Cochlear Implants Market Size 2026-2030

The Cochlear Implants Market size was valued at USD 2.02 billion in 2025, growing at a CAGR of 9.4% during the forecast period 2026-2030.

Major Market Trends & Insights

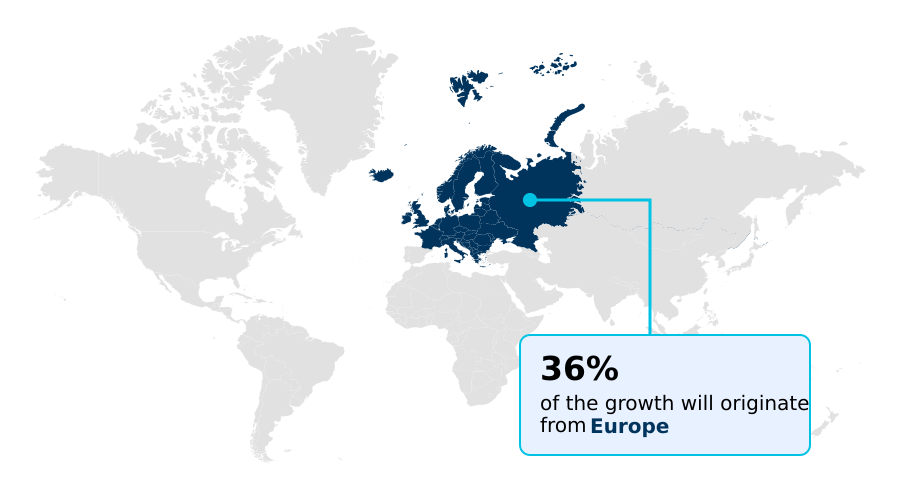

- Europe dominated the market and accounted for a 36.4% growth during the forecast period.

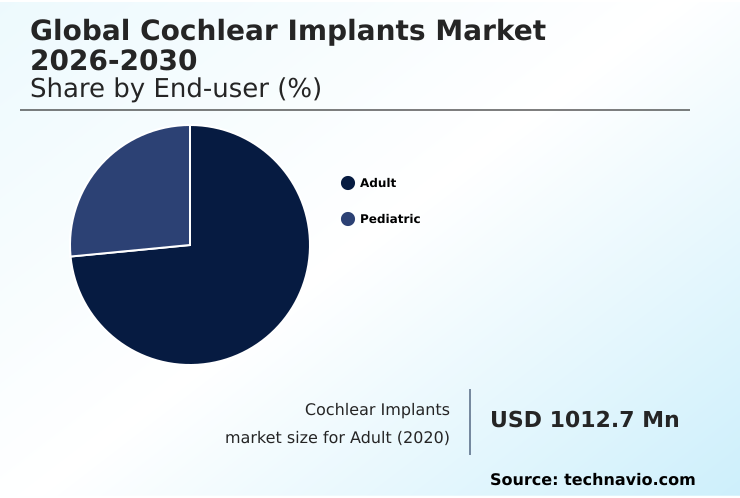

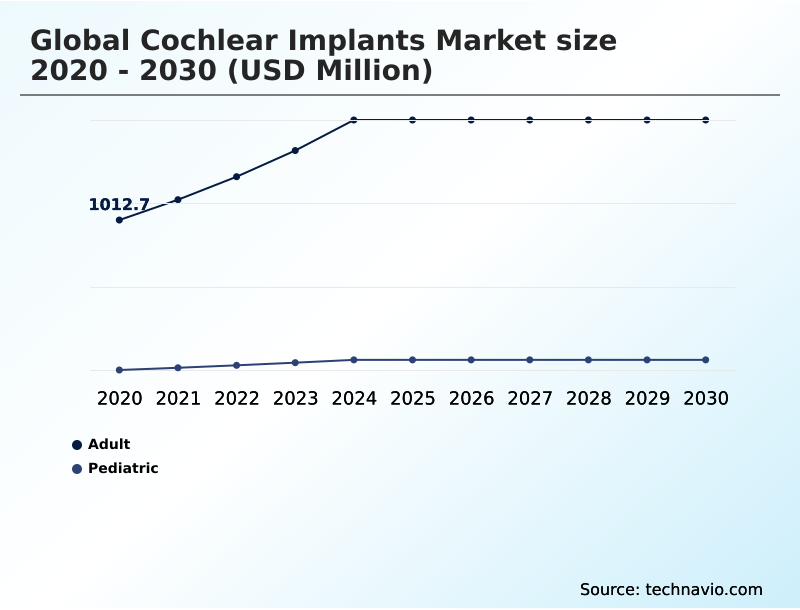

- By End-user - Adult segment was valued at USD 1.44 billion in 2024

- By Product - Unilateral segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 1.78 billion

