Germany Construction Market Size 2026-2030

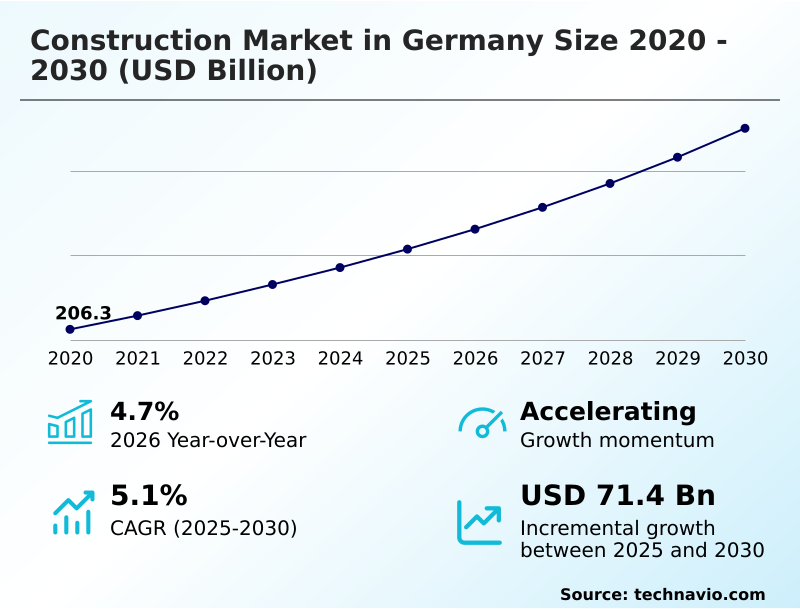

The germany construction market size is valued to increase by USD 71.4 billion, at a CAGR of 5.1% from 2025 to 2030. Climate-neutral building modernization and energy-efficient residential renovation will drive the germany construction market.

Major Market Trends & Insights

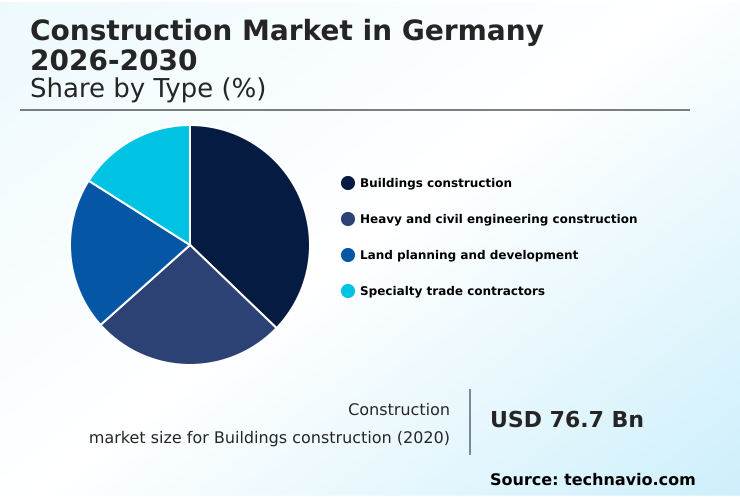

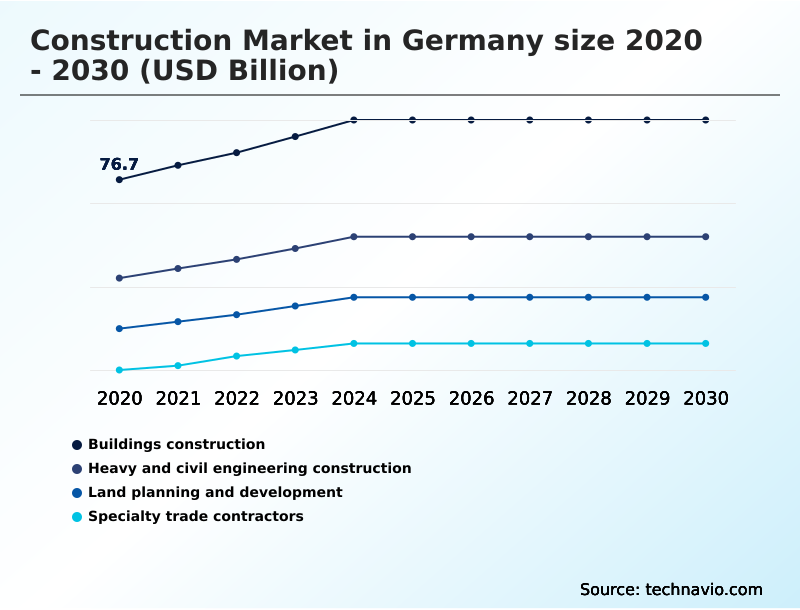

- By Type - Buildings construction segment was valued at USD 90.4 billion in 2024

