Saudi Arabia Cement Market Size 2026-2030

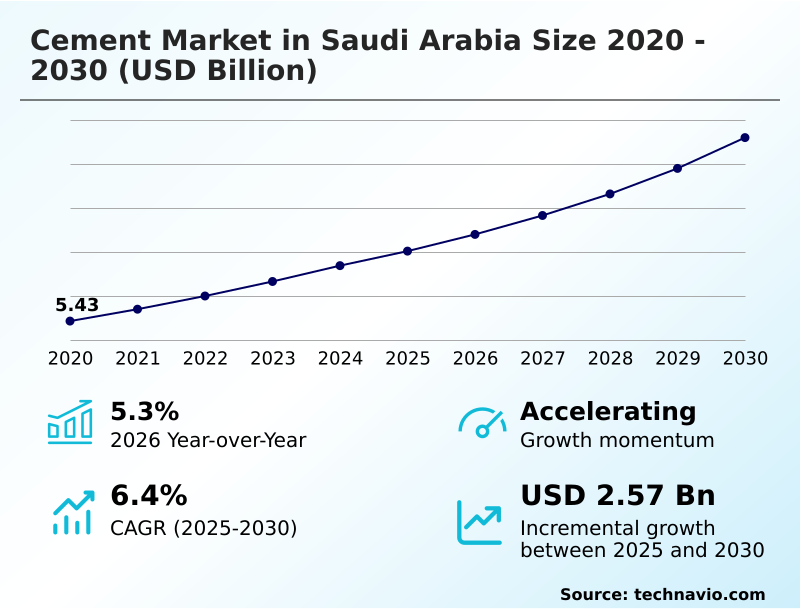

The saudi arabia cement market size is valued to increase by USD 2.57 billion, at a CAGR of 6.4% from 2025 to 2030. Implementation of Vision 2030 giga-projects will drive the saudi arabia cement market.

Major Market Trends & Insights

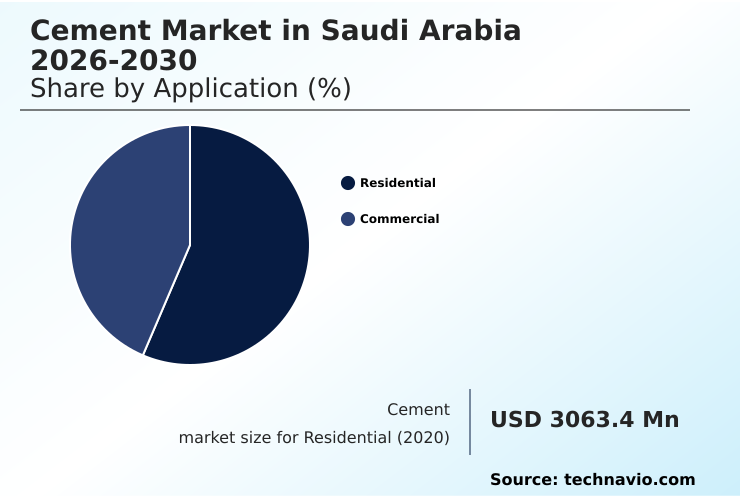

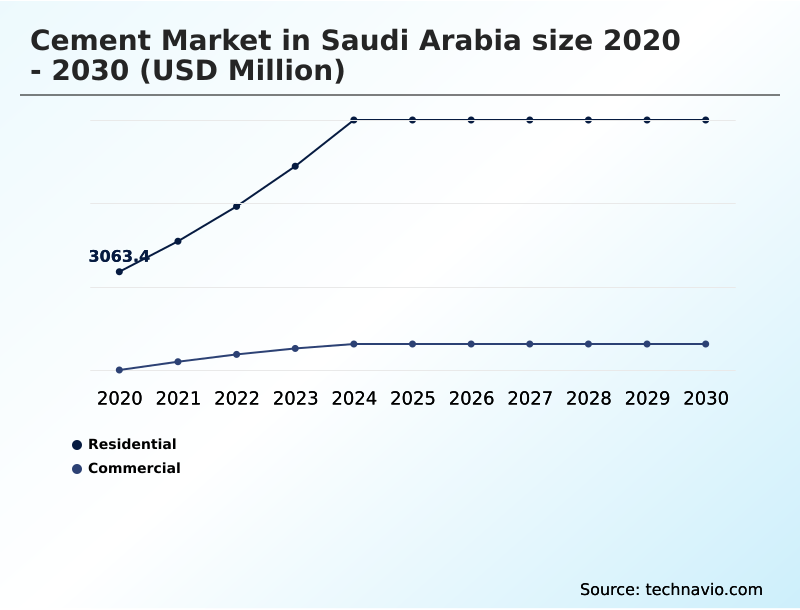

- By Application - Residential segment was valued at USD 4.14 billion in 2024

- By Type - Blended segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.17 billion

