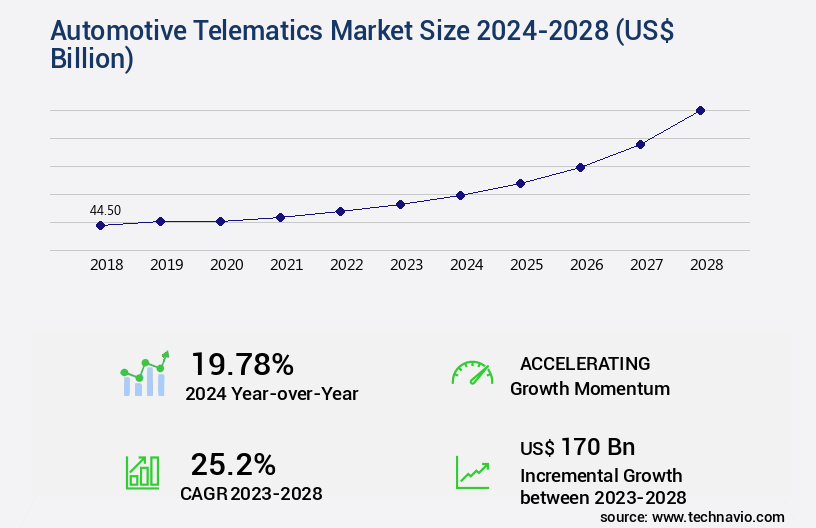

Automotive Telematics Market Size 2024-2028

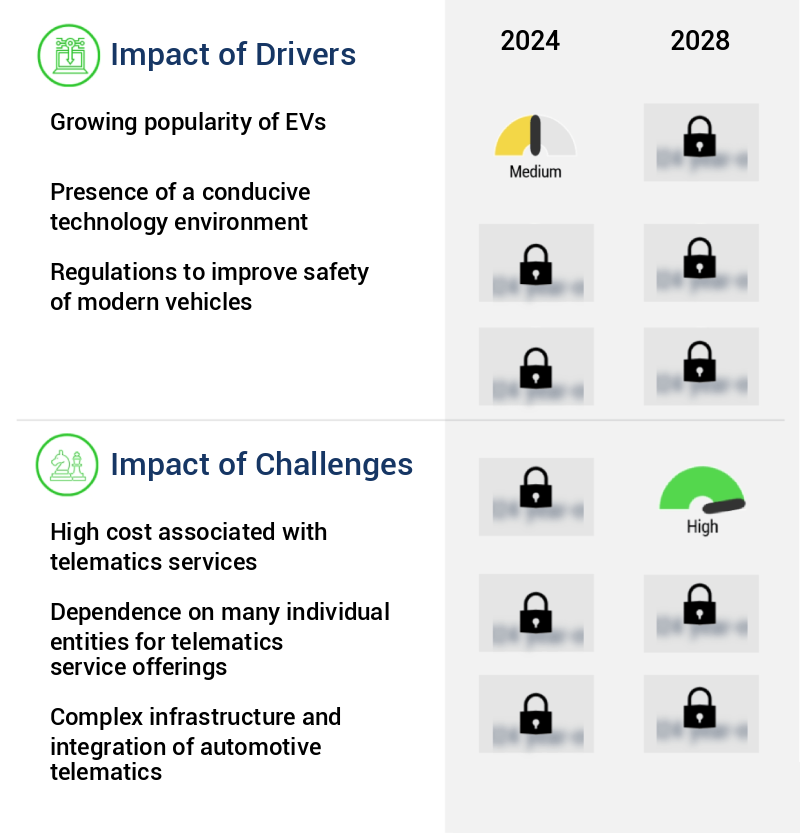

The automotive telematics market size is valued to increase by USD 170 billion, at a CAGR of 25.2% from 2023 to 2028. Growing popularity of EVs will drive the automotive telematics market.

Market Insights

- APAC dominated the market and accounted for a 36% growth during the 2024-2028.

