Cloud Finops Market Size 2026-2030

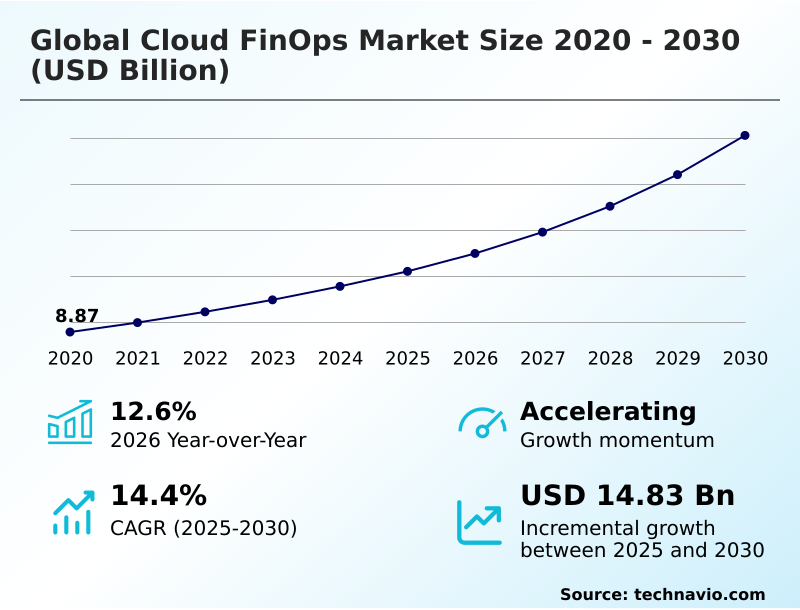

The cloud finops market size is valued to increase by USD 14.83 billion, at a CAGR of 14.4% from 2025 to 2030. Standardization across heterogeneous multi-cloud environments will drive the cloud finops market.

Major Market Trends & Insights

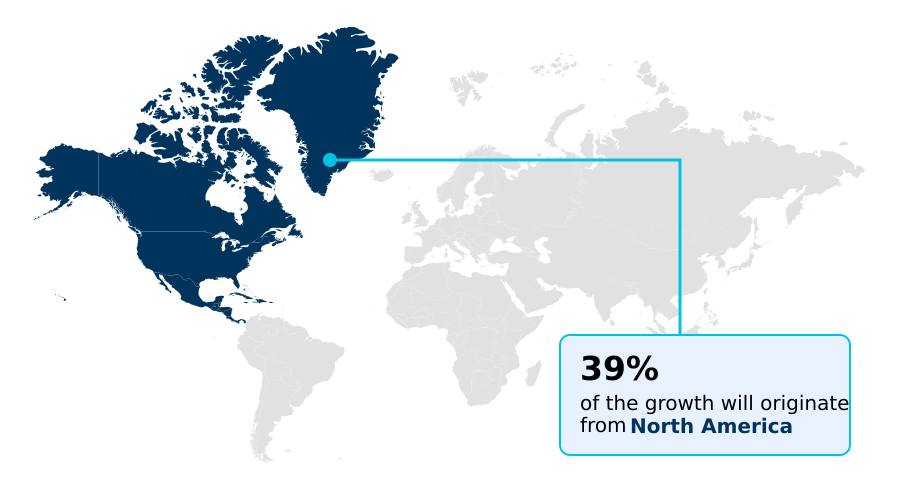

- North America dominated the market and accounted for a 38.9% growth during the forecast period.