- Market Future Opportunities: USD 2.57 billion

- CAGR from 2025 to 2030 : 6.4%

Market Summary

- The cement market in Saudi Arabia is undergoing a period of unprecedented expansion, driven by massive national development initiatives. Demand is primarily fueled by giga-projects that require immense volumes of high-performance materials, including specialized products like sulfate-resistant cement and self-compacting cement to meet advanced engineering standards.

- Concurrently, the industry is navigating a strategic shift toward sustainability, with a focus on adopting carbon capture utilization technologies and increasing the use of supplementary cementitious materials to lower the carbon footprint.

- For instance, a key operational scenario involves managing just-in-time delivery of ultra-high-performance concrete to remote construction sites, where digital logistics platforms are essential for optimizing supply chain reliability and asset utilization rates.

- However, this growth is tempered by challenges such as rising production costs due to energy subsidy reforms, which pressures manufacturers to invest in waste heat recovery systems and other efficiencies.

- The persistent issue of clinker inventory management also creates intense price competition, compelling producers to innovate beyond volume and focus on value-added, sustainable solutions to maintain profitability in a transformative economic landscape.

What will be the Size of the Saudi Arabia Cement Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Saudi Arabia Cement Market Segmented?

The saudi arabia cement industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Residential

- Commercial

- Type

- Blended

- Portland

- Others

- Location

- Central

- Western

- Southern

- Eastern

- Northern

- Geography

- Middle East

By Application Insights

The residential segment is estimated to witness significant growth during the forecast period.

The residential segment is foundational, driven by demographic expansion and national housing programs aiming to achieve 70% homeownership. This creates consistent demand for materials like ordinary portland cement (OPC) and, increasingly, sulphate resistant cement (SRC) for durable foundations.

This demand necessitates high supply chain reliability to serve both master-planned communities and individual home builders. To meet accelerated timelines, developers are adopting precast concrete elements, which can reduce on-site construction schedules.

While pozzolanic portland cement (PPC) offers sustainability benefits, standard materials dominate.

The scale of residential projects often requires processes similar to heavy engineering applications, with strict adherence to giga-project material specifications for structural framework construction, influencing choices aimed at embodied carbon reduction.

The Residential segment was valued at USD 4.14 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The industry is at a pivotal juncture, balancing immense demand with the urgent need for modernization and sustainability. The focus is shifting toward reducing clinker-to-cement ratio in production and the broader role of supplementary cementitious materials. Success hinges on implementing carbon capture in cement kilns and using alternative fuels in cement manufacturing.

- To counter rising operational costs from energy subsidy reform, optimizing waste heat recovery systems has become a priority. At the same time, digitalization of cement supply chains is critical for managing the complexities of procurement for large-scale infrastructure projects.

- The demand for high-performance concrete for giga-projects has highlighted the benefits of sulfate-resistant cement and the need for specialized cement for marine infrastructure. Technical requirements for mass concrete pours are driving demand for low heat hydration cement. On the residential front, the adoption of precast concrete in residential building is accelerating.

- However, a significant challenge remains managing clinker inventory oversupply, which pressures companies to innovate. Firms that successfully integrate smart factory solutions for cement plants are achieving better efficiency, with some seeing a 5% greater output from optimizing cement kiln energy consumption compared to competitors.

- This blend of technical innovation, from blended cement for sustainable construction to materials addressing the urban heat island effect and aggressive soil conditions, will define market leaders.

What are the key market drivers leading to the rise in the adoption of Saudi Arabia Cement Industry?