- By End-user - Residential segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 118.8 billion

- Market Future Opportunities: USD 71.4 billion

- CAGR from 2025 to 2030 : 5.1%

Market Summary

- The construction market in germany is navigating a period of significant structural transformation, defined by a dual-track environment where resilient public infrastructure spending counterbalances a challenged residential sector. Strategic government initiatives are channeling massive investment into the modernization of transport networks, energy grids, and climate-resilient infrastructure, creating steady demand for civil engineering projects.

- Concurrently, the industry is grappling with persistent challenges, including a chronic skilled labor shortage, elevated financing costs, and complex decarbonization mandates that require a pivot toward sustainable material sourcing. A key trend is the accelerated adoption of digitalization, with building information modeling becoming standard practice for optimizing complex projects.

- For instance, a contractor undertaking a major railway construction project now utilizes digital twin technology not just for planning and execution but also for creating digital material passports.

- This enables compliance with circular economy protocols by tracking every component for future reuse, demonstrating a tangible shift toward resource-efficient engineering and long-term asset value management in response to evolving regulatory and market pressures. This integration of technology is critical for navigating the sector’s high-density urbanization demands and ensuring the delivery of modern multi-unit dwellings.

What will be the Size of the Germany Construction Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Germany Construction Market Segmented?

The germany construction industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Buildings construction

- Heavy and civil engineering construction

- Land planning and development

- Specialty trade contractors

- End-user

- Residential

- Commercial

- Public

- Sector

- Private sector

- Public sector

- Geography

- Europe

- Germany

- Europe

By Type Insights

The buildings construction segment is estimated to witness significant growth during the forecast period.

The buildings construction segment is shifting from conventional projects to specialized structures, driven by stringent decarbonization mandates. Activity is pivoting toward complex, high-value buildings that demand advanced capabilities in building information modeling and sustainable material sourcing.

While high financing costs have moderated new project starts in some areas, the market is adapting through the strategic application of modular construction methods and adaptive reuse of existing assets, which can improve project delivery timelines by up to 30%.

There is a clear focus on energy-efficient retrofitting and high-tech industrial facilities that support public infrastructure goals. The growing emphasis on timber-hybrid construction and resource-efficient engineering highlights a transition toward a more sustainable and climate-resilient infrastructure.

The Buildings construction segment was valued at USD 90.4 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The construction market is undergoing a profound transformation, driven by the convergence of digital innovation and sustainability mandates. The widespread adoption of BIM for infrastructure project management is a cornerstone of this shift, enabling firms to execute complex designs with greater precision.

- This is particularly vital for implementing sustainable urban development strategies and addressing the housing crisis through high-density housing project development. Advanced modeling allows for detailed prefabricated housing cost analysis models, making factory-built solutions more accessible. Simultaneously, a strong focus on energy efficiency in building renovation is reshaping the existing building stock.

- The persistent impact of labor shortage on construction is accelerating the adoption of automated equipment in earth-moving tasks and increasing investment in off-site fabrication in building projects. The circular economy in building materials is gaining traction, supported by technologies like material passports in sustainable construction, which track components from cradle to grave.

- Innovators are exploring self-repairing concrete technology applications and advanced framing solutions for construction to enhance durability and reduce waste. The use of a digital twin for civil engineering provides a virtual replica for lifecycle management, while virtual reality for 3D model comparison improves on-site accuracy.

- Companies integrating AI and machine learning in construction have reported reducing project planning cycles by more than half compared to those using conventional approaches. These advancements are crucial for navigating the challenges in urban infrastructure expansion, meeting regulatory compliance for green buildings, and modernizing public transport networks within new financing models for residential construction.

What are the key market drivers leading to the rise in the adoption of Germany Construction Industry?

