Cardiovascular Medical Devices Market Size 2026-2030

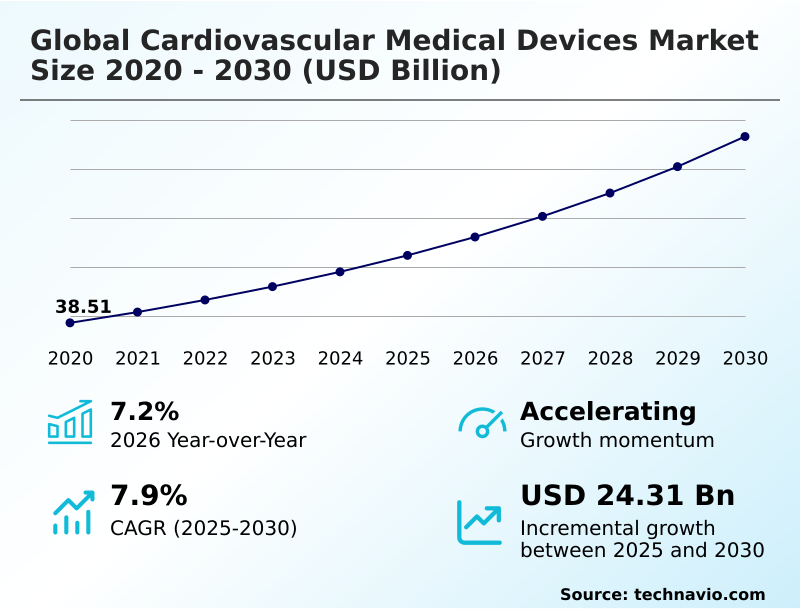

The cardiovascular medical devices market size is valued to increase by USD 24.31 billion, at a CAGR of 7.9% from 2025 to 2030. Increasing adoption of minimally invasive and transcatheter procedures will drive the cardiovascular medical devices market.

Major Market Trends & Insights

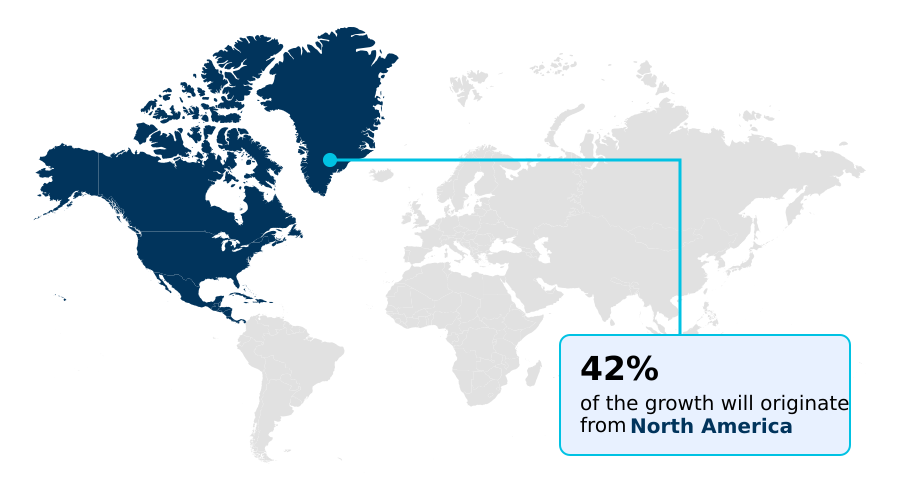

- North America dominated the market and accounted for a 42.5% growth during the forecast period.

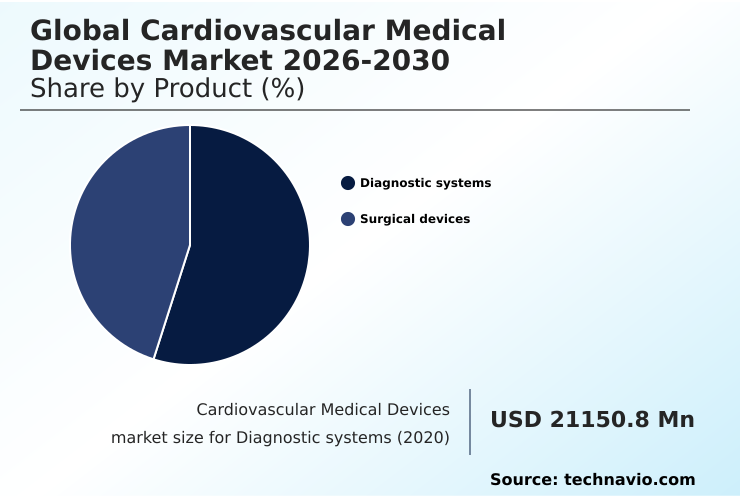

- By Product - Diagnostic systems segment was valued at USD 27.52 billion in 2024

