Enjoy complimentary customisation on priority with our Enterprise License!

The cellulose fiber market size is forecast to increase by USD 17.62 billion, at a CAGR of 9.55% between 2023 and 2028. The growth rate of the market depends on several factors, including growing demand from the textile industry, environment-friendly properties of cellulose fibers, and increasing adoption of these for vehicle interiors.

Cellulose fibers are natural fibers derived from cellulose, which is a complex carbohydrate found in plants. It is manufactured by dissolving pulp from cellulose-rich plants such as cotton, bamboo, jute, hemp

To Know more about the market report Request Free Sample

The increasing adoption of cellulose fibers for vehicle interiors is a noteworthy catalyst driving the growth of the market. Fiber-reinforced polymeric composites, recognized for their elevated specific strength and modulus compared to metals, have gained widespread use. This surge, propelled by environmental awareness and concerns over petrol resource overuse, has spurred the development of innovative materials known as biocomposites. These composites, comprising a matrix (resin) and a reinforcement of natural fibers, find significant application in the automotive sector, where cellulose fibers are utilized as filler material. This utilization contributes to a substantial reduction in vehicle weight, making them half as heavy as conventional automobiles.

Additionally, cellulose serves as a soft filler for bolster and interior trim pieces in the automotive industry. The escalating demand for cellulose fibers in the automotive sector, coupled with the increasing vehicle sales in emerging economies like China, India, and Japan, is anticipated to drive the market. The market is also witnessing global cellulose expansion, and a positive market forecast indicates a trajectory of substantial production of cellulose fibers contributing to the overall growth in the textile sector. The incorporation of biodegradable materials reflects a positive change in the industry, aligning with the growing emphasis on sustainable practices and the need for more environmentally friendly solutions in apparel and textiles.

Increasing preference for cellulose fiber over petrochemical fibers is an emerging trend shaping market growth. Petrochemical fibers are a type of synthetic fibers made from petroleum. Petroleum fibers are similar to plastic bags and other disposable plastics; thus, they are non-biodegradable. They end up in landfills and oceans. Petroleum-derived fibers include polyester, acrylic, nylon, and spandex. Additionally, these are often hypoallergenic and less likely to cause skin irritation or allergic reaction as compared to clothes made of petrochemical fibers, making them the preferable choice for sensitive skin. These are softer, more natural, and aesthetic compared to petrochemical fibers, which give a synthetic feel.

Thus, clothing and home textiles are adopting these for their enhanced moisture absorption, thermal regulation and smooth appearance. Therefore, these are being used to replace petrochemical fibers due to their environment-friendly and versatile nature. Sustainable cellulose sources, such as bacterial nanocellulose, will witness high growth in the textile industry due to their environment-friendly nature. Thus, the market will witness growth during the forecast period.

Increasing labor costs and shortage of labors is a significant challenges hindering market growth. The labor-intensive nature of the market, coupled with increasing labor costs and shortage of labor, presents a hindrance to its expansion and scalability. Due to its labor-intensive nature, large-scale production of cellulose thread is hampered, which drives its costs. The production of cellulose yarns needs manpower that is skilled or semi-skilled. With the global shortage of workers with these requisite skills, labor costs have been increasing as it has become more costly to hire people who are qualified or trained to carry out production at industrial sites. Similarly, when businesses, including those involved in such production, engage with unskilled labor, they must train them to carry out activities properly, which drives up labor costs. Some of the other reasons behind increasing labor costs include supply-demand imbalance in industrial labor and government regulations on minimum wages.

For instance, governments across various nations frequently create rules and regulations to establish a minimum wage that businesses must give their employees. It could take the shape of a rise in the base salary or other employee perks and benefits, such as health insurance and others. According to the US Bureau of Labor Statistics, in 2023, wages and salaries increased by 0.9%, while benefit costs increased by 0.7% from September 2023. Therefore, increasing labor costs pose a challenge to vendors operating in the market, which, in turn, may hamper the growth of the market during the forecast period.