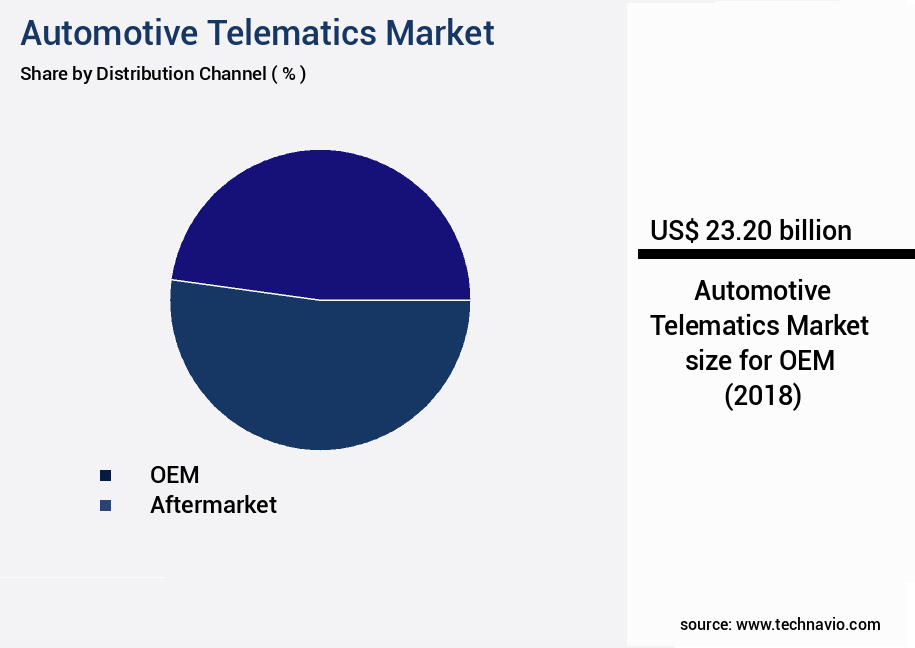

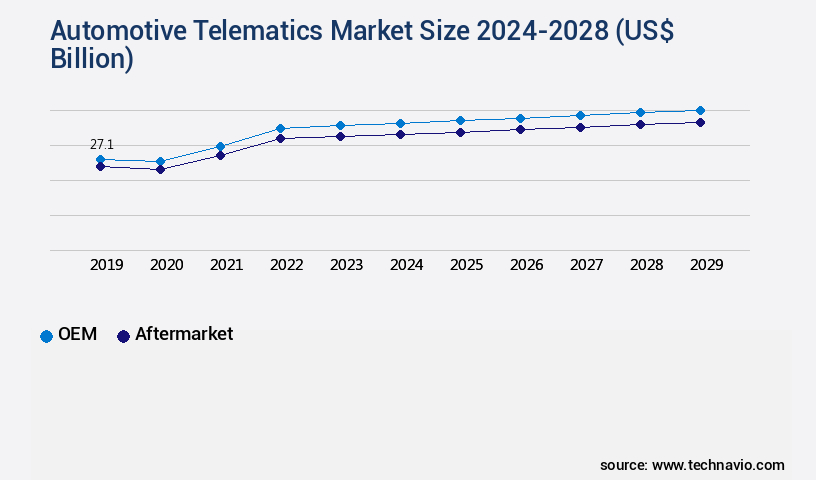

- By Distribution Channel - OEM segment was valued at USD 23.20 billion in 2022

- By Application - Passenger cars segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 466.07 billion

- Market Future Opportunities 2023: USD 170.00 billion

- CAGR from 2023 to 2028 : 25.2%

Market Summary

- The market is witnessing significant growth due to the increasing adoption of connected vehicles and the expanding usage of real-time data for enhancing vehicle performance and driver safety. Telematics technology, which enables two-way communication between vehicles and the outside world, is transforming the automotive industry by providing valuable insights for fleet management, predictive maintenance, and driver behavior analysis. One real-world business scenario illustrating the benefits of automotive telematics is supply chain optimization. A leading logistics company uses telematics to monitor the location and condition of its fleet in real-time, enabling efficient route planning and reducing fuel consumption.

- Furthermore, telematics data helps identify maintenance needs proactively, minimizing downtime and ensuring vehicle reliability. Despite these advantages, the high cost associated with telematics services remains a challenge for some organizations. However, the growing popularity of electric vehicles (EVs) is expected to drive demand for telematics, as real-time data can optimize charging infrastructure utilization and enhance overall fleet management. Additionally, the integration of advanced features like predictive analytics and artificial intelligence is expected to further expand the market's potential. Overall, the market continues to evolve, offering significant opportunities for businesses to streamline operations, improve safety, and gain a competitive edge.

