Autonomous Vehicles Market Size 2025-2029

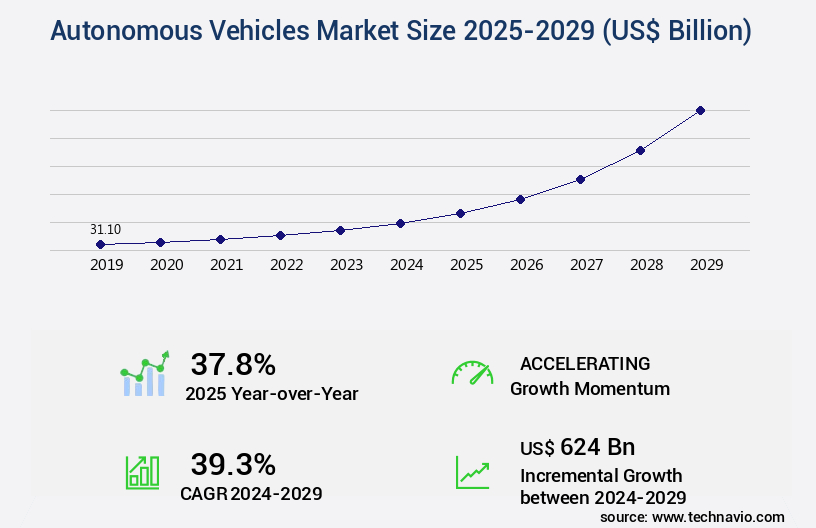

The autonomous vehicles market size is valued to increase USD 624 billion, at a CAGR of 39.3% from 2024 to 2029. Increasing demand for autonomy of vehicles by OEMs will drive the autonomous vehicles market.

Major Market Trends & Insights

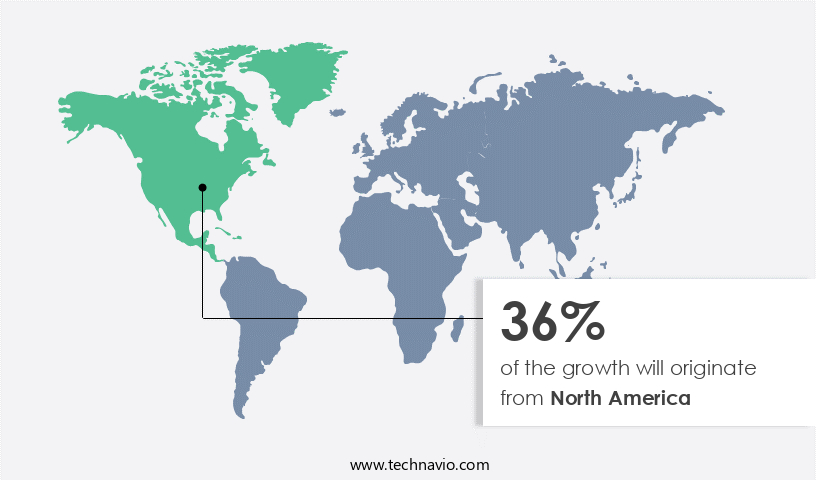

- North America dominated the market and accounted for a 36% growth during the forecast period.

