Automotive Racing Seat Market Size 2024-2028

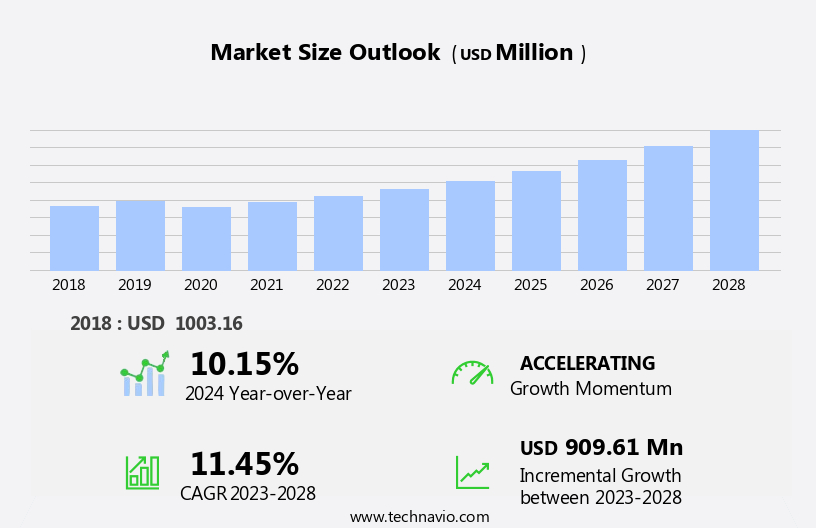

The automotive racing seat market size is forecast to increase by USD 909.61 million at a CAGR of 11.45% between 2023 and 2028.

- The market is experiencing significant growth, driven by several key trends. One of the primary factors fueling market expansion is the increasing focus on lightweighting of seats to achieve desirable emission levels and improve fuel economy. Additionally, the emergence of autonomous and electric vehicles is creating new opportunities for racing seat manufacturers. However, the market is also facing challenges, such as the growing taxation on luxury vehicles, which may impact the affordability of high-end racing seats. Overall, these trends and challenges are shaping the future growth trajectory of the market.

What will be the Size of the Automotive Racing Seat Market During the Forecast Period?

- The market caters to the demand for enhanced comfort, safety, and performance In the motorsports industry. As a spectator sport with a global following, racing continues to push the boundaries of technology. Racing seats are engineered to provide superior lateral support, ensuring driver safety during high-speed turns and gravity force. Technological advancements in racing seat design include the use of lightweight materials such as carbon fiber and natural fiber composites, which reduce weight and improve weight distribution. Consumer preferences for high-performance vehicles and racing events fuel the market's growth. Racing seats are no longer limited to high-end models; mid-segment cars, SUVs, and even OEMs are integrating racing seat technology as a luxury feature.

- Modular seats and memory seats cater to individual preferences, while powered seats offer added convenience. The integration of racing harnesses and advanced safety features further underscores the market's commitment to enhancing both driver and passenger experiences. The evolution of autonomous vehicles may present new opportunities for racing seat technology, as they offer a unique blend of performance and comfort.

How is this Automotive Racing Seat Industry segmented and which is the largest segment?

The automotive racing seat industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- High-performance