- Market Future Opportunities 2025-2030: USD 1.14 billion

- CAGR from 2025 to 2030 : 9.4%

Market Summary

- The cochlear implants market is characterized by a strategic focus on technological integration to expand patient access and improve auditory outcomes, with device reliability rates now exceeding 99% over a ten-year period. A key driver is the expansion of clinical candidacy, which has increased the potential patient pool by over 40% in developed markets.

- In a typical business scenario, manufacturers are shifting from one-time hardware sales to service-based models offering remote firmware updates, creating recurring revenue streams. This addresses patient concerns about technological obsolescence. However, this progress is constrained by inconsistent reimbursement frameworks, which can delay patient access to these advanced systems by more than 12 months in some regions.

- This challenge requires manufacturers to navigate complex technology appraisal pathways to prove long-term cost-effectiveness.

What will be the Size of the Cochlear Implants Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cochlear Implants Market Segmented?

The cochlear implants industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Adult

- Pediatric

- Product

- Unilateral

- Bilateral

- Technology

- Conventional cochlear implants

- Hybrid cochlear implants

- Electro-acoustic stimulation

- Fully implantable cochlear implants

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

How is the Cochlear Implants Market Segmented by End-user?

The adult segment is estimated to witness significant growth during the forecast period.

The adult segment, representing over 70% of the cochlear implants market, is strategically shifting from treating only profound deafness to addressing moderate-to-severe hearing loss.

This evolution is driven by advancements in residual hearing preservation, which can improve speech perception in noisy environments by up to 30% compared to traditional approaches.

The focus on bimodal hearing solutions allows for the integration of a cochlear implant with a hearing aid, enhancing sound quality.

Consequently, the emphasis is on electro-acoustic stimulation and personalized sound map optimization to improve auditory outcomes and user autonomy, moving beyond a one-size-fits-all model. This patient-centric approach ensures better adaptation and satisfaction for a broader demographic.

The Adult segment was valued at USD 1.44 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Cochlear Implants market is rising in the leading region?

