Certificate Authority Market Size 2026-2030

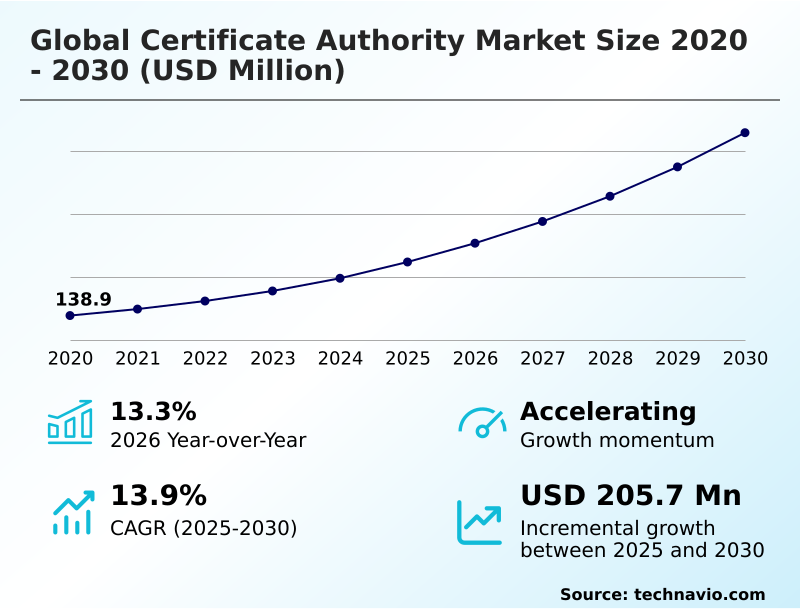

The certificate authority market size is valued to increase by USD 205.7 million, at a CAGR of 13.9% from 2025 to 2030. Escalating sophistication of cyber threats and heightened security awareness will drive the certificate authority market.

Major Market Trends & Insights

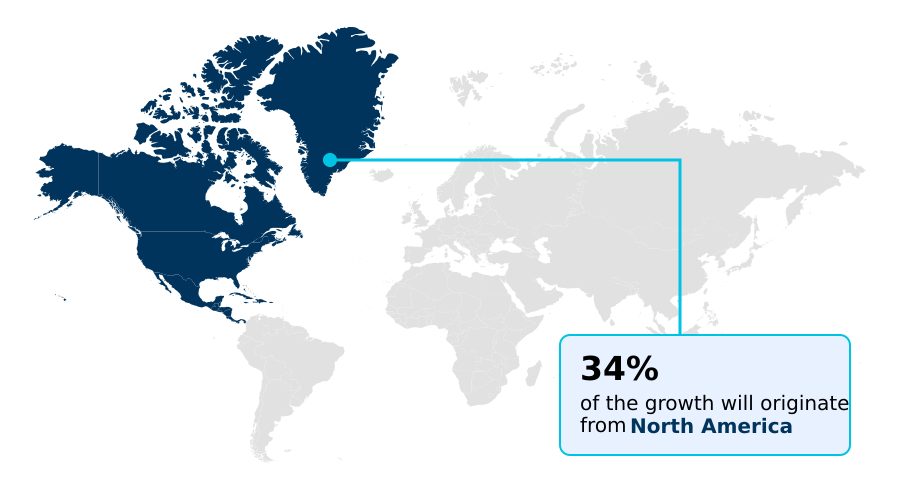

- North America dominated the market and accounted for a 33.6% growth during the forecast period.