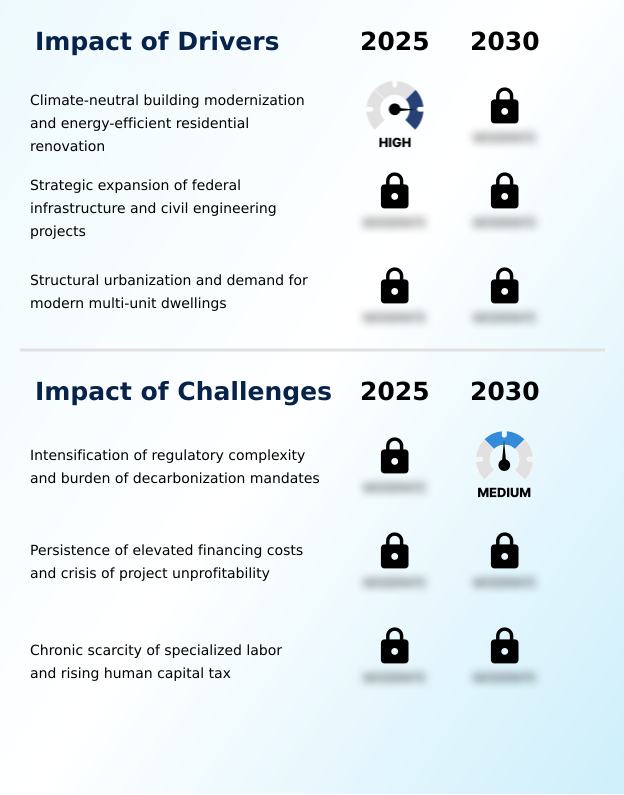

- Climate-neutral building modernization and energy-efficient residential renovation are key drivers propelling market growth.

- Market growth is primarily propelled by three key drivers. First, the strategic expansion of public infrastructure and civil engineering projects is a critical stabilizer, with a twelve-year government funding program underpinning modernization efforts.

- Second, the urgent need for climate-neutral building modernization and energy-efficient renovation is unlocking significant investment, supported by subsidies for technologies like heat pumps.

- Third, persistent demand for modern multi-unit dwellings driven by high-density urbanization continues to fuel real estate development, evidenced by a recent 8.4% rise in building permits for apartments.

- The adoption of AI-driven operational intelligence and resilience-based design is becoming essential for firms to execute these complex projects efficiently while navigating the transition to advanced, lightweight prefabricated envelopes.

What are the market trends shaping the Germany Construction Industry?

- The integration of circular economy protocols and digital material passports is becoming a defining market trend. This development is reshaping resource management and sustainability standards throughout the industry.

- Market trends are heavily influenced by the adoption of industrialization and digitalization to meet sustainability goals. The use of serial construction with volumetric units is accelerating project delivery, with some firms reporting productivity gains of up to 30%. This trend is critical for urban development projects aimed at providing affordable housing.

- Concurrently, the integration of circular economy protocols, facilitated by digital material passports, is enabling a reduction in construction waste by over 25% on compliant projects. There is also a major expansion in civil engineering to build climate-resilient infrastructure, requiring advanced structural engineering for tunneling and bridge construction.

- This is complemented by a focus on inclusive urban design and transit-oriented development, shaping how new communities are planned and executed.

What challenges does the Germany Construction Industry face during its growth?

- The intensification of regulatory complexity and the burden of decarbonization mandates present key challenges to industry growth.

- The market faces significant structural headwinds that temper growth prospects. The foremost challenge is the persistence of elevated financing costs, with interest rates more than tripling from recent lows, rendering many residential projects unprofitable and leading to widespread cancellations.

- This is compounded by intensifying regulatory complexity and a chronic skilled labor shortage, which together drive up project costs and extend timelines. Industry sentiment reflects these pressures, with activity in the housing sector contracting for several consecutive months.

- While the adoption of prefabricated systems and serial construction offers a path to mitigate labor constraints, the high initial capital investment remains a barrier for smaller firms. Navigating these challenges requires a strategic focus on efficiency and securing roles in large-scale transport infrastructure projects, often through public-private partnership models.

Exclusive Technavio Analysis on Customer Landscape

The germany construction market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the germany construction market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Germany Construction Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, germany construction market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bickhardt Bau AG - Analysis points to a specialization in integrated construction, delivering services across building, civil engineering, tunneling, and ground engineering for complex infrastructure.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bickhardt Bau AG

- Bremer AG

- Depenbrock Gruppe

- Ed. Zublin AG

- Eurovia Deutschland

- GOLDBECK GmbH

- GP Guenter Papenburg AG

- HOCHTIEF AG

- Johann Bunte Bauunternehmung

- KAEFER SE and Co.

