Automated Teller Machine (ATM) Market Size 2026-2030

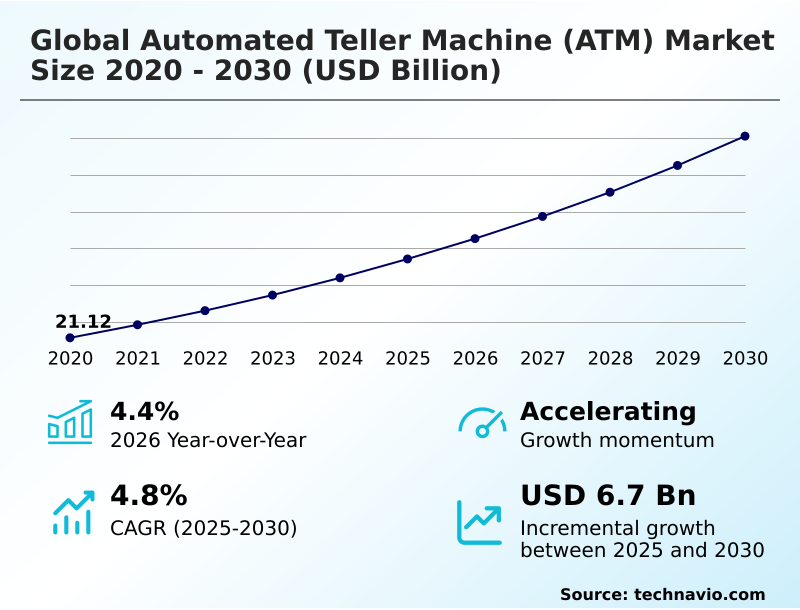

The automated teller machine (atm) market size is valued to increase by USD 6.70 billion, at a CAGR of 4.8% from 2025 to 2030. Proliferation of self-service banking and operational efficiency will drive the automated teller machine (atm) market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 43.6% growth during the forecast period.

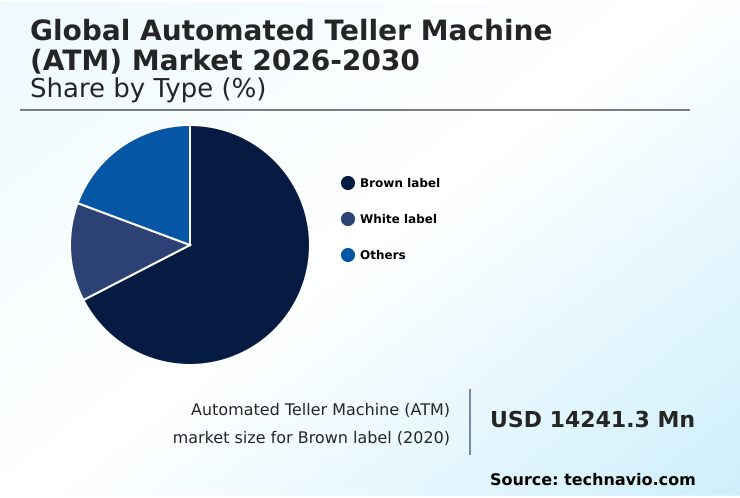

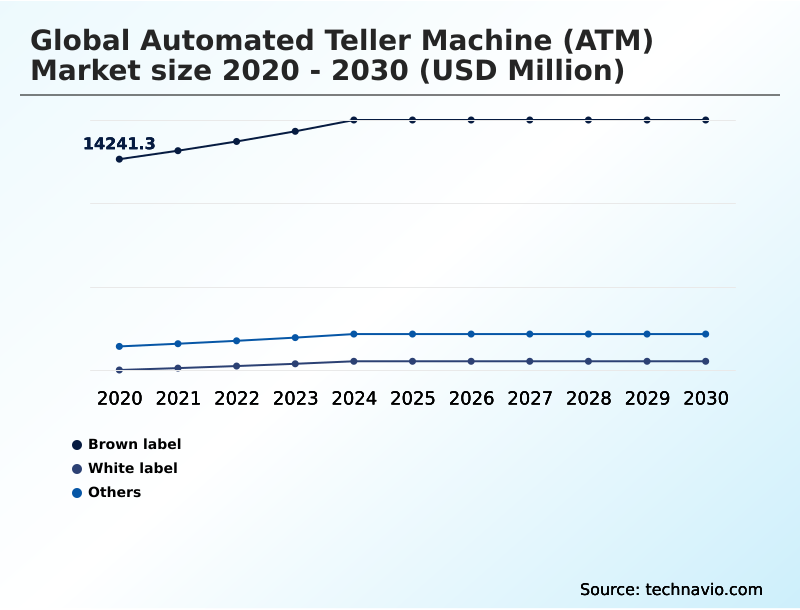

- By Type - Brown label segment was valued at USD 16.37 billion in 2024

- By Deployment - Offsite ATM segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 11.00 billion

