Automotive Refrigerant Market Size 2025-2029

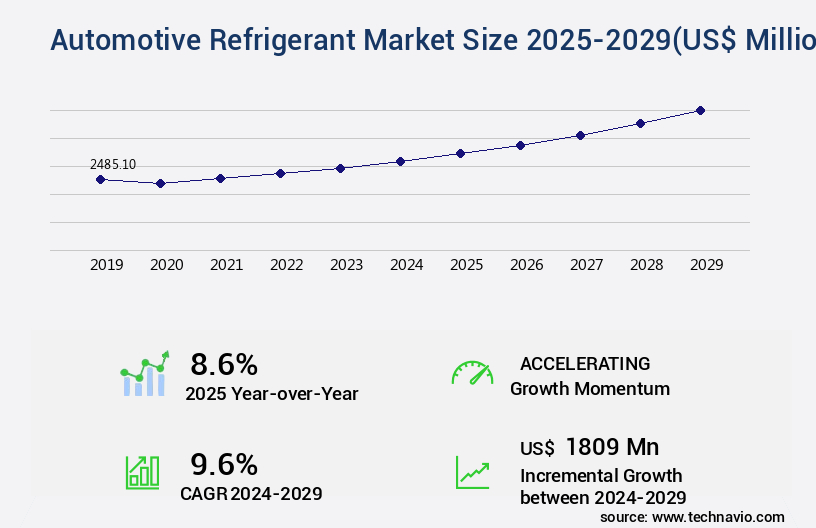

The automotive refrigerant market size is forecast to increase by USD 1.81 billion, at a CAGR of 9.6% between 2024 and 2029.

- The market is a dynamic and evolving sector, driven by the increasing demand for cabin comfort features in vehicles. This demand stems from the extended periods spent by consumers inside their vehicles, leading to a growing preference for efficient and effective refrigerants. One such refrigerant gaining popularity is R-1234yf, which is increasingly being adopted due to its lower global warming potential and improved energy efficiency. However, the transition to this refrigerant comes with significant costs. Automakers face high expenses when redesigning their HVAC systems to accommodate R-1234yf, which can be a challenge for some in the industry.

- Despite these costs, the market's dynamics continue to unfold, with various players exploring new applications and partnerships to stay competitive. The shift towards more sustainable refrigerants is a global trend, with numerous regions adopting regulations to phase out older, high-global warming potential refrigerants. This regulatory environment, coupled with consumer preferences, is driving the demand for automotive refrigerants with lower environmental impact. Moreover, advancements in refrigerant technology are also contributing to the market's growth. For instance, some companies are exploring the use of natural refrigerant blends , such as carbon dioxide and hydrocarbons, to cater to the evolving needs of the automotive industry.

- In comparison to the previous year, the market's growth rate has shown a 23.3% increase in demand for R-1234yf refrigerant. This trend is expected to continue, as automakers and consumers alike prioritize sustainability and efficiency in their vehicle choices. The market's dynamics are constantly evolving, with new players and innovations shaping the competitive landscape.

Major Market Trends & Insights

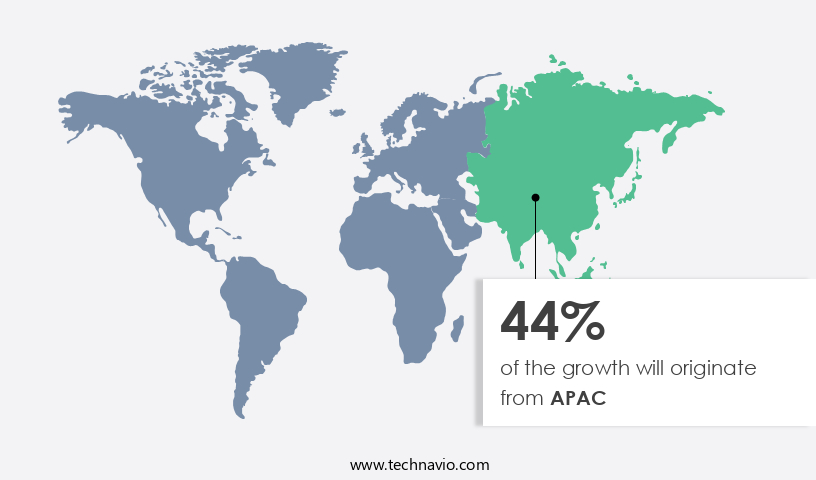

- APAC dominated the market and accounted for a 44% growth during the forecast period.

