Thoracic Surgery Market Size 2024-2028

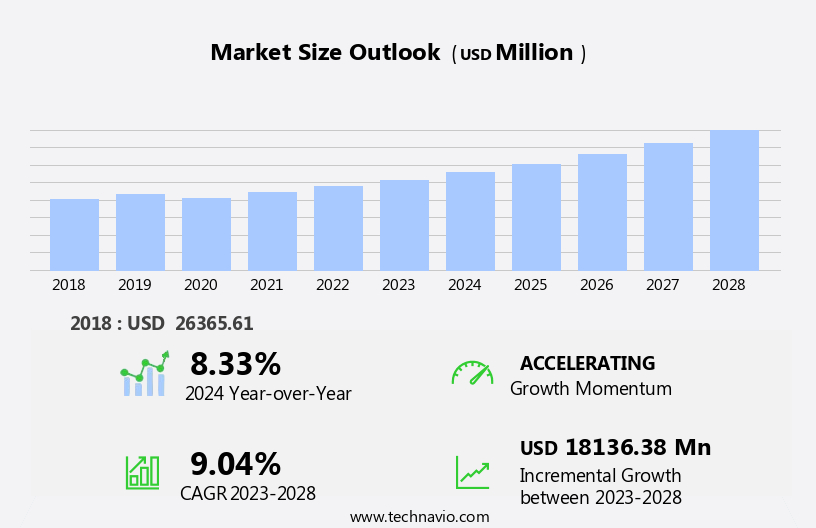

The thoracic surgery market size is forecast to increase by USD 18.14 billion at a CAGR of 9.04% between 2023 and 2028.

What will be the Size of the Thoracic Surgery Market During the Forecast Period?

How is this Thoracic Surgery Industry segmented and which is the largest segment?

The thoracic surgery industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Ambulatory surgical centers

- Specialty clinics

- Product

- CRM and cardiac assist devices

- Heart valve repair and replacement devices

- Cardiopulmonary devices

- Heart defect closure devices

- Other thoracic surgery devices

- Geography

- North America

- US

- Europe

- Germany

- France

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

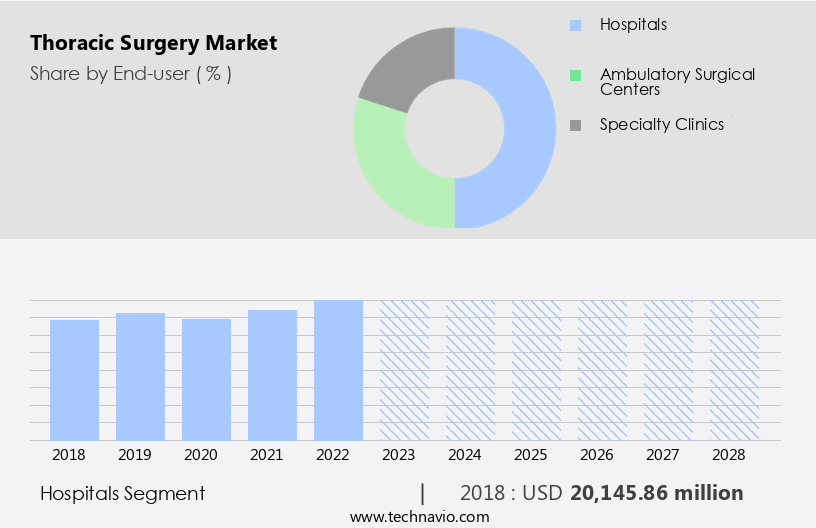

By End-user Insights

- The hospitals segment is estimated to witness significant growth during the forecast period.

Thoracic surgery devices are primarily utilized in hospitals, accounting for a significant market share due to the complex nature of thoracic conditions, such as advanced cardiovascular diseases and late-stage lung cancer, which necessitate extensive resources, sophisticated technologies, and a multidisciplinary approach. The expansion of private hospitals and clinics, the provision of specialized thoracic surgery packages, and the rising incidence of respiratory disorders are key market growth drivers. Moreover, key players invest in establishing robust distribution networks with hospitals to boost market presence. The thoracic surgery devices market encompasses a range of instruments, including MRI-compatible devices, bio-absorbable stents, self-expandable stents, surgical sutures, staples, handheld surgical equipment, electrosurgical devices, forceps and spatulas, retractors, dilators, graspers, auxiliary instruments, cutter instruments, and various lung cancer-related surgical tools.

Common procedures include lobectomy, pneumonectomy, and esophagectomy, with potential complications including wound infection, pneumonia, hemorrhage, respiratory failure, and the use of energy-based devices for lung disorders.

Get a glance at the Thoracic Surgery Industry report of share of various segments Request Free Sample

The Hospitals segment was valued at USD 20.15 billion in 2018 and showed a gradual increase during the forecast period.