- Market Future Opportunities: USD 6.70 billion

- CAGR from 2025 to 2030 : 4.8%

Market Summary

- The automated teller machine (atm) market is defined by a strategic transition toward advanced self-service banking solutions and integrated service models. While digital payments expand, the need for physical cash access remains a cornerstone of the financial infrastructure, particularly for promoting financial inclusion in developing economies.

- Growth is fueled by the replacement of legacy hardware with multi-function ATMs featuring innovations like cash recycling technology and biometric authentication. This evolution helps financial institutions improve operational efficiency and reduce costs associated with cash-in-transit. For instance, a typical branch transformation strategy involves deploying smart ATMs to handle complex tasks, allowing staff to focus on high-value advisory services.

- Concurrently, the ATM-as-a-service model is gaining traction, enabling banks to outsource ATM fleet management to specialized providers. This approach mitigates risks related to hardware obsolescence and cybersecurity while ensuring the physical touchpoint aligns with modern omnichannel banking experiences.

- The integration of ATM software with digital banking solutions is crucial for delivering a seamless customer journey, reinforcing the ATM's role as a vital bridge between physical and digital finance.

What will be the Size of the Automated Teller Machine (ATM) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automated Teller Machine (ATM) Market Segmented?

The automated teller machine (atm) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Brown label

- White label

- Others

- Deployment

- Offsite ATM

- Onsite ATM

- Others

- Solution

- Deployment solutions

- Managed services

- Geography

- APAC

- India

- China

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The brown label segment is estimated to witness significant growth during the forecast period.

The global automated teller machine (atm) market is segmented by type, deployment, and geography.

The brown-label ATM model allows a financial institution to expand its physical footprint using hardware owned by a service provider, with branding maintained by the sponsor bank.

This approach is critical for balancing service accessibility with fiscal constraints, driving operational efficiency. It enables network expansion into new areas without the high capital expenditure of full hardware ownership, optimizing cash management.

This segment leverages remote ATM monitoring and predictive maintenance to ensure high uptime.

As part of a broader branch transformation, this strategy reduces the total cost of ATM ownership, with some operators reporting a 15% reduction in annual maintenance-related expenses by outsourcing through these agreements, enhancing self-service banking capabilities.

The use of advanced ATM software is crucial for managing these distributed networks and ensuring secure transaction processing.

The Brown label segment was valued at USD 16.37 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automated Teller Machine (ATM) Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the global automated teller machine (atm) market is characterized by divergent growth patterns.

APAC is set to contribute over 43% of the market's incremental growth, driven by aggressive financial inclusion initiatives and the need for banking automation in rural areas.

This contrasts with mature regions like North America and Europe, where the focus is on ATM fleet modernization and implementing a cohesive branch transformation strategy.

In these markets, there is less emphasis on new unit deployment and more on upgrading to multi-function ATMs that support an omnichannel banking experience.

South America continues to prioritize ATM security and the deployment of offsite ATMs to serve its large unbanked population.

The Middle East and Africa present a dual market, with high-tech smart ATM deployments in affluent nations and a focus on basic, durable machines for financial inclusion elsewhere. This regional diversity requires adaptable ATM deployment solutions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the global automated teller machine (atm) market increasingly revolve around complex trade-offs. A cost-benefit analysis of ATM outsourcing often reveals that the ATM-as-a-service vs in-house management debate is central to modern operational planning. While outsourcing can lower upfront capital expenditure, it requires careful vendor selection to maintain service quality and security.

- The future of self-service banking channels depends on integrating ATMs with mobile banking applications, a trend that enhances user convenience but also expands the threat landscape. Accordingly, a deep understanding of security features in modern ATM models is non-negotiable for risk mitigation. Preventing jackpotting and black box attacks requires robust ATM software and hardware-level protections.

- In parallel, the benefits of cash recycling technology in banking are clear, with some institutions reporting cash handling cost reductions of over 25% compared to traditional models. The role of ATMs in emerging market financial inclusion remains pivotal, where a comparison of white-label vs brown-label ATMs shows different approaches to expanding access.