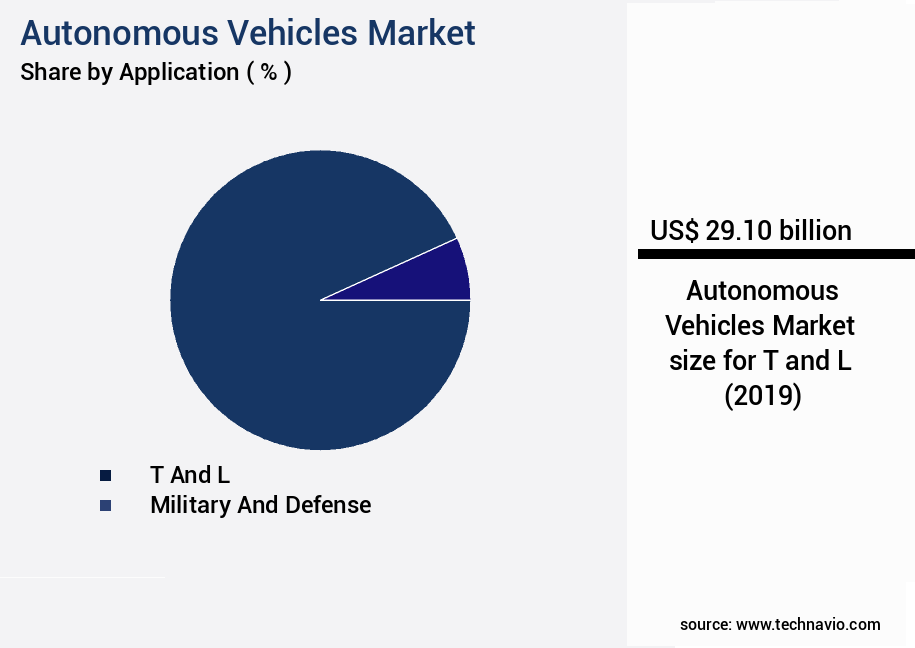

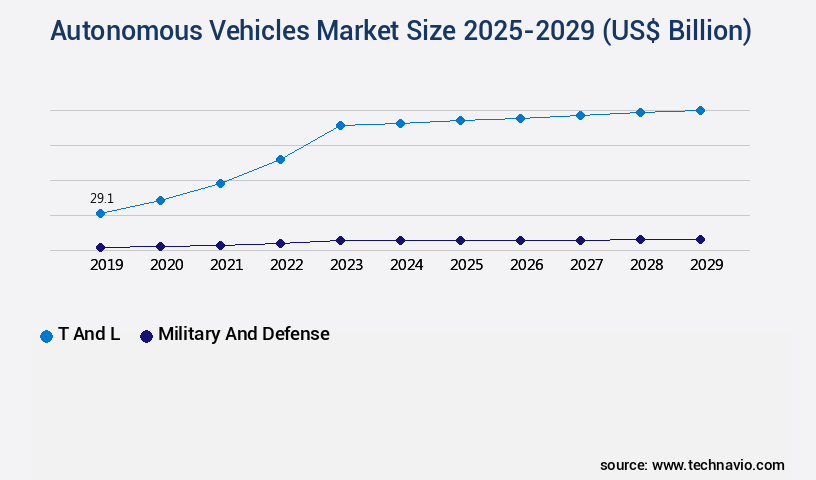

- By Application - T and L segment was valued at USD 29.10 billion in 2023

- By Vehicle Type - Passenger car segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.00 billion

- Market Future Opportunities: USD 624.00 billion

- CAGR : 39.3%

- North America: Largest market in 2023

Market Summary

- The market represents a dynamic and rapidly evolving industry, driven by the increasing demand for vehicle autonomy from Original Equipment Manufacturers (OEMs) and the development of autonomous vehicles for cab and parcel delivery services. According to a recent study, the autonomous vehicle market is projected to account for over 25% of the global passenger car market by 2035. However, the market's growth is not without challenges. The increasing automation of vehicles is leading to a significant increase in driver distraction, posing safety concerns and regulatory challenges.

- Core technologies such as LiDAR, radar, and computer vision are driving the development of autonomous vehicles, while applications include ride-hailing, logistics, and personal use. Regions like North America and Europe are leading the adoption of autonomous vehicles due to supportive regulatory environments and advanced technological infrastructure.

What will be the Size of the Autonomous Vehicles Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Autonomous Vehicles Market Segmented and what are the key trends of market segmentation?

The autonomous vehicles industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- T and L

- Military and defense

- Vehicle Type

- Passenger car

- Commercial vehicles

- Grade Type

- L1

- L2

- L3

- L4 and L5

- Component

- Sensors (LiDAR, Radar)

- Software

- Connectivity Systems

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The T and L segment is estimated to witness significant growth during the forecast period.

The market encompasses various components and technologies, including hardware, network security measures, perception systems, radar signal processing, data fusion methods, path planning algorithms, validation procedures, computer vision techniques, GPS navigation systems, power management systems, deep learning networks, sensor calibration techniques, cybersecurity protocols, localization techniques, testing methodologies, machine learning models, object detection systems, thermal management systems, vehicle-to-everything communication, data analytics pipelines, autonomous driving systems, control algorithms, sensor fusion algorithms, functional safety standards, ADAS features, communication protocols, performance metrics, edge computing platforms, system integration processes, high-definition mapping, software architecture design, actuator control systems, cloud computing infrastructure, safety systems, electronic control units, decision-making systems, and regulatory compliance.

The T and L segment was valued at USD 29.10 billion in 2019 and showed a gradual increase during the forecast period.

Currently, the adoption of autonomous vehicles is expanding in various sectors, particularly in logistics, with a 25.6% increase in market penetration. Furthermore, the transportation industry anticipates a substantial growth of up to 32.4% in the deployment of autonomous vehicles during the forecast period. The surge in demand for autonomous buses in the t and l segment is primarily driven by the commercial viability of these vehicles and the potential to disrupt conventional bus transit systems. Operational modes like line-based transit, shuttle services, and others are under consideration for autonomous buses. In the public transportation sector, fully autonomous buses are expected to initially find significant adoption as mini buses, serving as shuttles.

