Cold Chain Market Size 2026-2030

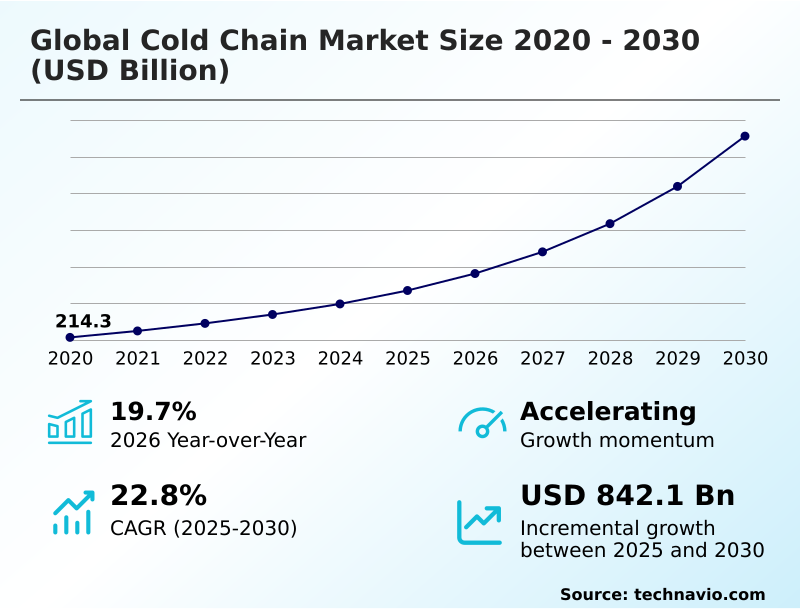

The cold chain market size is valued to increase by USD 842.1 billion, at a CAGR of 22.8% from 2025 to 2030. Rising use of RFID in cold chain logistics will drive the cold chain market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 32.7% growth during the forecast period.

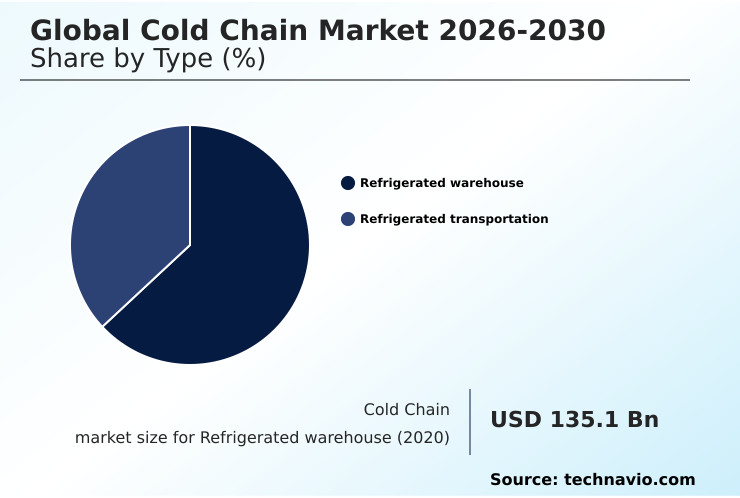

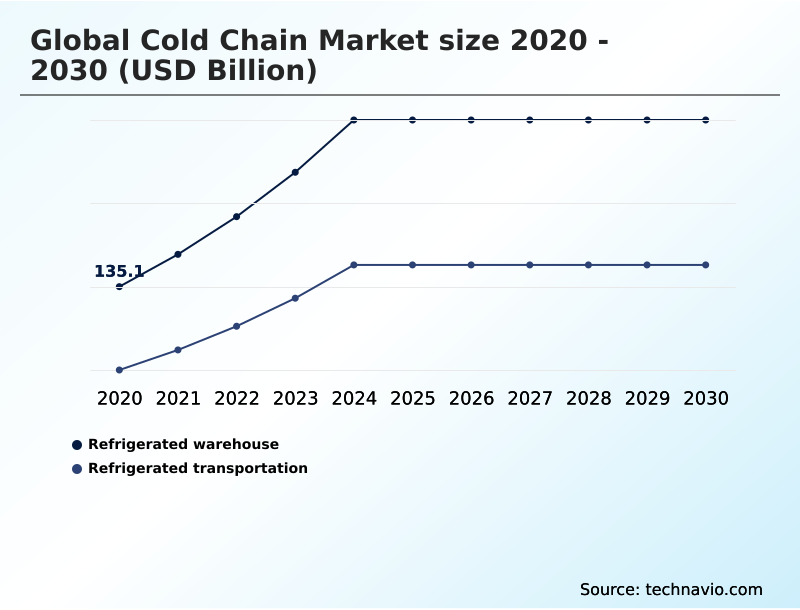

- By Type - Refrigerated warehouse segment was valued at USD 247 billion in 2024

- By Application - Meat fish and seafood segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1097.8 billion