- Eco-performance

- Application

- Sports cars

- Rally vehicles

- Touring vehicles

- Geography

- Europe

- Germany

- Italy

- North America

- US

- APAC

- China

- Japan

- South America

- Middle East and Africa

- Europe

By Type Insights

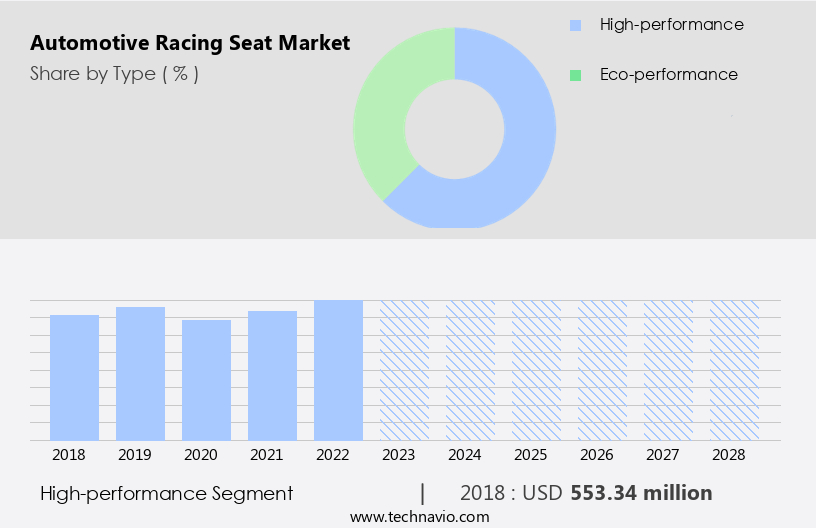

- The high-performance segment is estimated to witness significant growth during the forecast period.

In the realm of automotive racing, seats play a pivotal role in ensuring both driver safety and vehicle performance. Designed to restrict occupant movement during dynamic loads caused by high speeds and sudden maneuvers, these seats adhere to industry safety standards. High-performance racing seats, characterized by a one-piece construction, offer the necessary rigidity and strength for extreme conditions. The focus on safety and weight reduction outweighs comfort and luxury features. These seats are indispensable in motor sports, where the vehicle's performance and driver's agility are paramount. Carbon fiber and lightweight materials are common in high-performance racing seats, enhancing both durability and weight efficiency.

Consumer preferences lean towards lateral support, racing harnesses, and optimal weight distribution for optimal cornering. Environmental concerns have led to the exploration of natural fiber substitutes for carbon fibers and the reduction of fuel emissions. As urbanization continues to accelerate, the demand for high-performance seats in various vehicle segments, including mid-segment cars, SUVs, and OEM offerings, remains robust. Powered seats and memory functions are luxury features that have gained popularity, while modular seats cater to diverse consumer needs. Side curtain airbags are integrated into the design for added safety.

Get a glance at the Automotive Racing Seat Industry report of share of various segments Request Free Sample

The High-performance segment was valued at USD 553.34 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

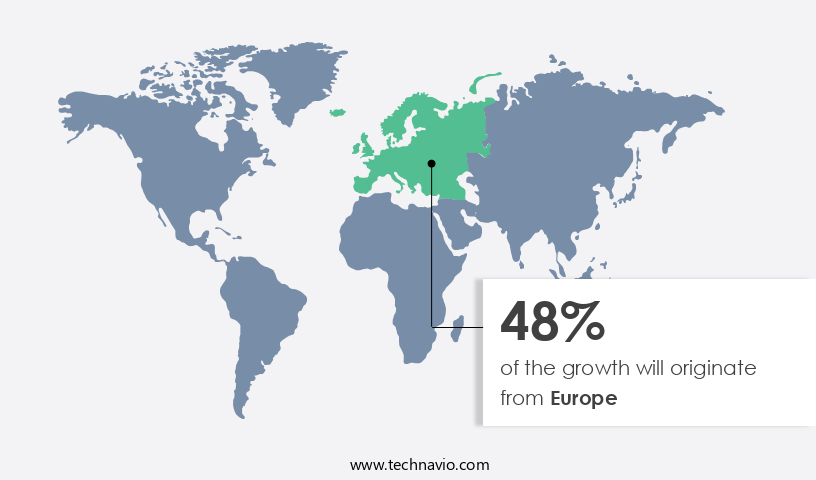

- Europe is estimated to contribute 48% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market is currently In the maturity phase, with Europe being a leading region for technological advancements in motorsports. Major automotive manufacturers, including Mercedes-Benz, BMW, Volkswagen, Volvo, Pagani, Ferrari, Lamborghini, Porsche, McLaren, Jaguar, and Land Rover, are based in Europe, with RECARO Automotive Seating headquartered in Germany. In 2024, the Formula 1 calendar features numerous racing events across Europe, such as the prestigious Monaco Grand Prix in France. Brands like BMW M Performance, Audi Racing, and Ferrari organize circuit racing events throughout the year. Racing seats prioritize comfort, safety, and performance, utilizing lightweight materials like carbon fiber. Consumer preferences lean towards high-performance vehicles, and racing seats cater to this demand.

