Cardiopulmonary Stress Testing Systems Market Size 2024-2028

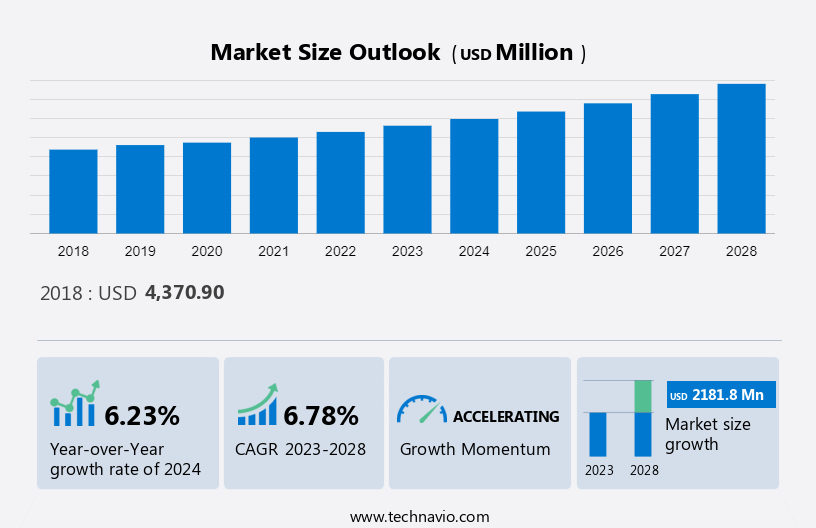

The cardiopulmonary stress testing systems market is to increase by USD 2.18 billion and is estimated to grow at a CAGR of 6.78% between 2023 and 2028. The market is experiencing significant expansion, driven by several key factors. The increasing prevalence of cardiovascular diseases (CVDs) and respiratory disorders necessitates more specialized diagnostic services. This trend is further fueled by the rising incidence of cardiac diseases, which is leading to an increased demand for advanced testing systems. Additionally, the growth of insurance providers and their coverage for diagnostic services is creating new opportunities for market expansion. These factors collectively contribute to the robust growth of the market.

What will be the size of the Market During the Forecast Period?

To learn more about this report, Download Report Sample

Market Dynamics and Customer Landscape

The Market is witnessing significant growth propelled by the increasing prevalence of heart and lung disorders, particularly among the elderly and geriatric populations. Athletes and individuals with cardiovascular diseases benefit from technologically enhanced testing systems that accurately measure cardiac output, arterial pressure, and venous return during exercise. Cardiopulmonary stress testing plays a crucial role in diagnosing conditions such as arrhythmia, valve imbalance, coronary artery disease, and acute myocardial infarction. The market forecast depends on the Heart and lung function, Elderly population, Portable device sector, Ischemic heart disease, Myocardial infection, Geriatric population, Coronary artery diseases, Angina pectoris, Congenital heart defect. These diagnostic techniques aid in early detection and management, ultimately reducing mortality rates associated with cardiovascular diseases. The market is witnessing a surge in demand for portable devices, including high-sensitivity ECG equipment, catering to the growing need for convenient diagnostic solutions. Healthcare spending on cardiovascular disease management continues to rise, driving innovation in cardiopulmonary stress testing systems. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The increasing number of heart specialty centers is notably driving market growth. The growing prevalence of CVDs across the globe is driving the growth of cardiac specialty centers, mainly in developed countries. The rising need to diagnose and treat CVDs is driving the demand for specialized outpatient cardiovascular centers. These centers/clinics offer the diagnosis and treatment of various CVDs, such as heart failure, hypertrophic cardiomyopathy, atrial fibrillation, hypertension, and valvular heart disease. The main aim of these clinics is to provide improved clinical outcomes at reduced costs and fulfill the need of patients.

These clinics are equipped with advanced devices for various diagnostic purposes. The availability of licensed and skilled physicians and other healthcare personnel in specialty cardiac centers has a positive impact on the clinical workflow and patient outcomes. Therefore, the rising number of specialized heart centers is expected to spur the growth of the global market during the forecast period.

Significant Market Trend

The growing integration of technologies is an emerging trend in the market. The global market has been witnessing an increase in the adoption of new technology platforms. Most providers have started focusing on virtual platforms to enable easy and better diagnoses from any location. Individuals and doctors are benefiting significantly from digital health devices and mobile health applications. Heart rate monitoring devices, coupled with mobile health applications, are likely to be adopted by many consumers and will have a positive effect on the healthcare industry. The development of new monitoring technologies has helped in improving disease diagnosis and treatment.

