Autoimmune Drugs Market Size 2024-2028

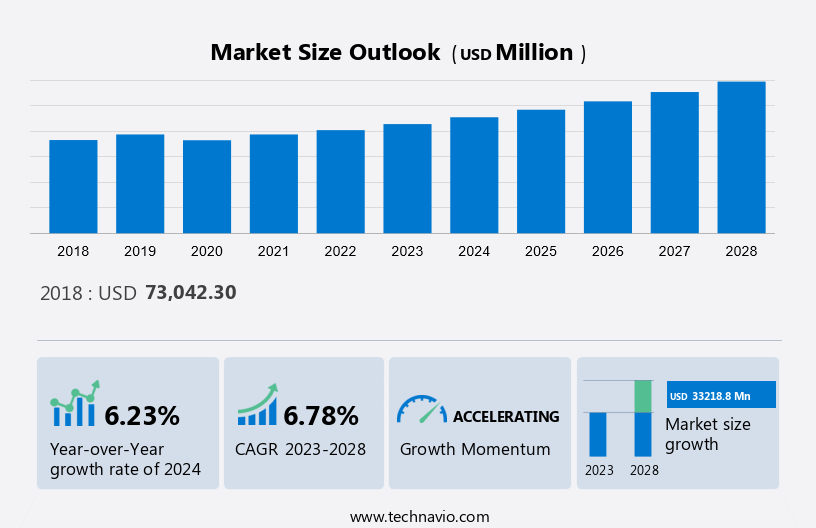

The autoimmune drugs market size is estimated to grow by USD 33.22 billion and at a CAGR of 6.78% between 2023 and 2028. Our company is a leading biotech firm, renowned for our robust Research and Development (R&D) pipeline. We are committed to advancing innovative therapeutic solutions, with a focus on the targeted mechanism of biologics. Our pipeline includes potential breakthroughs in various therapeutic areas, promising to address unmet medical needs. Additionally, we are dedicated to introducing affordable biosimilars, ensuring accessibility to life-changing treatments for a broader patient population. By combining scientific excellence with a patient-centric approach, we strive to transform lives and redefine the future of healthcare.

What will be the size of the Autoimmune Drugs Market Report During the Forecast Period?

To learn more about this report, Download Autoimmune Drug Market Research Report Sample Pdf

Market Dynamics

The market encompasses a range of pharmaceutical products designed to treat various autoimmune conditions, including Rheumatoid Arthritis, Inflammatory Bowel Disease, Ankylosing Spondylitis, and Psoriasis. These drugs work by suppressing the immune system's response, reducing inflammation, and managing symptoms. Anti-TNF therapy, which includes Etanercept, Adalimumab, Golimumab, Certolizumab pegol, and biosimilars, is a significant segment of the market. Salicylates derived from Willow spp and Aspirin are traditional treatments for inflammation. Non-steroidal anti-inflammatory drugs (NSAIDs) like Sulfasalazine, Azathioprine, Cyclophosphamide, and Gold compounds have long been used to manage autoimmune diseases. More recent additions to the market include Antimalarials, Cyclosporine, Interferon gamma, Folic acid, and Dihydroorotate dehydrogenase inhibitors. Regulatory T cells and Effector T cells are crucial targets for developing new therapeutic approaches. The market for autoimmune drugs is driven by the increasing prevalence of autoimmune diseases and the growing demand for effective treatments. The development of targeted therapies and the increasing use of biosimilars are expected to offer significant growth opportunities in the coming years. Our researchers analyzed the data with 2023 as the base year and the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The introduction of affordable biosimilars is notably driving market growth. Biologics used to treat autoimmune disorders are expensive, thus, they become unaffordable for the majority of patients. As a solution to the high cost of biologics, biosimilars are emerging as affordable therapies. Biosimilars are called follow-on biologics and are similar but not identical to biologics. They are priced 20%-25% less than originator biologics.

The number of clinical trials required for the approval of biosimilars is comparatively less than biologics, this directly reduces the cost of biologics. In addition, biosimilars do not have any post-marketing R&D costs or any marketing or market access expenses, because of which they are less expensive than biologics. The lower price of biosimilars compared with originator biologics is attracting healthcare providers to provide reimbursement for them. Thus, the introduction of biosimilars has increased access to advanced treatment options for patients with autoimmune disorders. Therefore, such factors will drive the autoimmune disease therapeutics market growth during the forecast period.

