Immunotherapy Drugs Market Size 2025-2029

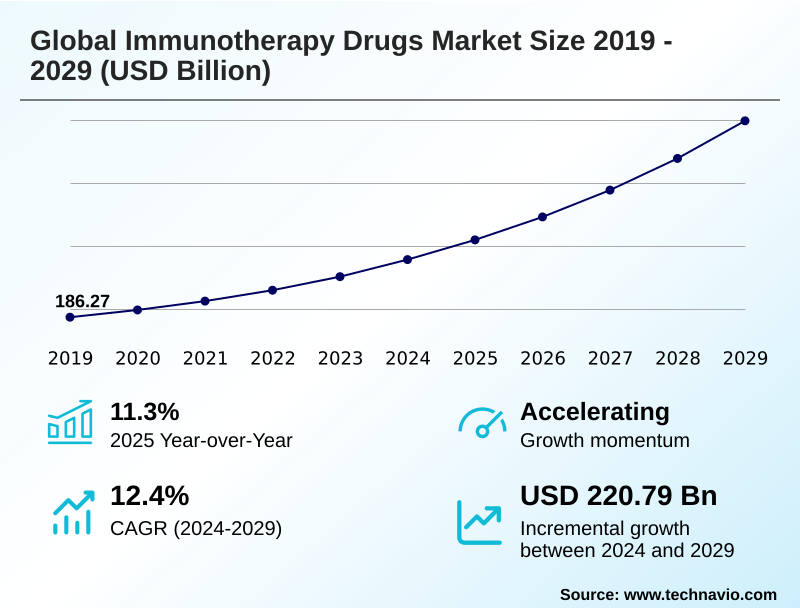

The immunotherapy drugs market size is valued to increase by USD 220.79 billion, at a CAGR of 12.4% from 2024 to 2029. Escalating incidence of chronic diseases and cancer will drive the immunotherapy drugs market.

Major Market Trends & Insights

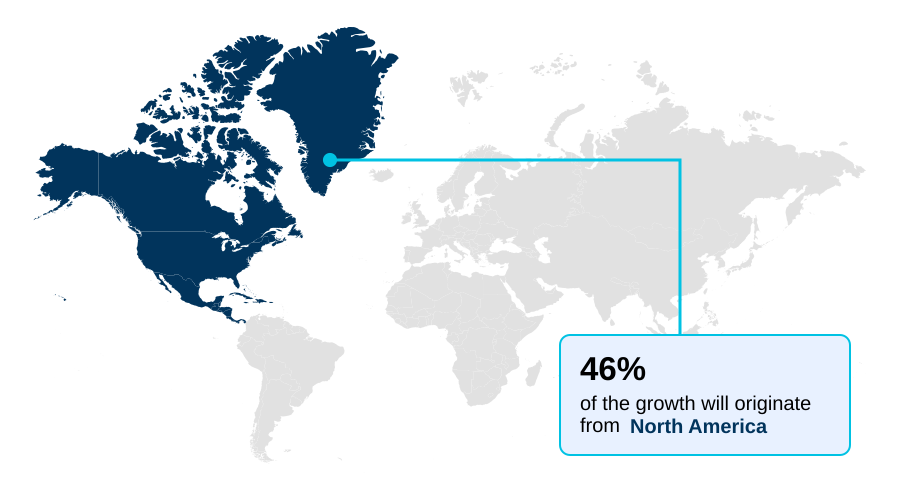

- North America dominated the market and accounted for a 45.6% growth during the forecast period.