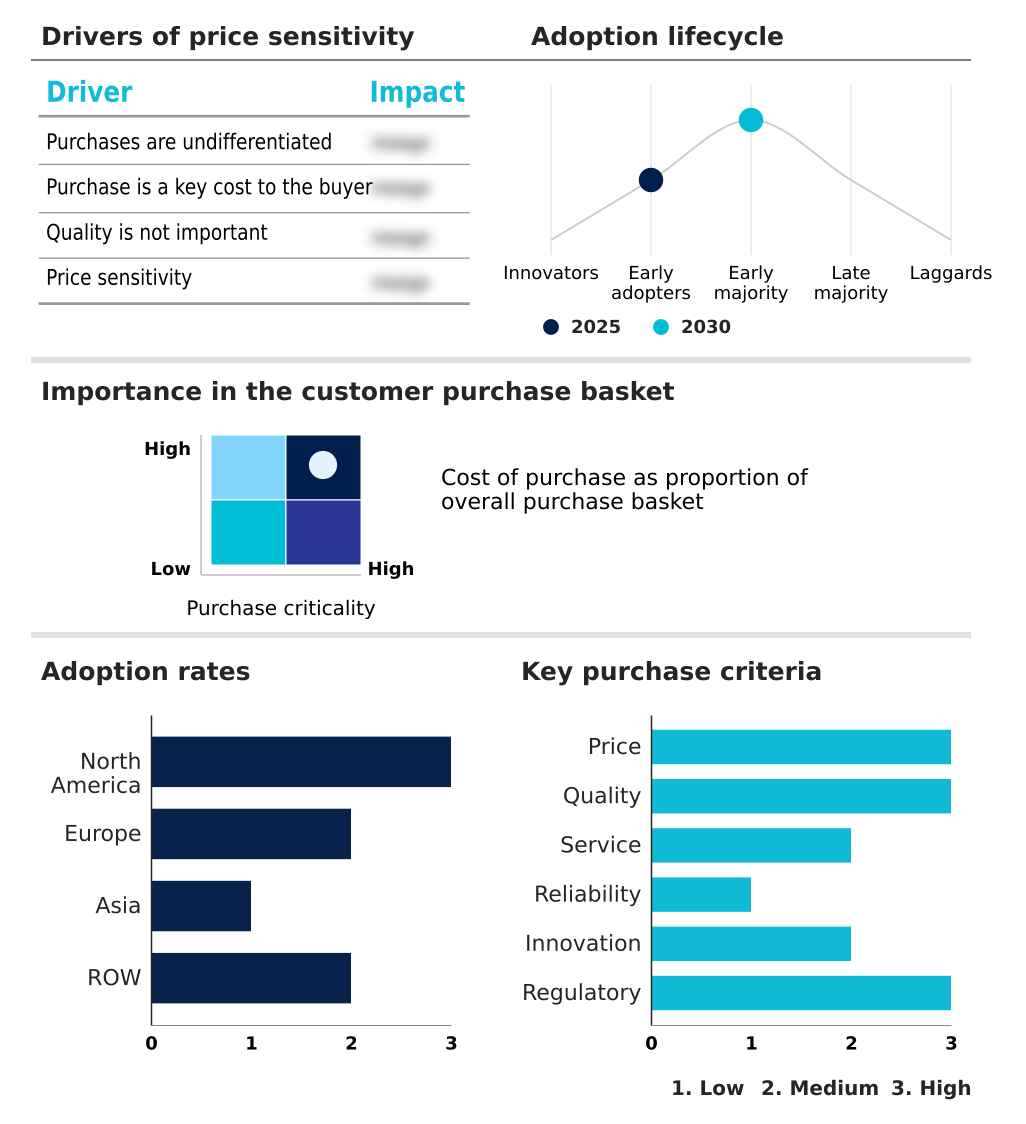

Europe is estimated to contribute 36.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cochlear Implants Market demand is rising in Europe Request Free Sample

The global geographic landscape for cochlear implants is led by Europe, which accounts for approximately 36% of the market's incremental growth, closely followed by North America at 35%.

This dominance is due to established reimbursement frameworks and high bilateral implantation rates in pediatric populations, which are over 30% higher in Europe than in other regions.

Within North America, the US market contributes over 70% of the regional revenue, driven by high healthcare spending and rapid adoption of new technologies.

In contrast, the market in Asia is the fastest-growing but faces challenges in access, with decentralized care models and telehealth platform integration lagging behind Western markets by an estimated two to three years.

This disparity requires companies to adopt regionally tailored strategies for market penetration and patient support, focusing on building clinical infrastructure in emerging economies.

What are the key Drivers, Trends, and Challenges in the Cochlear Implants Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- For many individuals, understanding the total cost of cochlear implant surgery is the first step in their journey toward better hearing. Potential candidates carefully evaluate the cochlear implant benefits for adults, which often include significant improvements in communication, social engagement, and a reduced risk of cognitive decline, weighing these against the financial investment.

- For families, analyzing pediatric cochlear implant outcomes is crucial, as data consistently shows that early intervention leads to superior language and academic development, with implanted children often achieving literacy levels comparable to their hearing peers. A frequent point of confusion is the cochlear implant vs hearing aid comparison; implants are specifically for severe-to-profound loss where aids no longer provide benefit.

- The industry is on the cusp of a major shift with emerging updates on fully implantable cochlear implant availability. This next-generation technology, which eliminates all external hardware, is projected to increase market adoption by over 25% by addressing the aesthetic and lifestyle concerns that currently deter a significant portion of eligible candidates.

What are the key market drivers leading to the rise in the adoption of Cochlear Implants Industry?