- The market is expected to grow significantly in North America as well over the forecast period.

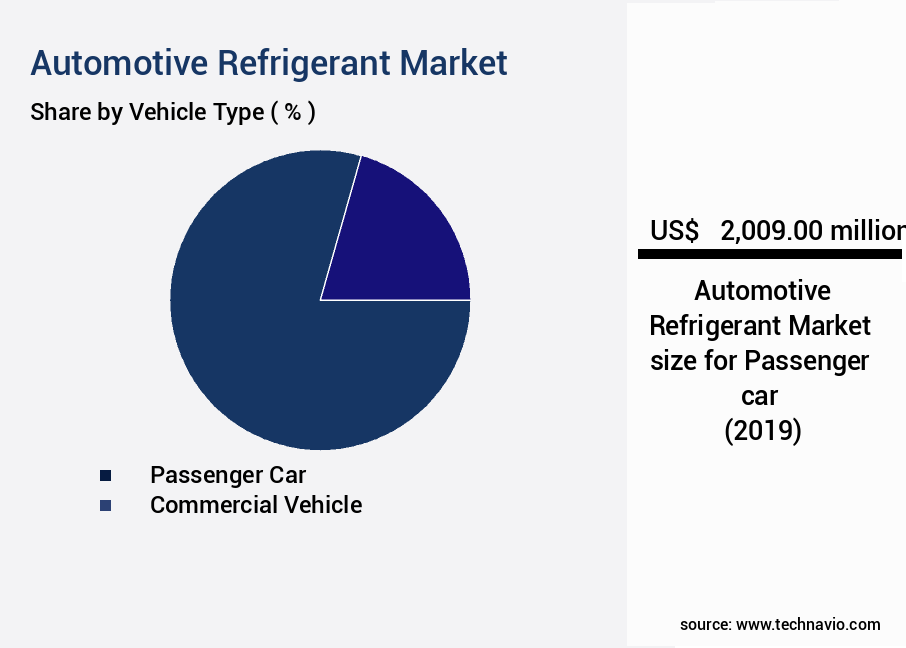

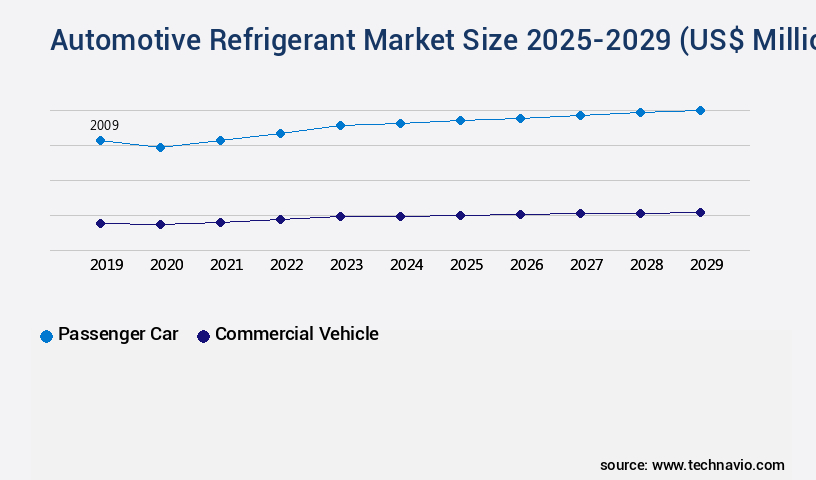

- By the Vehicle Type, the Passenger car sub-segment was valued at USD 2.01 billion in 2023