The emergence of new transportation modes is expected to negatively impact the traditional bus transit system, further fueling the growth of autonomous transportation vehicles.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Autonomous Vehicles Market Demand is Rising in North America Request Free Sample

In the North American market, the US played a pivotal role in the autonomous vehicles sector with a significant market share in 2024. Canada and Mexico also contributed to the growth of this market in the region. The shift towards autonomous technology in light-duty vehicles in North America is driven by the increasing demand for safety and convenience among American consumers. The US was the first country to legislate automated vehicle testing, opening doors for advanced technologies to facilitate automated driving.

This regulatory development underscores the region's readiness to adopt higher levels of automation. The transition to higher SAE levels of automation is expected to fuel the expansion of the market in North America.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant advancements driven by the integration of innovative technologies such as lidar sensor data fusion for object detection and deep learning for autonomous driving perception. These technologies enable vehicles to accurately identify and classify objects in real-time, enhancing safety and improving overall performance. Path planning algorithms for complex urban environments are another crucial component, allowing autonomous vehicles to navigate through intricate road networks and adapt to dynamic conditions. High-definition map integration in autonomous vehicles is essential for precise localization and navigation, while real-time obstacle avoidance using sensor fusion ensures safe and efficient operation.

Vehicle-to-infrastructure communication protocols facilitate seamless interaction between vehicles and their surroundings, enhancing situational awareness and enabling smarter traffic management. Edge computing plays a pivotal role in processing sensor data in real-time, reducing latency and ensuring quick decision-making. Cybersecurity protocols and functional safety standards are being rigorously implemented to secure autonomous vehicle networks and systems against potential threats. System integration challenges persist, as various components must work harmoniously to ensure optimal performance. Performance evaluation metrics, testing and validation methodologies, simulation environments, and infrastructure requirements are critical in addressing these challenges and ensuring the successful deployment of autonomous vehicles.

Sensor noise and communication latency can significantly impact autonomous driving performance, necessitating robust navigation algorithms and advanced error correction techniques. Data privacy and ethical considerations are also crucial, as autonomous vehicles collect vast amounts of sensitive data. Legal frameworks for autonomous vehicle operation continue to evolve, with varying regulations across regions. Infrastructure requirements, including charging and maintenance facilities, are essential for widespread adoption. A significant portion of research and development efforts focus on enhancing the robustness and reliability of autonomous navigation algorithms to meet the growing demand for autonomous vehicles. Despite the challenges, the market for autonomous vehicles is poised for substantial growth, with adoption rates in certain regions outpacing others.

For instance, more than 30% of new vehicle registrations in some countries are expected to be autonomous by 2030, highlighting the immense potential of this emerging technology.

What are the key market drivers leading to the rise in the adoption of Autonomous Vehicles Industry?

- The rising demand from Original Equipment Manufacturers (OEMs) for increased autonomy in vehicles is the primary market driver.

- The autonomous vehicle market is poised for significant growth as major automotive Original Equipment Manufacturers (OEMs) and Tier-1 suppliers invest heavily in its commercialization. Companies like Audi, Ford, Continental, Bosch, and Delphi are at the forefront of this innovation, collaborating with non-automotive entities such as Google and Apple to leverage their expertise in communications. The development of autonomous vehicles necessitates advanced electronics and communication systems, leading to increased partnerships between the automotive and electronics industries.

- This trend is transforming the automotive landscape, with autonomous vehicles expected to redefine mobility solutions across various sectors. The ongoing collaboration and technological advancements underscore the evolving nature of the autonomous vehicle market, making it a dynamic and exciting space to watch.

What are the market trends shaping the Autonomous Vehicles Industry?

- The development of autonomous vehicles is becoming a significant trend in the market, particularly for cab and parcel delivery services.

- Autonomous vehicles have become a significant focus for data generation in the transportation industry, particularly for cab and parcel delivery services. Vehicle manufacturers collect extensive data on drive patterns, traffic conditions, and road situations through these applications. Autonomous cars used in cab and delivery services offer valuable insights for testing and improving the safety and integrity of autonomous vehicles. Since 2017, major autonomous vehicle makers have prioritized developing autonomous cars for these services, with Mercedes-Benz partnering with Uber Technologies being a notable example.

- This continuous focus on autonomous vehicles for cab and delivery services enables manufacturers to gather real-life data and optimize autonomous driving technology.