Significant Market Trends

The market dominance by TNF-alpha inhibitors is an emerging trend in the market. The global market is dominated by TNF-alpha inhibitors that are very effective as they target specific receptors on the cell surface. Some of the widely sold TNF-alpha inhibitors are HUMIRA, Enbrel, Cimzia, and SIMPONI, which are routinely prescribed as a first line of treatment for the management of autoimmune disorders, mainly rheumatoid arthritis, psoriasis, and multiple sclerosis.

Moreover, several efforts are being made to introduce a different class of drugs for autoimmune diseases. Some of the emerging drugs include the JAK kinase inhibitors that target the JAK kinase protein, a mechanism different from those of TNF-alpha inhibitors. Some of the marketed products under this category include XELJANZ and ACTEMRA. It is expected that in the future, they will have the potential to even replace some of the TNF-alpha inhibitors. Hence, such developments will boost the growth of the market in focus during the forecast period.

Major Market Challenge

The high cost of biologics is a major challenge impeding market growth. For autoimmune diseases, the therapeutic benefits offered by biologics outweigh the benefits of small molecules. Biologics not only have a targeted action but also have minimal side effects. However, the biggest challenge is the high cost of these miraculous therapies. Manufacturers continue to keep high prices for these treatments and state that manufacturing costs and clinical trials associated with biologics are responsible for the heavy price tags of biologics.

Biologics are manufactured by using living organisms. The production of biologics using bacterial systems is economical, but when monoclonal antibodies are used, the production costs more. The production of monoclonal antibodies requires immunization procedures to be done in animals such as rabbits, rats, and Guinea pigs, which are among the most important process in research and the costliest ones. Also, separate animal house facilities for raring animals, skilled labor, and government approvals for sacrificing animals add up to the cost of biologics. Due to high costs, the majority of patients with autoimmune diseases, mainly in developing nations, cannot afford biologics. Hence, these factors will hinder the market growth prospects during the market forecast period.

Key Market Customer Landscape

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Autoimmune Drugs Market Customer Landscape

Who are the Major Autoimmune Drugs Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AbbVie Inc. - The company offers conducts R&D, manufacturing, commercialization, and sale of innovative medicines and therapies to allocate resources and assess business performance on a global basis in order to achieve established long-term strategic goals. The key offerings of the company include autoimmune drugs.

The autoimmune drug market research report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

- AdvaCare Pharma

- Amgen Inc.

- AstraZeneca Plc

- Bristol Myers Squibb Co.

- Cardinal Health Inc.

- Delphis Pharmaceutical India

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- GlaxoSmithKline Plc

- Hikma Pharmaceuticals Plc

- Johnson and Johnson

- Medexus Pharmaceuticals Inc.

- Parvus Therapeutics Inc.

- Prometheus Laboratories Inc.

- Regeneron Pharmaceuticals Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize vendors as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

