plane for both web and API assets. This trend simplifies operations and enhances api posture management by ensuring consistent policy application, from initial api security testing to ongoing monitoring in production environments.

Key Industry Challenge: The inherent complexity of securing and managing heterogeneous assets across hybrid and multi-cloud environments poses a significant challenge to market growth.

A primary challenge constraining market growth is the operational complexity of securing APIs across fragmented multi-cloud and hybrid environments. This heterogeneity impedes efforts to establish consistent multi-cloud api security policies and complicates api inventory management, making shadow api discovery a persistent issue.

The problem is compounded by a global shortage of skilled cybersecurity professionals with expertise in modern application architectures and logic-based threats. This talent gap makes it difficult for organizations, particularly small and medium enterprises, to manage sophisticated platforms and effectively respond to security alerts.

Without sufficient human oversight, even advanced tools for api security monitoring and api risk assessment may fail to deliver their full protective value.

Explore Full Market Dynamics Analysis Request Free Sample

Api Security Management Platforms Market Segmentation

The api security management platforms industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Component Segment Analysis

The solutions segment is estimated to witness significant growth during the forecast period.

The market is segmented by component, deployment, end-user, and geography. The solutions segment, which is projected to grow from a 2024 value of USD 976.9 million, represents the core of the market, providing the technological tools for api threat protection.

These platforms deliver essential capabilities such as automated api security, real-time monitoring, and robust api governance frameworks. As organizations expand their digital footprint, the demand for comprehensive solutions that offer runtime api security and effective api data protection intensifies.

These systems are critical for identifying vulnerabilities highlighted by standards like the owasp api security top 10 and ensuring secure data exchange across distributed architectures, making them a foundational investment for enterprise cybersecurity.

The Solutions segment was valued at USD 976.9 million in 2024 and showed a gradual increase during the forecast period.

Api Security Management Platforms Market by Region: North America Leads with 36.1% Growth Share

North America is estimated to contribute 36.1% to the growth of the global market during the forecast period.

The geographic landscape is led by North America, which accounts for approximately 36.1% of the market's incremental growth, driven by a high concentration of technology firms and stringent data privacy regulations.

Concurrently, the APAC region is forecast to expand at the fastest rate, with a CAGR of 17.9%, fueled by rapid digitalization in countries like India and China.

In Europe, adoption is strongly influenced by mandates such as the gdpr api compliance requirements, compelling organizations to implement rigorous api access control and data protection measures.

The global distribution of cloud infrastructure further necessitates cloud native api security solutions that can enforce consistent policies across jurisdictions. This regional divergence creates a complex but opportunity-rich environment for vendors.

Customer Landscape Analysis for the Api Security Management Platforms Market

The api security management platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the api security management platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Api Security Management Platforms Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the api security management platforms market industry.

42Crunch Ltd - Offerings include high-performance application delivery controllers with integrated endpoint protection and traffic analysis, designed to secure and manage modern distributed architectures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 42Crunch Ltd

- A10 Networks Inc.

- Akamai Technologies Inc.

- Amazon.com Inc.

- Axway Software SA

- Broadcom Inc.

- Cequence Security Inc.

- Check Point Software Tech Ltd.

- Cloudflare Inc.

- Data Theorem Inc.

- F5 Inc.

- Google LLC

- Kong Inc

- Microsoft Corp.

- Palo Alto Networks Inc.

- Salesforce Inc.

- Salt Security

- Thales Group

- Traceable AI

- Wallarm Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Api Security Management Platforms Market

- In May 2025, Cequence Security Inc. announced strategic partnerships with Skyfire and Inspira to enhance agentic AI security, strengthen bot defense capabilities, and improve protection against API-based threats.

- In April 2025, 42Crunch Ltd. released an update to its platform, deepening integrations with popular CI/CD tools to automate API contract security testing earlier in the development lifecycle, addressing the growing 'shift-left' security trend.

- In February 2025, the International Standards Organization published revised protocols for autonomous API authentication, establishing a new global benchmark to address threats like broken object level authorization and credential stuffing.

- In November 2024, F5 Inc. expanded its F5 Distributed Cloud Services to include advanced API discovery and posture management, providing organizations with unified visibility into both documented and shadow APIs across hybrid environments.

Research Analyst Overview: Api Security Management Platforms Market

The operational imperative to secure digital supply chains is driving significant investment in API security management platforms. A primary factor is the architectural shift to distributed systems, where the proliferation of interfaces mandates robust api governance and automated api security.

Boardroom decisions on cybersecurity budgets are now directly linked to the need for advanced api threat protection and compliance with regulations like GDPR. Solutions are a dominant market component, reflecting the demand for tools that manage the entire secure api lifecycle management, from api discovery and api security testing in pre-production to runtime api security in live environments.

Enterprises are prioritizing platforms that address the owasp api security top 10, particularly vulnerabilities like broken object level authorization (bola) and sensitive data exposure prevention. The adoption of web application and api protection (waap) unifies defenses, while technologies such as behavioral api security and zero trust api security provide granular api access control.

Effective api inventory management and api posture management are becoming standard practice, with api encryption and api rate limiting serving as foundational controls.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Api Security Management Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.7% |

| Market growth 2026-2030 | USD 2022.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.9% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, The Netherlands, Italy, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Api Security Management Platforms Market: Key Questions Answered in This Report

-

What is the expected growth of the Api Security Management Platforms Market between 2026 and 2030?

-

The Api Security Management Platforms Market is expected to grow by USD 2.02 billion during 2026-2030, registering a CAGR of 16.7%. Year-over-year growth in 2026 is estimated at 15.9%%. This acceleration is shaped by proliferation of microservices and cloud-native architectures, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), Deployment (Cloud-based, On-premises, and Hybrid), End-user (Large enterprises, and Small and medium enterprises) and Geography (North America, APAC, Europe, Middle East and Africa, South America). Among these, the Solutions segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, APAC, Europe, Middle East and Africa and South America. North America is estimated to contribute 36.1% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, The Netherlands, Italy, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is proliferation of microservices and cloud-native architectures, which is accelerating investment and industry demand. The main challenge is complexity of hybrid and multi-cloud environments, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Api Security Management Platforms Market?

-

Key vendors include 42Crunch Ltd, A10 Networks Inc., Akamai Technologies Inc., Amazon.com Inc., Axway Software SA, Broadcom Inc., Cequence Security Inc., Check Point Software Tech Ltd., Cloudflare Inc., Data Theorem Inc., F5 Inc., Google LLC, Kong Inc, Microsoft Corp., Palo Alto Networks Inc., Salesforce Inc., Salt Security, Thales Group, Traceable AI and Wallarm Inc. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Api Security Management Platforms Market Research Insights

Market dynamics are shaped by the aggressive adoption of cloud-native architectures, where the cloud-based deployment segment outpaces on-premises growth due to its scalability and lower upfront costs. This shift is particularly evident in regulated industries requiring strong api security for financial services and healthcare.

Procurement decisions are increasingly influenced by regulatory frameworks like the gdpr api compliance mandates in Europe, which necessitate robust data protection controls. Consequently, platforms that facilitate open banking api security and automate compliance are gaining prominence.

Decision-makers are prioritizing solutions that offer not only advanced threat detection but also comprehensive visibility for api security audit and risk assessment, ensuring resilience across an expanding and complex digital ecosystem.

We can help! Our analysts can customize this api security management platforms market research report to meet your requirements.

RIA -

RIA -