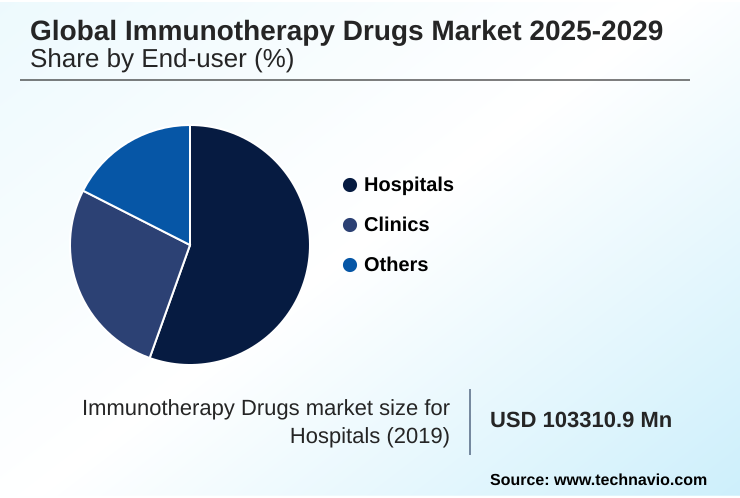

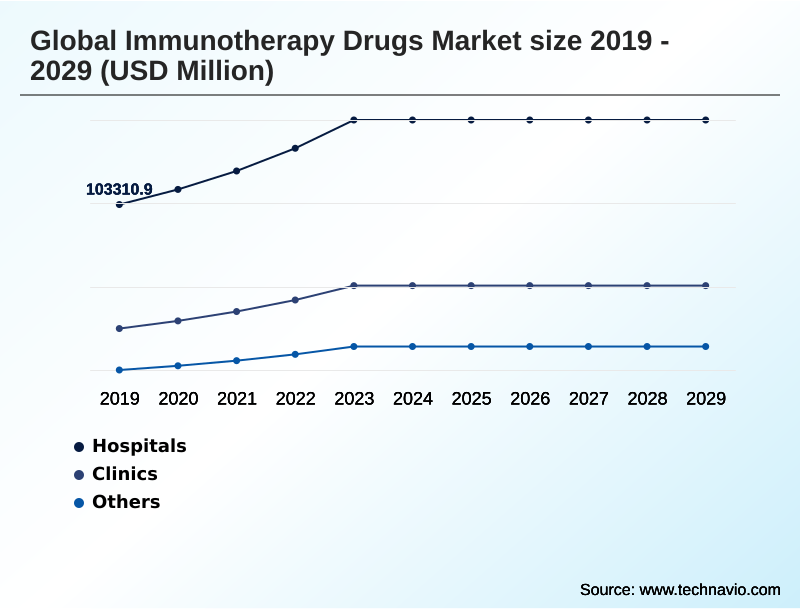

- By End-user - Hospitals segment was valued at USD 139.43 billion in 2023

- By Type - Monoclonal antibodies segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 312.42 billion

- Market Future Opportunities: USD 220.79 billion

- CAGR from 2024 to 2029 : 12.4%

Market Summary

- The immunotherapy drugs market is fundamentally reshaping disease treatment by leveraging the body's immune system. This expansion is driven by the increasing prevalence of chronic conditions, particularly cancer, creating a sustained demand for more effective therapies beyond traditional methods. Key innovations defining the market include the rise of personalized neoantigen therapies, such as mrna-based cancer vaccines, and advanced cell-based therapies.

- For instance, a biopharmaceutical firm specializing in chimeric antigen receptor (car) t-cell therapy must navigate an intricate supply chain. Optimizing this process to reduce vein-to-vein time is a critical business objective, as delays in the cryopreservation supply chain for autologous cell therapy can directly impact patient outcomes. This scenario underscores the operational complexities involved.

- Despite the transformative potential, the market contends with significant hurdles, including the high cost of treatment, mechanisms of therapeutic resistance, and the logistical challenges of manufacturing personalized medicines at scale, which temper the pace of widespread adoption.

What will be the Size of the Immunotherapy Drugs Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Immunotherapy Drugs Market Segmented?

The immunotherapy drugs industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Hospitals

- Clinics

- Others

- Type

- Monoclonal antibodies

- Vaccines

- Immune checkpoint inhibitors

- Others

- Therapeutic area

- Cancer

- Autoimmune and inflammatory diseases

- Infectious diseases

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

Hospitals remain the primary setting for administering advanced immunotherapies, particularly complex treatments such as chimeric antigen receptor (car) t-cell therapy.

The infrastructure required for managing potential immune-related adverse events and the severe complication of cytokine release syndrome necessitates this specialized environment. Analysis shows that 79% of autologous cell therapy infusions occur in inpatient settings, reflecting the logistical and clinical intensity.

However, the development of subcutaneous immunotherapy formulations is creating a shift toward outpatient care. Hospitals are navigating this transition through managed entry agreements and by establishing dedicated immuno-oncology toxicity management teams.

These efforts aim to balance the cost-effectiveness of immunotherapy with the complex demands of the cryopreservation supply chain and aseptic processing for biologics.

The Hospitals segment was valued at USD 139.43 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Immunotherapy Drugs Market Demand is Rising in North America Get Free Sample

The geographic landscape of the immunotherapy drugs market is characterized by established leadership and high-growth frontiers.

North America remains the dominant region, accounting for 45.6% of the market's incremental growth, driven by a robust R&D ecosystem and high adoption rates of novel treatments like adoptive cell transfer.