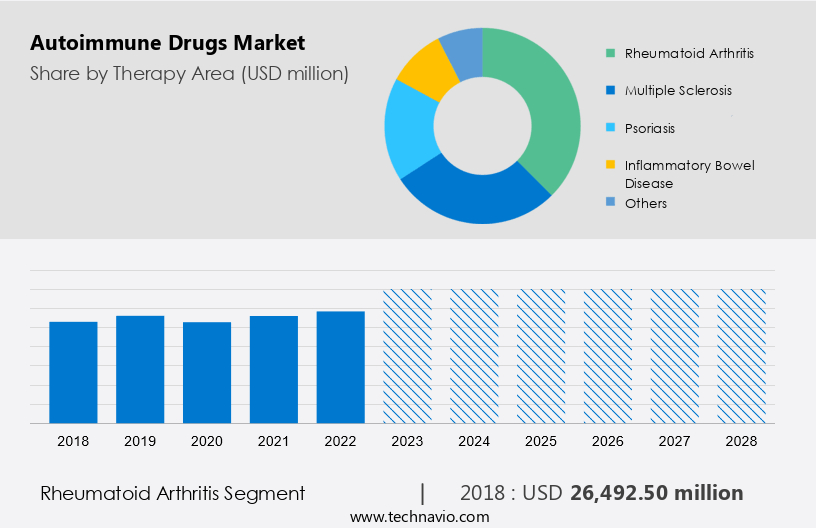

The market share growth by the rheumatoid arthritis segment will be significant during the market growth analysis period. Rheumatoid arthritis is an autoimmune disorder in which the immune system attacks the body's own cells, including the joints, which results in inflammation, pain, and swelling in the joints, mainly in the hands and feet. It is a chronic disease that can ultimately lead to joint deformity and bone erosion.

Get a glance at the market contribution of various segments Request Market Research Report Sample Pdf

The rheumatoid arthritis segment was valued at USD 26.49 billion in 2018. The incidence of rheumatoid arthritis is majorly increasing in the elderly population in several regions. The treatments available for rheumatoid arthritis include conventional DMARDs, small molecule therapeutics, and innovative biologics. Biologics have shown effective results in the long-term management of the disease and are widely prescribed by rheumatologists worldwide. Some of the blockbuster biologics include HUMIRA, Cimzia, SIMPONI, REMICADE, and STELARA. These agents are priced high but have huge worldwide sales, therefore, they significantly contribute to the market size of this segment. Furthermore, initiatives are being undertaken to develop innovative approaches to manage rheumatoid arthritis, and this is likely to propel the market growth. With the expiry of patents for many biologics under this category, the emergence of biosimilars and novel biologics will likely contribute to the gradual increase in market size. Novel treatment approaches are also evolving for this segment. Therefore, these factors are expected to accelerate the growth of this segment which is expected to propel the growth of the market in focus during the forecast period.

Key Region

For more insights on the market share of various regions Request Market Research Report Sample Pdf

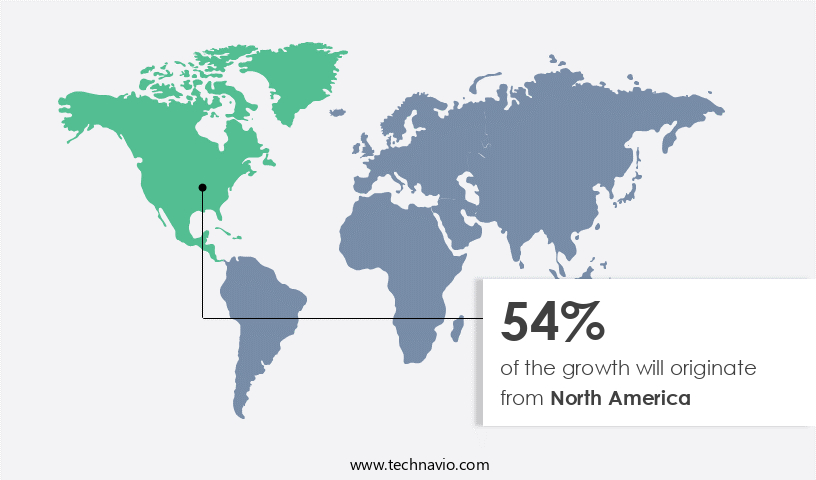

North America is estimated to contribute 54% to the growth of the global market during the market forecasting period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The US is the key country in North America, being a leader in the global market. The availability of advanced technical procedures for disease diagnosis and management, better healthcare awareness, and reimbursement policies for highly prevalent diseases, including autoimmune diseases, has resulted in the US being the biggest market in the Americas. Moreover, the sale of autoimmune drugs, including HUMIRA, Enbrel, REMICADE, STELARA, SIMPONI, ENTYVIO, ORENCIA, and XELJANZ, in the US, is also higher than in other countries.

Factors such as increasing incidence rates of autoimmune diseases and the prevalence of rheumatoid arthritis among the rising aging population in the US are attributed to the increasing market size of North America. Apart from this, there is a robust pipeline of autoimmune drugs in North America, which shows that the market in this region is going to proliferate during the forecast period. Another reason for the growth of the market in North America is the growing involvement of national institutes, including NIH, in developing advanced therapeutics in the autoimmune disease domain. Hence, such factors are expected to drive the growth of the regional market during the market research and growth period.

