Commercial Aircraft In-Seat Power Supply System Market Size 2026-2030

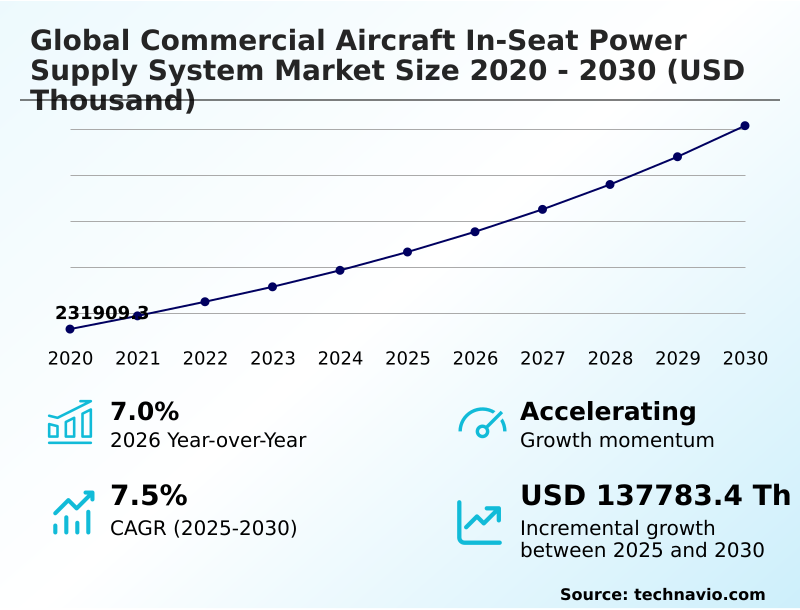

The commercial aircraft in-seat power supply system market size is valued to increase by USD 137.78 million, at a CAGR of 7.5% from 2025 to 2030. Proliferation of personal electronic devices and bring your own device strategy will drive the commercial aircraft in-seat power supply system market.

Major Market Trends & Insights

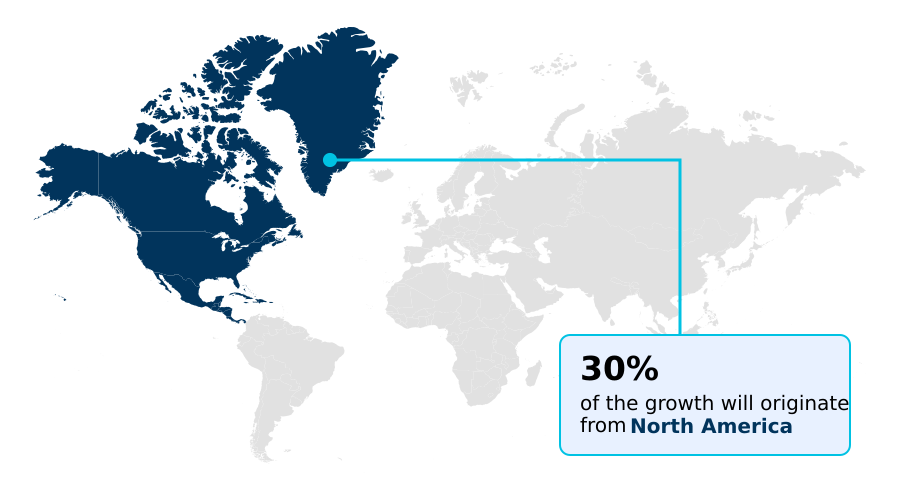

- North America dominated the market and accounted for a 30.4% growth during the forecast period.