- Market Future Opportunities: USD 842.1 billion

- CAGR from 2025 to 2030 : 22.8%

Market Summary

- The cold chain market is a critical network of temperature-controlled supply chain infrastructure, encompassing both refrigerated warehouse facilities and refrigerated transportation. Its primary function is to maintain product integrity for temperature-sensitive goods, driven by the global trade in perishable food items and the expansion of the pharmaceutical supply chain.

- Key trends influencing the sector include widespread industry consolidation and the integration of digital technologies such as real-time tracking and IoT-enabled telematics. For instance, a global distributor of biologics and vaccines might leverage a combination of vacuum insulated panels and real-time temperature logging to guarantee thermal stability across continents, ensuring that life-saving medicines do not suffer a temperature excursion.

- This level of precision is becoming standard. However, the industry faces challenges related to high energy consumption and significant infrastructure deficits in emerging economies, which can lead to high rates of post-harvest spoilage. As a result, companies are increasingly investing in energy-efficient cooling and sustainable refrigeration to balance operational excellence with environmental responsibility while navigating complex cross-border logistics.

What will be the Size of the Cold Chain Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cold Chain Market Segmented?

The cold chain industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Refrigerated warehouse

- Refrigerated transportation

- Application

- Meat fish and seafood

- Fruits vegetables and beverages

- Dairy and frozen desserts

- Bakery and confectionery

- Healthcare

- Product type

- Chilled

- Frozen

- Deep frozen

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The refrigerated warehouse segment is estimated to witness significant growth during the forecast period.

The refrigerated warehouse segment is the cornerstone of the cold chain, evolving into sophisticated hubs with multi-temperature environments. These facilities are critical for the pharmaceutical supply chain and for handling a surge in frozen convenience foods.

The primary driver of transformation is automation, where the integration of automated storage and retrieval systems (ASRS) has increased storage density by up to 40% in high-cost urban areas.

Operators are focused on maintaining thermal stability and preventing any temperature excursion through advanced monitoring.

This shift toward technology-driven operations is essential for meeting the complex demands of modern logistics and ensuring product safety, addressing everything from high-resolution temperature data requirements to zero-drift performance for sensitive goods from the warehouse to the final destination.

The Refrigerated warehouse segment was valued at USD 247 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 32.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cold Chain Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the cold chain market is characterized by a dual dynamic: rapid expansion in developing regions and technological maturation in established ones.

APAC leads global expansion, accounting for 32.7% of the market's incremental growth, driven by urbanization and the need to improve food security.

This contrasts with North America and Europe, which together represent over 60% of the market and focus on optimizing existing infrastructure.

In these mature markets, third-party logistics (3PL) providers are leveraging technology to achieve a 15% reduction in transit times for perishable food items.

The deployment of specialized reefer containers and the establishment of sophisticated cryogenic logistics networks are critical for handling the international trade of both food and pharmaceuticals.

This regional divergence underscores the varied strategies required to capitalize on opportunities, from building foundational temperature-controlled supply chain networks to refining advanced controlled atmosphere storage solutions for high-value goods.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic shifts in the cold chain market are increasingly visible, with the M&A impact on cold chain market consolidation creating larger, more integrated service providers. These entities are better positioned to invest in technology to differentiate their offerings.

- For instance, the widespread adoption of RFID for cold chain traceability and IoT integration in refrigerated transport is becoming standard for improving customer satisfaction cold chain services. In warehousing, the trend is toward automation in refrigerated warehousing, where the ASRS benefits in cold storage include higher density and reduced labor costs.

- These technological advancements are crucial for addressing the growth of pharma e-commerce logistics, which demands flawless last-mile logistics for pharmaceuticals and sophisticated thermal packaging for biologics delivery. Simultaneously, the food sector benefits from innovations like controlled atmosphere for fruits vegetables and specialized deep frozen logistics for seafood, which are key to reducing post-harvest loss with cold chain networks.