Segment Overview

The market report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments

- Therapy Area Outlook

- Rheumatoid arthritis

- Multiple sclerosis

- Psoriasis

- Inflammatory bowel disease

- Others

- Distribution Channel Outlook

- Hospital

- Pharmacy

- Drug store/Retail pharmacy

- Online

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- Asia

- China

- India

- Vietnam

- Others

- Rest of World

- Saudi Arabia

- South Africa

- Brazil

- Others

- North America

You may also be interested in:

- Immunotherapy Drugs Market Analysis North America, Europe, Asia, Rest of World (ROW) - US, Germany, UK, China, Japan - Size and Forecast

- Anti-inflammatory Therapeutics Market Analysis North America, Europe, Asia, Rest of World (ROW) - US, Germany, UK, Canada, China - Size and Forecast

- Autoimmune Disease Diagnostics Market Analysis North America, Europe, Asia, Rest of World (ROW) - US, Canada, UK, Germany, Japan - Size and Forecast

Market Analyst Overview

Autoimmune diseases, such as rheumatoid arthritis, inflammatory bowel disease, ankylosing spondylitis, psoriasis, and others, affect millions of people worldwide. These conditions are characterized by the immune system attacking healthy cells and tissues, leading to inflammation and damage. Treatment options for autoimmune diseases include various therapies, including Anti-TNF therapy, Salicylates derived from Willow spp and Aspirin, NSAID therapy, and Disease-modifying anti-rheumatic drugs (DMARDs). DMARDs include Glucocorticoids, Methotrexate, Leflunomide, Gold compounds, Sulfasalazine, Azathioprine, Cyclophosphamide, Antimalarials, D-penicillamine, and Cyclosporine. Biosimilars of these drugs are also available.

TNF receptor inhibitors, such as Etanercept, Adalimumab, Golimumab, and Certolizumab pegol, are effective in treating autoimmune diseases by blocking the action of TNF, a protein that plays a key role in inflammation. Other therapies include Interleukin-1 inhibitors, Interferon gamma, Folic acid, and Dihydroorotate dehydrogenase inhibitors. Immunosuppressants, such as regulatory T cells and effector T cells, play a role in managing autoimmune diseases. Cyclooxygenase inhibitors, like NSAIDs, reduce the production of prostaglandins, which contribute to inflammation.

Complement-dependent cytotoxicity and antibody-dependent cytotoxicity are other mechanisms used in the treatment of autoimmune diseases. Juvenile rheumatoid arthritis and psoriatic arthritis are common autoimmune diseases that affect the joints. Treatment for these conditions may include a combination of therapies, including DMARDs, biologics, and NSAIDs. In conclusion, the autoimmune drugs market caters to the growing demand for effective treatments for various autoimmune diseases. The market is expected to grow due to the increasing prevalence of these conditions and the development of new therapies.

|

Industry Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 33.22 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 54% |

|

Key countries |

US, Germany, Canada, China, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AbbVie Inc., AdvaCare Pharma, Amgen Inc., AstraZeneca Plc, Bristol Myers Squibb Co., Cardinal Health Inc., Delphis Pharmaceutical India, Eli Lilly and Co., F. Hoffmann La Roche Ltd., GlaxoSmithKline Plc, Hikma Pharmaceuticals Plc, Johnson and Johnson Services Inc., Medexus Pharmaceuticals Inc., Parvus Therapeutics Inc., Prometheus Laboratories, Regeneron Pharmaceuticals Inc., Sanofi SA, Takeda Pharmaceutical Co. Ltd., Teva Pharmaceutical Industries Ltd., and Wellona Pharma |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

Request Market Research Report Sample Pdf

What are the Key Data Covered in this Autoimmune Drugs Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the autoimmune drugs market between 2023 and 2027

- Precise estimation of the size of the autoimmune drugs market size and its contribution to the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the industry across North America, Europe, Asia, and Rest of World (ROW)

- A thorough analysis of the market’s competitive landscape and detailed information about vendors

- Comprehensive analysis of factors that will challenge the growth of autoimmune drugs market vendors

RIA -

RIA -