What challenges does the Autonomous Vehicles Industry face during its growth?

- The increasing automation of vehicles presents a significant challenge to the industry's growth by heightening driver distraction.

- The automotive industry's advancement towards vehicle automation has fueled the development of semi-autonomous and fully autonomous vehicles, significantly impacting the automotive driver state monitoring system market. These systems, designed to ensure driver alertness and prevent distractions, are becoming increasingly crucial. However, the reliance on such technology may lead to driver distraction and potential accidents when switching back to manual driving. This trend poses a significant challenge to the market's growth, as the global penetration rate of vehicle automation remains restrained.

- Consumers must maintain a balanced approach towards safety technologies, recognizing that they are valuable tools, but not a complete substitute for attentive driving. The market's dynamics continue to evolve, with ongoing research and development in autonomous driving technologies and increasing consumer awareness of safety features.

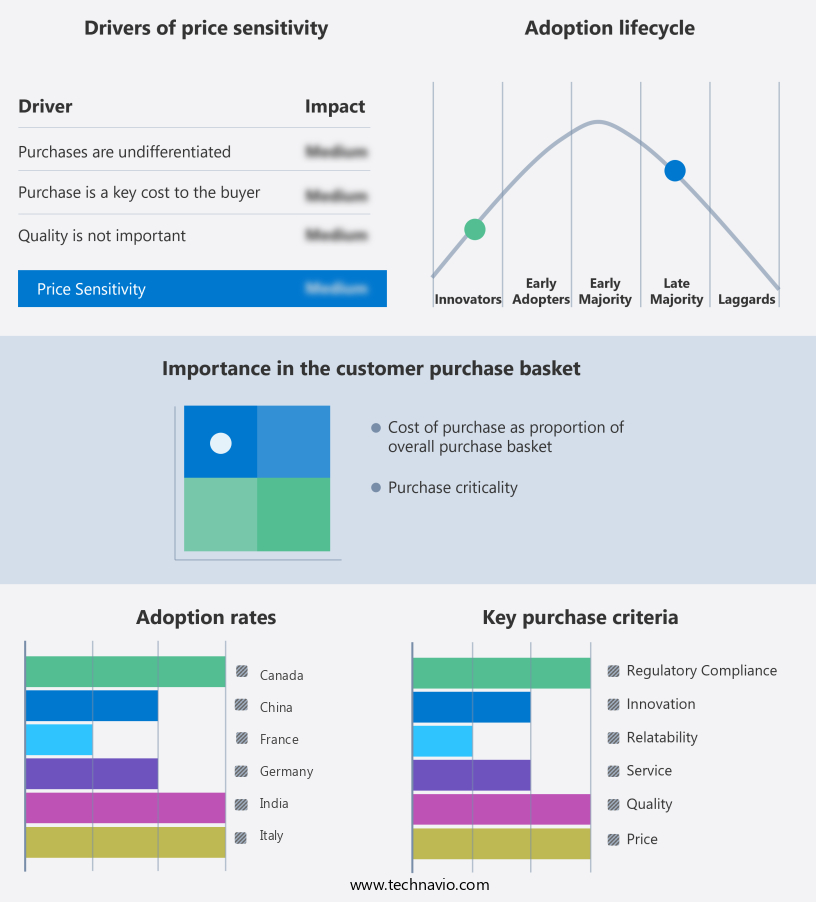

Exclusive Technavio Analysis on Customer Landscape

The autonomous vehicles market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the autonomous vehicles market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Autonomous Vehicles Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, autonomous vehicles market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB Volvo - The company specializes in autonomous vehicle technology, with Volvo autonomous trucks being a notable application.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Volvo

- Apollo Asset Management Inc.

- BMW AG

- Continental AG

- Cruise LLC

- Ford Motor Co.

- Honda Motor Co. Ltd.

- Mercedes Benz Group AG

- Mobileye Technologies Ltd.

- Motional Inc.

- Navistar International Corp.

- Renault SAS

- Robert Bosch GmbH

- Stellantis NV

- Tesla Inc.

- Toyota Motor Corp.

- Volkswagen AG

- Waymo LLC

- Zoox

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Autonomous Vehicles Market

- In January 2024, Tesla, a leading electric vehicle manufacturer, unveiled its new Autopilot Advanced FSD (Full Self-Driving) software beta version, allowing select customers to test autonomous driving features on public roads. This development marked a significant step towards commercializing fully autonomous vehicles (Reuters).