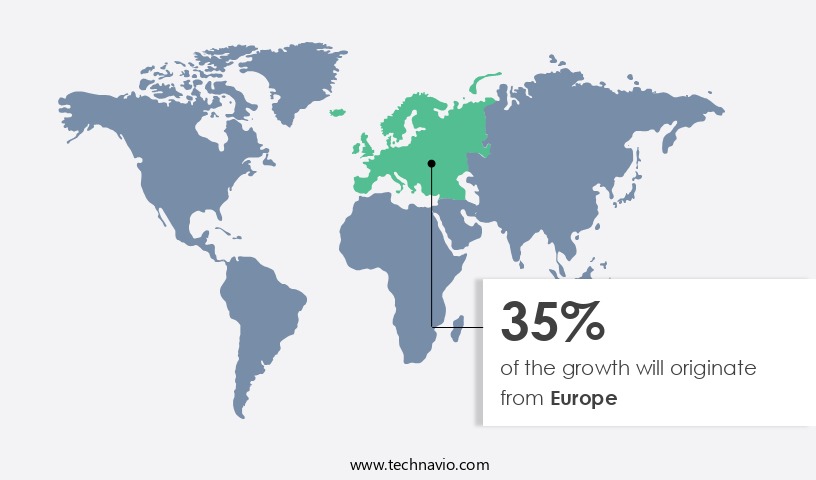

Regional Analysis

- Europe is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market represents a significant share In the market in 2023. Factors such as favorable reimbursement policies, high healthcare expenditure, and the increasing prevalence of cardiac and respiratory disorders contribute to this dominance. According to the American College of Allergy, Asthma & Immunology, approximately 8.3% of Americans have asthma, with 20.4 million adults and 6.1 million children affected. Thoracic surgeries, including heart, lung, and redo heart surgeries for cardiac disorders, and aortic surgery for aortic dissection, are common procedures. Thoracic surgeries also address lung disorders like lung cancer and COPD. The geriatric population, with its increased susceptibility to cardiac and respiratory diseases, further fuels market growth.

Advancements in medical instruments, such as MRI, bio-absorbable stents, self-expandable stents, surgical sutures, staples, handheld surgical equipment, electrosurgical devices, forceps, and spatulas, retractors, dilators, graspers, auxiliary instruments, cutter instruments, clamps, scissors, spreaders, and needle holders, facilitate faster healing and shorter hospitalization. Energy-based devices and minimally invasive procedures are also gaining popularity. Postoperative care, patient-centered care, and the adoption of cardiopulmonary devices and chest drains are essential aspects of thoracic surgery.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Thoracic Surgery Industry?

Rising prevalence of respiratory diseases is the key driver of the market.

What are the market trends shaping the Thoracic Surgery Industry?

Emergence of telehealth and remote monitoring is the upcoming market trend.

What challenges does the Thoracic Surgery Industry face during its growth?

Concerns associated with screening and diagnosis of thoracic surgery is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The thoracic surgery market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the thoracic surgery market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, thoracic surgery market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Abbott Laboratories - Thoracic surgery involves the treatment of various conditions affecting the chest and lungs, including heart diseases. The market for thoracic surgery products encompasses a range of innovative solutions. Among these, Cardiac Rhythm Management (CRM) catheters and CRT devices play significant roles. CRM catheters are instrumental in diagnosing and treating cardiac arrhythmias, while CRT devices help restore synchronous contractions of the heart chambers, improving heart function. These advanced technologies contribute to enhanced patient outcomes and improved quality of life. The thriving the market reflects the growing demand for advanced medical solutions to address complex cardiac and thoracic conditions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AbbVie Inc.

- Becton Dickinson and Co.

- Biosensors International Group Ltd.

- BioVentrix Inc.

- Boston Scientific Corp.

- Cardio Medical GmbH

- Edwards Lifesciences Corp.

- GE Healthcare Technologies Inc.

- Intuitive Surgical Inc.

- Johnson and Johnson

- LivaNova Plc

- Medtronic Plc

- Richard Wolf GmbH

- Teleflex Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Thoracic surgery refers to a specialized branch of medicine that deals with the surgical treatment of disorders related to the chest and lungs. This complex field encompasses a wide range of procedures, from the removal of tumors and repair of cardiac defects to the treatment of respiratory conditions and lung resections. The market is driven by several factors, including the increasing prevalence of cardiac and lung disorders, an aging population, and advancements in surgical techniques and technologies. The geriatric population is particularly vulnerable to thoracic conditions, as age increases the risk of developing heart diseases, lung disorders, and other related conditions.

Patient-centered care and postoperative care are critical aspects of thoracic surgery. Faster healing and shorter hospitalization are key priorities for both patients and healthcare providers, leading to a growing demand for advanced surgical instruments and technologies. These include energy-based devices, self-expandable stents, and bio-absorbable stents, among others. Surgical instruments play a crucial role in thoracic surgery. Handheld surgical equipment, such as forceps, spatulas, and retractors, are essential for accessing and manipulating the surgical site. Dilators, graspers, and auxiliary instruments are used to facilitate the procedure and improve surgical outcomes. Cutter instruments and scissors are used for cutting and separating tissues, while clamps and spreaders are used for controlling bleeding and maintaining tissue separation.

Thoracic surgery also involves the use of advanced cardiopulmonary devices, such as heart defect closure systems and cardiac assist devices. These technologies help to minimize invasiveness, reduce the risk of complications, and improve patient outcomes. The market is diverse and complex, with a wide range of applications and procedures. Lung cancer and COPD are common indications for thoracic surgery, with procedures such as lobectomy and pneumonectomy used to remove affected lung tissue. Other procedures include the treatment of conditions such as aortic dissection and aortic surgery, as well as redo heart surgery for patients with recurring cardiac issues.

Despite the advances in thoracic surgery, complications such as wound infection, pneumonia, hemorrhage, and respiratory failure remain a concern. Ongoing research and development efforts are focused on reducing the risk of these complications and improving patient outcomes through the use of advanced technologies and techniques. In conclusion, the market is driven by the increasing prevalence of cardiac and lung disorders, an aging population, and advancements in surgical techniques and technologies. Patient-centered care and postoperative care are critical priorities, and surgical instruments and advanced cardiopulmonary devices play a crucial role in minimizing invasiveness, reducing complications, and improving patient outcomes.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.04% |

|

Market growth 2024-2028 |

USD 18136.38 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.33 |

|

Key countries |

US, Germany, France, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Thoracic Surgery Market Research and Growth Report?

- CAGR of the Thoracic Surgery industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the thoracic surgery market growth of industry companies

We can help! Our analysts can customize this thoracic surgery market research report to meet your requirements.

RIA -

RIA -