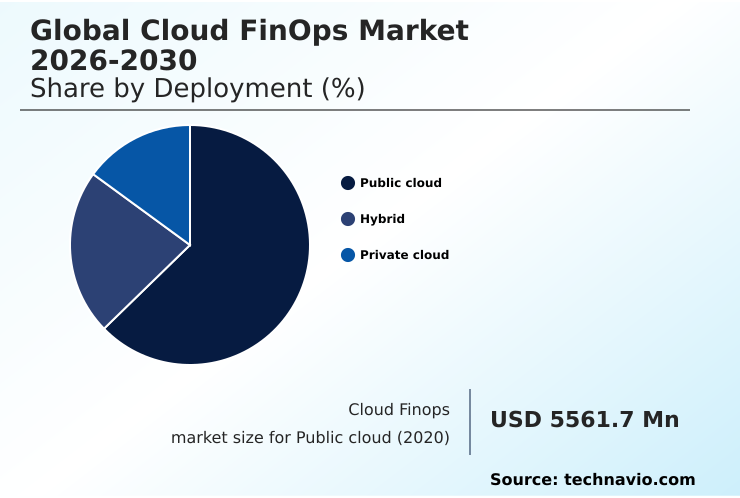

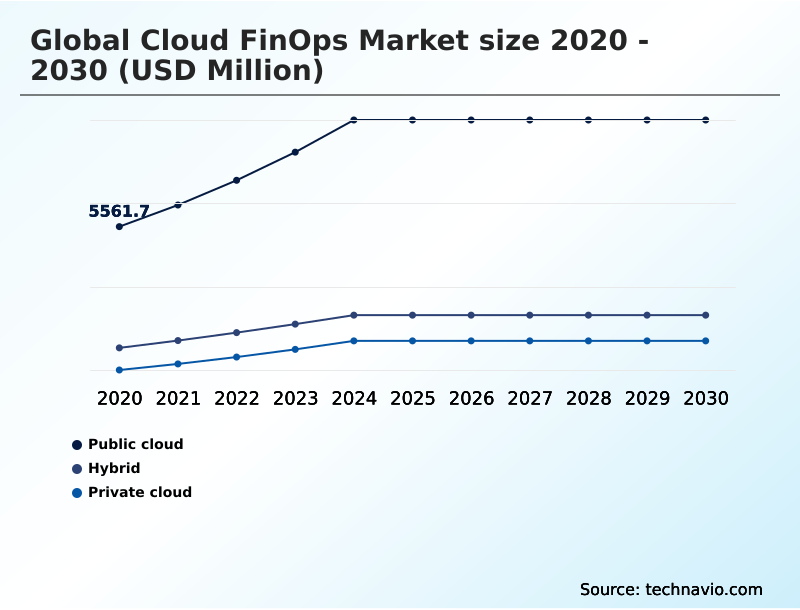

- By Deployment - Public cloud segment was valued at USD 8.71 billion in 2024

- By Application - Cost allocation and chargeback segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 21.45 billion

- Market Future Opportunities: USD 14.83 billion

- CAGR from 2025 to 2030 : 14.4%

Market Summary

- The Cloud FinOps market represents a crucial cultural and strategic evolution, shifting organizational focus from passive cost monitoring to active financial management of cloud resources. This discipline is driven by the need to control the variable spend associated with multi-cloud architectures and the escalating costs of AI workloads.

- Key trends include the integration of autonomous governance through AI, which enables proactive anomaly detection and rightsizing, and the expansion of financial principles to the entire technology stack, including software-as-a-service platforms. For instance, a global retail enterprise can leverage unit economics calculation to determine the precise cloud cost of each online transaction.

- During a peak sales event, this allows the business to make data-driven decisions on resource scaling, ensuring that infrastructure spend remains aligned with revenue growth and profitability targets.

- However, progress is often constrained by internal challenges such as organizational silos between engineering and finance teams and a persistent lack of data standardization, which complicates efforts to achieve a unified view of technology spend. The practice of cloud cost allocation and automated rightsizing are central to overcoming these hurdles.

What will be the Size of the Cloud Finops Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cloud Finops Market Segmented?

The cloud finops industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Public cloud

- Hybrid

- Private cloud

- Application

- Cost management and optimization

- Budgeting and forecasting

- Cost allocation and chargeback

- Reporting and analytics

- Others

- Business segment

- Large enterprises

- Small and medium enterprises

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The public cloud segment is estimated to witness significant growth during the forecast period.

The public cloud segment drives demand for advanced financial governance automation due to its inherently variable and decentralized nature. In these environments, practices focus on optimizing complex pricing models through commitment-based discount optimization and savings plan automation to maximize value.

A robust strategy for cloud cost allocation and resource utilization monitoring is essential for attributing expenses and calculating unit economics. Organizations employing automated rightsizing and real-time spend monitoring have improved budget forecast accuracy by over 20%.

Managing GPU workload costs and data egress cost reduction are also critical.

This proactive approach, involving kubernetes cost management and idle resource termination, transforms the scalability of public cloud infrastructure from a potential liability into a strategic financial asset for modern enterprises.

The Public cloud segment was valued at USD 8.71 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Finops Market Demand is Rising in North America Get Free Sample

The geographic landscape reveals a market maturing at different velocities.

North America leads in sophistication, with organizations focusing on workload placement optimization and deep analytics to measure the business value of cloud investments, improving their infrastructure cost-to-revenue ratio by over 10%.

In Europe, the emphasis on regulatory compliance drives demand for cross-platform cost visibility. The APAC region is the fastest-growing, with enterprises tackling multi-cloud cost normalization and establishing a finops center of excellence to manage rapid scaling.

Across all regions, the goal is to use unit cost for digital products and other metrics to link cloud spend to revenue.