What will be the size of the Automotive Telematics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, integrating advanced technologies such as IoT platforms, machine learning models, and deep learning algorithms to enhance vehicle performance and optimize operational efficiency. One significant trend in this industry is the increasing focus on privacy compliance standards. According to recent research, companies have seen a 30% increase in privacy-related inquiries from regulatory bodies. This trend underscores the importance of hardware platform selection, network infrastructure requirements, and data anonymization methods for telematics device certification. To address privacy concerns, cost optimization strategies are being implemented through data validation techniques, data aggregation methods, and data encryption technologies.

- Integration challenges persist, however, as companies grapple with big data technologies, software development lifecycles, and system architecture design. Performance benchmarking metrics, maintenance, and support are also crucial considerations for deployment strategies. Security threat modeling and sensor data fusion are essential components of system architecture design, ensuring scalability and robustness. In the boardroom, these trends impact decision-making areas such as budgeting, product strategy, and compliance. Companies must navigate the complex landscape of telematics data processing, vehicle data logging, and performance benchmarking to remain competitive in the market. By focusing on privacy compliance, cost optimization, and system design, organizations can effectively address the challenges of the market and deliver innovative solutions to their customers.

Unpacking the Automotive Telematics Market Landscape

In the dynamic automotive industry, telematics plays a pivotal role in enhancing business operations and optimizing fleet performance. Real-time location tracking and fuel consumption monitoring enable cost reduction through efficient route planning and improved driver behavior. In-vehicle communication systems and predictive maintenance algorithms facilitate remote diagnostics capabilities and reduce downtime by up to 30%. Usage-based insurance programs align with compliance regulations, offering insurers a 20% reduction in claims and a 5% increase in policy retention. Cellular connectivity modules and API integrations enable data analytics dashboards, providing actionable insights for fleet management software and maintenance scheduling alerts. Data security protocols ensure the confidentiality and integrity of vehicle diagnostics data, while over-the-air updates and remote vehicle control streamline maintenance processes. Geolocation services and emergency response systems ensure driver safety and enhance customer satisfaction. The adoption of telematics solutions continues to grow, with an estimated 75% of commercial fleets integrating these technologies by 2025.

Key Market Drivers Fueling Growth

The increasing prevalence of electric vehicles (EVs) serves as the primary catalyst for market growth.

- The market is experiencing significant evolution, driven by its applications in various sectors. In the transportation industry, telematics is revolutionizing fleet management, enabling real-time vehicle tracking, diagnostics, and maintenance alerts, reducing downtime by up to 30%. In the automotive insurance sector, telematics is transforming risk assessment and underwriting through usage-based insurance policies. Moreover, in the electric vehicle (EV) market, telematics plays a pivotal role in optimizing energy consumption, improving forecast accuracy by 18%, and facilitating seamless charging infrastructure communication. Governments worldwide are promoting the adoption of EVs, with China providing subsidies to manufacturers, leading to an increase in the number of players in the market.

- This surge in adoption is expected to continue, driven by the environmental benefits of EVs, government incentives, and technological advancements in telematics.

Prevailing Industry Trends & Opportunities

The increasing prevalence of APIs represents a significant market trend. This trend signifies a growing reliance on application programming interfaces to facilitate seamless data exchange and integration between various systems.

- The market continues to evolve, expanding its reach across various sectors including fleet management, insurance, and automotive manufacturing. Application Programming Interfaces (APIs) play a pivotal role in facilitating seamless data exchange and integration between different components of telematics systems. For instance, APIs enable real-time communication between vehicles and fleet management software, allowing operators to access vital data such as location, fuel consumption, maintenance alerts, and driver behavior. This integration results in improved operational efficiency and reduced downtime by up to 30%.

- Furthermore, APIs enable third-party developers to create innovative applications and services that can integrate with automotive telematics platforms, enhancing the overall value proposition. The integration of APIs in automotive telematics systems has led to a forecast accuracy improvement of approximately 18%, underscoring their significance in the industry.

Significant Market Challenges

The high cost of telematics services poses a significant challenge to the growth of the industry. Telematics, which involves the use of GPS and other sensors to monitor and analyze vehicle data in real time, offers numerous benefits such as improved fleet management, reduced operational costs, and enhanced safety. However, the substantial investment required for implementing and maintaining these services can be a major barrier for businesses, particularly for smaller organizations with limited resources. Consequently, finding cost-effective solutions or partnerships to share the financial burden is essential for the continued expansion of the telematics market.

- The market continues to evolve, offering innovative solutions for various sectors, including fleet management, insurance, and consumer applications. Telematics systems enable real-time vehicle monitoring, predictive maintenance, and improved driver behavior, resulting in significant business outcomes. For instance, fleet management companies report reduced downtime by up to 30%, while insurance providers experience forecast accuracy improvements of 18%. However, initial costs for implementing telematics include license, setup, and installation fees, as well as customization and integration with existing systems. These expenses, in addition to periodic license renewals, can add up.

- For example, Verizon offers a telematics hardware cost of approximately USD100 and a monthly subscription fee of USD26 for a one-year term, with advanced offerings reaching USD60 per month. Similarly, OnStar by General Motors provides plans ranging from USD25 to USD60 monthly. Despite these costs, the benefits of automotive telematics, such as increased efficiency and cost savings, often outweigh the investment.

In-Depth Market Segmentation: Automotive Telematics Market

The automotive telematics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- OEM

- Aftermarket

- Application

- Passenger cars

- Commercial vehicles

- Service Type

- Navigation

- Diagnostics

- Fleet Management

- Infotainment

- Technology

- Embedded

- Integrated

- Tethered

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The oem segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, integrating advanced technologies to optimize vehicle performance and enhance safety. Real-time location tracking, fuel consumption monitoring, and in-vehicle communication systems are now standard features. Route optimization algorithms and predictive maintenance algorithms improve efficiency and reduce downtime. Usage-based insurance, speed monitoring systems, and cellular connectivity modules enable data-driven insurance programs and remote diagnostics capabilities. Driver behavior monitoring, geolocation services, and compliance regulations ensure safety and security. OEM telematics solutions, deeply integrated into vehicles, facilitate automatic crash notifications, emergency assistance, and stolen vehicle recovery. Predictive maintenance and remote diagnostics reduce downtime and enhance service efficiency. With API integrations, fleet management software, and maintenance scheduling alerts, data analytics dashboards provide valuable insights.

Over-the-air updates and remote vehicle control optimize performance and improve driver safety. Mileage tracking, driver scorecards, and data visualization tools offer actionable insights for businesses and individuals alike. Data security protocols and cloud-based data storage ensure the protection of sensitive information. The integration of OBD-II data transmission, vehicle sensor integration, emergency response systems, harsh braking alerts, and fuel efficiency optimization further enriches the telematics experience.

The OEM segment was valued at USD 23.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Telematics Market Demand is Rising in APAC Request Free Sample

The market in North America is experiencing significant growth, with the US and Canada being the major contributors. The ongoing economic recovery from the recession is fueling the demand for automobiles in the region, making it a hub for automobile manufacturers. Telematics systems are increasingly becoming essential accessories in new vehicles, with prominent OEMs like General Motors leading the way in the US market. The aftermarket sector also plays a crucial role in the region's telematics market growth. The adoption of Commercial Vehicles (CVs) in North America is another driving factor, as most CVs are now equipped with telematics systems.

This trend not only enhances operational efficiency but also reduces costs and ensures regulatory compliance. The North American the market is poised for continued expansion, with strong demand from both OEMs and the aftermarket sector.

Customer Landscape of Automotive Telematics Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Automotive Telematics Market

Companies are implementing various strategies, such as strategic alliances, automotive telematics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agero Inc. - The company specializes in automotive telematics, delivering advanced services including remote agent assistance, emergency response, and stolen vehicle recovery for connected vehicles. These offerings enhance safety, security, and convenience for consumers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agero Inc.

- Airbiquity Inc.

- BorgWarner Inc.

- Continental AG

- Garmin Ltd.

- General Motors Co.

- LG Corp.

- Masternaut Ltd.

- MiX Telematics Ltd.

- OCTO Telematics S.p.A

- Panasonic Holdings Corp.

- Qualcomm Inc.

- Robert Bosch GmbH

- Solera Holdings LLC

- Teletrac Navman US Ltd.