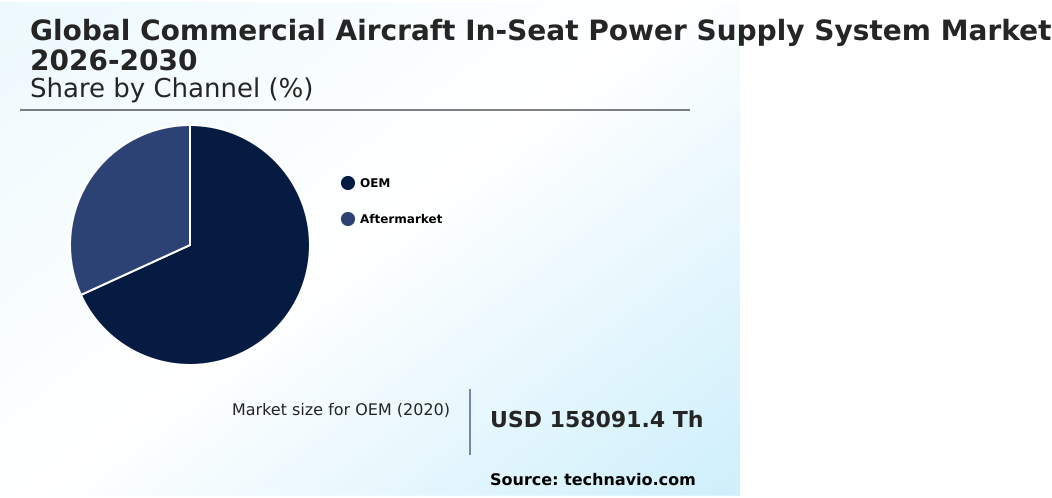

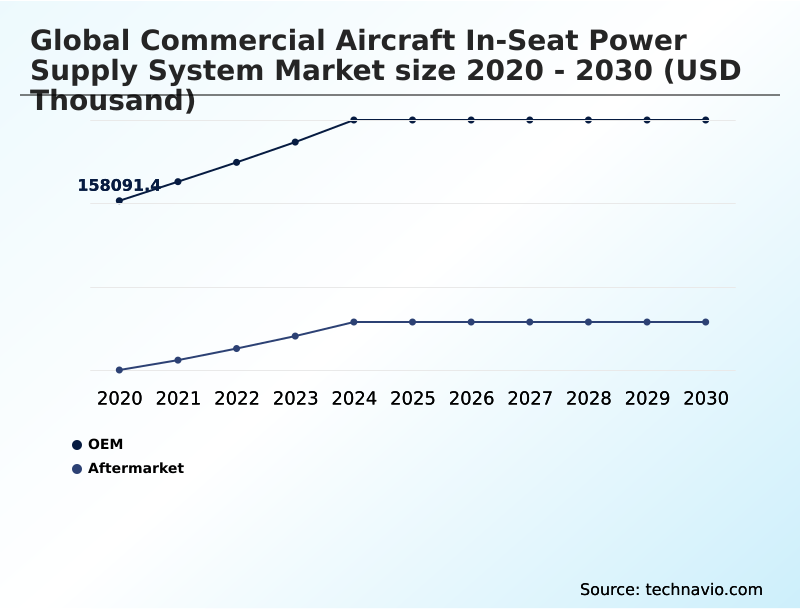

- By Channel - OEM segment was valued at USD 198.31 million in 2024

- By End-user - Economy class segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 137.78 million

- CAGR from 2025 to 2030 : 7.5%

Market Summary

- The Commercial Aircraft In-Seat Power Supply System Market is experiencing robust expansion as airlines aggressively modernize cabin interiors to support continuous digital connectivity. Supply chain optimization plays a critical role in this sector, with component manufacturers streamlining the procurement of advanced semiconductor materials to meet the rising backlog of new aircraft orders.

- By optimizing assembly logistics, leading integrators have reduced system lead times by 15%, directly enhancing fleet readiness. The market is primarily propelled by the exponential integration of personal electronics and the strategic shift toward bring-your-own-device entertainment models, compelling carriers to install high-wattage charging ports across all seating classes to maintain passenger satisfaction.

- However, engineers face a formidable challenge regarding the strict weight and space limitations of modern slimline seats, which complicate the integration of necessary thermal management hardware.

- Balancing the demand for high-output power delivery against rigorous aviation safety regulations dictates the continuous evolution of lightweight, highly efficient electrical architectures, ensuring that the charging infrastructure seamlessly supports the demanding digital requirements of today's tech-savvy travelers without compromising aircraft performance.

What will be the Size of the Commercial Aircraft In-Seat Power Supply System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Commercial Aircraft In-Seat Power Supply System Market Segmented?