This global trend, supported by a rigorous finops maturity assessment, transforms cloud financial management into a strategic function for governance for decentralized teams and better cloud capacity planning, with some achieving a 20% improvement in resource efficiency.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully navigating the complexities of the modern cloud requires a detailed understanding of the best practices for multi-cloud finops implementation. A primary focus is on how to reduce AWS data transfer costs, as these can quickly accumulate and lead to budget overruns. For other platforms, automating google cloud commitment discount management is crucial for maximizing savings.

- At a more granular level, calculating unit economics for kubernetes applications provides essential visibility into the efficiency of containerized workloads. The true value emerges when integrating finops into the devops lifecycle, creating a culture of cost awareness among engineers. This becomes particularly vital when developing strategies for managing unpredictable ai workload costs, which demand specialized monitoring.

- Implementing chargeback for shared cloud services ensures accountability, while measuring roi of cloud migration projects validates the business case for digital transformation. To achieve this, organizations are building a business case for finops tools and developing a comprehensive cloud cost allocation strategy. This extends to finops for serverless application cost management and even tracking carbon footprint with cloud data.

- Teams that effectively integrate these practices, such as rightsizing workloads without performance impact, resolve deployment-related cost issues nearly twice as fast as those with siloed operations, demonstrating a clear link between operational and fiscal discipline.

What are the key market drivers leading to the rise in the adoption of Cloud Finops Industry?

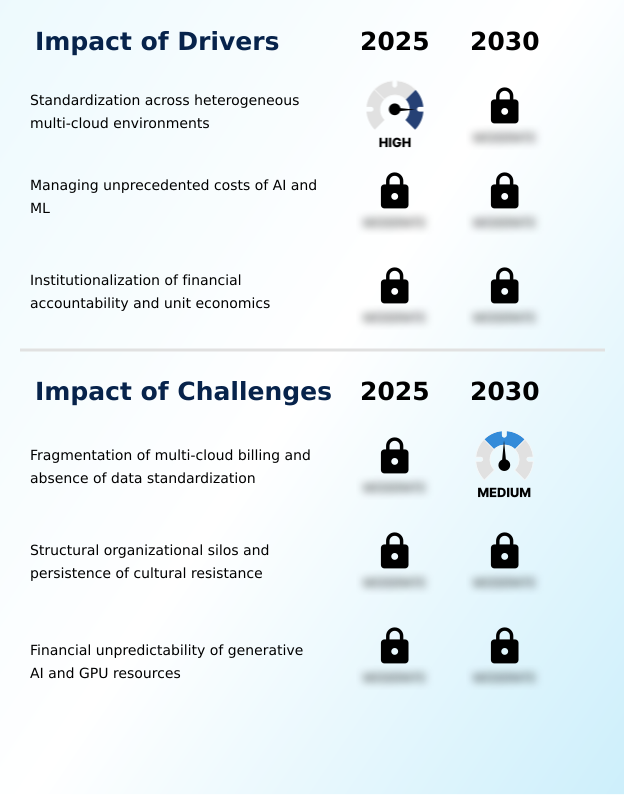

- A key driver for the market is the increasing need for standardization to manage financial data effectively across heterogeneous multi-cloud environments.

- Market growth is fueled by the urgent need for multi-cloud cost normalization and the establishment of clear technology value streams.

- The ongoing finops cultural transformation promotes financial accountability in engineering, a shift that has improved cost efficiency on new projects by up to 20%.

- Unifying multi-cloud billing data is a primary objective, with cloud spend optimization techniques enabling a more accurate cloud TCO calculation across hybrid cloud cost control frameworks.

- As enterprises adopt multi-cloud cost governance, the implementation of automated budget alerting systems becomes essential. This driver is further supported by the availability of finops as a service, which helps organizations without in-house expertise implement effective cloud financial management.

- Standardization initiatives have also been shown to reduce data reconciliation workloads by over 40%, freeing up teams to focus on strategic analysis.

What are the market trends shaping the Cloud Finops Industry?

- The market is witnessing a significant trend toward autonomous financial governance. This shift is primarily driven by the integration of generative artificial intelligence for proactive cost management.

- Key market trends are redefining financial management, with a notable shift toward predictive cloud cost analytics and automating cloud cost remediation. The integration of a greenops framework is gaining traction, with a focus on sustainability reporting integration to align fiscal responsibility with environmental goals; this has helped organizations reduce their carbon footprint by 12%.

- Demand for finops for containerized environments is surging, necessitating advanced tools for container cost optimization. AI/ML cost management is becoming a specialized field, with generative AI cost tracking providing granular visibility into high-spend workloads. Enhanced finops tooling now incorporates sophisticated spend forecasting models, and firms leveraging these tools report a 15% improvement in budget accuracy.