Technological advances have also allowed the flexibility and portability of these systems. Continuous digitization of record systems in physicians' offices and cardiology departments has led companies to improve data connectivity for a range of management solutions. For instance, the CASE exercise testing system by GE HealthCare Technologies Inc. (GE Healthcare) enables quick and easy access to cardiac functions during exercise for better diagnostic confidence. Thus, technological advances in heart rate monitoring devices and their integration with other compatible technologies will have a positive impact on the growth of the global market during the forecast period.

Major Market Challenge

The high cost of stress-testing devices is a major challenge impeding market growth. Cardiopulmonary stress testing is performed in hospitals, clinics, and diagnostic laboratories to diagnose and assess patients with CVDs. The systems used for cardiopulmonary stress testing are expensive, owing to which medium and small hospitals and clinics find it difficult to purchase such products. The high cost of these systems also restricts their use in home care settings and small clinical laboratories. It may impact the cost of the overall diagnosis procedure. The cost of the systems used for stress testing varies depending on the type of product used for the diagnosis.

Furthermore, stress tests coupled with echocardiography or nuclear imaging are more expensive, which increases the out-of-pocket expenses of patients. Moreover, the radiation exposure from the radionuclide imaging used during the nuclear stress test (myocardial perfusion scan) carries more risks, which may limit the acceptance of this test among patients. These factors are expected to hamper the growth of the global market during the forecast period.

Market Customer Landscape

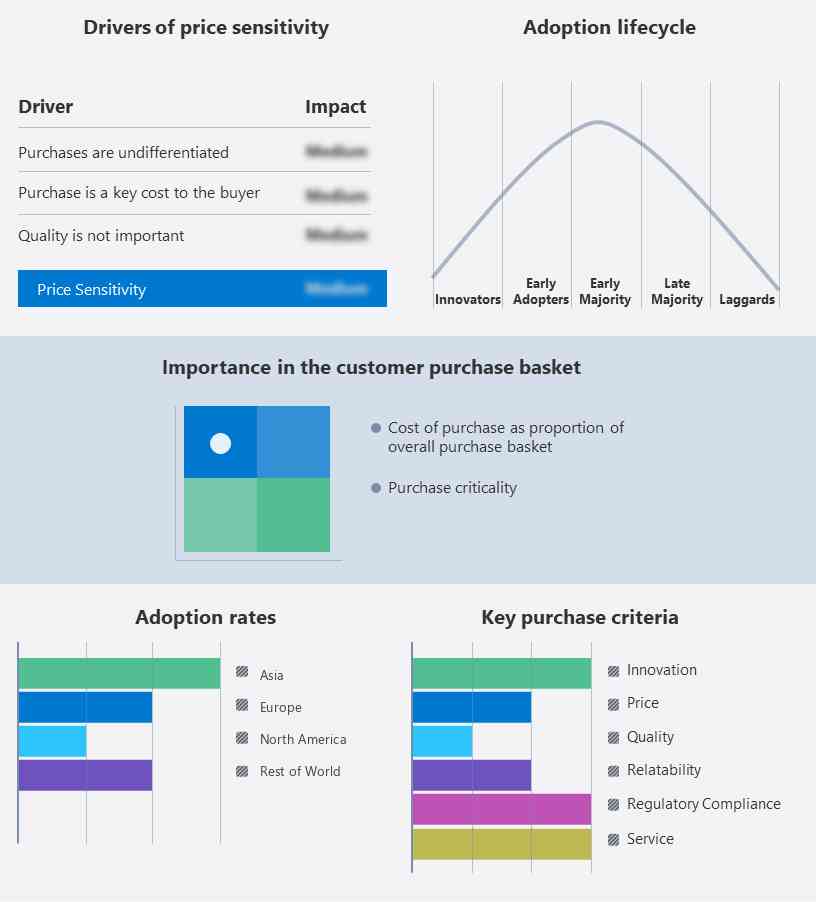

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

Who are the Major Market Players?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Biosensors International Group Ltd. - The company offers pioneering technology and proprietary technology. The key offerings of the company include various cardiopulmonary stress testing systems.

The report also includes detailed analyses of the competitive landscape of the market growth and information about 15 market companies, including:

- Becton Dickinson and Co.

- Cardinal Health Inc.

- COSMED Srl

- Fukuda Denshi Co. Ltd.

- General Electric Co.