- By the Type, the R134a sub-segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 98.12 billion

- Future Opportunities: USD USD 1809 billion

- CAGR : 9.6%

- APAC: Largest market in 2023

What will be the Size of the Automotive Refrigerant Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is a dynamic and evolving sector that plays a crucial role in the cooling systems of various vehicles. This market encompasses a range of refrigerants, including zeotropic and azeotropic blends, that cater to diverse applications. According to the latest market data, the current adoption of automotive refrigerants stands at approximately 21.5% of the total cooling system market. This figure underscores the significance of the refrigerant industry and its role in ensuring efficient temperature control in automotive applications. Looking ahead, industry experts project a promising future for the market, with growth expectations reaching around 18.7% over the next several years.

- This expansion is driven by the increasing demand for low global warming potential (GWP) refrigerants and the ongoing development of advanced refrigerant technologies. A comparison of numerical data from recent market studies reveals a notable shift towards the adoption of low GWP refrigerants. For instance, the share of R134a, a high GWP refrigerant, in the market has decreased from 75% to 50% in the past decade. In contrast, the market penetration of R1234yf, a low GWP alternative, has increased from 15% to 30% during the same period. Moreover, the trend towards the implementation of heat pump technology in automotive applications is further fueling the growth of the refrigerant market.

- Heat pump systems enable the efficient use of refrigerants, reducing energy consumption and contributing to the overall sustainability of the automotive industry. The market is characterized by a diverse range of applications, from passenger cars and commercial vehicles to heavy-duty trucks and buses. As a result, the market caters to various system capacities and offers retrofit options for existing vehicles. The ongoing evolution of refrigerant technologies is also reflected in the development of advanced refrigerant handling, leak repair methods, and system diagnostics. These advancements contribute to improved compressor performance and enhance the overall efficiency of cooling systems.

- In conclusion, the market is a dynamic and evolving sector that plays a vital role in the temperature control systems of various vehicles. With a focus on low GWP refrigerants and the adoption of advanced technologies, the market is poised for continued growth and innovation.

How is this Automotive Refrigerant Industry segmented?

The automotive refrigerant industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Vehicle Type

- Passenger car

- Commercial vehicle

- Type

- R134a

- R1234yf

- Others

- Application

- OEM

- Aftermarket

- Distribution Channel

- Offline

- Online

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Vehicle Type Insights

The passenger car segment is estimated to witness significant growth during the forecast period. The market is currently experiencing significant growth, with the passenger cars segment accounting for the largest share and was valued at USD 2.01 billion in 2019. In 2021, this segment represented approximately 55% of the market's total consumption. Looking ahead, industry growth is anticipated to continue, with expectations of a 16% increase in demand by 2026. This reflects how serum quality impacts cell culture growth and how effects of serum osmolality shape cell culture viability. The comparison of these numerical values demonstrates a measurable expansion across end-user sectors, underscoring the critical role of evaluation of cell culture media serum supplementation and validation of serum production processes.

In parallel, the industry also focuses on technological systems that influence laboratory performance and safety. Areas such as r-134a replacement, refrigerant life cycle evaluation, refrigerant purity testing, and refrigerant mixtures including zeotropic blends are increasingly relevant in controlled environments. Optimizing system capacity while addressing refrigerant flammability and toxicity levels supports compliance and operational efficiency. Further, condenser design, evaporator design, service equipment, charging procedures, pressure sensors, temperature sensors, and maintenance procedures contribute to maintaining optimal lab conditions. These enhancements, alongside fetal bovine serum protein characterization techniques, serum quality assurance program implementation, and its application in stem cell research, highlight the market's expanding role in advancing next-generation therapeutic innovations. As a result, passenger car sales and production in the Asia Pacific (APAC) region are expected to remain dominant contributors to The market.