Lateral support, racing harnesses, weight distribution, and gravity force management are essential features for optimal cornering. Environmental concerns have led to the exploration of natural fiber substitutes for carbon fibers, reducing fuel emissions and minimizing environmental degradation. Industry standards ensure safety and performance, with powered seats, luxury features, and modular designs becoming increasingly popular in mid-segment cars and SUVs. Memory seats and polyester fabrics or synthetic leather upholstery are common options. Side curtain airbags are integrated for added safety.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Automotive Racing Seat Industry?

Lightweighting of seats contributing to desired emission levels and fuel economy is the key driver of the market.

- The market is a significant segment of the motorsports industry, catering to the demand for enhanced comfort, safety, and performance in racing applications. Racing seat technology continues to evolve, focusing on lightweight materials like carbon fiber and other high-performance vehicles to meet consumer preferences. Weight reduction is a critical factor, with automakers integrating systems and utilizing co-molded processes to reduce weight in seat frames. In heavier vehicle segments, such as high-performance and luxury vehicles, lightweight racing seat sets can save approximately 46.3 pounds per set. Advanced racing seats, such as those used in professional racing events, can save up to 57.3

- pounds compared to standard seats. Safety features like racing harnesses, lateral support, and weight distribution are essential considerations in racing seats. Additionally, environmental concerns have led to the exploration of natural fiber substitutes for carbon fibers and other harmful substances. The application of lightweight materials in automotive seating systems is a response to the increasing demand for fuel efficiency and reducing overall vehicle weight, mitigating the effects of rapid urbanization and the associated environmental degradation.

What are the market trends shaping the Automotive Racing Seat Industry?

Emergence of autonomous and EV market is the upcoming market trend.

- The Automotive Racing Seats market is a significant segment of the motorsports industry, catering to the demands of both high-performance vehicles and spectator sports. Racing seat technology prioritizes comfort, safety, and performance, with lightweight materials like carbon fiber being increasingly utilized. Consumer preferences for eco-friendly alternatives have led to the exploration of natural fiber substitutes for carbon fibers. In the realm of high-performance vehicles, racing seats offer lateral support and racing harnesses to distribute weight and withstand gravity forces during cornering. Safety features, such as side curtain airbags, further enhance protection. Comfort is essential, with memory seats and adjustable features becoming luxury options in mid-segment cars and SUVs.

- Weight distribution and fuel emission reduction are essential considerations In the automotive industry, making lightweight materials and modular seats a priority. As urbanization continues to rapidize, the focus on environmental degradation and the use of harmful substances in racing seats is becoming increasingly important. Industry standards dictate the use of non-toxic materials and adherence to safety regulations. Powered seats, once a luxury feature, are now becoming standard in various vehicle segments. Polyester fabrics and synthetic leather are common materials used in racing seats due to their durability and resistance to wear and tear. As the automotive industry evolves, racing seats will continue to adapt to meet the demands of performance, safety, and consumer preferences.

What challenges does the Automotive Racing Seat Industry face during its growth?

Growing tax on luxury vehicles is a key challenge affecting the industry growth.

- The Automotive Racing Seats market is a significant segment of the motorsports industry, catering to the needs of high-performance vehicles in both racing events and cinematic use. Racing seat technology prioritizes comfort, safety, and performance, incorporating lightweight materials like carbon fiber and natural fiber substitutes. Consumer preferences for enhanced lateral support and racing harnesses have driven the demand for advanced seat designs. Weight distribution and gravity force management are crucial factors in cornering and fuel emission reduction for lightweight vehicles. Industry standards mandate safety features such as side curtain airbags and powered seats as luxury features in mid-segment cars and SUVs.