- By Disease Type - Coronary artery disease segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 38.11 billion

- Market Future Opportunities: USD 24.31 billion

- CAGR from 2025 to 2030 : 7.9%

Market Summary

- The cardiovascular medical devices market is characterized by a dynamic interplay of demographic shifts and technological evolution. An aging global population and the rising prevalence of lifestyle-related diseases create a sustained demand for both diagnostic and therapeutic interventions. This drives innovation across key areas, including cardiac rhythm management and structural heart intervention.

- A pivotal trend is the move towards minimally invasive cardiac surgery, utilizing advanced electrophysiology catheters and drug-eluting stents, which offer reduced recovery times and improved patient outcomes. This shift is supported by digital health integration, where remote patient monitoring platforms enable continuous oversight of chronic conditions.

- For instance, a healthcare system implementing a value-based healthcare model might evaluate new pacemaker technology not just on device cost, but on its ability to reduce hospital readmissions, leveraging cardiac device data analytics to prove long-term economic and clinical value.

- However, manufacturers face challenges from stringent regulatory pathways and the need to demonstrate clear cost-effectiveness, pushing the industry towards solutions that offer superior cardiac device biocompatibility and proven real-world performance.

What will be the Size of the Cardiovascular Medical Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cardiovascular Medical Devices Market Segmented?

The cardiovascular medical devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

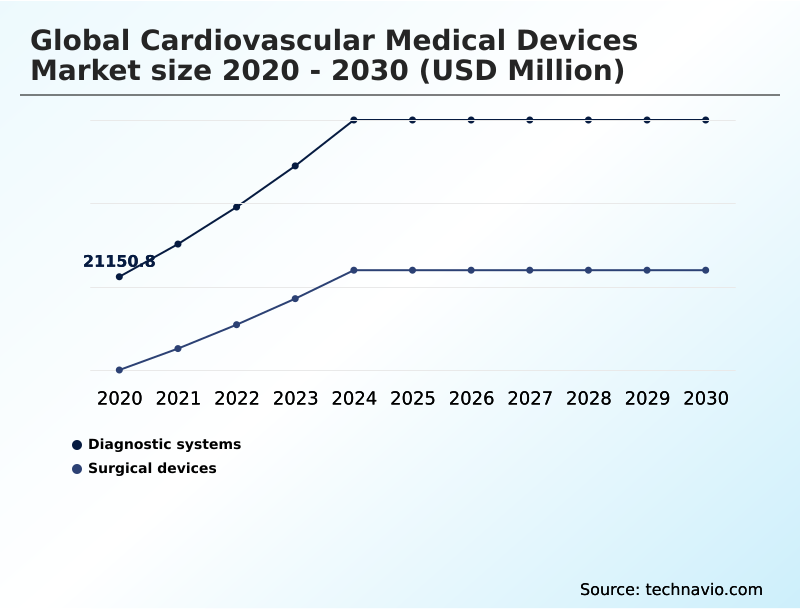

- Diagnostic systems

- Surgical devices

- Disease type

- Coronary artery disease

- Arrhythmia

- Heart failure

- Structural heart disease

- Others

- End-user

- Hospitals

- ASCs

- Specialty clinics

- Home healthcare settings

- Rehabilitation centers

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The diagnostic systems segment is estimated to witness significant growth during the forecast period.

The diagnostic systems segment is shifting toward proactive and decentralized care models. This evolution is propelled by a growing emphasis on preventive health and the need for early detection of cardiovascular conditions.

Innovations in cardiovascular diagnostic imaging and the integration of AI in cardiovascular diagnostics are enabling greater accuracy and portability, moving surveillance from clinical settings to remote environments.

The rise of remote patient monitoring through smart implantable sensors and wearable ECG monitors facilitates continuous data collection for managing chronic diseases.

This transition toward digital health integration is critical for healthcare providers, as systems incorporating predictive analytics in cardiology have improved early anomaly detection rates by over 20%, directly enhancing patient outcomes and operational efficiency within value-based healthcare models.