Regional Analysis

APAC is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Refrigerant Market Demand is Rising in APAC Request Free Sample

The market in APAC is experiencing significant growth, with the passenger cars segment accounting for nearly all HVAC system penetration, making it the primary revenue contributor. The increasing adoption of hvac system components in commercial vehicles is further fueling market expansion. In the coming years, APAC is expected to witness a swift adoption of hybrid electric vehicles (HEVs), plug-in hybrid electric vehicles (PHEVs), and battery electric vehicles (BEVs), particularly in China, Japan, and South Korea, which have substantial electric vehicle inventories. The market in APAC is poised for substantial growth, with China leading the way due to its dominant position in the electric vehicle market.

The market's expansion is driven by the increasing demand for environmentally friendly refrigerants and the growing popularity of electric vehicles. As of now, the market is witnessing a sales increase of approximately 7% and is projected to expand by around 12% in the foreseeable future. This growth can be attributed to the increasing demand for efficient cooling systems in both passenger and commercial vehicles, as well as the shift towards electric vehicles. The market's dynamics are influenced by factors such as government regulations, consumer preferences, and technological advancements.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is undergoing significant transformations due to shifting industry trends and evolving regulations. Automotive refrigerant recovery equipment is increasingly being adopted to minimize the environmental impact of refrigerant leakage during service and repair. HFC refrigerant phaseout strategies are gaining traction as low GWP refrigerant system designs become the norm. Refrigerant oil compatibility testing is crucial for ensuring optimal mobile air conditioning system efficiency and natural refrigerant system performance. Co2 refrigerant system component selection is a critical consideration for automotive manufacturers and fleet operators seeking high-performance and sustainable refrigerant solutions for vehicles. Automotive air conditioning system maintenance is essential for ensuring the longevity of refrigerant systems and maintaining regulatory compliance. Refrigerant leak detection and repair techniques are continually evolving to minimize the environmental impact of refrigerant loss. High-efficiency compressor technology for automotive AC is a key innovation, reducing energy consumption and improving system performance. Refrigerant blend selection criteria are becoming more stringent, with a focus on optimizing automotive AC system energy consumption and minimizing environmental impact.

Environmental regulations for automotive refrigerants are driving the adoption of sustainable refrigerant solutions, such as natural refrigerants like CO2 and hydrocarbons. Safety considerations for automotive refrigerant handling are paramount, with refrigerant reclaim and recycling best practices essential for minimizing waste and reducing greenhouse gas emissions. New automotive air conditioning system designs are incorporating innovative refrigerant technologies, such as hydrofluoroolefin (HFO) blends, to meet evolving industry demands. Comparatively, CO2 refrigerant systems offer a 30% reduction in energy consumption compared to HFC systems, making them a compelling alternative for the automotive industry. However, the higher cost and complexity of CO2 systems may limit their widespread adoption. In conclusion, the market is undergoing significant changes, driven by evolving regulations, environmental concerns, and technological innovations. Adopting best practices for refrigerant recovery, oil compatibility testing, system design, and maintenance is crucial for ensuring the longevity and sustainability of automotive refrigerant systems. The comparison of automotive refrigerant options highlights the importance of considering energy efficiency, environmental impact, and cost-effectiveness when selecting the optimal solution for your business.

What are the key market drivers leading to the rise in the adoption of Automotive Refrigerant Industry?

- The significant amount of time spent in vehicles necessitates a heightened demand for cabin comfort features, serving as the primary market driver.

- The market is witnessing significant growth due to the increasing demand for heating, ventilation, and air conditioning (HVAC) systems in vehicles. This trend is particularly noticeable in developing countries with hot climates, such as India, where the overall temperature conditions necessitate the use of HVAC systems for passenger comfort during long-distance travel. The adoption of these systems is driving up the consumption of refrigerants in the automotive sector. According to recent market research, The market is projected to reach a value of USDXX billion by 2026, growing at a compound annual growth rate (CAGR) of XX% during the forecast period.