- Koester GmbH

- Leonhard Weiss GmbH and Co.

- Lindner Group

- Ludwig Freytag GmbH and Co.

- Max Bogl Bauservice GmbH

- PORR AG

- STRABAG SE

- W. MARKGRAF GmbH and Co. KG

- Zech Group SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Germany construction market

- In April 2025, HOCHTIEF AG secured two major building contracts totaling approximately $160 million, which include the development of a sustainable research center and the conversion of an industrial boiler house into a modern event center, highlighting a strategic pivot toward complex, specialized buildings.

- In March 2025, the German Parliament approved a significant debt package to fund infrastructure and climate-related projects over the next twelve years, with a substantial portion specifically earmarked for transport and utility developments, signaling a massive public investment push.

- In February 2025, at the digitalBAU trade fair in Cologne, industry leaders presented new software tools designed for the database-supported creation of digital material passports linked to 6D BIM models, reflecting the move toward resource-efficient engineering.

- In January 2025, the German parliament advanced the Act to Accelerate Residential Construction, introducing a 'construction turbo' mechanism to speed up planning and permitting procedures by allowing municipalities to deviate from existing zoning plans under certain conditions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Germany Construction Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 183 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.1% |

| Market growth 2026-2030 | USD 71.4 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.7% |

| Key countries | Germany |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a significant transition, driven by the dual pressures of high-density urbanization and stringent decarbonization mandates. This has led to a strategic pivot towards climate-neutral building and energy-efficient renovation, especially for multi-unit dwellings.

- The primary growth engine is the expansion of public infrastructure, including transport networks and energy grids, which requires advanced structural engineering for civil engineering projects such as road construction, railway construction, tunneling, and bridge construction.

- In response to regulatory complexity and a persistent skilled labor shortage, the industry is increasingly adopting building information modeling (BIM), serial construction, and prefabricated systems, which have demonstrated productivity increases of up to 30%. This shift is evident in the demand for turnkey building solutions for industrial construction and building envelope solutions.

- Key to navigating this landscape is the management of elevated financing costs and the adoption of technologies like digital material passports to comply with circular economy protocols.

- The focus is on delivering climate-resilient infrastructure by replacing fossil-fuel heating systems with high-performance building envelopes, all while managing the complexities of hydraulic engineering, ground engineering, asphalt paving, interior fit-out, real estate development, and project management services for urban development projects.

What are the Key Data Covered in this Germany Construction Market Research and Growth Report?

-

What is the expected growth of the Germany Construction Market between 2026 and 2030?

-

USD 71.4 billion, at a CAGR of 5.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Buildings construction, Heavy and civil engineering construction, Land planning and development, and Specialty trade contractors), End-user (Residential, Commercial, and Public), Sector (Private sector, and Public sector) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Climate-neutral building modernization and energy-efficient residential renovation, Intensification of regulatory complexity and burden of decarbonization mandates

-

-

Who are the major players in the Germany Construction Market?

-

Bickhardt Bau AG, Bremer AG, Depenbrock Gruppe, Ed. Zublin AG, Eurovia Deutschland, GOLDBECK GmbH, GP Guenter Papenburg AG, HOCHTIEF AG, Johann Bunte Bauunternehmung, KAEFER SE and Co., Koester GmbH, Leonhard Weiss GmbH and Co., Lindner Group, Ludwig Freytag GmbH and Co., Max Bogl Bauservice GmbH, PORR AG, STRABAG SE, W. MARKGRAF GmbH and Co. KG and Zech Group SE

-

Market Research Insights

- The market is characterized by divergent dynamics, with robust public-sector investment in civil engineering offsetting stagnation in private residential construction. Firms utilizing modular construction methods report productivity gains of up to 30%, a critical advantage in addressing the skilled labor shortage.

- While restrictive financing has cooled new housing starts, recent data indicates a nascent recovery, with building permits for apartments rising by 8.4% in early 2026, signaling renewed investor confidence. This environment favors companies proficient in resilience-based design and advanced structural engineering, as demand pivots toward high-value, energy-efficient assets and strategic infrastructure projects.

- The adoption of smart building management systems and transit-oriented development principles is becoming essential for developers to meet modern sustainability standards and attract capital.

We can help! Our analysts can customize this germany construction market research report to meet your requirements.

RIA -

RIA -