Beer Packaging Market Size 2024-2028

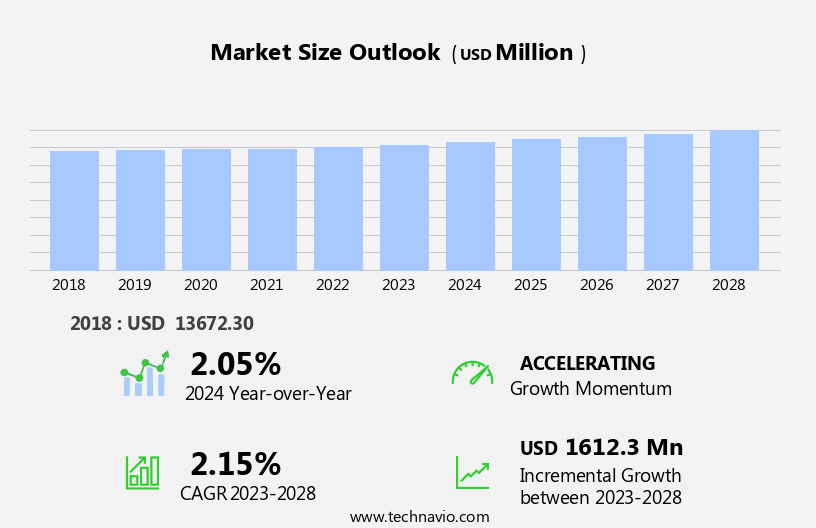

The beer packaging market size is forecast to increase by USD 1.61 billion, at a CAGR of 2.15% between 2023 and 2028.

- The market is driven by the increasing popularity of online retailing, which is transforming the way consumers purchase beer. This shift towards e-commerce is necessitating the development of innovative and sustainable packaging solutions to ensure product safety and quality during transportation. Another key trend influencing the market is the introduction of pouch packaging in the beer industry. This alternative to traditional glass and metal containers offers numerous benefits, including lightweight design, ease of use, and reduced environmental impact. However, the market faces significant challenges. The rising cost of raw materials and energy is increasing the production cost of packaging, putting pressure on manufacturers to find cost-effective solutions.

- Additionally, the growing concern for sustainability is pushing companies to invest in eco-friendly packaging alternatives, creating a competitive landscape. To capitalize on opportunities and navigate challenges effectively, market players must stay informed of consumer preferences and regulatory requirements while continuously innovating to meet evolving market demands.

What will be the Size of the Beer Packaging Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by dynamic market trends and shifting consumer preferences. Supply chain optimization, from palletizing machines to labeling and filling processes, plays a crucial role in ensuring efficient production and delivery. The rise of import beer and taproom packaging has led to increased competition, necessitating innovative brand identity strategies and waste reduction measures. Shelf life and product protection are key concerns, with packaging design and labeling machines integral to maintaining beer quality. Digital printing and offset techniques offer flexibility in meeting diverse branding needs. The circular economy ethos is gaining traction, with e-commerce packaging, crown caps, and post-consumer recycled content becoming increasingly popular.

Bio-based materials and screen printing contribute to sustainability efforts, while carbon footprint reduction and recycled content are essential for brand loyalty and consumer appeal. Beer styles, from wheat beer to non-alcoholic and craft brews, require customized packaging solutions. Inventory management and packaging materials sourcing are ongoing challenges, requiring continuous innovation and adaptation. Quality control and sustainability certifications, such as compostable packaging and corrugated cardboard, are essential for meeting evolving consumer expectations. Reusable packaging and on-premise solutions cater to the unique needs of various sectors, from craft breweries to large-scale commercial operations. Capping machines and product protection remain crucial for ensuring the integrity of the final product.

The market's continuous dynamism underscores the importance of staying informed and adaptive to meet the evolving needs of consumers and the industry.

How is this Beer Packaging Industry segmented?