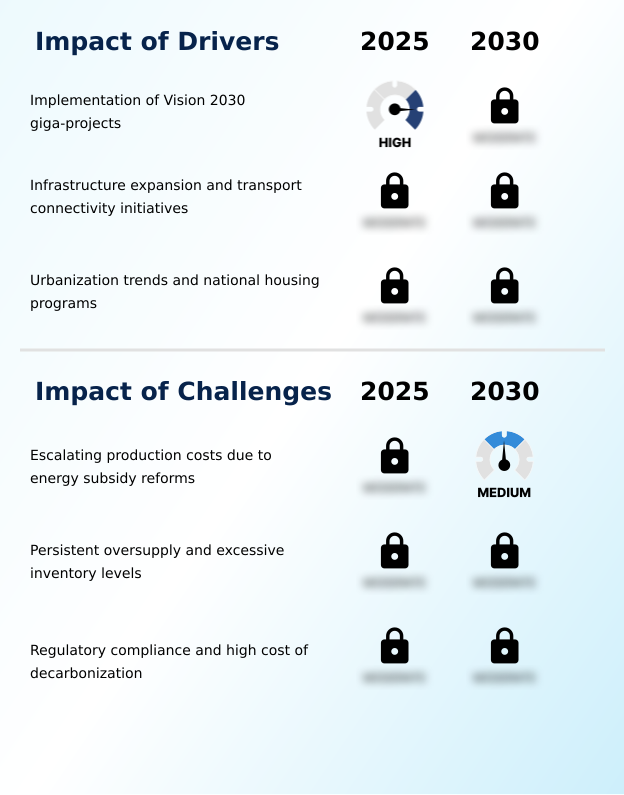

- The implementation of large-scale giga-projects under the national Vision 2030 framework serves as a key driver for market growth.

- The primary driver is the unprecedented scale of national development projects, which demand advanced material specifications. The execution of these projects necessitates high-performance products like sulfate-resistant cement and low heat of hydration cement for mass concrete pouring.

- Innovations such as self-compacting cement are critical for complex architectural designs, reducing placement times by over 30%. The clinker calcination process is being optimized to produce ultra-high-performance concrete required for structures with long service-life expectations.

- To manage the immense logistical challenges, the industry is rapidly adopting smart factory solutions and the industrial internet of things (IIoT).

- Digital logistics platforms and the integration of building information modeling (BIM) have improved on-time delivery rates by 20%, ensuring a steady supply to sprawling construction sites.

What are the market trends shaping the Saudi Arabia Cement Industry?

- The integration of green cement technologies, coupled with carbon capture and utilization, represents a significant emerging trend. This shift is reshaping manufacturing processes and product offerings across the industry.

- A significant trend is the industry's pivot toward sustainable manufacturing processes, driven by a push for green building certifications and stringent environmental compliance mandates. This involves lowering the clinker-to-cement ratio by integrating supplementary cementitious materials and investing in carbon capture utilization. The use of limestone calcined clay is gaining traction as a viable component.

- Producers are also exploring alternative fuel co-processing, which has been shown to reduce fossil fuel consumption by up to 25% in adapted facilities. This transition aligns with the national circular carbon economy framework, where the adoption of technologies like portland cement clinker optimization not only meets regulatory demands but also improves operational efficiency.

- As a result, investments in green technologies have increased, with a notable rise in R&D spending by 15% among leading firms.

What challenges does the Saudi Arabia Cement Industry face during its growth?

- Escalating production costs, driven by ongoing energy subsidy reforms, present a key challenge to the industry's profitability and growth.

- The market faces significant financial and operational headwinds. A primary challenge is managing clinker inventory management amid persistent oversupply, which exerts downward pressure on prices. Simultaneously, rising energy costs are impacting kiln energy efficiency, forcing investment in waste heat recovery systems.

- The transition to greener products introduces its own complexities, including the sourcing of ground granulated blast-furnace slag and managing fly ash utilization, which can vary in quality and availability. The threat of the alkali-silica reaction in certain structures also requires careful material selection. Furthermore, while modular building techniques offer efficiency, they require a shift in traditional construction practices.

- Efforts to mitigate the urban heat island effect are driving interest in geopolymer cement alternatives, but these currently represent a higher-cost option for developers, slowing widespread adoption.