Europe follows, with a strong focus on rigorous clinical validation. However, the Asia Pacific region is emerging as the fastest-growing market, with significant investments in building domestic manufacturing and research capabilities.

Across all regions, a key operational trend is the shift to more efficient administration methods.

The development of targeted immunomodulatory therapies that can be administered in under 10 minutes, a significant reduction from previous infusion times, is expanding access beyond specialized centers.

This evolution, supported by decentralized clinical trials and evolving regulatory pathways for biologics, is democratizing access to advanced treatments.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the immunotherapy drugs market is marked by a strategic pivot from broad-acting agents to highly specific platforms. This shift is reshaping clinical practice and creating new value streams, but also introduces significant operational complexities.

- For instance, managing cytokine release syndrome toxicity is a critical competency for centers administering advanced treatments, just as understanding the impact of gut microbiome on checkpoint inhibitors is vital for optimizing patient outcomes. The industry is actively pursuing strategies for overcoming checkpoint inhibitor primary resistance and advancing the use of car-t therapy for solid tumor treatment.

- A key focus is on logistical and manufacturing hurdles, including scaling autologous cell therapy manufacturing and navigating the complex regulatory approval for bispecific antibodies. The cost-benefit analysis of combination immunotherapies and the development of value-based pricing for cancer immunotherapies are central to ensuring market access.

- A stark operational contrast exists between the rapid deployment of subcutaneous delivery of monoclonal antibodies, which takes minutes, and the weeks-long, logistically intensive process for personalized cell therapies, which impacts facility planning and resource allocation. This highlights the ongoing need for innovation in both therapeutic design and delivery.

What are the key market drivers leading to the rise in the adoption of Immunotherapy Drugs Industry?

- The escalating global incidence of chronic diseases and cancer serves as a key driver for the immunotherapy drugs market.

- Pioneering technological innovation and robust R&D investment are primary market drivers, leading to more effective therapeutic options. The evolution of monoclonal antibodies into sophisticated antibody-drug conjugates and other therapeutic cancer vaccines is broadening the range of treatable conditions.

- The application of AI is accelerating drug discovery, enabling faster identification of candidates for combination immunotherapy strategies.

- This focus on innovation translates directly into improved patient outcomes; certain biomarker-driven patient selection strategies for new therapies have demonstrated an ability to improve recurrence-free survival by over 40% compared to previous standards of care.

- Furthermore, the systematic collection of real-world evidence is helping to build compelling cases for value-based healthcare models, ensuring that novel treatments like those involving tumor-infiltrating lymphocytes gain reimbursement and wider adoption.

What are the market trends shaping the Immunotherapy Drugs Industry?

- The ascendancy of personalized cancer vaccines marks an important upcoming market trend. This approach signifies a critical shift toward developing highly individualized treatments in oncology.

- Key trends are reshaping the market, driven by the pursuit of highly personalized medicine in oncology. The development of personalized neoantigen therapies, particularly mrna-based cancer vaccines, is at the forefront, with some combination approaches demonstrating a 44% reduction in recurrence risk for certain cancers.

- This move toward specificity is also evident in the rise of bispecific antibodies, which employ dual-targeting mechanisms to enhance efficacy. Concurrently, innovations in delivery, such as subcutaneous formulations, are reducing administration times from over 30 minutes to less than 10, expanding treatment accessibility beyond hospitals.

- These advancements, coupled with progress in oncolytic virus therapy and next-generation biotherapeutics, are broadening the scope of pan-cancer treatment approaches and accelerating advancements in cell therapy manufacturing.

What challenges does the Immunotherapy Drugs Industry face during its growth?

- The high cost of treatment and complex reimbursement hurdles present a key challenge affecting the industry's growth trajectory.

- Significant challenges constrain market growth, primarily related to therapeutic resistance and manufacturing complexity. Many patients develop therapeutic resistance mechanisms, creating a need for strategies aimed at overcoming checkpoint inhibitor resistance to agents like pd-1/pd-l1 inhibitors. Furthermore, the logistics for advanced cell-based therapies are formidable.

- The expansion of car-t for solid tumors is hampered by manufacturing bottlenecks, with a notable percentage of patients facing significant wait times. The process requires a robust cold chain logistics for cell therapy and highly controlled environments, with analysis showing nearly 80% of treatments necessitate costly inpatient administration.