The beer packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Material

- Glass

- Metal

- Others

- Type

- Bottle

- Keg

- Can

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- South America

- Brazil

- Rest of World (ROW)

- North America

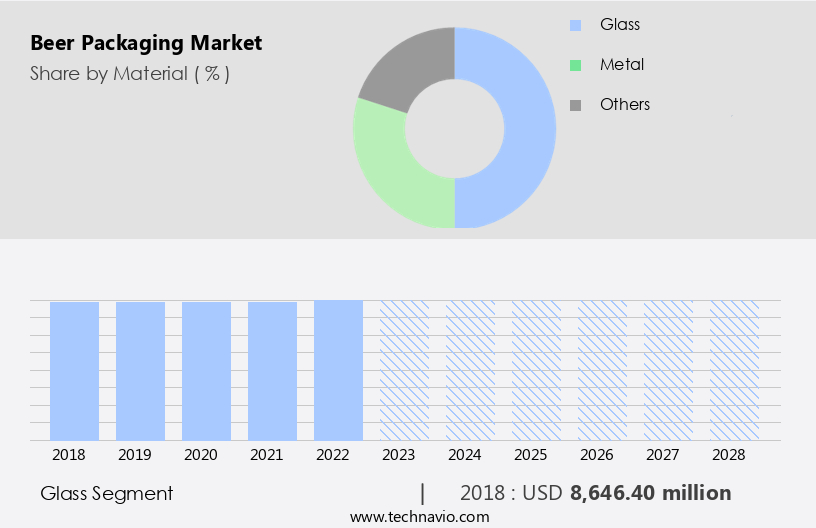

By Material Insights

The glass segment is estimated to witness significant growth during the forecast period.

The market encompasses various types of packaging solutions catering to the unique needs of brewers and consumers. Glass remains the dominant packaging material due to its ability to preserve beer's taste and shelf life. Glass bottles' impermeability to oxygen and carbon dioxide molecules enables brewers to store beer for extended periods. Additionally, glass's resistance to leaching and the pasteurization process makes it a preferred choice. In the supply chain, palletizing machines streamline the packaging process, while labeling, filling, and capping machines ensure consistency and efficiency. The import beer sector continues to grow, driving the demand for innovative packaging solutions.

The circular economy concept is gaining traction, with breweries focusing on waste reduction and sustainability. Brand identity and consumer appeal are crucial factors influencing packaging design. Beer styles, such as wheat beer and pale ale, require specific packaging considerations. Offset printing, digital printing, and flexographic printing are popular methods for creating eye-catching labels. Inventory management and packaging materials sourcing are essential aspects of the brewing process, with a growing preference for bio-based materials. Sustainability certifications, such as those for corrugated cardboard, post-consumer recycled content, and compostable packaging, are increasingly important for brand loyalty. Non-alcoholic and domestic beers, as well as e-commerce packaging, also require specialized packaging solutions.

The carbon footprint of packaging is a significant concern, with efforts underway to reduce it through the use of recycled content and reusable packaging. Craft beer and on-premise packaging present unique challenges and opportunities. Quality control is paramount, with capping machines ensuring product protection during transportation and storage. Overall, the market is dynamic, with trends focusing on sustainability, brand identity, and consumer appeal.

The Glass segment was valued at USD 8.65 billion in 2018 and showed a gradual increase during the forecast period.

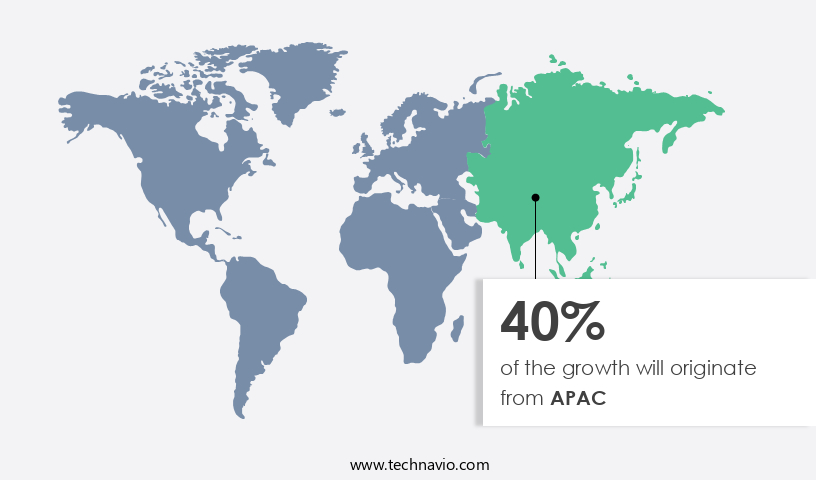

Regional Analysis

APAC is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The beer market in APAC is experiencing significant growth due to the expanding middle-class population and increasing disposable income levels. With over 7.7 billion people in the middle class globally in 2020, this demographic is driving the demand for alcoholic beverages, particularly beer. This ancient beverage, prepared from the fermentation of grains, is popular in APAC, with nations like India and China leading the way in consumption. The beer market's evolution is not limited to traditional sales channels. Taprooms and on-premise packaging have gained popularity, necessitating palletizing machines for efficient supply chain management. Imported beer continues to capture market share, with consumers seeking diverse beer styles such as wheat beer and pale ale.