- Trends in ATM software development focus on open APIs and platform-based architectures to support these evolving demands. Ultimately, strategies for reducing ATM operational costs while meeting compliance requirements for ATM deployment define competitive positioning.

What are the key market drivers leading to the rise in the adoption of Automated Teller Machine (ATM) Industry?

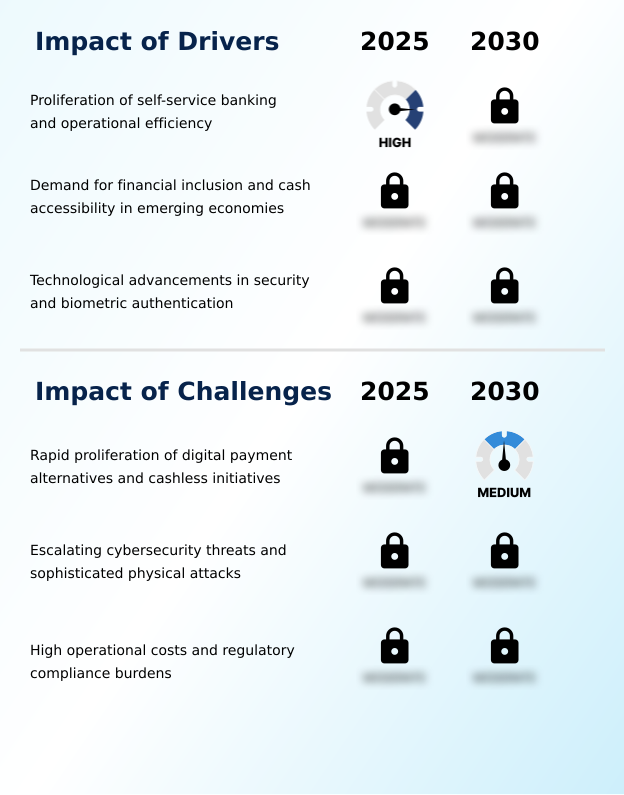

- The proliferation of self-service banking models, driven by the strategic imperative for greater operational efficiency, serves as a key driver for the market.

- Market growth is primarily driven by the strategic imperative for financial institutions to enhance operational efficiency and expand financial inclusion.

- The proliferation of self-service banking, supported by advanced payment processing software and fraud management solutions, allows banks to reduce reliance on costly physical branches. Cash recycling technology is a major catalyst, enabling a more efficient cash cycle.

- In emerging economies, the deployment of white-label ATMs and brown-label ATMs is critical for providing access to cash management services for unbanked populations.

- Furthermore, continuous advancements in ATM security, such as sophisticated anti-skimming technology and encrypted communication protocols, build consumer trust and are essential for regulatory compliance for ATMs, including adherence to payment card industry (pci) compliance standards.

What are the market trends shaping the Automated Teller Machine (ATM) Industry?

- The integration of artificial intelligence and predictive maintenance frameworks is an important emerging trend. This development is fundamentally reshaping operational strategies and service delivery models within the industry.

- Key trends are reshaping the market, with a strong emphasis on integrating artificial intelligence into ATM network management. The use of predictive analytics for cash demand is becoming standard, enabling operators to optimize cash levels and reduce the frequency of cash-in-transit, lowering operational costs by up to 15%. This data-driven approach enhances ATM uptime and availability.

- Another significant trend is the rise of the ATM-as-a-service outsourcing model, allowing financial institutions to leverage the expertise of a managed services provider (msp) for ATMs. This shift supports ATM fleet modernization without significant capital outlay.

- The focus on customer experience at the ATM is driving innovation in user interface (ui) for ATMs and the adoption of NFC technology for frictionless, cardless transactions, which improves transaction speeds by over 30%.

What challenges does the Automated Teller Machine (ATM) Industry face during its growth?

- The rapid and widespread proliferation of digital payment alternatives and cashless initiatives presents a significant challenge to the market's traditional growth trajectory.

- The primary challenge facing the industry is the increasing competition from digital-first payment systems, which impacts ATM transaction volume analysis. This necessitates a re-evaluation of the cost of ATM ownership and business models for the independent ATM deployer (iad).

- Additionally, the escalating sophistication of both logical and physical threats requires constant investment in cybersecurity for financial terminals and physical ATM security measures. These include defenses against jackpotting and black box attacks, which can lead to significant financial losses.