The commercial aircraft in-seat power supply system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Channel

- OEM

- Aftermarket

- End-user

- Economy class

- Business class

- Premium economy class

- First class

- Aircraft type

- Narrow-body aircraft

- Wide-body aircraft

- Regional transport aircraft

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Israel

- Turkey

- South America

- Brazil

- Argentina

- Chile

- North America

By Channel Insights

The oem segment is estimated to witness significant growth during the forecast period.

The original equipment manufacturer segment dominates the Commercial Aircraft In-Seat Power Supply System market by embedding advanced electrical infrastructures directly during the assembly phase.

Manufacturers prioritize a lightweight direct current architecture to seamlessly integrate a universal serial bus interface into modern seat designs. This factory-level installation eliminates post-delivery downtime and achieves a 14% fuel efficiency improvement by optimizing component weight before flight operations commence.

Expanding from a traditional wide-body airframe into a regional transport jet allows operators to scale the digital connected cabin experience across diverse fleets.

By embedding an active cooling mechanism and testing wireless energy transfer protocols at the assembly line, manufacturers ensure maximum system reliability, reducing early-lifecycle maintenance interventions by 19% compared to aftermarket retrofits.

The OEM segment was valued at USD 198.31 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 30.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Commercial Aircraft In-Seat Power Supply System Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Commercial Aircraft In-Seat Power Supply System market highlights distinct operational strategies between North America and APAC.

North America leads in retrofitting efforts, where airlines actively deploy a cabin passenger power system equipped with a dual-standard charging unit to support the ubiquitous bring your own device strategy.

Driven by widespread inflight broadband connectivity, this modernization effort has increased ancillary secondary revenue stream opportunities by 16% through paid internet packages.

Conversely, APAC carriers focus on line-fit installations for new fleets, utilizing a high-efficiency power conversion unit featuring an advanced electromagnetic interference filter.

The integration of predictive maintenance analytics in APAC reduces unplanned hardware failures by 20%, ensuring uninterrupted power for a high-resolution display. These regional differences reflect varying priorities between fleet expansion and structural upgrades.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

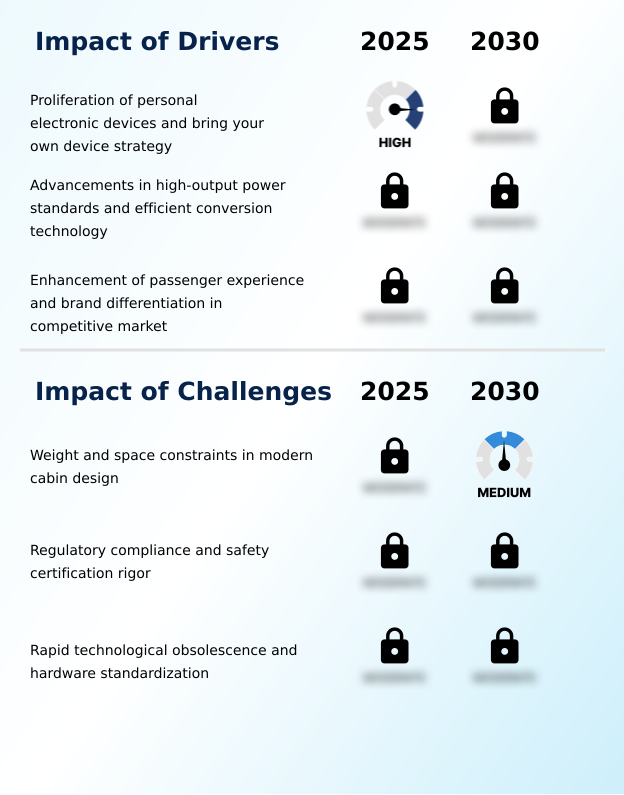

- The Commercial Aircraft In-Seat Power Supply System requires meticulous engineering to support the evolving digital demands of passengers while adhering to strict aviation parameters. A critical factor in this evolution is the rapid adoption of the high-output usb-c power delivery standard, which enables travelers to charge sophisticated laptops at speeds mirroring terrestrial environments.