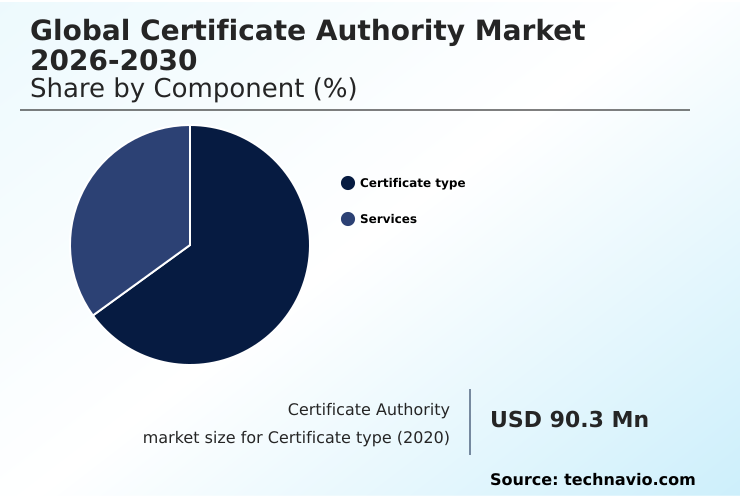

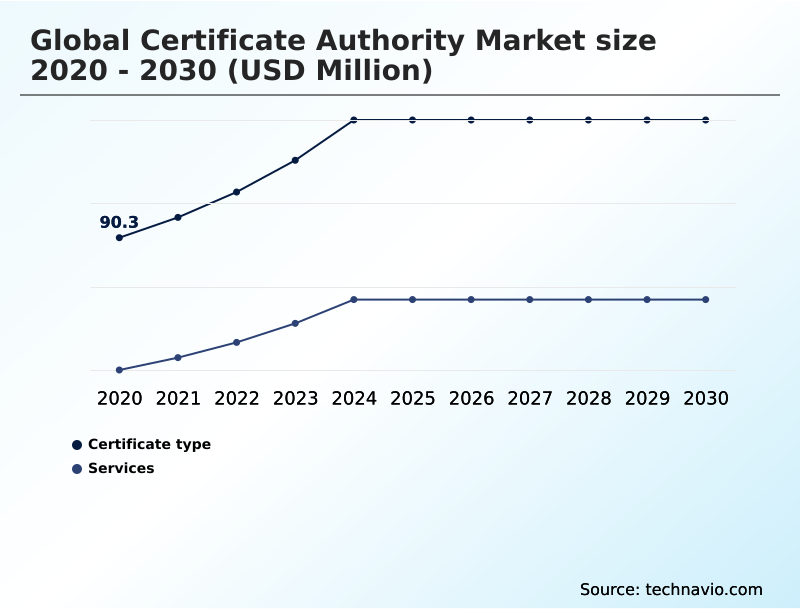

- By Component - Certificate type segment was valued at USD 127.4 million in 2024

- By Organization Size - SMEs segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 290.9 million

- Market Future Opportunities: USD 205.7 million

- CAGR from 2025 to 2030 : 13.9%

Market Summary

- The certificate authority market provides the foundational layer of digital trust essential for the modern economy. Its relevance is amplified by the unrelenting pace of digital transformation, which expands the attack surface for cyber threats and necessitates robust encryption and verified digital identities.

- Key drivers include the exponential growth of the Internet of Things (IoT), where each device requires a unique identity, and stringent regulatory mandates for data protection. A dominant trend is the industry-wide push toward shorter certificate lifecycles, which, while enhancing security, compels the adoption of automated certificate lifecycle management (clm) to handle the increased operational complexity.

- For instance, in a complex software supply chain, a reliance on automated code signing certificates is critical to ensure the integrity of continuous software updates, a process that would be untenable with manual intervention.

- This imperative for automation, coupled with the strategic preparation for post-quantum cryptography, is reshaping the competitive landscape, moving the focus from selling individual certificates to delivering comprehensive, scalable trust management platforms.

What will be the Size of the Certificate Authority Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Certificate Authority Market Segmented?

The certificate authority industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Certificate type

- Services

- Organization size

- SMEs

- Large enterprises

- Type

- Domain validation

- Organization validation

- Extended validation

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The certificate type segment is estimated to witness significant growth during the forecast period.

The certificate authority market is segmented by certificate type, differentiated by the level of identity validation and intended use case.

This ranges from domain validation (dv) certificates, which provide basic encryption, to organization validation (ov) certificates that confirm a business's legal identity. At the highest tier, extended validation (ev) certificates require rigorous vetting, offering maximum assurance.

Beyond website security, the market includes critical products for securing software supply chains and enabling digital identity frameworks.

For example, the mandate requiring private keys for all new code signing certificates to be stored on hardware-compliant tokens enhances key security by over 99% compared to software-based storage.

This evolution underscores a market shifting from simple encryption to providing foundational trust for diverse digital interactions, including public key infrastructure (pki) and the transition to post-quantum cryptography.