- This evolution enables more strategic cloud financial governance, moving beyond simple cloud waste reduction to proactive resource orchestration.

What challenges does the Cloud Finops Industry face during its growth?

- The fragmentation of billing data across multi-cloud platforms and the absence of data standardization present a key challenge to market growth.

- Significant challenges persist, primarily from the lack of a standardized cloud billing data schema, which complicates shared cost distribution and necessitates complex platform engineering integration. Without a unified schema, organizations spend up to 30% of their FinOps team's time on manual data cleansing, hindering the adoption of cost-aware architecture.

- The financial unpredictability of AI workloads, coupled with immature chargeback for shared services, can lead to budget overruns exceeding 50% on specific projects. Overcoming cultural silos requires more than just tools; it demands a shift toward infrastructure as code for cost and a defined finops lifecycle management process.

- Furthermore, inconsistent tagging and labeling strategy makes effective shared services cost allocation nearly impossible, limiting the effectiveness of cloud cost intelligence and cost optimization automation.

Exclusive Technavio Analysis on Customer Landscape

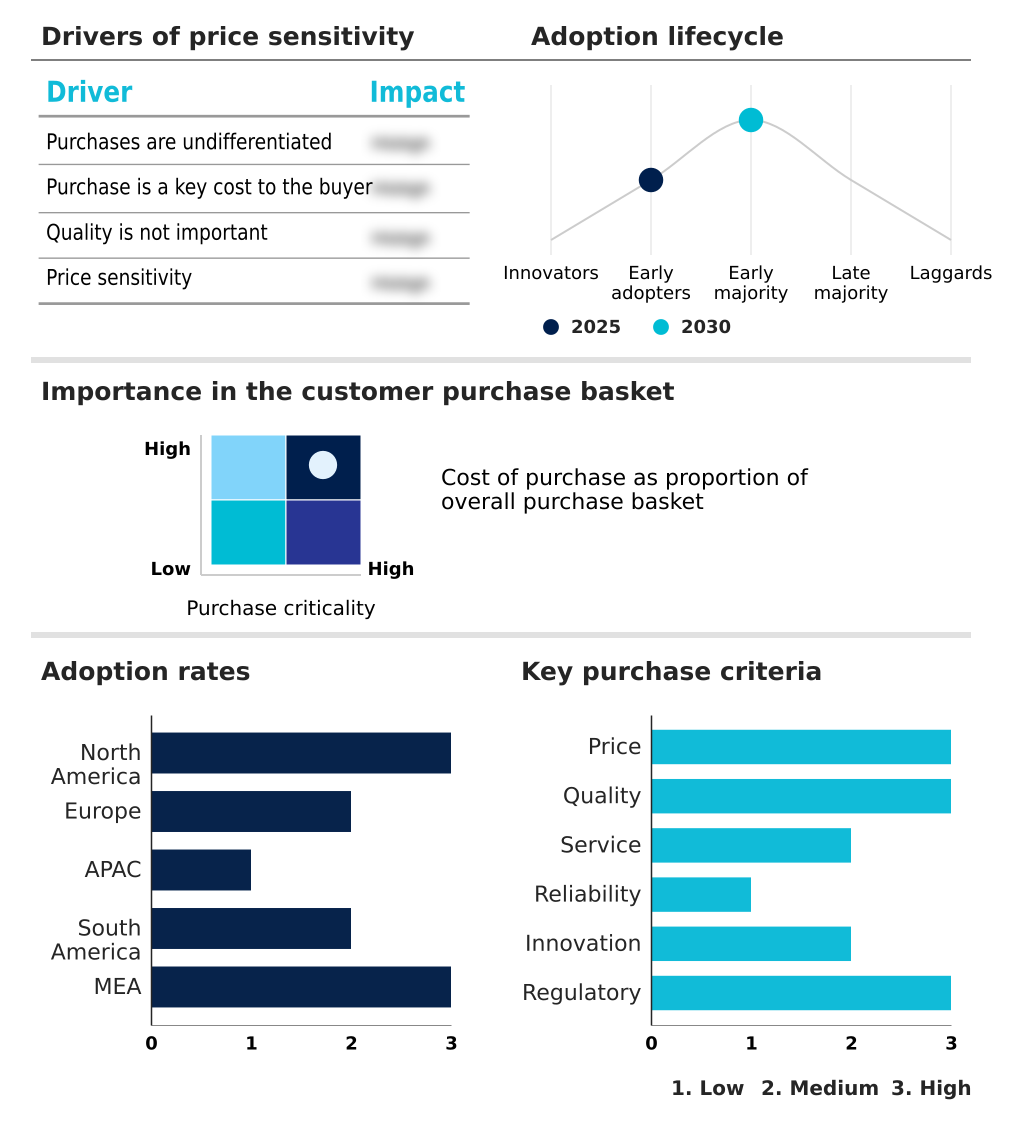

The cloud finops market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud finops market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud Finops Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud finops market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Delivers integrated multi-cloud financial management solutions, leveraging advisory, automation, and managed services to optimize spend and enhance governance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Amazon.com Inc.