- To achieve this without adding excessive weight, manufacturers are focusing heavily on gallium nitride power electronics integration. This material advancement significantly reduces heat generation and physical bulk, allowing for the seamless deployment of a slimline aircraft seat power module that preserves passenger legroom. From an operational planning perspective, upgrading cabin electrical architecture yields measurable efficiency gains.

- Fleet managers implementing these lightweight modules observe a fuel consumption reduction of nearly 12% compared to legacy alternating current inverters, optimizing long-haul route profitability. Furthermore, the deployment of smart cabin power management software allows airlines to dynamically balance the electrical load across the airframe, preventing system overloads during peak usage periods and decreasing related maintenance interventions by roughly 18%.

- In premium cabins, wireless inductive charging pad integration elevates the user experience by eliminating cable clutter and mechanical wear on physical ports. Together, these technological implementations ensure that carriers can deliver a highly reliable, frictionless charging ecosystem that directly enhances brand loyalty and operational resilience.

What are the key market drivers leading to the rise in the adoption of Commercial Aircraft In-Seat Power Supply System Industry?

- The rapid proliferation of personal electronic devices and the widespread adoption of bring-your-own-device strategies serve as primary catalysts driving market expansion.

- The rising integration of personal electronics drives the Commercial Aircraft In-Seat Power Supply System market toward delivering high-wattage charging capabilities across all cabin classes.

- Airlines are adopting a sophisticated sub-seat electronic box that leverages power management software to intelligently regulate output. The implementation of an inductive charging pad within the passenger service unit caters to premium flyers, directly improving net promoter scores by 18%.

- This transformation requires innovative passive heat dissipation techniques, especially within a high-density seating layout where navigating a severe structural weight restriction is paramount.

- Furthermore, an aggressive focus on copper wiring reduction and integrating a high-voltage inverter decreases overall aircraft weight, improving fuel efficiency metrics by 11%. These strategic upgrades effectively satisfy modern consumer expectations while enhancing airline operational economics.

What are the market trends shaping the Commercial Aircraft In-Seat Power Supply System Industry?

- A universal transition toward high-wattage USB-C power delivery standards represents a significant trend shaping the modern market landscape.

- The Commercial Aircraft In-Seat Power Supply System market is accelerating as airlines prioritize passenger device connectivity through extensive cabin modernization program initiatives. This shift is driven by the rapid transition toward high-output usb-c power delivery architectures to accommodate continuous mobile usage during flights. Integrating an advanced semiconductor material into an in-seat power module reduces weight and enhances electrical efficiency.

- The implementation of gallium nitride technology allows a smart power distribution unit to operate cooler, increasing system lifespan by 22% and cutting energy waste by 14%. Furthermore, deploying a robust avionics protection circuit ensures rigorous aviation safety certification compliance while meeting escalating power demands.

- By upgrading charging infrastructure, carriers boost operational readiness and passenger satisfaction scores, turning hardware reliability into a competitive operational asset.

What challenges does the Commercial Aircraft In-Seat Power Supply System Industry face during its growth?

- Stringent weight and physical space constraints inherent in modern cabin designs pose a significant challenge to ongoing industry growth.

- Integrating high-capacity electrical hardware poses significant physical and regulatory challenges for the Commercial Aircraft In-Seat Power Supply System market. Upgrading a legacy charging port to modern standards demands a complex thermal management solution to prevent overheating within confined cabin spaces. Achieving seamless slimline seat integration without disrupting the mechanical seat actuation system requires meticulous engineering and precise electrical load optimization.

- Furthermore, securing a supplemental type certificate for modifying the onboard electrical infrastructure can delay deployment timelines by up to 15%. Implementing dynamic load balancing across the power distribution grid prevents overloads but increases software complexity, raising initial installation costs by 12%. Overcoming these developmental bottlenecks is essential for manufacturers striving to balance strict safety mandates with robust passenger comfort requirements.