The Certificate type segment was valued at USD 127.4 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Certificate Authority Market Demand is Rising in North America Get Free Sample

The geographic landscape of the certificate authority market is diverse, with North America representing the largest market opportunity at approximately 34% due to its mature digital economy and high concentration of technology firms.

Europe's market is heavily influenced by stringent regulations like eIDAS and GDPR, which mandate high-assurance identity verification and create a strong demand for qualified trust services.

Meanwhile, the APAC region, accounting for over 28% of market opportunity, is the fastest-growing due to rapid digitalization, mobile-first economies, and evolving data protection legislation.

In South America, government mandates for e-invoicing using digital signatures have created a unique and substantial market foundation; these initiatives have been credited with reducing certain types of tax fraud by up to 15%.

This regional diversity requires providers to tailor their strategies, balancing global trust standards with local regulatory and compliance demands.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the future of web pki and digital trust requires a strategic approach to several converging challenges. Enterprises are grappling with managing certificate sprawl in multi-cloud environments, a complexity that is magnified by the industry-wide impact of shorter certificate lifecycles. This reality makes automating pki for devops environments not just a best practice but an operational necessity.

- Firms with mature automation strategies report certificate renewal times that are ten times faster than those relying on manual processes, directly impacting operational planning and risk mitigation. The scope of pki is also expanding far beyond websites.

- Securing iot devices with digital certificates is now crucial for industries from manufacturing to healthcare, while specialized use cases like pki for electric vehicle charging infrastructure are creating new ecosystems of trust. Concurrently, the entire industry is focused on transitioning to post-quantum cryptography standards to counter future threats.

- This involves a complex migration away from legacy systems and necessitates a focus on cryptographic agility. Understanding the security of code signing in ci/cd pipelines and managing the certificate management for iot devices are now boardroom-level conversations.

- Enterprises must address certificate discovery in hybrid clouds and implement robust certificate revocation policies to maintain a secure and resilient posture against advanced threats.

What are the key market drivers leading to the rise in the adoption of Certificate Authority Industry?

- The escalating sophistication of cyber threats, coupled with heightened security awareness among enterprises and consumers, serves as a primary driver for the market.

- The market is propelled by the escalating sophistication of cyber threats and stringent regulatory mandates.

- High-profile incidents like the moveit software vulnerability, which affected over 2,000 organizations, serve as stark reminders of the need for authenticated, encrypted communication channels at every data exchange point.

- This hostile environment has elevated cybersecurity to a boardroom priority, driving sustained demand for transport layer security (tls) certificates as a foundational element of digital trust.

- Furthermore, regulations like the gdpr in Europe and hipaa in the US, along with the sec's new cybersecurity disclosure rules, compel organizations to adopt strong encryption and authentication.

- This compliance pressure directly fuels investment in public key infrastructure (pki) and high-assurance certificates, as failure to comply can result in severe financial penalties and reputational damage.

What are the market trends shaping the Certificate Authority Industry?

- A defining market trend is the acceleration of certificate lifecycles toward shorter validity periods. This shift creates a compelling imperative for enterprises to adopt automated management solutions.

- A transformative trend in the certificate authority market is the proactive industry-wide mobilization toward post-quantum cryptography (pqc). Driven by the threat from quantum computers, this shift is compelling organizations to adopt crypto-agility and plan for a complex, multi-year migration. This transition creates new revenue streams from specialized pqc certificates and advanced certificate lifecycle management (clm) tools.

- Simultaneously, the diversification of use cases beyond traditional ssl/tls for websites is accelerating. The proliferation of iot devices, the need for secure software supply chains with robust code signing practices, and the development of digital identity frameworks like the eu's eidas 2.0 are creating massive new markets.

- For instance, the matter smart home standard mandates a unique device attestation certificate for 100% of compliant products, creating predictable, high-volume demand.

What challenges does the Certificate Authority Industry face during its growth?

- The increasing complexity of certificate lifecycle management (CLM) across hybrid and multi-cloud environments presents a significant challenge to the industry.

- A formidable challenge is the increasing complexity of certificate lifecycle management (clm) as enterprises navigate hybrid, multi-cloud environments. The proliferation of certificates for web servers, apis, and iot devices leads to 'certificate sprawl,' a critical visibility gap that increases risk. Manual management is untenable, leading to service outages in over 50% of large enterprises annually.

- This complexity is intensified by the commoditization of domain validation (dv) certificates, driven by free providers like lets encrypt, which now account for over 70% of active web certificates.