Sustainability is a key trend, with a focus on circular economy principles, waste reduction, and the use of packaging materials like corrugated cardboard and post-consumer recycled content. Brand identity and consumer appeal are crucial factors, leading to the adoption of various packaging designs, labeling machines, filling machines, and capping machines. Digital printing and offset printing technologies cater to the demand for customized packaging. The market also offers e-commerce packaging solutions and various sustainability certifications. The non-alcoholic and craft beer segments are growing, catering to diverse consumer preferences. Inventory management and packaging materials sourcing are essential aspects, with a shift towards bio-based materials and reusable packaging.

Sustainability and product protection are top priorities, with a focus on reducing carbon footprint and ensuring quality control.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Beer Packaging Industry?

- Online retailing's expansion is the primary catalyst for market growth. With the increasing preference for convenience and the continuous advancement of technology, the online retail sector continues to experience significant expansion, driving the overall market forward.

- The market is experiencing significant growth due to the increasing popularity of online sales and delivery channels. This trend is particularly beneficial for small craft breweries, allowing them to expand their customer base beyond local markets. Online retailers, such as The Beer Store, Minibar, Drizly, and Liquor Mart Inc., offer a wide selection of bottled beers and craft brews, enhancing their visibility and increasing sales among tech-savvy consumers. These platforms provide detailed product descriptions and customer reviews, contributing to informed purchasing decisions. In the context of sustainability, taproom packaging and circular economy principles are gaining traction in the beer industry.

- Supply chain optimization through the use of palletizing machines and efficient labeling systems is essential for reducing waste and preserving shelf life. Imported beers also require specialized packaging to ensure safe transportation and maintain brand identity. Innovations in packaging design continue to emerge, emphasizing eco-friendly materials and immersive consumer experiences.

What are the market trends shaping the Beer Packaging Industry?

- The introduction of pouch packaging in the beer market is an emerging trend. This innovative packaging solution offers numerous benefits, including increased portability, extended shelf life, and reduced environmental impact compared to traditional glass bottles or cans.

- The market is witnessing significant innovation with the introduction of various packaging solutions to cater to evolving consumer preferences. Filling machines are being utilized to produce different beer styles, such as wheat beer, in various packaging formats. Retail packaging is increasingly focusing on sustainability, with compostable packaging gaining popularity. Customers' brand loyalty and consumer appeal are key factors driving the adoption of unique and eco-friendly packaging. Offset printing technology is used to create custom designs on packaging materials, enhancing the visual appeal and differentiating brands. Inventory management is another crucial aspect, as breweries aim to minimize waste and optimize storage space.

- Packaging materials sourcing is also a critical consideration, with an emphasis on sustainable and biodegradable options. Flexible beer pouches, which can be custom cut, sized, and printed, offer an alternative to traditional glass bottles and metal cans. Consumers appreciate the ease of handling and unique design of cans, while custom-printed pouches offer the advantage of a non-traditional shape and reduced storage space. Moreover, the environmental impact of pouches is less damaging, as they can be flattened and recycled after use, unlike cans, which require crushing and contribute to increased landfill waste.

What challenges does the Beer Packaging Industry face during its growth?

- The escalating costs of raw materials and energy significantly impact the manufacturing process and represent a major challenge to the growth of the packaging industry.

- The market is influenced by various factors that impact the cost and sustainability of packaging solutions. One significant factor is the cost of raw materials, such as aluminum and glass, which directly affects the price of packaging for beer. The rising cost of energy, often sourced from fossil fuels, also contributes to the overall expense. For instance, glass manufacturers face increasing manufacturing costs due to the escalating prices of raw materials like sand and energy. The demand for sand, a vital component in glass production, has surged due to the emergence of fracking technology. Sustainability is another critical trend in the market, with an emphasis on using eco-friendly materials, such as bio-based plastics and post-consumer recycled content.

- Digital printing and screen printing techniques are increasingly being adopted to create unique and personalized packaging designs. Non-alcoholic beer and e-commerce packaging segments are also gaining traction, necessitating innovative and efficient packaging solutions. companies must navigate these market dynamics to offer cost-effective and sustainable packaging options while minimizing their carbon footprint.

Exclusive Customer Landscape

The beer packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the beer packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, beer packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - The company specializes in innovative beer packaging solutions, including PET bottles, enhancing product preservation and sustainability in the global beverage industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Ardagh Group SA

- Ball Corp.

- Berlin Packaging LLC

- Berry Global Inc.

- Carlsberg Breweries AS

- Crown Holdings Inc.

- East Asia Packaging Ltd.

- Gamer Packaging Inc.

- MJS Packaging

- Nampak Ltd.

- O I Glass Inc.

- Orora Ltd.

- Pakko Pty Ltd.

- Plastipak Holdings Inc.

- Smurfit Kappa Group

- Tetra Laval SA

- Toyo Seikan Group Holdings Ltd.

- Verallia SA

- WestRock Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Beer Packaging Market

- In January 2024, Anheuser-Busch InBev, the world's largest brewer, announced the launch of its new lightweight, 100% recycled PET (polyethylene terephthalate) beer bottles in the United States. These bottles, which are 30% lighter than traditional glass bottles, are part of the company's commitment to reducing its carbon footprint and increasing sustainability (Anheuser-Busch InBev press release, 2024).

- In March 2024, Ball Corporation, a leading supplier of aluminum beverage packaging, signed a strategic partnership with Heineken, the Dutch brewer, to develop and manufacture aluminum cans for Heineken's brands. This collaboration aims to expand Ball's reach in the European market and strengthen Heineken's sustainability initiatives (Ball Corporation press release, 2024).

- In May 2024, Constellation Brands, a major beer, wine, and spirits company, completed the acquisition of Modelo's U.S. Business from Anheuser-Busch InBev for USD4.8 billion. This deal significantly expanded Constellation Brands' beer portfolio and market share in the U.S. (Constellation Brands press release, 2024).

- In April 2025, Crown Holdings, a global packaging company, received approval from the European Commission for its acquisition of Alcan Packaging, a leading European supplier of metal packaging. This merger created a larger player in the European metal packaging market and expanded Crown's capabilities in the beverage sector (European Commission press release, 2025).

Research Analyst Overview

- In the dynamic market, brand perception plays a crucial role in consumer purchase decisions. Point-of-sale displays and packaging aesthetics are essential for capturing customers' attention. The packaging lifecycle encompasses various stages, from brewing processes to sales channels, including retail partnerships and e-commerce platforms. Circular economy models and recycling programs are increasingly important for minimizing packaging waste and reducing environmental impact. Packaging regulations and food safety requirements are key considerations for brewers, influencing material selection, design for manufacturing, and production efficiency. Supply chain optimization and inventory control are vital for managing costs and ensuring quality assurance. Sustainability reporting and cost optimization are essential marketing strategies for breweries seeking to differentiate themselves.

- Demand forecasting and sales channels are critical for breweries to optimize their distribution networks and meet consumer demand. Smart packaging, such as RFID tags and sensory evaluation, offer opportunities for enhancing customer experience and improving product quality. Breweries are also exploring innovations in packaging, including life cycle assessment, design for manufacturing, and end-of-life management, to reduce their carbon footprint and promote sustainability. Furthermore, breweries are adopting circular economy models and implementing recycling programs to minimize packaging waste and reduce their environmental impact. Packaging costs are a significant consideration, with breweries seeking to balance affordability and sustainability. Breweries are also exploring new sales channels, such as online sales, to expand their reach and meet evolving consumer preferences.

- In summary, the market is characterized by a focus on sustainability, innovation, and consumer experience. Breweries are exploring various strategies to optimize their packaging lifecycle, from brewing processes to end-of-life management, while also addressing regulatory requirements and consumer preferences. Packaging regulations, food safety, and cost optimization are key considerations, with breweries seeking to balance affordability and sustainability. The use of smart packaging and RFID tags is becoming increasingly common, offering opportunities for enhancing product quality and customer experience. Ultimately, the market is a dynamic and evolving landscape, with breweries continually seeking to innovate and adapt to changing consumer preferences and regulatory requirements.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Beer Packaging Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.15% |

|

Market growth 2024-2028 |

USD 1612.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.05 |

|

Key countries |

US, China, UK, Germany, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Beer Packaging Market Research and Growth Report?

- CAGR of the Beer Packaging industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the beer packaging market growth of industry companies

We can help! Our analysts can customize this beer packaging market research report to meet your requirements.

RIA -

RIA -