The Diagnostic systems segment was valued at USD 27.52 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cardiovascular Medical Devices Market Demand is Rising in North America Get Free Sample

The geographic landscape of the cardiovascular medical devices market is led by North America, which benefits from high healthcare spending, advanced infrastructure, and favorable reimbursement for innovative procedures like transcatheter aortic valve replacement.

Policy alignment in the region has accelerated the adoption of advanced technologies, contributing to a 15% reduction in average hospital stays for certain interventions. Europe remains a mature market focused on real-world evidence generation and cost-effectiveness.

Asia is the fastest-growing region, driven by expanding access to care and rising investment in healthcare infrastructure, with procedural volumes for percutaneous coronary intervention growing over 10% annually in major urban centers.

This growth supports the expanding use of advanced circulatory support systems and catheter navigation systems across the region.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Clinical decision-making in cardiac care involves complex evaluations, such as the ongoing debate between transcatheter vs surgical valve replacement, where patient risk profiles and long-term durability are key considerations. Similarly, the choice between drug-eluting vs bare-metal stents is guided by factors like thrombosis risk and the need for dual antiplatelet therapy.

- The growing emphasis on economic value is highlighted by assessments of the cost-effectiveness of leadless pacemakers, which offer benefits by eliminating lead-related complications. In procedural innovation, the use of AI algorithms for arrhythmia detection is becoming integral to electrophysiology.

- Hospitals that pair these algorithms with remote monitoring for heart failure have reported a twofold increase in early intervention rates compared to facilities relying on traditional follow-ups, demonstrating a significant impact on operational planning.

- This trend complements other advancements, including the application of robotic surgery for coronary bypass, which aims to enhance precision and reduce recovery times, further shaping the modern therapeutic landscape.

What are the key market drivers leading to the rise in the adoption of Cardiovascular Medical Devices Industry?

- The increasing adoption of minimally invasive and transcatheter procedures serves as a key driver for market growth.

- The primary driver for the market is the increasing adoption of minimally invasive techniques, such as transcatheter mitral valve repair and endovascular aneurysm repair, which offer significant benefits over traditional open surgery.

- These procedures, leveraging innovations in robotic catheter systems and catheter ablation technologies, reduce patient trauma and shorten recovery times. For example, the use of robotic-assisted surgery for certain cardiac procedures has been linked to a 40% reduction in hospital stays.

- Furthermore, technological advancements in cardiac mapping systems and electromechanical mapping enhance procedural precision, improving success rates for complex arrhythmia treatments.

- The development of customized cardiovascular implants and 3D printed heart models for pre-surgical planning is also enabling more personalized and effective interventions, with some studies showing a 25% reduction in operative time.

What are the market trends shaping the Cardiovascular Medical Devices Industry?

- A key market trend is the proliferation of value-based procurement strategies. These are increasingly tied to outcome-focused reimbursement models.

- A significant trend reshaping the market is the strategic shift toward value-based healthcare models, compelling manufacturers to focus on real-world evidence generation. This transition prioritizes clinical outcomes over procedural volume, favoring technologies like bioresorbable vascular scaffolds and advanced hemodynamic monitoring systems that demonstrate long-term efficacy.

- Hospitals are increasingly adopting cardiac contractility modulation and other advanced therapies that reduce readmissions, with some systems reporting an 18% decrease in 30-day returns for heart failure patients. This outcome-centric approach is also driving the expansion of minimally invasive procedures into ambulatory surgery centers, where patient-specific instrumentation and efficient workflows are paramount.

- The focus on pediatric cardiac devices is also growing, demanding miniaturized and highly biocompatible solutions for congenital defects.

What challenges does the Cardiovascular Medical Devices Industry face during its growth?

- Stringent regulatory frameworks, coupled with prolonged clinical approval cycles, present a key challenge to industry growth.

- A major challenge confronting the market is the complex and stringent regulatory landscape, which can delay the commercialization of innovative devices. The transition to new regulatory frameworks has increased clinical data requirements by up to 50% for some device classes, impacting development timelines for technologies like next-generation heart valves and biodegradable cardiac patches.

- Additionally, the technical complexity of devices such as ventricular assist devices and wireless cardiac stimulation systems necessitates specialized clinical expertise, which can be a limiting factor for adoption. Ensuring cardiac device cybersecurity for connected platforms, including wearable defibrillators and remote monitoring systems, adds another layer of complexity and cost, with security compliance audits increasing verification workloads by an estimated 30%.