- Halma Plc

- Hill Rom Holdings Inc.

- Koninklijke Philips NV

- MGC Diagnostics Corp.

- Nasiff Associates Inc.

- Nihon Kohden Corp.

- Nonin Medical Inc.

- SCHILLER AG

- Siemens Healthineers AG

- SunTech Medical Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

What is the Fastest-Growing Segment in the Market?

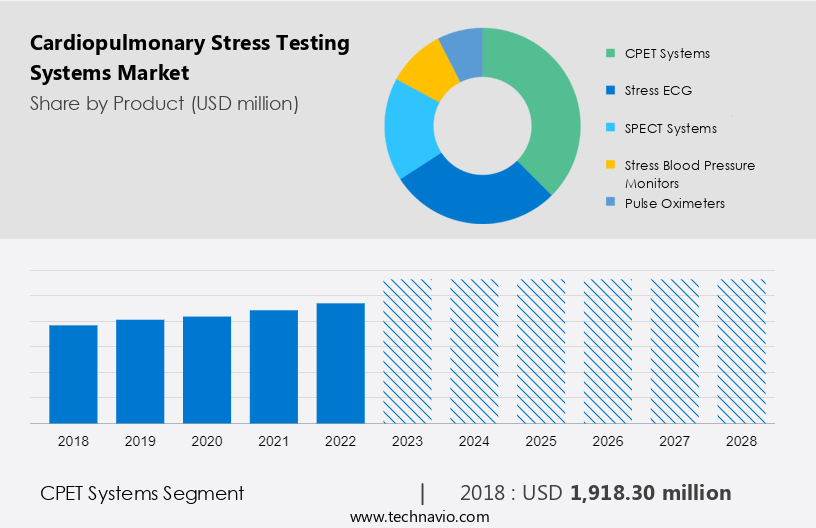

The market share growth by the CPET segment will be significant during the forecast period. The CPET is used for the evaluation of the cardiopulmonary system. CPET, also known as CPX, is a noninvasive cardiopulmonary stress testing method designed to evaluate the activity of the heart and lungs during exercise. CPET is considered the gold standard by physicians for the functional assessment and evaluation of patients with chronic heart failure.

Get a glance at the market contribution of various segments Request a PDF Sample

The CPET systems segment was valued at USD 1.92 billion in 2018 and continued to grow until 2022. CPET is an advanced diagnostic tool that can help physicians assess consolidative exercise responses involving the pulmonary, cardiovascular, and skeletal muscle systems. This test is widely used for a broad range of clinical applications for the evaluation of undiagnosed exercise intolerance and the determination of functional impairments. CPET systems are mainly used for CPET testing. Lightweight and portable CPET systems are mainly used in hospitals and clinics for cardiopulmonary stress testing. The increasing use of CPET systems as a validated tool for the diagnosis of patients with heart failure and the capability of these systems to perform distinct assessments by simplifying the precise and reliable measurement of the functional capacity of patients are the major factors fueling the adoption of these systems by physicians. companies in the global market are also focusing on the development of CPET systems. Hence, these factors will drive the growth of the global market during the forecast period.

Which are the Key Regions for the Market?

For more insights on the market share of various regions Request PDF Sample now!

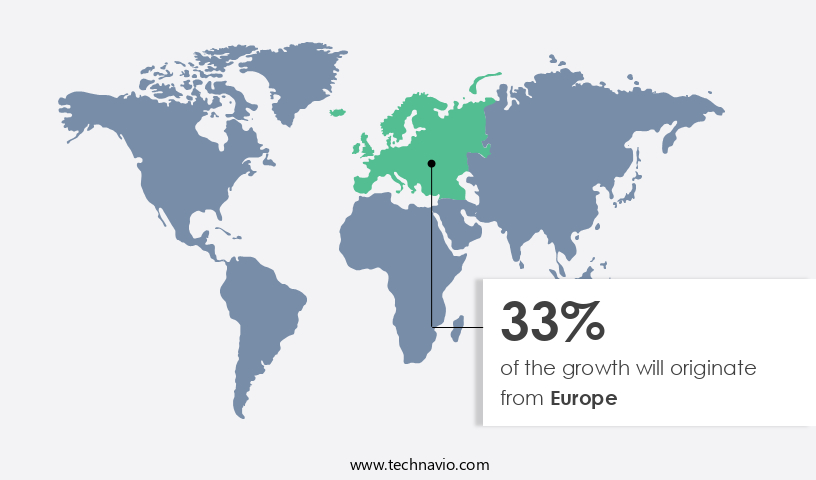

Europe is estimated to contribute 33% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

