Chemical Storage Cabinets Market Size 2024-2028

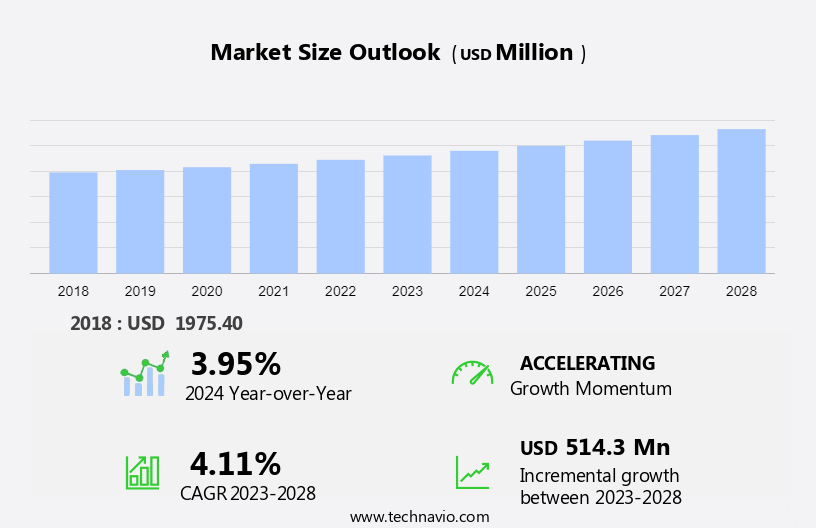

The chemical storage cabinets market size is forecast to increase by USD 514.3 million, at a CAGR of 4.11% between 2023 and 2028. The market's trajectory is influenced by various pivotal factors. Primarily, the manufacturing industries play a crucial role in driving the consumption of specialty chemicals, with diverse sectors relying on these chemicals for their production processes. Furthermore, the rise in international chemical trade facilitates the global distribution and exchange of specialty chemicals, contributing to market expansion. Additionally, the increasing demand for temperature-controlled storage cabinets for chemicals underscores the importance of proper storage and handling in ensuring product quality and safety. As industries prioritize efficiency and compliance with regulatory standards, the market for specialty chemicals continues to grow, driven by the ongoing evolution of manufacturing practices and the dynamic nature of international trade relationships.

What will be the Size of the Market During the Forecast Period?

Market Forecast 2024-2028

To learn more about this report, Request Free Sample

Market Dynamic

The market encompasses a wide range of storage solutions designed for the safe and compliant storage of toxic, corrosive, and hazardous chemicals. These storage cabinets are available in various sizes, including Below 30 gallon, 30-60 gallon, and Above 60 gallon capacities. Workplace safety and regulatory compliance are paramount in industries dealing with such chemicals, making fire resistance, ventilation, spill containment, and accident prevention essential features. Pharmaceuticals, laboratories, manufacturing, and research facilities are significant end-users of chemical storage cabinets. Safety standards mandate advanced technologies such as sensors, monitoring systems, and connectivity features to mitigate risks associated with chemical exposures and ensure employee well-being. Environmental sustainability is also a growing concern, driving the adoption of eco-friendly and energy-efficient storage solutions. The market for chemical storage cabinets is expected to grow significantly due to the increasing demand for safety and compliance in the handling and storage of hazardous chemicals.

Key Market Driver - Manufacturing industries driving the consumption of specialty chemicals

Specialty chemicals are used in various industrial applications due to their functions and performance. The addition or use of these chemicals imparts performance benefits and functionality to the final product. Specialty chemicals are manufactured in small quantities and used to make personal care products and cosmetics, water chemicals, organic chemicals, polymers, plastic additives, dyes, pigments, foods, construction products, electronics, and surfactants.

Moreover, warehousing and storage are important aspects of the specialty chemicals supply chain. It is critical that specialty chemicals are safely stored before being shipped to the end-user or the next stage of the supply chain. Therefore, the rising demand for specialty chemicals from the processing industry and their increasing distribution are expected to boost the demand for chemical storage cabinets, further driving the growth of the market during the forecast period.

Significant Market Trends - Increasing use of flame retardants in end-user industries

Flame retardants are chemicals added to combustible materials to prevent ignition or to slow or retard combustion. Bromine, chlorine, phosphorus, aluminum, magnesium, and boron are most commonly used in the production of flame retardants used in the production of epoxy resins, paints and coatings, polyolefins, unsaturated polyesters, and polyvinyl chloride (PVC). Chemicals, and others.

Moreover, there are different types of brominated flame retardants (BFRs), including polybrominated biphenyls (PBBs), polybrominated diphenyl ethers (PBDEs), octabromodiphenyl ether, decabromodiphenyl ether, and pentabromodiphenyl ether. BFRs are used in the production of polystyrene foams, plastics, and polymers. Thus, the growth in the polymer industry is expected to increase the consumption of BFRs, resulting in increased demand for flame retardant chemicals during the forecast period.