- Managing the complexities of ATM hardware procurement and the logistics of a global supply chain while adhering to evolving regulations presents another significant hurdle. The need for continuous software updates and patches to maintain a secure transaction processing environment adds to the operational burden for ATM operators.

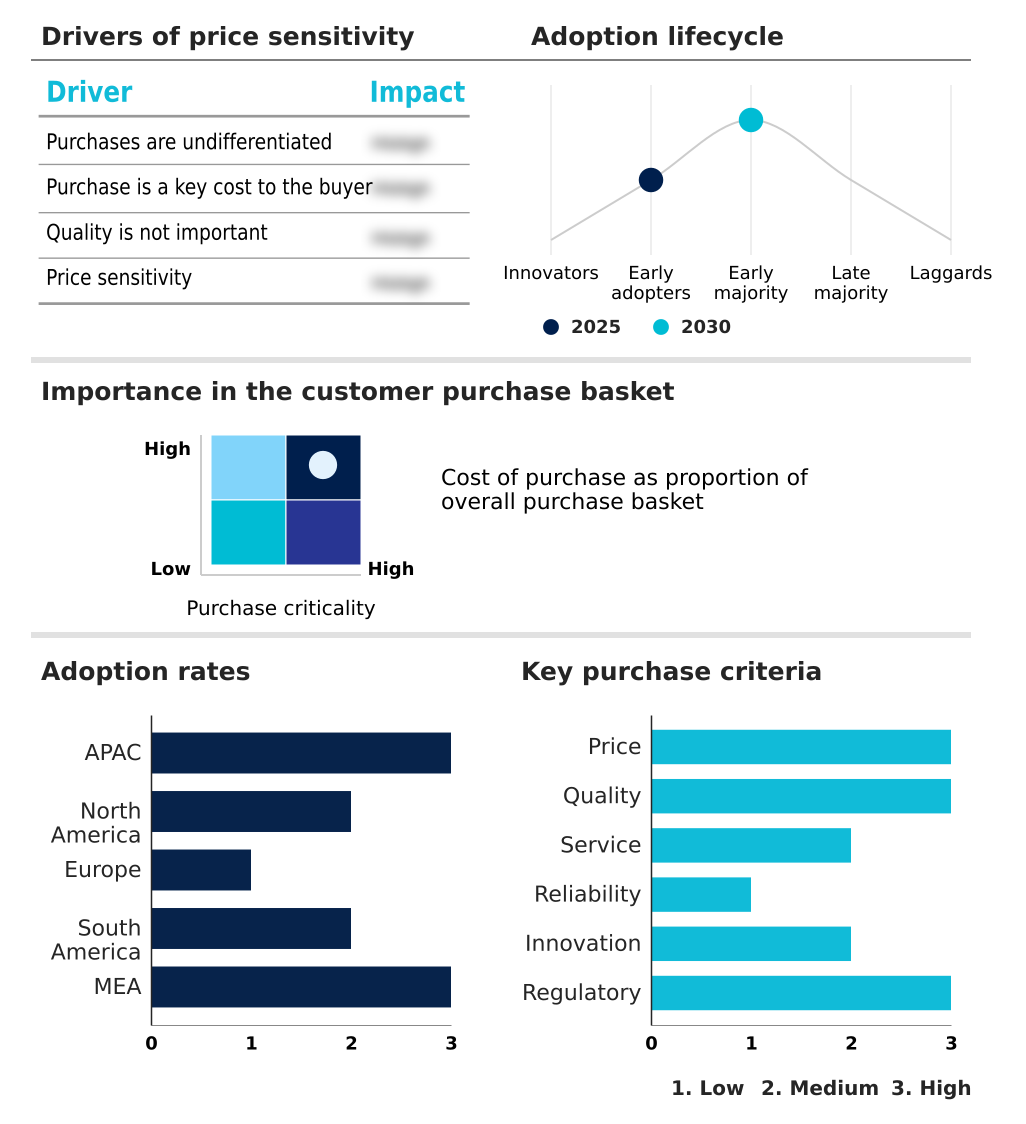

Exclusive Technavio Analysis on Customer Landscape

The automated teller machine (atm) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automated teller machine (atm) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automated Teller Machine (ATM) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automated teller machine (atm) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACI Worldwide Inc. - Key offerings center on ATM transaction processing, integrated payment software, and fraud management solutions designed for modern financial ecosystems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACI Worldwide Inc.

- Cennox Inc.