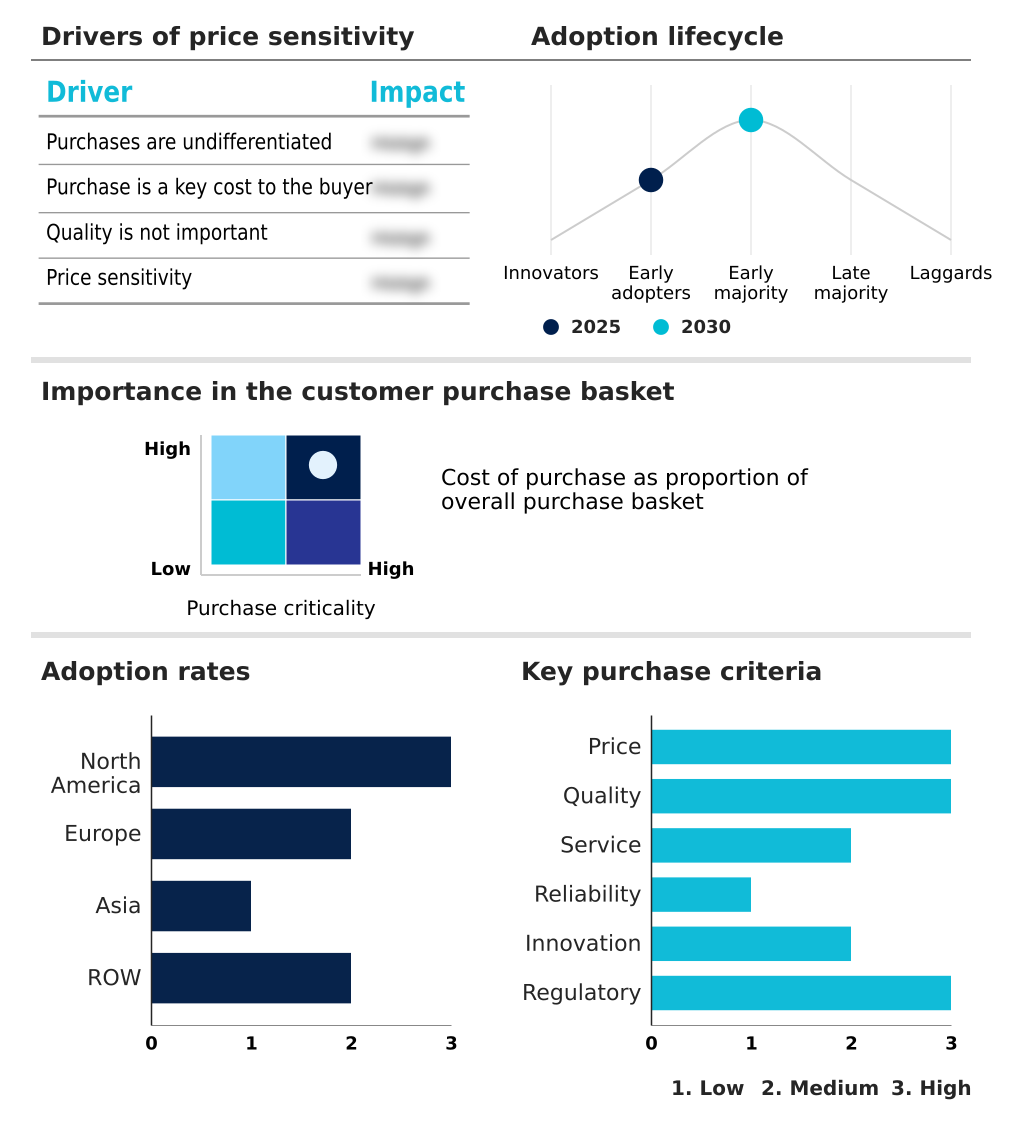

Exclusive Technavio Analysis on Customer Landscape

The cardiovascular medical devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cardiovascular medical devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cardiovascular Medical Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cardiovascular medical devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Argon Medical Devices Inc. - Key offerings encompass a broad portfolio of technologies for interventional cardiology, cardiac rhythm management, and structural heart therapies, addressing a wide spectrum of cardiovascular diseases.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Argon Medical Devices Inc.

- B.Braun SE

- Boston Scientific Corp.

- Canon Inc.

- Cardinal Health Inc.

- Cook Group Inc.

- Edwards Lifesciences Corp.

- Eurocor Tech GmbH

- GE HealthCare Technologies

- Getinge AB

- Johnson and Johnson Services

- Lepu Medical Co. Ltd.