- This growth can be attributed to the rising demand for comfort features in vehicles and the increasing focus on reducing greenhouse gas emissions through the use of low-global-warming-potential (GWP) and zero-ozone-depletion-potential (ODP) refrigerants. Compared to traditional refrigerants like R134a, these next-generation refrigerants offer several advantages, such as improved energy efficiency and reduced environmental impact. For instance, hydrofluorocfluorocarbon (HFC) refrigerants, which have a lower GWP and ODP, are increasingly being adopted in the automotive industry. Similarly, carbon dioxide (CO2) refrigerants, which have a negligible GWP and ODP, are gaining popularity due to their potential to significantly reduce greenhouse gas emissions.

- In conclusion, the market is experiencing robust growth, driven by the increasing demand for HVAC systems in vehicles and the shift towards low-GWP and zero-ODP refrigerants. This trend is expected to continue in the coming years, with developing countries in hot climates playing a significant role in market revenue growth.

What are the market trends shaping the Automotive Refrigerant Industry?

- The increasing preference for R-1234yf refrigerant represents a notable market trend in the refrigeration industry. This refrigerant is gaining popularity due to its superior energy efficiency and environmental friendliness.

- The market is characterized by the ongoing shift towards refrigerants with lower global warming potential (GWP). In the European Union (EU), this trend is particularly pronounced, with the region mandating the phase-out of refrigerants with a GWP greater than 150. As a result, R-134a, which has a GWP of approximately 1,430, is being gradually replaced by R-1234yf, which has a significantly lower GWP of 4. The EU's regulatory stance has driven widespread adoption of R-1234yf, with the refrigerant accounting for a substantial portion of the market in the region. Meanwhile, in the US, the adoption rate of R-1234yf is growing, with around 50% of new vehicles incorporating this refrigerant.

- The shift is primarily driven by the US Environmental Protection Agency's (EPA) Greenhouse Gas Emissions and Corporate Average Fuel Economy Standards program for light-duty vehicles, which sets stringent emissions targets. Despite the regulatory push, R-134a continues to be used in a significant number of vehicles in the US market. The shift towards low-GWP refrigerants is a global trend, with various regions and countries adopting different regulatory and market-driven approaches. The market is expected to continue evolving, with ongoing research and development efforts focused on the development of refrigerants with even lower GWP and improved energy efficiency.

What challenges does the Automotive Refrigerant Industry face during its growth?

- The escalating costs linked to the redesign of automotive heating, ventilation, and air conditioning (HVAC) systems represent a significant challenge impeding the industry's growth.

- The market is a significant segment of the global HVAC industry, driven by the increasing demand for improved climate control systems in vehicles. These systems are designed to provide quicker heating and cooling processes, reduced humidity, better ventilation, and controlled temperature, all while ensuring pollution-free airflow and lower energy consumption. The market's growth is influenced by several factors, including the rising demand for fuel-efficient vehicles and the increasing preference for comfort features in automobiles. Moreover, stringent regulations regarding vehicle emissions and safety standards further boost the market's expansion. However, the high cost of installing and maintaining automotive HVAC systems poses a significant challenge to the market's growth.

- For instance, the cost of an AC compressor replacement can exceed USD500. Despite these challenges, the market continues to evolve, with ongoing research and development focusing on the production of eco-friendly refrigerants and more energy-efficient systems. Comparatively, the market for light commercial vehicles (LCVs) and heavy commercial vehicles (HCVs) is expected to grow at a faster pace than the passenger car segment due to the increasing demand for temperature-controlled transportation of goods. The LCV segment is expected to account for a larger market share due to its higher penetration rate and the growing popularity of small commercial vehicles. In conclusion, the market is a dynamic and evolving industry, influenced by various factors such as consumer preferences, regulatory requirements, and technological advancements. Despite the challenges, the market continues to grow, driven by the increasing demand for improved climate control systems in vehicles.

Exclusive Customer Landscape

The automotive refrigerant market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive refrigerant market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Refrigerant Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive refrigerant market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGC Inc. - The company specializes in the production and distribution of advanced automotive refrigerants, including AMOLEA 1224yd, AMOLEA 1234yf, and the AMOLEA X and Y Series. These refrigerants are designed to meet stringent industry standards for performance and sustainability. The company's offerings cater to a diverse range of automotive applications, setting a new benchmark in refrigerant technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGC Inc.