- This forces commercial certificate authorities to differentiate through high-assurance certificates like organization validation (ov) and extended validation (ev) and by offering comprehensive, enterprise-grade trust management platforms that provide robust automation and solve the critical pain point of certificate sprawl.

Exclusive Technavio Analysis on Customer Landscape

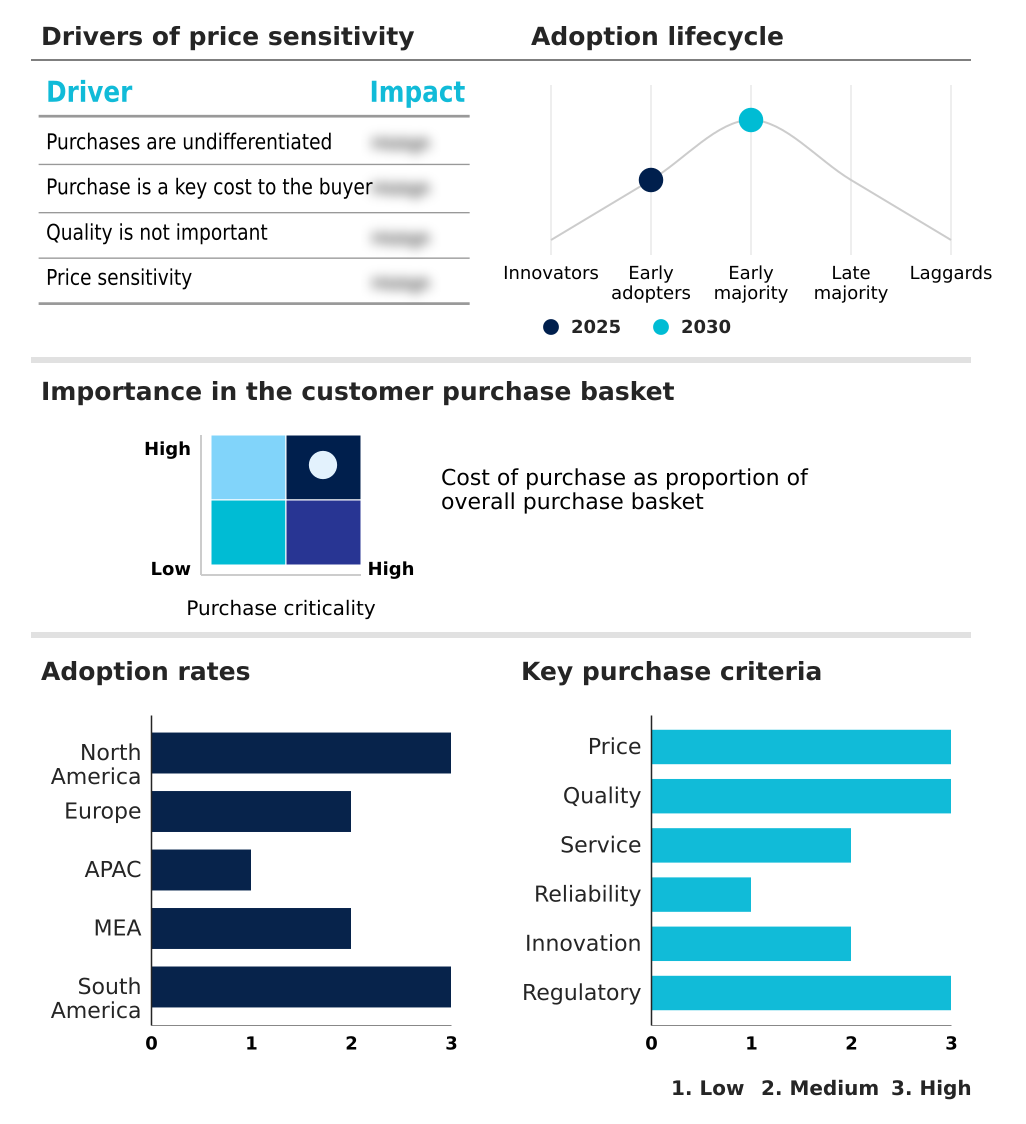

The certificate authority market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the certificate authority market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Certificate Authority Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, certificate authority market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AC Camerfirma SA - Provides digital certificates and legally compliant electronic signature solutions, enabling secure commercial and administrative transactions for businesses and public entities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AC Camerfirma SA

- Alphabet Inc.

- Amazon Web Services Inc.

- Aruba Spa

- Buypass AS

- Cloudflare Inc.

- DigiCert Inc.

- D-Trust GmbH

- Entrust Corp.

- E-Tugra

- GlobalSign Ltd.

- GoDaddy Inc.

- IdenTrust Inc.

- Microsoft Corp.

- Sectigo Ltd.

- SSL.com

- SwissSign AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Certificate authority market

- In August, 2024, the National Institute of Standards and Technology (NIST) finalizes its post-quantum cryptography (PQC) standards, initiating a multi-year migration cycle for enterprises to develop crypto-agility.

- In November, 2024, QuantumSafe Inc. launched its 'Crypto-Agility Suite,' a platform designed to help organizations inventory cryptographic assets and automate the transition to PQC-ready hybrid certificates.

- In February, 2025, AutoTrust Corp. announced a strategic partnership with a global automaker to deploy a large-scale public key infrastructure (PKI) for securing vehicle-to-everything (V2X) communications across its new vehicle lineup.

- In May, 2025, the Connectivity Standards Alliance reported that the Matter smart home standard now requires all certified devices to include a device attestation certificate (DAC), significantly boosting demand for high-volume certificate issuance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Certificate Authority Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13.9% |

| Market growth 2026-2030 | USD 205.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, India, Japan, Australia, South Korea, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The certificate authority market is fundamental to digital trust, moving beyond simple website encryption to enable secure interactions across a vast digital ecosystem. This evolution is driven by the need for robust public key infrastructure (pki) and crypto-agility to address a complex threat landscape.

- The market is defined by various validation levels, from domain validation and organization validation to the high-assurance extended validation, each serving different trust requirements. Key technologies like transport layer security (tls) and its predecessor, secure sockets layer (ssl), are foundational.

- However, the growth is now in advanced use cases such as iot device certificates, secure email (s/mime), and legally binding document signing certificates. The entire ecosystem is preparing for the transition to post-quantum cryptography (pqc). This shift requires a strategic focus on cryptographic agility and a move toward hybrid certificate models.

- A critical boardroom focus is the imperative for automated certificate lifecycle management (clm). Enterprises with centralized clm platforms have demonstrated a 40% improvement in compliance reporting accuracy, a vital metric in an era of stringent regulations and zero trust architecture. This trend underscores the shift from discrete certificate purchases to integrated trust management.

What are the Key Data Covered in this Certificate Authority Market Research and Growth Report?

-

What is the expected growth of the Certificate Authority Market between 2026 and 2030?

-

USD 205.7 million, at a CAGR of 13.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Certificate type, and Services), Organization Size (SMEs, and Large enterprises), Type (Domain validation, Organization validation, and Extended validation) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating sophistication of cyber threats and heightened security awareness, Increasing complexity of certificate lifecycle management (CLM)

-

-

Who are the major players in the Certificate Authority Market?

-

AC Camerfirma SA, Alphabet Inc., Amazon Web Services Inc., Aruba Spa, Buypass AS, Cloudflare Inc., DigiCert Inc., D-Trust GmbH, Entrust Corp., E-Tugra, GlobalSign Ltd., GoDaddy Inc., IdenTrust Inc., Microsoft Corp., Sectigo Ltd., SSL.com and SwissSign AG

-

Market Research Insights

- The certificate authority market is shaped by dynamic security and operational demands. The adoption of automated certificate management is critical, as it can reduce certificate-related service outages by up to 90%, bolstering operational resilience. This shift is driven by the move to shorter lifecycles and the complexity of hybrid cloud deployments.

- The foundational security provided by a secure sockets layer (ssl) is now table stakes, with enterprises focusing on higher-assurance credentials and managing certificate sprawl. Implementing strong authentication methods beyond basic certificates, such as those used in a zero trust model, can decrease the success rate of phishing attacks by over 75%.

- As organizations adopt DevOps, the integration of public key infrastructure into developer workflows is becoming standard, ensuring security is built-in rather than applied as an afterthought, thus improving both security posture and development velocity.

We can help! Our analysts can customize this certificate authority market research report to meet your requirements.

RIA -

RIA -