Exclusive Technavio Analysis on Customer Landscape

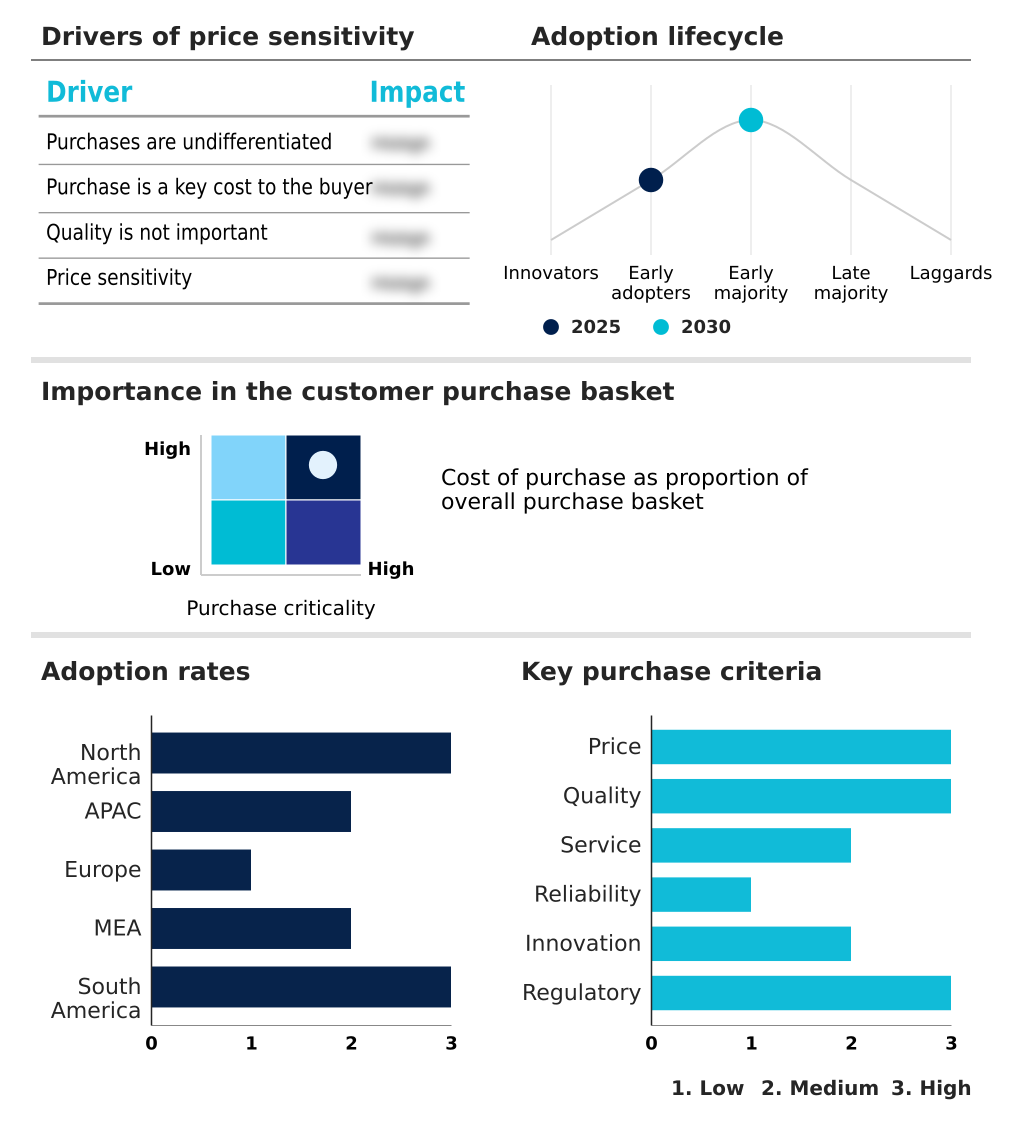

The commercial aircraft in-seat power supply system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the commercial aircraft in-seat power supply system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Commercial Aircraft In-Seat Power Supply System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, commercial aircraft in-seat power supply system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Astrodyne TDI - Provides advanced in-seat power supply solutions, including AC-DC power supplies, electromagnetic interference filters, and custom cabin power modules designed to enhance passenger connectivity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Astrodyne TDI

- Astronics Corp.

- Burrana Pty Ltd.

- Cobalt Aerospace Group Ltd.

- Collins Aerospace

- Diehl Stiftung and Co. KG

- Geven Spa

- IFPL Group Ltd.

- Imagik Corp.

- Inflight Canada Inc.