- Developing scalable manufacturing for emerging allogeneic car-t therapies using automated bioreactor systems is a critical priority to address these operational and cost hurdles.

Exclusive Technavio Analysis on Customer Landscape

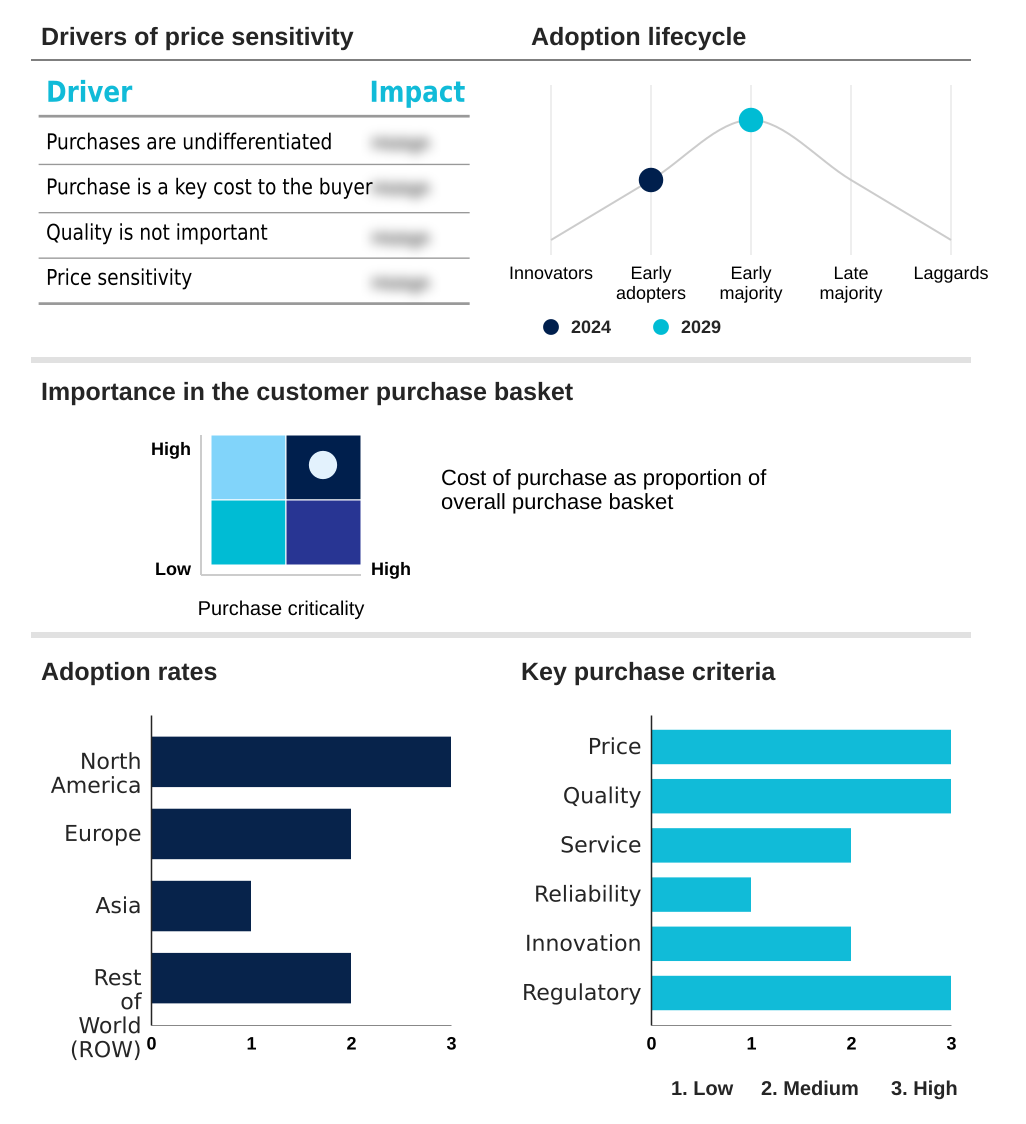

The immunotherapy drugs market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the immunotherapy drugs market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Immunotherapy Drugs Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, immunotherapy drugs market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - A portfolio focused on discovering, developing, and commercializing pharmaceutical products includes key immunotherapy drugs designed to address complex diseases through innovative biological mechanisms.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Amgen Inc.

- AstraZeneca Plc

- Bayer AG

- BioNTech SE

- Boehringer Ingelheim GmbH

- Bristol Myers Squibb Co.

- Celldex Therapeutics Inc

- F. Hoffmann La Roche Ltd.