- However, operators still grapple with significant hurdles, including the persistent challenges in last-mile cold delivery and underdeveloped cold chain infrastructure in developing economies. Operationally, managing fuel price volatility logistics remains a primary concern, pushing firms toward sustainable cold storage solutions and the use of natural refrigerants in cold chain operations.

- Companies that successfully deploy real-time monitoring for perishable goods report customer retention rates more than 15% higher than peers using legacy systems, highlighting that technology is key to overcoming both new and old industry challenges.

What are the key market drivers leading to the rise in the adoption of Cold Chain Industry?

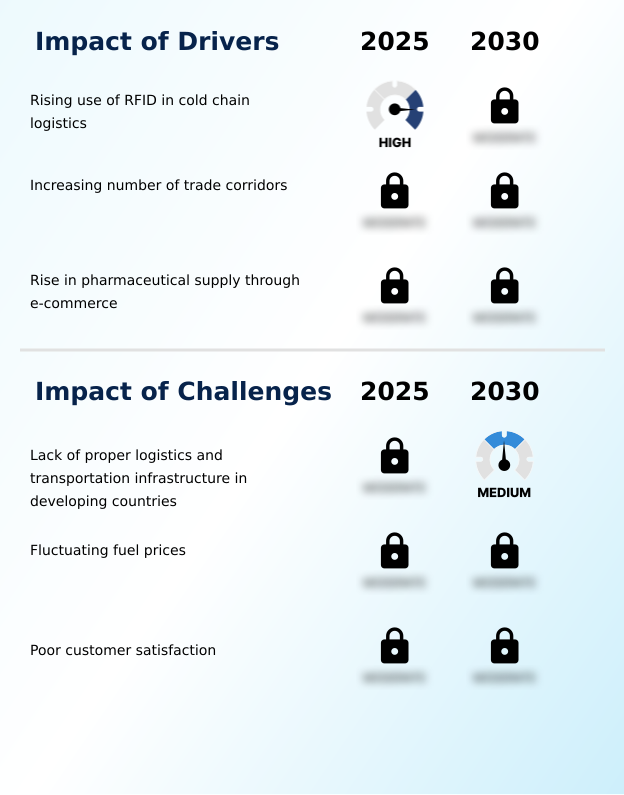

- The rising use of RFID technology in cold chain logistics is a key driver, enhancing traceability and operational efficiency across the supply chain.

- Market growth is significantly propelled by technological advancements and evolving consumer demands. The rising adoption of RFID for real-time tracking is a primary driver, enhancing product integrity and reducing manual errors by over 95%.

- This is complemented by the expansion of international trade corridors, which bolsters cross-border logistics and strengthens supply chain resilience.

- Simultaneously, the rapid growth of pharma e-commerce logistics is creating immense demand for specialized last-mile cold chain solutions capable of handling sensitive biologics and vaccines.

- This has spurred a 30% rise in demand for advanced delivery systems supported by digital health platforms.

- Together, these drivers are fostering a more connected and responsive logistics network that supports both global commerce and public health, particularly in port-centric logistics hubs.

What are the market trends shaping the Cold Chain Industry?

- A significant trend shaping the industry is the increasing consolidation through merger and acquisition activities, which allows major players to expand their global footprint and diversify service offerings.

- Key trends are reshaping the cold chain market, driven by a pursuit of greater efficiency and transparency. Industry consolidation through mergers and acquisitions is creating large-scale operators capable of making significant investments in technology, which is leading to greater economies of scale.

- The integration of the Internet of Things is central to this transformation, with IoT-enabled telematics platforms providing unprecedented control and visibility. This shift supports the rise of fully automated dark warehouses that utilize advanced warehouse management software and automated storage and retrieval systems (ASRS).

- The adoption of such technologies has been shown to increase high storage density by up to 40% in urban fulfillment centers. This commitment to technology-driven operational excellence is fundamentally altering how temperature-sensitive goods are stored and moved globally.

What challenges does the Cold Chain Industry face during its growth?

- A key challenge affecting industry growth is the lack of proper logistics and transportation infrastructure, particularly in developing countries.

- The market contends with persistent operational and economic challenges that can impede growth. A primary restraint is the energy-intensive logistics model, where fluctuating fuel prices can elevate operating costs for refrigerated vehicle fleets by up to 25% in a single quarter, often necessitating unpopular fuel surcharges. In many emerging markets, inadequate infrastructure leads to high rates of post-harvest spoilage.