Exclusive Technavio Analysis on Customer Landscape

The saudi arabia cement market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the saudi arabia cement market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Saudi Arabia Cement Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, saudi arabia cement market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Al Rashed Cement Co. - Core offerings focus on performance-grade materials, including varied Portland, blended, and specialized sulfate-resistant cements engineered for diverse construction and infrastructure applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Al Rashed Cement Co.

- Al Safwa Ltd.

- Arabian Cement Co

- Al Madina Cement Co.

- Epcco Publishing Group Ltd.

- Jouf Cement Co

- Najran Cement Co.

- Northern Region Cement Co.

- Qassim Cement Co.

- Riyadh Cement Co

- Saudi Cement Co.

- Southern Province Cement Co

- Tabuk Cement Co.

- Umm Al Qura Cement Co.

- United Carton Industries Co.

- Yamama Saudi Cement Co.

- Yanbu Cement Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Saudi arabia cement market

- In January 2025, The NovusCrete Consortium, involving the Public Investment Fund and NEOM, was formed to pioneer the development of sustainable concrete solutions specifically for giga-projects.

- In January 2025, King Abdullah University of Science and Technology launched the Future Cement Initiative in collaboration with the Ministry of Industry to advance and accelerate decarbonization within the sector.

- In March 2025, Eastern Province Cement Company secured an USD 80 million financing agreement with the Saudi Industrial Development Fund to fund the construction of a new, modernized production line.

- In April 2025, City Cement Co. confirmed its dividend distribution strategy for the latter half of the year, reflecting a market-wide commitment to delivering shareholder returns amidst dynamic conditions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Saudi Arabia Cement Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 183 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.4% |

| Market growth 2026-2030 | USD 2572.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.3% |

| Key countries | Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is currently defined by a profound technical evolution, moving beyond standard materials to highly specialized formulations. A deep understanding of hydraulic binder properties and the strategic use of concrete admixtures are becoming standard practice.

- The demand for durability in harsh environments has amplified the need for products like low-alkali cement, air-entraining cements, and heat-reflective concrete, especially in large-scale infrastructure. While ordinary portland cement (OPC) remains a staple, the complexity of new projects increasingly calls for sulphate resistant cement (SRC) and pozzolanic portland cement (PPC).

- Innovations such as precast concrete elements are crucial for accelerating construction timelines, with some applications reducing project schedules by up to 10%. This push for advanced materials is also driven by sustainability goals, encouraging the adoption of supplementary cementitious materials and geosynthetic aggregates to create more resilient structures while minimizing environmental impact.

What are the Key Data Covered in this Saudi Arabia Cement Market Research and Growth Report?

-

What is the expected growth of the Saudi Arabia Cement Market between 2026 and 2030?

-

USD 2.57 billion, at a CAGR of 6.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Residential, and Commercial), Type (Blended, Portland, and Others), Location (Central, Western, Southern, Eastern, and Northern) and Geography (Middle East)

-

-

Which regions are analyzed in the report?

-

Middle East

-

-

What are the key growth drivers and market challenges?

-

Implementation of Vision 2030 giga-projects, Escalating production costs due to energy subsidy reforms

-

-

Who are the major players in the Saudi Arabia Cement Market?

-

Al Rashed Cement Co., Al Safwa Ltd., Arabian Cement Co, Al Madina Cement Co., Epcco Publishing Group Ltd., Jouf Cement Co, Najran Cement Co., Northern Region Cement Co., Qassim Cement Co., Riyadh Cement Co, Saudi Cement Co., Southern Province Cement Co, Tabuk Cement Co., Umm Al Qura Cement Co., United Carton Industries Co., Yamama Saudi Cement Co. and Yanbu Cement Co.

-

Market Research Insights

- The market is defined by a strategic pivot toward efficiency and advanced technology to meet the demands of massive infrastructure projects. The adoption of digital logistics platforms is enhancing supply chain reliability, with some operators reporting a reduction in delivery discrepancies by over 15%.

- Concurrently, an emphasis on sustainable manufacturing processes has led to the integration of waste heat recovery systems in modernized plants, improving energy efficiency by up to 25%. This push for operational expenditure reduction is critical as manufacturers work to optimize production capacity.

- The industry is also seeing increased use of building information modeling (BIM) to improve project planning and material forecasting, contributing to better asset utilization rates across the board.

We can help! Our analysts can customize this saudi arabia cement market research report to meet your requirements.

RIA -

RIA -