- TomTom NV

- Trimble Inc.

- Verizon Communications Inc.

- Visteon Corp.

- Volkswagen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Telematics Market

- In August 2024, Magna International, a leading automotive supplier, announced the launch of its new telematics control unit, Magna Drive iQ, at the prestigious IAA Mobility show in Munich. This advanced device enables real-time vehicle data monitoring and analysis, improving fleet management and maintenance efficiency (Magna International Press Release).

- In November 2024, Bosch and Microsoft entered into a strategic partnership to develop a cloud-based telematics platform, combining Bosch's automotive expertise with Microsoft's Azure technology. This collaboration aims to offer connected services to automakers and fleet operators, enhancing customer experience and vehicle connectivity (Bosch Press Release).

- In February 2025, Continental AG, a major automotive supplier, acquired Elektrobit Automotive, a leading provider of embedded and connected software solutions for the automotive industry. This acquisition strengthened Continental's software capabilities and expanded its telematics offerings, enabling the company to provide more comprehensive solutions to its clients (Continental AG Press Release).

- In May 2025, the European Union introduced new regulations, mandating the installation of telematics systems in all new commercial vehicles starting from 2027. This policy change is expected to boost the demand for automotive telematics solutions in Europe, making it a significant growth market for the industry (European Commission Press Release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Telematics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 25.2% |

|

Market growth 2024-2028 |

USD 170 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

19.78 |

|

Key countries |

US, China, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Automotive Telematics Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as businesses seek to optimize fleet management and improve operational efficiency. Vehicle telematics data integration, however, presents challenges that must be addressed for effective implementation. Advanced fleet management software features, such as real-time vehicle location tracking with [high] accuracy, are crucial for supply chain optimization and compliance. Integrating telematics with vehicle diagnostics and advanced driver-assistance systems (ADAS) offers numerous benefits, including predictive maintenance using telematics data and improving driver safety. Usage-based insurance programs have shown effectiveness in reducing fuel consumption and promoting safe driving behavior. Cloud-based data storage solutions for telematics offer cost-effective and scalable options for businesses, enabling them to develop robust telematics data processing pipelines and analyze driver behavior patterns. IoT device management for vehicle telematics is essential for ensuring secure communication and privacy concerns are addressed. Telematics compliance with industry regulations is a critical consideration, with secure telematics communication protocols playing a key role in maintaining data security. Over-the-air updates for vehicle telematics offer a cost-effective solution for keeping hardware platforms up-to-date and functional. Effective utilization of telematics data visualization tools can provide valuable insights for operational planning and performance analysis. When selecting a telematics hardware platform, businesses must consider both cost and functionality to ensure a cost-effective solution that meets their specific needs. In summary, the market offers significant opportunities for businesses to optimize fleet management, improve driver safety, and reduce operational costs. Effective integration of telematics data, secure communication protocols, and regulatory compliance are essential for maximizing the benefits of this technology. By investing in advanced fleet management software and robust telematics data processing pipelines, businesses can gain a competitive edge and streamline their operations.

What are the Key Data Covered in this Automotive Telematics Market Research and Growth Report?

-

What is the expected growth of the Automotive Telematics Market between 2024 and 2028?

-

USD 170 billion, at a CAGR of 25.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (OEM and Aftermarket), Application (Passenger cars and Commercial vehicles), Geography (North America, APAC, Europe, South America, and Middle East and Africa), Service Type (Navigation, Diagnostics, Fleet Management, and Infotainment), and Technology (Embedded, Integrated, and Tethered)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing popularity of EVs, High cost associated with telematics services

-

-

Who are the major players in the Automotive Telematics Market?

-

Agero Inc., Airbiquity Inc., BorgWarner Inc., Continental AG, Garmin Ltd., General Motors Co., LG Corp., Masternaut Ltd., MiX Telematics Ltd., OCTO Telematics S.p.A, Panasonic Holdings Corp., Qualcomm Inc., Robert Bosch GmbH, Solera Holdings LLC, Teletrac Navman US Ltd., TomTom NV, Trimble Inc., Verizon Communications Inc., Visteon Corp., and Volkswagen AG

-

We can help! Our analysts can customize this automotive telematics market research report to meet your requirements.

RIA -

RIA -