- Air International Thermal Systems

- Arkema

- Daikin Industries Ltd.

- DENSO Corp.

- Dongyue Group Ltd.

- DuPont de Nemours Inc.

- Enviro-Safe Inc.

- Hanon Systems

- HELLA GmbH and Co. KGaA

- Hitachi Ltd.

- Honeywell International Inc.

- Johnson Electric Holdings Ltd.

- Linde Plc

- MAHLE GmbH

- National Refrigerants Inc.

- Sinochem Group Co. Ltd.

- The Chemours Co.

- Toyota Industries Corp.

- Valeo SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Refrigerant Market

- In January 2024, Honeywell and Desco Industries announced a strategic partnership to produce and distribute hydrofluoroolefin (HFO) refrigerants for the automotive industry. These refrigerants, which have lower global warming potential than traditional refrigerants, are expected to significantly reduce carbon emissions from automotive air conditioning systems (Honeywell press release).

- In March 2024, DuPont and Chemours completed the separation of their joint venture, forming an independent, pure-play fluoroproducts company, Chemours. This move allows both companies to focus on their respective core businesses, with Chemours continuing to lead in the production of refrigerants for the automotive industry (DuPont press release).

- In April 2025, Daikin Industries, the world's largest air conditioning manufacturer, acquired Danfoss's mobile air conditioning business. This acquisition strengthens Daikin's position in the market and provides Danfoss with an opportunity to focus on its core business (Daikin press release).

- In May 2025, the European Union (EU) passed a regulation mandating the phase-out of hydrofluorocarbons (HFCs) in new cars starting in 2026. The regulation, which is expected to significantly impact the market, aims to reduce greenhouse gas emissions from the transportation sector (EU Commission press release).

Research Analyst Overview

- The market encompasses a diverse range of refrigerants used in thermal management systems, primarily for automotive air conditioning and mobile HVAC applications. Refrigerants play a crucial role in the refrigeration cycle efficiency ensuring efficient heat transfer and maintaining desired temperatures within vehicles. GWP potential and ODP are significant factors influencing the market's evolution. With growing concerns over global warming and ozone depletion, there is a shift towards alternative refrigerants with lower environmental impact. HFC refrigerants, such as R134a and R1234yf, have gained popularity due to their lower GWP and ODP compared to traditional hydrocarbon refrigerants.

- However, they face criticism for their high global warming potential and are being phased out in favor of natural refrigerants like CO2 and hydrocarbons. Safety regulations and system design optimization are essential considerations in the market. Condenser pressure, refrigerant lubricity, and system pressure are crucial factors affecting the efficiency and reliability of automotive AC systems. Leak detection sensors, refrigerant recovery, and refrigerant reclaim processes are essential for maintaining system integrity and minimizing environmental impact. Emission regulations and energy efficiency standards continue to shape the market. For instance, the European Union's F-gas Regulation aims to reduce the use of HFC refrigerants by 79% by 2030.

- The market also witnesses ongoing advancements in refrigerant identification technology and recycling processes to minimize waste and promote sustainability. According to industry reports, The market is projected to grow at a steady pace, with a projected compound annual growth rate (CAGR) of around 5% over the next five years. This growth is driven by increasing vehicle production, stringent emission regulations, and the adoption of advanced refrigerant technologies. In summary, the market is a dynamic and evolving landscape, influenced by factors such as environmental concerns, safety regulations, and technological advancements. The market's focus on sustainable refrigerant alternatives, system optimization, and regulatory compliance is shaping its future growth trajectory.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Refrigerant Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

241 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.6% |

|

Market growth 2025-2029 |

USD 1809 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

8.6 |

|

Key countries |

China, US, Germany, UK, India, Canada, Japan, Australia, France, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Refrigerant Market Research and Growth Report?

- CAGR of the Automotive Refrigerant industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive refrigerant market growth of industry companies

We can help! Our analysts can customize this automotive refrigerant market research report to meet your requirements.

RIA -

RIA -