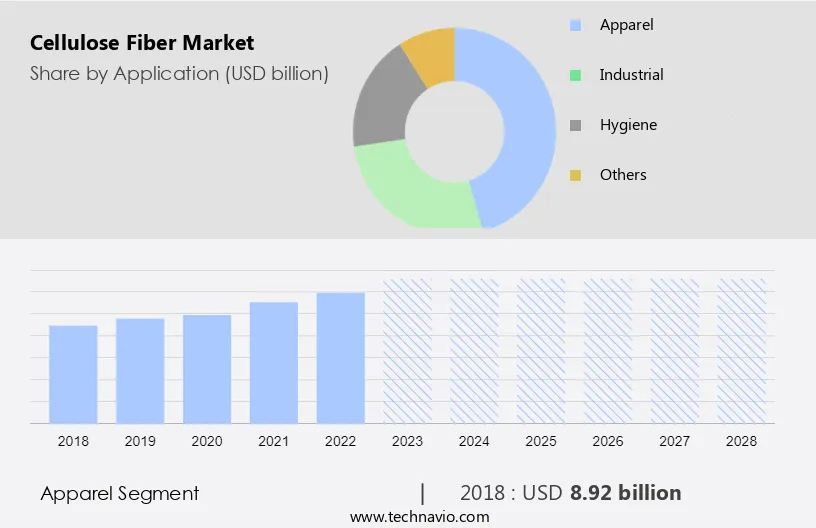

The market share growth by the apparel segment will be significant during the forecast years. Cellulose fibers used in the textile industry are natural (cotton, hemp, and linen) and manufactured (Viscose, rayon, Tencel, lyocell, and model). Cellulose-fiber-based fabrics have special properties, such as moisture-absorbing features. The ability of cellulose fiber to absorb moisture is far better than the conventional cotton quality. Clothes made with cellulose fiber are smooth and soft.

Get a glance at the market contribution of the End User segment Request Free Sample

The apparel segment was the largest and was valued at USD 8.92 billion in 2018. Cellulose fibers are gaining popularity as a sustainable alternative in a variety of textile applications because of their strength and environmental friendliness. They are used to produce strong and light fabrics for clothing, accessories, home decor, and even industrial textiles. The textile industry is focusing on a sustainable approach to reduce environmental impact. For example, nanocellulose, which is are innovative technology for the production and processing of cellulose extracted from algae, fungi, invertebrates, and bacteria, has the potential to impact changes in the global cellulose industry and offer an environmentally sustainable alternative to plant-based cellulose materials. Such factors will increase the adoption in the textile industry during the forecast period.

Based on the type, the market has been segmented into synthetic and natural. The synthetic ?segment will account for the largest share of this segment.? The first man-made fibers, which were developed and produced, used polymers of natural origin, more precisely cellulose, which is a raw material available in large quantities in the vegetable world. One of the most common synthetic cellulose fibers is rayon. Plant-based cellulose is eco-friendly and is also used to produce man-made threads. These are processed into pulp and then extruded in the same ways as other synthetic fibers. Originally, these fibers were produced to minimize the use of expensive natural fibers such as cotton and jute. However, today, the majority of manufactured cellulose fibers are engineered specifically to have properties that natural fibers do not possess. The most sought-after properties of synthetic fibers are that they are highly absorbable, washable, soft and smooth, comfortable, and have good drapes. Therefore, the synthetic segment is expected to witness growth in the fiber market during the forecast period.

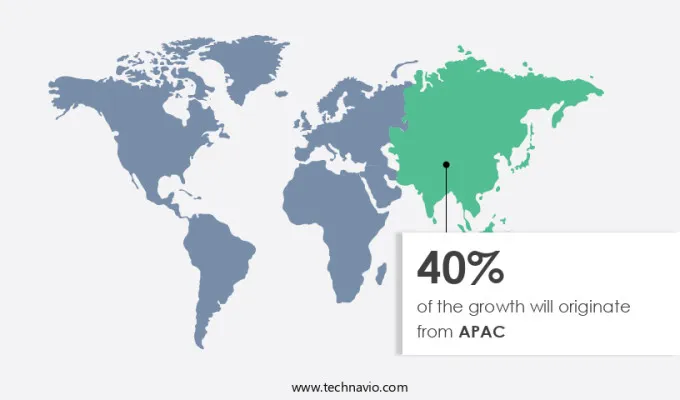

APAC is estimated to contribute 40% to the growth of the global market during the projection period. Technavio's analysts have provided extensive insight into the market forecasting, detailing the regional trends and drivers influencing the market's trajectory throughout the projection period.