- Furthermore, a failure to provide end-to-end visibility often results in poor customer satisfaction, with service failures accounting for over 50% of complaints. To mitigate these issues, companies are adopting more customer-centric logistics strategies, investing in energy-efficient cooling systems, and utilizing validated thermal packaging to safeguard shipments and rebuild trust.

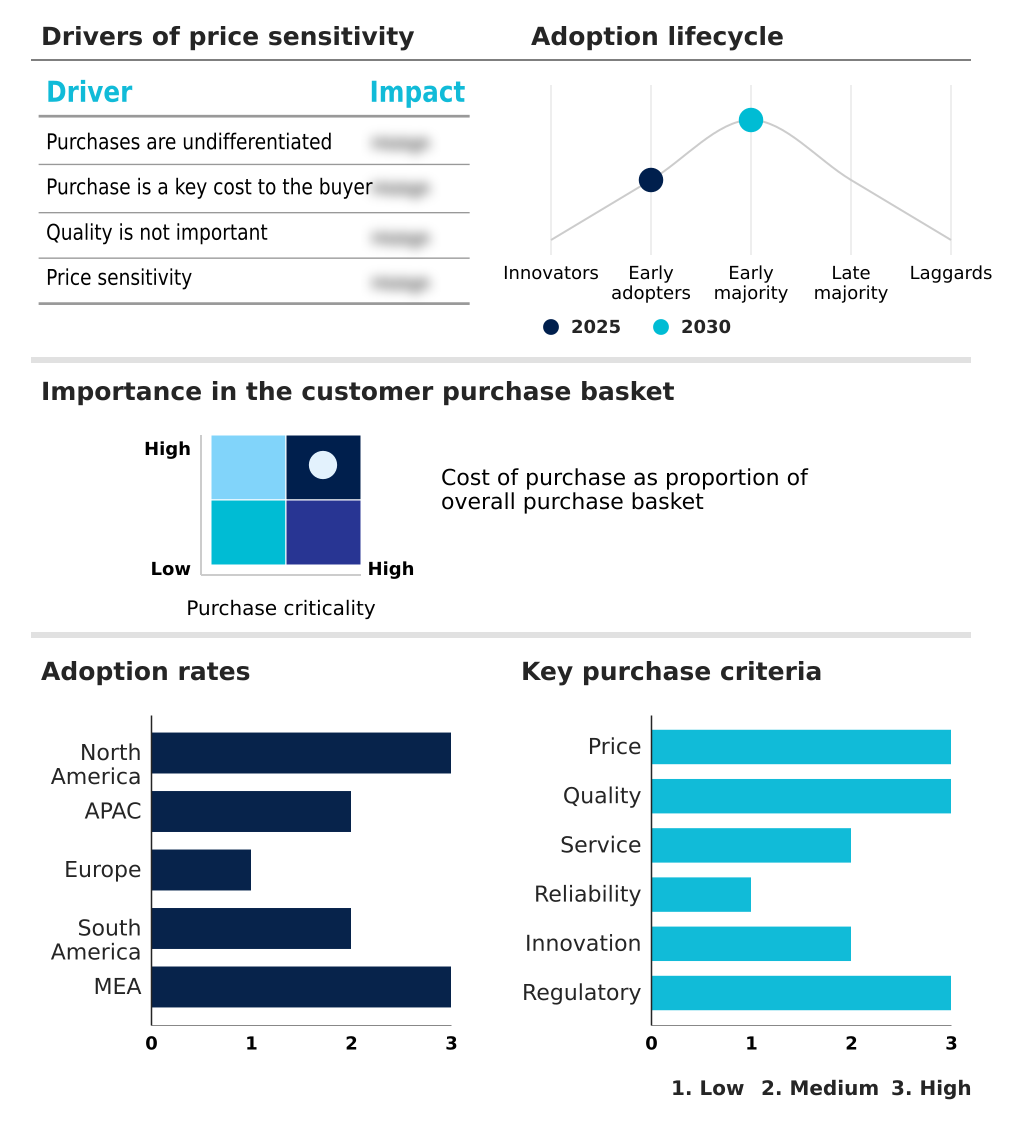

Exclusive Technavio Analysis on Customer Landscape

The cold chain market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cold chain market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cold Chain Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cold chain market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Americold Realty Trust Inc. - Offerings include end-to-end temperature-controlled logistics, ensuring product integrity for sensitive food and pharmaceutical supply chains through advanced monitoring and specialized handling.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Americold Realty Trust Inc.