Anothere significant region contributing to the market growth is North America. North America accounted for the major share of the global market in 2022. This is mainly due to the rapid growth in the number of cardiac specialty centers and the favorable reimbursement scenario in the region. The high prevalence of CVDs in this region, coupled with the presence of skilled physicians to conduct advanced diagnostic procedures, is likely to drive the market in North America during the forecast period. Government organizations and other private organizations are taking various initiatives, such as funding and program launches, to increase the awareness of CVDs in North America. In the US, the American Heart Association (AHA) observed February 2022 as American Heart Month, which is a federally designated event to promote awareness about heart diseases and their early diagnosis. Such initiatives support the research on diagnosis and treatment procedures for evaluating and treating heart diseases. This is expected to augment the growth of the market in the region during the forecast period.

Favorable initiatives in North American countries are driving the growth of the market in the region. The National Heart, Lung, and Blood Institute of the National Institutes of Health (NIH) has developed an awareness program, The Heart Truth, to create awareness of heart diseases. With the help of this program, the National Heart, Lung, and Blood Institute works with national and community organizations and provides educational materials for the public and health professionals to increase awareness of heart diseases, especially among women, in the US. This will help in increasing the screening and diagnostic procedures for heart diseases and fuel the growth of the market in North America during the forecast period.

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments

- Product Outlook

- CPET systems

- Stress ECG

- SPECT systems

- Stress blood pressure monitors

- Pulse oximeters

- End-user Outlook

- Hospitals

- Ambulatory surgical centers

- Diagnostic centers

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- Asia

- China

- India

- Argentina

- Others

- Rest of World

- Saudi Arabia

- South Africa

- Brazil

- Others

- North America

You may also interested in below market reports:

- Airway Management Products Market: Airway Management Products Market Analysis North America, Europe, Asia, Rest of World (ROW) - US, Canada, Germany, UK, China - Size and Forecast

- Extracorporeal Membrane Oxygenation Machines Market: Extracorporeal Membrane Oxygenation Machines Market by Modality, Product, and Geography - Forecast and Analysis

- Thoracic Surgery Market: Thoracic Surgery Market Analysis North America, Europe, Asia, Rest of World (ROW) - US, Germany, France, China, Japan - Size and Forecast

Market Analyst Overview

The Market is witnessing remarkable growth driven by the increasing prevalence of cardiovascular conditions and lifestyle diseases, compounded by rising obesity rates and serum cholesterol levels. These factors contribute to a surge in hospital admissions and the demand for monitoring products in healthcare facilities. Cardiac output measurements play a pivotal role in diagnosing and managing heart-related ailments, supported by advanced technologies such as the cardiopulmonary bypass machine and single-photon emission computed tomography. Healthcare professionals rely on software-based stress testing solutions and exercise cardiac stress testing, often utilizing treadmills to assess heart rhythm and identify diseases like heart attack and heart failure.

Artificial intelligence and wearable technologies are revolutionizing disease identification, enabling early intervention and personalized treatment plans. Specialty clinics and cardiology clinics are adopting smart technologies and integrated software systems to enhance patient care and streamline workflows. The portable device sector is experiencing significant growth, catering to the demand for convenient diagnostic solutions and enabling remote monitoring of patients. As the prevalence of cardiovascular diseases continues to rise globally, the Market remains a critical component of healthcare delivery, driving innovation and improving outcomes for patients.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

186 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 2.18 billion |

|

Market structure |

USD Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

Europe at 33% |

|

Key countries |

US, Germany, France, UK, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Baxter International Inc., Becton Dickinson and Co., Biosensors International Group Ltd., Cardinal Health Inc., COSMED Srl, Fukuda Denshi Co. Ltd, General Electric Co., Halma Plc, InBody Co. Ltd., Koninklijke Philips N.V., MGC Diagnostics Corp., Nasiff Associates Inc., Neurosoft, Nihon Kohden Corp., Nonin Medical Inc., OSI Systems Inc., SCHILLER AG, Siemens Healthineers AG, SunTech Medical Inc., Thermo Fisher Scientific Inc., and Vyaire Medical Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market between 2023 and 2028

- Precise estimation of the size of the market size and its contribution to the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the industry across North America, Europe, Asia, and Rest of World (ROW)

- A thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market players

We can help! Our analysts can customize this report to meet your requirements. Get in touch

RIA -

RIA -