For more insights on the market share of various regions Request Free Sample

Further, the market will witness growth during the forecast period due to the growth of the textile industry in the region. APAC has a large presence of textile vendors and a huge consumer base, while raw materials and low-cost labor are easily available. The presence of many textile manufacturers in China, India, Japan, Pakistan, South Korea, and Bangladesh is benefiting the APAC textile industry, given the availability of low-cost labor, a rural population that depends on farming, and favorable climatic conditions. China was the leading textile consumer globally in 2022, as demand for textiles in fashion and household applications was high. Pulp mills make pulp, a mixture of cellulose yarns and water used as the basis of all paper products. China is one of the leading consumers of paper and paperboard containers and packaging in APAC. Increasingly, the adoption of paper packaging alternatives to plastic packaging will increase the demand for paper products in APAC.

Furthermore, countries such as China, India, Japan, South Korea, Australia, and Indonesia are increasingly witnessing growth in their retail and manufacturing sectors. In the retail sector, the aesthetic appeal of the packaging of products attracts more customers. This is creating demand for paper and paperboard containers and packaging with attractive graphics for the products sold through retail stores. Also, the thriving e-commerce market, mainly the business-to-business and business-to-customer segments, is contributing to the growth of the region's paper and paperboard container and packaging market. These factors will drive paper production, thereby increasing the growth of the regional market during the forecast period.

Companies are implementing various market growth and forecasting strategies by analyzing factors such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product or service launches to enhance their presence in the market.

Aditya Birla Management Corp - The company offers cellulose fibers such as Eco-enhanced Viscose called Livaeco and LIVA REVIVA, used for women apparel, men apparel, and textile industries. These products are offered through its subsidiary Birla Cellulose.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including: Aditya Birla Management Corp. Pvt. Ltd., Celanese Corp., Celotech Chemical Co. Ltd., CFF GmbH and Co. KG, Daicel Corp., Eastman Chemical Co., Formosa Plastics Corp., Fulida Group Holding Co. Ltd., Indorama Ventures Public Co. Ltd., International Paper Co., Ioncell Oy, JELU WERK J. Ehrler GmbH and Co. KG, Kelheim Fibers GmbH, Lenzing AG, Maple Biotech Pvt. Ltd., Mitsubishi Chemical Group Corp., Rayonier Advanced Materials, RGE Pte Ltd., Sappi Ltd., and TangShan SanYou Chemical Industries Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market research and growth report predicts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028

The market is witnessing significant growth factors driven by the increasing demand for environmentally friendly and biodegradable products in the textile and garment industries. Petrochemical-sourced fibers, wood pulp, cotton fiber, and flax fiber are key players in this market, along with synthetic or man-made fibers like triacetate and acetate. Factors such as urbanization, consumer purchasing power, and per capita income contribute to the thriving textile and apparel industries. Modal and other eco-friendly products, including those sourced from natural cellulose fibers, find applications not only in the textile and apparel sectors but also in the construction and material industries. The rise in global population and concerns about global temperature alteration amplify the importance of sustainable, climate-friendly fibers like viscose and rayon. These skin-accommodating play a crucial role in addressing environmental pollution and carbon emissions.

Moreover, the market also intersects with the hygiene and industrial industries, particularly in filter chemicals. However, challenges such as volatility in prices, capital intensity, investments in research and development, cotton supply fluctuations, environmental regulations, and the need for competent workers and specialized machinery hinder the market's progress. PURCELL and glass-fiber-reinforced polymers showcase advancements, yet the market's trajectory is intricately linked to addressing sustainability and climate change concerns.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.55% |

|

Market Growth 2024-2028 |

USD 17.62 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.92 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 40% |

|

Key countries |

US, Canada, China, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Aditya Birla Management Corp. Pvt. Ltd., Celanese Corp., Celotech Chemical Co. Ltd., CFF GmbH and Co. KG, Daicel Corp., Eastman Chemical Co., Formosa Plastics Corp., Fulida Group Holding Co. Ltd., Indorama Ventures Public Co. Ltd., International Paper Co., Ioncell Oy, JELU WERK J. Ehrler GmbH and Co. KG, Kelheim Fibers GmbH, Lenzing AG, Maple Biotech Pvt. Ltd., Mitsubishi Chemical Group Corp., Rayonier Advanced Materials, RGE Pte Ltd., Sappi Ltd., and TangShan SanYou Chemical Industries Co. Ltd. |

|

Market dynamics |

Parent market growth analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.