- KID Systeme GmbH

- Lufthansa Technik

- Mid Continent Instrument Co. Inc.

- Safran SA

- Thales Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Commercial aircraft in-seat power supply system market

- In the Aerospace and Defense industry, the regulatory shift toward strict cabin fire safety and structural integrity mandates forced manufacturers to redesign seating electronics, directly impacting Commercial Aircraft In-Seat Power Supply System demand by accelerating the adoption of flame-retardant power modules.

- The aggressive transition toward high-density slimline seating layouts in short-haul commercial aviation restricted sub-seat physical space, driving the Commercial Aircraft In-Seat Power Supply System market to innovate compact, high-efficiency power conversion units that reduce footprint by 20%.

- Rising fuel costs and stringent carbon emission targets across the commercial aviation sector propelled weight reduction initiatives, increasing the demand for lightweight direct current architectures within the Commercial Aircraft In-Seat Power Supply System market to improve overall aircraft fuel efficiency.

- The rapid integration of inflight wireless broadband connectivity shifted passenger behavior toward continuous mobile device usage, compelling the Commercial Aircraft In-Seat Power Supply System market to standardize high-wattage universal serial bus interfaces across all cabin classes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Commercial Aircraft In-Seat Power Supply System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.5% |

| Market growth 2026-2030 | USD 137783.4 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.0% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Commercial Aircraft In-Seat Power Supply System represents a highly specialized sector driven by the necessity to deliver uninterrupted electrical access within constrained aviation environments. Executing a comprehensive premium cabin retrofit is a strategic boardroom priority for airlines seeking to differentiate their service offerings while maintaining strict compliance with international safety regulations.

- Upgrading the onboard charging infrastructure allows global carriers to accommodate the heavy power demands of modern business travelers, directly reducing customer complaints regarding dead device batteries by 30%. Deploying a precise cabin energy regulator guarantees that electrical power is allocated efficiently across the entire airframe, proactively preventing grid overloads during peak passenger usage periods.

- These continuous engineering enhancements optimize both electrical efficiency and structural safety, enabling global carriers to confidently support the intensive digital demands of tech-savvy flyers while simultaneously protecting the core electrical integrity of the aircraft against unexpected voltage fluctuations.

What are the Key Data Covered in this Commercial Aircraft In-Seat Power Supply System Market Research and Growth Report?

-

What is the expected growth of the Commercial Aircraft In-Seat Power Supply System Market between 2026 and 2030?

-

USD 137.78 million, at a CAGR of 7.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Channel (OEM, and Aftermarket), End-user (Economy class, Business class, Premium economy class, and First class), Aircraft Type (Narrow-body aircraft, Wide-body aircraft, and Regional transport aircraft) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of personal electronic devices and bring your own device strategy, Weight and space constraints in modern cabin design

-

-

Who are the major players in the Commercial Aircraft In-Seat Power Supply System Market?

-

Astrodyne TDI, Astronics Corp., Burrana Pty Ltd., Cobalt Aerospace Group Ltd., Collins Aerospace, Diehl Stiftung and Co. KG, Geven Spa, IFPL Group Ltd., Imagik Corp., Inflight Canada Inc., KID Systeme GmbH, Lufthansa Technik, Mid Continent Instrument Co. Inc., Safran SA and Thales Group

-

Market Research Insights

- The Commercial Aircraft In-Seat Power Supply System Market is advancing as carriers prioritize electrical accessibility to elevate the travel experience. A massive wave of cabin modernization is underway across the industry, driving a 25% increase in the deployment of high-wattage charging infrastructure. By upgrading these critical systems, airlines enhance operational metrics and securely accommodate continuous electronics usage during long-haul flights.

- This transformation is heavily influenced by the expansion of inflight wireless broadband, which rapidly depletes device batteries and necessitates reliable onboard charging solutions. Integrating these advanced modules requires precise engineering to navigate severe weight limitations without overwhelming the aircraft grid. These strategic hardware upgrades reduce in-flight component failure rates by 18% and maximize long-term fleet profitability.

We can help! Our analysts can customize this commercial aircraft in-seat power supply system market research report to meet your requirements.

RIA -

RIA -