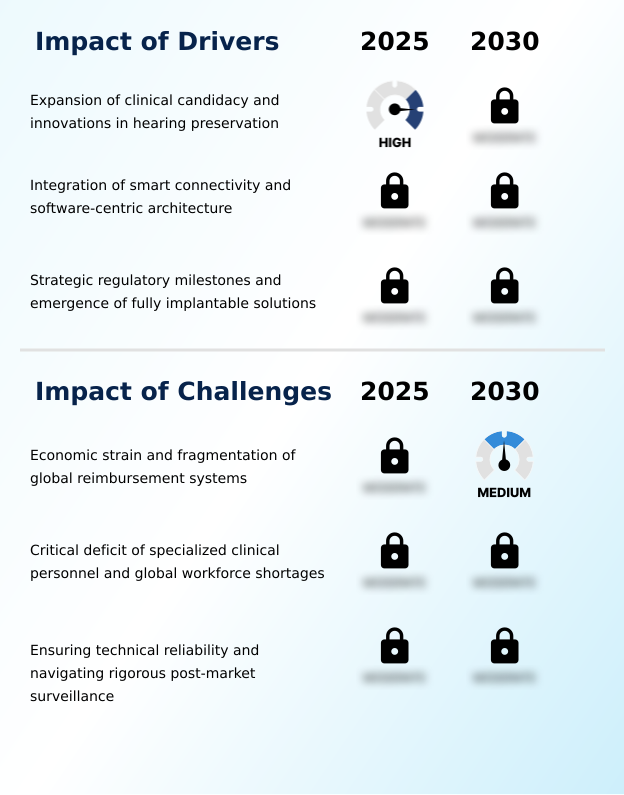

- The expansion of clinical candidacy criteria to include a wider range of hearing loss, coupled with innovations in surgical techniques for hearing preservation, is a primary driver of market growth.

- The expansion of clinical candidacy criteria is a primary market driver, increasing the addressable patient population for cochlear implants by nearly 40% in some regions.

- This shift includes individuals with significant residual hearing, made possible by innovations like atraumatic electrode arrays and surgical robotics integration that minimize intracochlear trauma.

- Such techniques preserve natural hearing, with robotic-assisted procedures reducing surgical force by over 50% compared to manual insertion.

- This driver is amplified by a growing medical consensus on the benefits of earlier prelingual deafness intervention to maximize neurocognitive development and improve long-term auditory rehabilitation outcomes, making implantation a more viable and attractive option for a wider demographic.

What are the market trends shaping the Cochlear Implants Industry?

- A pivotal market trend is the shift toward software-defined hardware and upgradeable smart systems. This approach prioritizes long-term adaptability and future-proofs the technology for recipients, ensuring continuous access to the latest innovations.

- A defining trend in the cochlear implants market is the move toward fully implantable solutions, which addresses significant aesthetic and functional limitations of current devices and is projected to increase user adoption by over 25%. This innovation aims to provide 24-hour hearing without external hardware.

- Simultaneously, the industry is embracing software-defined hardware, where remote firmware updates can enhance performance, improving speech perception in noise by more than 15% without revision surgery. This approach provides lifelong hearing support through patient-centric digital applications and decentralized care models, decoupling technological advancement from the physical implant and increasing the long-term value for recipients.

- These trends reflect a broader shift toward greater user autonomy and seamless integration with a digital lifestyle.

What challenges does the Cochlear Implants Industry face during its growth?

- Economic strain resulting from the high initial cost of care and the fragmentation of global reimbursement systems presents a key challenge to market expansion and equitable patient access.

- Fragmented global reimbursement frameworks remain a significant challenge, creating access disparities where approval times for cochlear implants can vary by over 50% between different healthcare systems. This inconsistency is a major barrier, particularly as the high upfront cost of the technology requires robust funding pathways.

- The issue is compounded by critical clinical workforce shortages, with the demand for specialized audiologists outpacing supply by an estimated 20% in certain developed nations. This personnel gap creates bottlenecks in care delivery, from surgery to the complex sound map optimization required for modern devices.

- Navigating complex technology appraisal pathways further delays the adoption of innovative but higher-cost systems, impeding market growth.

Exclusive Technavio Analysis on Customer Landscape

The cochlear implants market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cochlear implants market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cochlear Implants Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cochlear implants market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Bionics AG - Develops and provides implantable neurostimulation technology focused on restoring hearing for individuals with profound sensorineural hearing loss through cochlear implant systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Bionics AG

- Cochlear Ltd.

- Demant AS

- Ear Technology Corp

- Earlens Corp.

- Envoy Medical Inc.

- Grace Medical Inc.

- MED EL Medical Electronics

- Medtronic Plc

- MicroPort Scientific Corp.

- Nurotron Biotechnology Co. Ltd.