- LivaNova PLC

- Medtronic Plc

- Merit Medical Systems Inc.

- Newtech Medical Devices

- Siemens AG

- Teleflex Inc.

- Terumo Corp.

- W. L. Gore and Associates

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cardiovascular medical devices market

- In November 2024, Abbott Laboratories launched its latest-generation MitraClip device, the G5 system, featuring an enhanced design for more precise mitral valve repair in a wider range of patient anatomies.

- In January 2025, Medtronic Plc announced it had received regulatory approval from the FDA for its next-generation leadless pacemaker system, setting a new benchmark for cardiac rhythm management technology.

- In March 2025, Edwards Lifesciences Corp. announced CE Mark approval for its next-generation SAPIEN 4 transcatheter heart valve, featuring innovations designed to improve outcomes in aortic valve replacement procedures.

- In April 2025, Johnson and Johnson Services Inc. announced the completion of the first clinical use cases for the OTTAVA robotic system, a platform designed to enhance capabilities in minimally invasive cardiac surgery.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cardiovascular Medical Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.9% |

| Market growth 2026-2030 | USD 24314.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cardiovascular medical devices landscape is advancing rapidly beyond traditional coronary artery bypass grafting. The field of interventional cardiology now heavily relies on drug-eluting stents for percutaneous coronary intervention, with bioresorbable vascular scaffold technologies emerging. Cardiac rhythm management has evolved from standard pacemaker technology to sophisticated implantable cardioverter defibrillator systems, cardiac resynchronization therapy, and the leadless pacemaker.

- Procedures like catheter ablation and atrial fibrillation ablation are guided by electrophysiology catheters and cardiac mapping systems. Structural heart intervention is increasingly common, featuring transcatheter aortic valve replacement and mitral valve repair. Intravascular imaging with optical coherence tomography and intravascular ultrasound, along with fractional flow reserve assessment, optimizes outcomes.

- Innovations such as intravascular lithotripsy, left atrial appendage closure, and thrombectomy devices are gaining traction. For advanced heart failure, ventricular assist device support, cardiac contractility modulation, and extracorporeal membrane oxygenation are pivotal.

- The integration of remote patient monitoring through wearable ECG monitors and the pulmonary artery pressure sensor is a strategic boardroom focus, as efficient use of vascular closure devices improves throughput by 15%.

What are the Key Data Covered in this Cardiovascular Medical Devices Market Research and Growth Report?

-

What is the expected growth of the Cardiovascular Medical Devices Market between 2026 and 2030?

-

USD 24.31 billion, at a CAGR of 7.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Diagnostic systems, and Surgical devices), Disease Type (Coronary artery disease, Arrhythmia, Heart failure, Structural heart disease, and Others), End-user (Hospitals, ASCs, Specialty clinics, Home healthcare settings, and Rehabilitation centers) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing adoption of minimally invasive and transcatheter procedures, Stringent regulatory frameworks and prolonged clinical approval cycles

-

-

Who are the major players in the Cardiovascular Medical Devices Market?

-

Argon Medical Devices Inc., B.Braun SE, Boston Scientific Corp., Canon Inc., Cardinal Health Inc., Cook Group Inc., Edwards Lifesciences Corp., Eurocor Tech GmbH, GE HealthCare Technologies, Getinge AB, Johnson and Johnson Services, Lepu Medical Co. Ltd., LivaNova PLC, Medtronic Plc, Merit Medical Systems Inc., Newtech Medical Devices, Siemens AG, Teleflex Inc., Terumo Corp. and W. L. Gore and Associates

-

Market Research Insights

- The market's momentum is fueled by technological convergence, where digital health integration reshapes care delivery. The adoption of remote cardiac monitoring platforms has been shown to reduce hospital readmission rates for heart failure patients by up to 25%, a compelling factor for providers operating under value-based healthcare models.

- Furthermore, the application of AI in cardiovascular diagnostics is delivering significant clinical gains; some algorithms have improved the accuracy of early arrhythmia detection by over 30% compared to conventional methods. This fusion of advanced hardware, such as next-generation heart valves, with sophisticated software is expanding treatment possibilities.

- As procedures increasingly shift to ambulatory surgery centers, demand grows for devices that facilitate efficiency, while the proliferation of connected technologies heightens the focus on cardiac device cybersecurity to ensure patient safety and data integrity.

We can help! Our analysts can customize this cardiovascular medical devices market research report to meet your requirements.

RIA -

RIA -