- AP Moller Maersk AS

- C H Robinson Worldwide Inc.

- Constellation Cold Logistics

- DHL International GmbH

- DSV AS

- Emergent Cold LatAm Management

- FedEx Corp.

- Kuehne Nagel Management AG

- Lineage Inc.

- NewCold Cooperatief UA

- Nichirei Corp.

- Nippon Express Holdings Inc.

- Schenker AG

- Snowman Logistics Ltd.

- STEF Group

- Tippmann Group

- United Parcel Service Inc.

- United States Cold Storage

- YUSEN LOGISTICS CO. LTD.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cold chain market

- In April 2025, Lineage Logistics announced a strategic expansion project in the Latin American region, focusing on building high-capacity refrigerated hubs to bridge infrastructure gaps between production zones and major shipping ports.

- In February 2025, Thermo King launched its new generation of IoT-enabled telematics platforms, designed to provide more precise control over refrigerated transport units and enhance real-time monitoring capabilities.

- In March 2025, Kuehne + Nagel Management AG announced a strategic partnership with a leading biotech firm to provide end-to-end cryogenic logistics for cell and gene therapies, enhancing its capabilities in the ultra-low temperature segment.

- In October 2024, C.H. Robinson Worldwide Inc. unveiled a new sustainability-focused cold storage facility in the Netherlands, featuring a full-rooftop solar array and an advanced CO2 refrigeration system to minimize its environmental footprint.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cold Chain Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.8% |

| Market growth 2026-2030 | USD 842.1 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.7% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cold chain market is an essential global infrastructure built upon a temperature-controlled supply chain that integrates refrigerated warehouse facilities with refrigerated transportation. Its function is to preserve sensitive goods, from perishable food items to advanced biologics and vaccines, by maintaining strict thermal stability.

- A dominant trend is the move toward fully automated dark warehouses leveraging automated storage and retrieval systems (ASRS), which presents a critical boardroom decision: balancing high capital expenditure against long-term operational savings and enhanced supply chain resilience. This technological shift is not merely for efficiency; it is a strategic response to increasing regulatory demands and customer expectations for end-to-end visibility.

- For example, facilities implementing IoT-enabled telematics with real-time temperature logging have cut undetected temperature excursion events by over 60%. This drive for precision is evident across all modalities, including the use of specialized reefer containers for sea freight, advanced thermal packaging solutions for the last-mile cold chain, and the expansion of port-centric logistics to streamline global trade.

What are the Key Data Covered in this Cold Chain Market Research and Growth Report?

-

What is the expected growth of the Cold Chain Market between 2026 and 2030?

-

USD 842.1 billion, at a CAGR of 22.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Refrigerated warehouse, and Refrigerated transportation), Application (Meat fish and seafood, Fruits vegetables and beverages, Dairy and frozen desserts, Bakery and confectionery, and Healthcare), Product Type (Chilled, Frozen, and Deep frozen) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising use of RFID in cold chain logistics, Lack of proper logistics and transportation infrastructure in developing countries

-

-

Who are the major players in the Cold Chain Market?

-

Americold Realty Trust Inc., AP Moller Maersk AS, C H Robinson Worldwide Inc., Constellation Cold Logistics, DHL International GmbH, DSV AS, Emergent Cold LatAm Management, FedEx Corp., Kuehne Nagel Management AG, Lineage Inc., NewCold Cooperatief UA, Nichirei Corp., Nippon Express Holdings Inc., Schenker AG, Snowman Logistics Ltd., STEF Group, Tippmann Group, United Parcel Service Inc., United States Cold Storage and YUSEN LOGISTICS CO. LTD.

-

Market Research Insights

- The market is defined by a push for greater efficiency and reliability to ensure product integrity. This is driven by the expansion of online grocery platforms and the complex needs of delivering biologics and vaccines. The adoption of advanced monitoring for end-to-end visibility has led to a 40% reduction in spoilage events due to temperature excursion issues.

- Furthermore, third-party logistics (3PL) providers are achieving operational excellence by focusing on customer-centric logistics models, which improve client retention by over 15%.

- Strict regulatory adherence, such as compliance with the Food Safety Modernization Act (FSMA), has been shown to improve overall supply chain resilience by 25%, reinforcing the importance of disciplined operational frameworks in managing cross-border logistics and maintaining food security.

We can help! Our analysts can customize this cold chain market research report to meet your requirements.

RIA -

RIA -