- Anodot Ltd.

- Broadcom Inc.

- CAST AI Group Inc.

- CloudZero Inc.

- Datadog Inc.

- DoiT International

- Dynatrace Inc.

- Flexera Software LLC

- Google LLC

- Harness Inc.

- IBM Corp.

- Microsoft Corp.

- NetApp Inc.

- New Relic Inc.

- Nutanix Inc.

- ProsperOps Inc.

- Snowflake Inc.

- Ternary Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud finops market

- In April 2025, the FinOps Foundation released version 1.1 of the FinOps Open Cost and Usage Specification (FOCUS), providing a common schema to normalize cloud billing data across providers.

- In June 2025, IBM announced a significant enhancement to its Turbonomic platform, integrating a generative AI engine to perform autonomous cloud cost remediation and reallocate reserved instances.

- In August 2025, Amazon Web Services introduced specialized cost monitoring and budget alerting features within its management console, designed specifically for generative AI applications to track model training and inference expenses.

- In October 2025, Google Cloud launched significant enhancements to its unified FinOps Hub, which integrated business value metrics directly with infrastructure cost data to provide a clearer view of unit economics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Finops Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.4% |

| Market growth 2026-2030 | USD 14829.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Cloud FinOps market is solidifying its role as a non-negotiable business discipline, moving beyond IT departments to become a central pillar of corporate strategy. The practice centers on creating cost-aware architecture and implementing rigorous financial governance automation. Key mechanisms include cloud cost allocation, unit economics calculation, and kubernetes cost management, which are now standard operating procedures for efficient organizations.

- The evolution is toward proactive and predictive control, using tools for cloud cost anomaly detection and automated rightsizing to prevent budget variances. At the boardroom level, these capabilities directly influence product profitability and strategic planning, as a detailed understanding of technology value streams allows for more accurate financial modeling.

- For instance, enterprises adopting a mature approach with disciplined reserved instance management and savings plan automation have achieved an infrastructure cost-to-revenue ratio improvement of over 10%. This is supported by the finops open cost and usage specification, which facilitates multi-cloud cost normalization and effective shared cost distribution through standardized chargeback and showback models.

- The integration of sustainability reporting integration is also becoming a critical component of this framework.

What are the Key Data Covered in this Cloud Finops Market Research and Growth Report?

-

What is the expected growth of the Cloud Finops Market between 2026 and 2030?

-

USD 14.83 billion, at a CAGR of 14.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Public cloud, Hybrid, and Private cloud), Application (Cost allocation and chargeback, Budgeting and forecasting, Cost allocation and chargeback, Reporting and analytics, and Others), Business Segment (Large enterprises, and Small and medium enterprises) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Standardization across heterogeneous multi-cloud environments, Fragmentation of multi-cloud billing and absence of data standardization

-

-

Who are the major players in the Cloud Finops Market?

-

Accenture Plc, Amazon.com Inc., Anodot Ltd., Broadcom Inc., CAST AI Group Inc., CloudZero Inc., Datadog Inc., DoiT International, Dynatrace Inc., Flexera Software LLC, Google LLC, Harness Inc., IBM Corp., Microsoft Corp., NetApp Inc., New Relic Inc., Nutanix Inc., ProsperOps Inc., Snowflake Inc. and Ternary Inc.

-

Market Research Insights

- The market is undergoing a dynamic shift as organizations move beyond basic reporting to embrace strategic cloud financial planning. This evolution is marked by a focus on cloud spend optimization techniques that create financial accountability in engineering teams, with mature practices reducing misconfigured cloud spend by up to 25%.

- Establishing a finops center of excellence has become a key strategy, enabling governance for decentralized teams and improving budget adherence by over 15%. The core objective is to link cloud spend to revenue, using metrics like unit cost for digital products to measure the business value of cloud investments.

- This data-driven approach ensures that all technology decisions are fiscally sound and aligned with corporate goals, transforming cloud costs from an unpredictable overhead into a managed component of business strategy.

We can help! Our analysts can customize this cloud finops market research report to meet your requirements.

RIA -

RIA -