- Modular seats and memory seats have gained popularity among OEMs for their versatility and customization options. While carbon fibers offer strength and durability, there is a growing concern for the environmental impact of harmful substances and toxic materials used in racing seat production. As urbanization accelerates and car racing gains popularity, the market for Automotive Racing Seats is expected to grow steadily, offering opportunities for innovation and differentiation In the competitive landscape.

Exclusive Customer Landscape

The automotive racing seat market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive racing seat market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive racing seat market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Adient Plc - The market encompasses high-performance seating solutions designed for motorsport applications. Notable brands include Recaro Automotive Seating, which delivers ergonomic and lightweight designs for enhanced driver support and safety. These seats cater to various racing disciplines, ensuring optimal comfort and durability for professional and amateur racers alike. Engineered with advanced materials and technologies, automotive racing seats provide superior hold and adjustability, enabling drivers to maintain focus and control during high-speed competition.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adient Plc

- BRAUM Racing

- COBRA SEATS

- Corbeau USA LLC

- Faurecia SE

- Fisher and Co.

- GRAMMER AG

- InterActiveCorp.

- Kirkey Racing Seats

- Lear Corp.

- MasterCraft Safety

- MW Company LLC

- NRG Innovations

- OMP Racing SPA

- Racetech Manufacturing Ltd.

- RECARO Holding GmbH

- Shiloh Industries LLC

- Sparco S.p.A

- Tata Sons Pvt. Ltd.

- Toyota Motor Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market caters to the unique requirements of motorsports, where comfort, safety, and performance are paramount. These seats are engineered to provide optimal lateral support and withstand the rigors of high-speed cornering and gravity forces. The demand for racing seats continues to grow, fueled by consumer preferences for high-performance vehicles and the increasing popularity of motorsports as a spectator sport. Racing seat technology has advanced significantly in recent years, with the use of lightweight materials such as carbon fiber becoming increasingly common. Carbon fiber's strength-to-weight ratio makes it an ideal material for racing seats, enabling manufacturers to create seats that are both lightweight and robust.

Additionally, the adoption of memory seats and powered seats as luxury features in mid-segment cars and SUVs has influenced the racing seat market, driving demand for more advanced and customizable seat designs. The racing seat market is also influenced by industry standards and regulations, which prioritize safety and performance. These standards include requirements for weight distribution, side curtain airbags, and racing harnesses. Racing seats must meet these standards to ensure the safety of drivers and passengers during racing events. As the demand for lightweight vehicles grows due to concerns over fuel emissions and environmental degradation, racing seat manufacturers are exploring the use of natural fiber substitutes for traditional materials.

These substitutes, such as hemp and flax, offer similar strength and durability to carbon fiber but are more sustainable and eco-friendly. The rapid urbanization and increasing popularity of car racing have led to an expansion of the racing seat market. Racing seats are not only used in actual racing events but also in cinematic use and simulators. The modular design of racing seats allows them to be easily integrated into various applications, making them versatile and adaptable to different markets. Despite the benefits of racing seats, there are concerns over the use of harmful substances and toxic materials In their production.

Manufacturers are addressing these concerns by investing in research and development to create racing seats that are free of harmful substances and meet the highest industry standards. In conclusion, the market is driven by the unique requirements of motorsports and the growing demand for high-performance vehicles. The use of advanced materials, such as carbon fiber, and the integration of luxury features, such as memory seats and powered seats, are key trends In the market. Additionally, concerns over sustainability and the use of harmful substances are influencing the market, driving innovation and growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.45% |

|

Market growth 2024-2028 |

USD 909.61 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.15 |

|

Key countries |

US, China, Japan, Germany, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Racing Seat Market Research and Growth Report?

- CAGR of the Automotive Racing Seat industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive racing seat market growth of industry companies

We can help! Our analysts can customize this automotive racing seat market research report to meet your requirements.

RIA -

RIA -