- Genmab AS

- Gilead Sciences Inc.

- GlaxoSmithKline Plc

- Incyte Corp.

- Johnson and Johnson Services

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Teva Pharmaceutical Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Immunotherapy drugs market

- In August 2024, Galapagos and Adaptimmune Therapeutics announced a strategic collaboration valued at up to USD 665 million, granting Galapagos exclusive rights to a next-generation T-cell receptor T-cell therapy.

- In November 2024, the European Medicines Agency's committee recommended extending the indications for the nivolumab and ipilimumab combination to treat certain types of colorectal cancer.

- In April 2025, Health Canada approved the combination of pembrolizumab and chemotherapy for treating unresectable advanced or metastatic malignant pleural mesothelioma, providing a new first-line option.

- In May 2025, ANVISA authorized the continuation of a landmark domestic Brazilian clinical trial for a CAR-T cell therapy, expanding patient recruitment to a second phase across multiple centers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Immunotherapy Drugs Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.4% |

| Market growth 2025-2029 | USD 220790.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 11.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Russia, Spain, The Netherlands, China, Japan, India, South Korea, Singapore, Indonesia, Thailand, Brazil, Saudi Arabia, South Africa, Turkey, UAE and Australia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The immunotherapy drugs market is defined by a rapid innovation cycle, shifting the therapeutic paradigm toward highly personalized and potent treatments. Boardroom strategy is increasingly focused on acquiring and developing platforms for personalized neoantigen therapies and next-generation agents like bispecific antibodies and antibody-drug conjugates, which offer dual-targeting mechanisms.

- A key clinical development fueling this investment is the success of mrna-based cancer vaccines, which, in some trials, reduced melanoma recurrence risk by 44%. This landscape includes a diverse arsenal, from established monoclonal antibodies and immune checkpoint inhibitors (pd-1/pd-l1 inhibitors and ctla-4 inhibitors) to advanced modalities like chimeric antigen receptor (car) t-cell therapy and oncolytic virus therapy.

- The scientific frontier involves modulating the host immune system and the tumor microenvironment, with ongoing research into adoptive cell transfer, t-cell receptor therapies, and tumor-infiltrating lymphocytes.

- However, managing immune-related adverse events and the potentially severe cytokine release syndrome remains a clinical priority across all cell-based therapies, including both autologous cell therapy and emerging allogeneic car-t therapies, driving demand for new subcutaneous immunotherapy formulations.

What are the Key Data Covered in this Immunotherapy Drugs Market Research and Growth Report?

-

What is the expected growth of the Immunotherapy Drugs Market between 2025 and 2029?

-

USD 220.79 billion, at a CAGR of 12.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, Clinics, and Others), Type (Monoclonal antibodies, Vaccines, Immune checkpoint inhibitors, and Others), Therapeutic Area (Cancer, Autoimmune and inflammatory diseases, Infectious diseases, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Escalating incidence of chronic diseases and cancer, High cost of treatment and reimbursement hurdles

-

-

Who are the major players in the Immunotherapy Drugs Market?

-

AbbVie Inc., Amgen Inc., AstraZeneca Plc, Bayer AG, BioNTech SE, Boehringer Ingelheim GmbH, Bristol Myers Squibb Co., Celldex Therapeutics Inc, F. Hoffmann La Roche Ltd., Genmab AS, Gilead Sciences Inc., GlaxoSmithKline Plc, Incyte Corp., Johnson and Johnson Services, Novartis AG, Pfizer Inc., Sanofi SA and Teva Pharmaceutical Ltd.

-

Market Research Insights

- Market dynamics are shaped by a push toward personalized medicine in oncology and more efficient administration. For example, advancements in subcutaneous immunotherapy formulations have reduced administration times from over 30 minutes to under 10, a significant operational improvement for clinics.

- Concurrently, the development of next-generation biotherapeutics, informed by genomic sequencing for neoantigens and biomarker-driven patient selection, is leading to better patient outcomes. Certain combination immunotherapy strategies have demonstrated a 44% reduction in recurrence risk in high-risk patient cohorts. However, addressing therapeutic resistance mechanisms and improving the cost-effectiveness of immunotherapy remain central to expanding access.

- As the field matures, value-based healthcare models and managed entry agreements are becoming crucial for integrating these high-cost, high-efficacy treatments into standard care, balancing innovation with fiscal responsibility.

We can help! Our analysts can customize this immunotherapy drugs market research report to meet your requirements.

RIA -

RIA -