- CSG Systems International Inc.

- Euronet Worldwide Inc.

- Fidelity National Information

- Financial software and systems

- Hyosung TNS Inc.

- KAL ATM Software GmbH

- KEBA Group AG

- Loomis AB

- NCR Payment Solutions LLC

- Optima Systems Ltd.

- Parabit Systems Inc.

- Phoenix Interactive Design Inc.

- Sesami Inc.

- Sigma Spa

- STEMMER IMAGING AG

- Triton Systems

- Vortex Engineering Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automated teller machine (atm) market

- In August 2025, Die Nixdorf Inc. launched its new Branch Automation Solutions portfolio, offering pre-packaged managed services on a cloud-native platform to help financial institutions optimize operations and deliver seamless omnichannel experiences.

- In October 2025, Die Nixdorf Inc. announced that Bank AlJazira in Saudi Arabia became the first Middle Eastern bank to implement its VCP-Lite 7 self-service software on over 400 DN Series ATMs running Microsoft Windows 11.

- In February 2025, GRG Banking Equipment Co. Ltd. expanded its strategic initiatives in Africa with high-level visits to Egypt and Morocco to promote its intelligent banking equipment and explore opportunities for ATM and cash management solutions.

- In May 2025, Die Nixdorf Inc. announced that QNB is the first bank in the Middle East to deploy ATMs with bulk cash deposit capabilities using its technology, enhancing customer convenience as part of QNB's digital transformation strategy.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automated Teller Machine (ATM) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.8% |

| Market growth 2026-2030 | USD 6703.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | India, China, Japan, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global automated teller machine (atm) market is undergoing a significant evolution, moving beyond simple cash dispensation to become a cornerstone of modern self-service banking. The industry is characterized by the widespread adoption of cash recycling technology and advanced ATM software to improve operational efficiency.

- Key developments include the integration of biometric authentication and cardless transactions, which enhance ATM security while aligning with consumer expectations for seamless digital banking solutions. A critical focus is on branch transformation, where multi-function ATMs and self-service kiosks are deployed to handle routine transactions, allowing financial institutions to optimize staffing.

- For instance, the use of predictive maintenance algorithms has been shown to increase ATM fleet uptime by over 15%. This shift toward ATM-as-a-service and managed services allows banks to focus on core activities.

- The deployment of both onsite ATMs and offsite ATMs, including mobile and smart ATM variants, is tailored to meet diverse market needs, from urban convenience to rural financial inclusion. This requires sophisticated cash management and real-time monitoring.

What are the Key Data Covered in this Automated Teller Machine (ATM) Market Research and Growth Report?

-

What is the expected growth of the Automated Teller Machine (ATM) Market between 2026 and 2030?

-

USD 6.70 billion, at a CAGR of 4.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Brown label, White label, and Others), Deployment (Offsite ATM, Onsite ATM, and Others), Solution (Deployment solutions, and Managed services) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of self-service banking and operational efficiency, Rapid proliferation of digital payment alternatives and cashless initiatives

-

-

Who are the major players in the Automated Teller Machine (ATM) Market?

-

ACI Worldwide Inc., Cennox Inc., CSG Systems International Inc., Euronet Worldwide Inc., Fidelity National Information, Financial software and systems, Hyosung TNS Inc., KAL ATM Software GmbH, KEBA Group AG, Loomis AB, NCR Payment Solutions LLC, Optima Systems Ltd., Parabit Systems Inc., Phoenix Interactive Design Inc., Sesami Inc., Sigma Spa, STEMMER IMAGING AG, Triton Systems and Vortex Engineering Pvt. Ltd.

-

Market Research Insights

- Market dynamics are shaped by a strategic push toward ATM fleet modernization and a comprehensive branch transformation strategy. Financial institutions are adopting ATM-as-a-service models, which can reduce the total cost of ATM ownership by up to 20% compared to traditional in-house management.

- This shift is coupled with a focus on enhancing the omnichannel banking experience through self-service banking solutions that offer more than just cash withdrawals. The adoption of advanced ATM security features, including end-to-end encryption for ATMs and physical ATM security measures, is critical.

- The efficiency of cash-in-transit optimization improves significantly with cash recycling technology, with some networks reporting a 30% decrease in replenishment frequency. These trends underscore the industry's move toward highly efficient, secure, and integrated self-service channels.

We can help! Our analysts can customize this automated teller machine (atm) market research report to meet your requirements.

RIA -

RIA -