Major Market Challenge - Stringent regulations associated with chemical storage cabinets

Various Regulations for Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) and Classification, Labeling, and Packaging (CLP) as well as stringent regulations of the Environmental Protection Agency (EPA) and the Biocidal Products Directive (BPD) will decline the production of specialty chemicals. For this reason, the manufacture of chemical storage cabinets requires a high degree of precision.

Moreover, storage cabinet facilities must maintain Material Safety Data Sheets (MSDSs) for all chemicals regulated under the Occupational Safety and Health Administration (OSHA) and Hazard Communication Standards (HCS) (29 CFR 1910.1200). The Safety Data Sheet should include the chemical name, physical and chemical properties of the chemical, associated health hazards, routes of entry, exposure limits, and other information. Hence, the market operates under a highly strict regulatory environment, which is expected to impede the growth of the market during the forecast period.

Market Segmentation

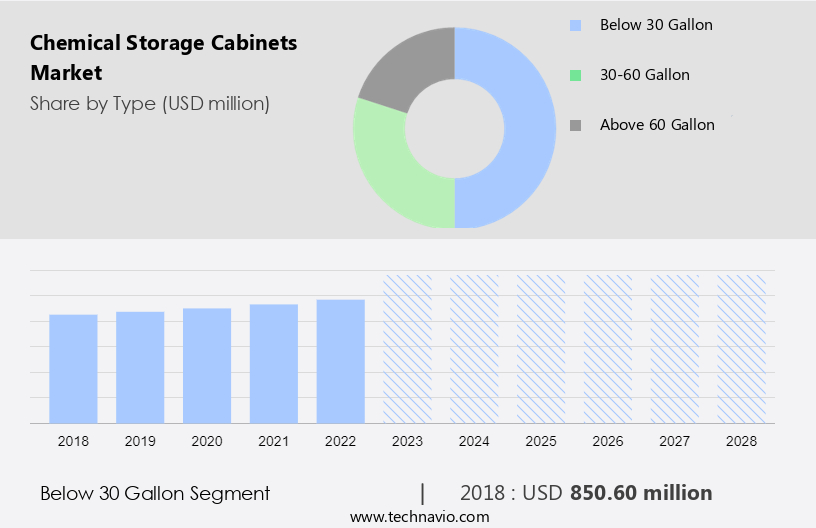

The below 30-gallon segment will account for a major share of the market's growth during the forecast period. Safety cabinets with a capacity of less than 30 gallons are the most viable option for storing a wide variety of chemicals such as flammable and non-flammable. These cabinets are designed to store small amounts of chemicals for easy maintenance. Most laboratories and research centers require small amounts of chemicals. Therefore, cabinets with a capacity of less than 30 gallons have separate cabinets inside to properly store all kinds of chemicals.

Get a Customised Report as per your requirements for FREE!

The below 30-gallon segment was valued at USD 850.60 million in 2018. These cabinets are fitted with secure locking mechanisms to limit access to authorized personnel and these chemicals are properly labeled with warning labels. Also, safety cabinets with a capacity of less than 30 gallons are easy to maintain. However, handling these chemicals requires regular supervision and trained workers. Therefore, safety cabinets with a capacity of less than 30 gallons are expected to grow during the forecast period, mainly due to increasing demand from various industries such as chemical, pharmaceutical, and biotechnology due to their safety benefits. Such factors will increase segment growth during the forecast period.

Application Segment Analysis:

Based on application, the market has been segmented into flammable and combustible chemicals, toxic chemicals, corrosive chemicals, and others. The flammable and combustible chemical segment will account for the largest share of this segment. Flammable and combustible chemicals ignite very easily and burn quickly. Flammable and combustible chemicals are stored in special cabinets to protect workers from exposure to these dangerous chemicals. In addition, these cabinets are well-ventilated and protected from direct sunlight, ignition sources, and heat storage. Flammable and combustible chemicals can decompose or oxidize at some point when exposed to external factors such as air, moisture, and dust particles. Thus, these storage cabinets provide a controlled environment and can also extend the stability and shelf life of these hazardous chemicals. Hence, the flammable and combustible chemicals segment in the market is expected to grow during the forecast period.

Regional Analysis

For more insights on the market share of various regions View PDF Sample now!