- NYU Langone Health

- Oticon Medical AS

- Phonak ltd.

- Sonova AG

- Starkey Laboratories Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Health Care Equipment industry, the increasing adoption of 3D printing for creating customized medical implants and surgical guides is directly impacting the cochlear implants market, allowing for patient-specific electrode arrays that enhance surgical precision and support intracochlear trauma minimization.

- A broader industry push toward smaller, more compact device form factors is influencing cochlear implant design, driving R&D in miniaturization to reduce the size of external processors and accelerate progress toward fully implantable solutions, which improves user autonomy.

- Stringent regulatory frameworks, such as the Unique Device Identification system, are creating new compliance pressures, forcing cochlear implant manufacturers to invest in robust post-market surveillance and traceability systems, which adds operational costs but improves long-term safety.

- The integration of IoT and digital technologies for connected product ecosystems is reshaping patient care, supporting the development of smart implants with remote clinical management capabilities and enabling sound map optimization through telehealth platforms.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cochlear Implants Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.4% |

| Market growth 2026-2030 | USD 1139.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Sweden, China, Japan, India, South Korea, Singapore, Malaysia, Brazil, Saudi Arabia, South Africa, UAE, Argentina, Egypt, Colombia and Qatar |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cochlear implants market ecosystem operates through a specialized value chain, where less than a dozen key suppliers provide critical components like biocompatible materials and microelectronics to major manufacturers. These manufacturers, who hold over 85% of the market, then assemble and distribute the final devices through hospital networks and specialized audiology clinics.

- Regulatory bodies such as the FDA and EMA impose strict standards, influencing product design and requiring extensive post-market surveillance. The adoption by end-users—both adult and pediatric—is heavily influenced by clinical outcomes, with bilateral implantation demonstrating a 30% improvement in sound localization over unilateral systems.

- Supporting entities, including research universities, drive innovation in areas like surgical robotics integration and sound processing architecture, ensuring continuous technological advancement across the industry.

What are the Key Data Covered in this Cochlear Implants Market Research and Growth Report?

-

What is the expected growth of the Cochlear Implants Market between 2026 and 2030?

-

The Cochlear Implants Market is expected to grow by USD 1.14 billion during 2026-2030, registering a CAGR of 9.4%. Year-over-year growth in 2026 is estimated at 9.1%%. This acceleration is shaped by expansion of clinical candidacy and innovations in hearing preservation, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Adult, and Pediatric), Product (Unilateral, and Bilateral), Technology (Conventional cochlear implants, Hybrid cochlear implants, Electro-acoustic stimulation, and Fully implantable cochlear implants) and Geography (North America, Europe, Asia, Rest of World (ROW)). Among these, the Adult segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, Asia and Rest of World (ROW). Europe is estimated to contribute 36.4% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, Sweden, China, Japan, India, South Korea, Singapore, Malaysia, Brazil, Saudi Arabia, South Africa, UAE, Argentina, Egypt, Colombia and Qatar, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is expansion of clinical candidacy and innovations in hearing preservation, which is accelerating investment and industry demand. The main challenge is economic strain and fragmentation of global reimbursement systems, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Cochlear Implants Market?

-

Key vendors include Advanced Bionics AG, Cochlear Ltd., Demant AS, Ear Technology Corp, Earlens Corp., Envoy Medical Inc., Grace Medical Inc., MED EL Medical Electronics, Medtronic Plc, MicroPort Scientific Corp., Nurotron Biotechnology Co. Ltd., NYU Langone Health, Oticon Medical AS, Phonak ltd., Sonova AG and Starkey Laboratories Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for cochlear implants is concentrated, with the top three vendors commanding over 85% of the global market share. Key players such as Cochlear Ltd. and MED-EL are differentiating through innovation in software-defined hardware and expanded pediatric indications, respectively.

- Recent developments focus on smart systems with upgradeable firmware, a feature now present in over 60% of new premium devices, to provide lifelong hearing support and address concerns about technological obsolescence. These advancements respond to the growing demand for user autonomy and seamless integration with personal electronics.

- A primary industry challenge remains navigating stringent post-market surveillance requirements, which can add significant operational costs and delay the introduction of next-generation devices, forcing companies to balance rapid innovation with rigorous long-term reliability testing.

We can help! Our analysts can customize this cochlear implants market research report to meet your requirements.

RIA -

RIA -