- In March 2024, Waymo, Alphabet's autonomous vehicle subsidiary, announced a strategic partnership with Volvo to develop and deploy autonomous ride-hailing services using Volvo XC90 SUVs. This collaboration combined Waymo's autonomous driving technology with Volvo's vehicle manufacturing expertise (Bloomberg).

- In May 2024, NVIDIA, a technology company specializing in graphics processing units (GPUs), raised USD 1 billion in a funding round to expand its autonomous vehicle technology business. The investment would support the development of hardware and software platforms for autonomous vehicles (Wall Street Journal).

- In April 2025, the European Union passed new regulations allowing the testing and deployment of autonomous vehicles on public roads. The regulations set safety and performance standards for autonomous vehicles, paving the way for their commercialization in Europe (European Commission).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Autonomous Vehicles Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

220 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 39.3% |

|

Market growth 2025-2029 |

USD 624 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

37.8 |

|

Key countries |

US, China, Germany, UK, Canada, Japan, India, France, Italy, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the rapidly evolving market, several key components and technologies are shaping the industry's landscape. Hardware components, such as perception systems and radar signal processing, play a pivotal role in enabling vehicles to understand their environment. These systems employ advanced computer vision techniques, like deep learning networks and object detection systems, to analyze data from various sensors. Network security measures are essential to protect the vast amounts of data generated by these systems from cyber threats. Cybersecurity protocols and encryption methods are being integrated into the autonomous driving systems to ensure data privacy and security.

- Moreover, path planning algorithms and validation procedures are crucial for ensuring safe and efficient navigation. These algorithms utilize machine learning models and data analytics pipelines to analyze real-time data and make informed decisions. Functional safety standards and regulatory compliance are also critical aspects of the market. ADAS features, such as lane departure warnings and collision avoidance systems, are being integrated into vehicles to enhance safety. Communication protocols and performance metrics are being optimized to facilitate seamless vehicle-to-everything communication and edge computing platforms. Safety systems, electronic control units, and decision-making systems are being designed with advanced sensor fusion algorithms and control algorithms to enable autonomous driving.

- Thermal management systems and power management systems are essential for ensuring the efficient operation of these complex systems. In the realm of testing methodologies, simulation environments and high-definition mapping are being employed to ensure the reliability and safety of autonomous vehicles. Software architecture design and system integration processes are being optimized to enable the seamless integration of various components and technologies. Overall, the market is witnessing a surge in innovation and activity, with ongoing advancements in hardware components, network security measures, perception systems, and other key technologies. These developments are driving the industry towards a future of safer, more efficient, and more connected transportation.

What are the Key Data Covered in this Autonomous Vehicles Market Research and Growth Report?

-

What is the expected growth of the Autonomous Vehicles Market between 2025 and 2029?

-

USD 624 billion, at a CAGR of 39.3%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (T and L and Military and defense), Vehicle Type (Passenger car and Commercial vehicles), Grade Type (L1, L2, L3, and L4 and L5), Geography (North America, Europe, APAC, South America, and Middle East and Africa), and Component (Sensors (LiDAR, Radar), Software, and Connectivity Systems)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for autonomy of vehicles by OEMs, High driver distraction with increase in vehicle automation

-

-

Who are the major players in the Autonomous Vehicles Market?

-

Key Companies AB Volvo, Apollo Asset Management Inc., BMW AG, Continental AG, Cruise LLC, Ford Motor Co., Honda Motor Co. Ltd., Mercedes Benz Group AG, Mobileye Technologies Ltd., Motional Inc., Navistar International Corp., Renault SAS, Robert Bosch GmbH, Stellantis NV, Tesla Inc., Toyota Motor Corp., Volkswagen AG, Waymo LLC, and Zoox

-

Market Research Insights

- The market encompasses a range of advanced technologies, including navigation algorithms, fleet management systems, and control strategies, aimed at enhancing transportation efficiency and safety. According to recent estimates, the global market for autonomous vehicles is projected to reach USD 556.67 billion by 2026. This growth is driven by the increasing demand for pedestrian detection, system availability, and traffic flow optimization. In contrast, data privacy concerns and infrastructure requirements pose significant challenges, with system reliability and ethical considerations also emerging as critical factors. Autonomous delivery robots and robotaxi operations are gaining traction, necessitating advanced sensor data processing and real-time control systems.

- Furthermore, the integration of parking assist systems, lane keeping assist, and adaptive cruise control into connected car technologies is transforming the transportation landscape. The market's evolution is marked by the development of communication networks, legal frameworks, and mapping technologies to support the seamless integration of autonomous vehicles into smart city infrastructure.

We can help! Our analysts can customize this autonomous vehicles market research report to meet your requirements.

RIA -

RIA -