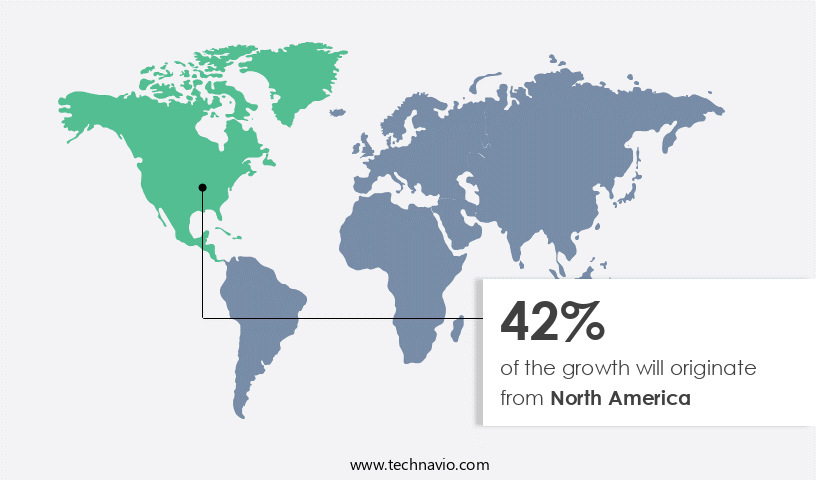

North America is estimated to contribute 42% to the growth by 2028. Technavio’s analysts have elaborately explained the regional market trends, drivers, and challenges that are expected to shape the market during the forecast period. The significant growth of the chemical industry in the region and the growing demand for specialty chemicals in various end-use industries in countries such as the US, Canada, and Mexico are some of the major factors driving the growth of the market in the region. In North America, the demand for chemical cabinets mainly comes from the US. However, there is moderate demand for chemical cabinets in Canada and Mexico.

Moreover, the increasing demand for specialty chemicals in the US, especially from the construction and agricultural industries, is driving the growth of the chemical storage cabinet market in the region. Specialty chemicals are widely used in coatings, adhesives, sealants, and elastomers. The chemical storage cabinet market is undergoing a transformation as chemical manufacturers switch to shale gas for heat and power generation. Growing demand for specialty chemicals from end-use industries such as automotive is expected to drive the growth of the chemical storage cabinet market in the region during the forecast period.

Who are the Major Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AltMet Pty Ltd.: The company offers chemical storage cabinets such as industrial and small safety cabinets, intelligent safety cabinets and big-sized outdoor chemical storage cabinets.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including asecos GmbH, DENIOS SE, Ecolab Inc., ECOSAFE SA, Fami S.r.l., Justrite Mfg. Co. LLC, Kewaunee Scientific Corp., LabGuard India Pvt. Ltd, Merck KGaA, Safety Storage Systems Ltd., Shanghai SYSBEL Industry and Technology Co. Ltd., Spectrum Laboratory Products Inc., Stericox India Pvt. Ltd., SYSPAL Ltd., and Alfa Chemistry

Technavio's market growth and forecasting report provides an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies into categories based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

Segment Overview

The market research and growth report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD million" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments.

- Type Outlook

- Below 30 gallon

- 30-60 gallon

- Above 60 gallon

- Application Outlook

- Flammable and combustible chemicals

- Toxic chemicals

- Corrosive chemicals

- Others

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also interested in below market reports:

- Cleanroom Storage Cabinet Market Analysis APAC, North America, Europe, South America, Middle East and Africa - US, China, Japan, South Korea, Germany - Size and Forecast

- Chemical Warehousing and Storage Market Analysis APAC, North America, Europe, South America, Middle East and Africa - US, China, Japan, Germany, UK - Size and Forecast

- Industrial Gas Storage Cabinets Market by End-user and Geography - Forecast and Geography

Market Analyst Overview

The market caters to the demand for safe and compliant storage solutions for toxic, corrosive, and hazardous chemicals used in various industries such as pharmaceuticals, laboratories, manufacturing, and research facilities. The market offers a range of storage options, including those below 30 gallons, 30-60 gallons, and above 60 gallons. Safety and compliance are paramount in this market, with features like fire resistance, ventilation, spill containment, and advanced locking systems ensuring risks are minimized. Toxic and corrosive chemicals, including those used in the Petroleum Chemical Industry for dyes and solvents, require specialized storage solutions. Industry 4.0 technologies, such as smart sensors, monitoring systems, and connectivity features, are increasingly being integrated into chemical storage cabinets, providing real-time data on temperature, humidity, and chemical levels for improved operational efficiency.

In addition, fire-resistant materials and advanced safety standards further enhance employee well-being and environmental sustainability. The market is evolving with a focus on high-quality solutions integrating smart technologies for enhanced safety. These cabinets prevent accidents by securely storing chemicals such as dyes and solvents while incorporating integrated ventilation systems to manage fumes effectively. The adoption of smart technologies further enhances monitoring and control, ensuring compliance with safety standards in laboratories and industrial settings. As industries prioritize worker safety and regulatory compliance, these advancements are crucial for mitigating risks associated with chemical handling and storage.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.11% |

|

Market growth 2024-2028 |

USD 514.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.95 |

|

Regional analysis |

North America, Europe, APAC, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 42% |

|

Key countries |

US, Germany, China, UK, and Janpan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Alfa Chemistry, AltMet Pty Ltd., asecos GmbH, DENIOS SE, Ecolab Inc., ECOSAFE SA, Fami S.r.l., Justrite Mfg. Co. LLC, Kewaunee Scientific Corp., LabGuard India Pvt. Ltd, Merck KGaA, Safety Storage Systems Ltd., Shanghai SYSBEL Industry and Technology Co. Ltd., Spectrum Laboratory Products Inc., Stericox India Pvt. Ltd., and SYSPAL Ltd. |

|

Market dynamics |

Parent market analysis, market report , market forecast , Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market between 2024 and 2028

- Precise estimation of the market size and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- A thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -