Corporate Blended Learning Market Size 2026-2030

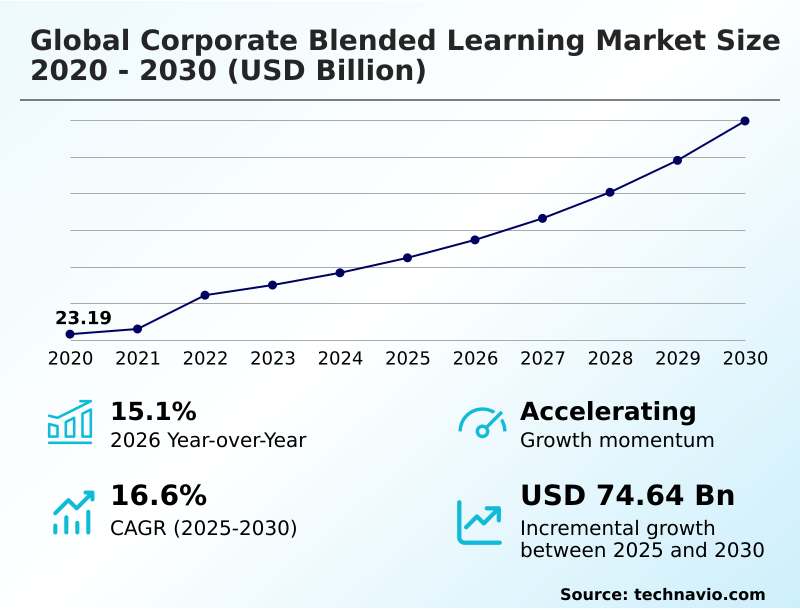

The Corporate Blended Learning Market size was valued at USD 64.83 billion in 2025, growing at a CAGR of 16.6% during the forecast period 2026-2030.

Major Market Trends & Insights

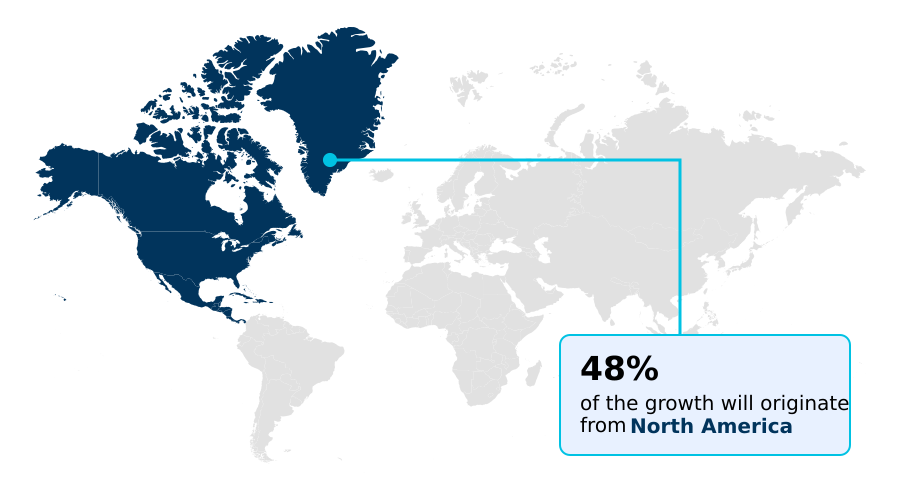

- North America dominated the market and accounted for a 48.2% growth during the forecast period.

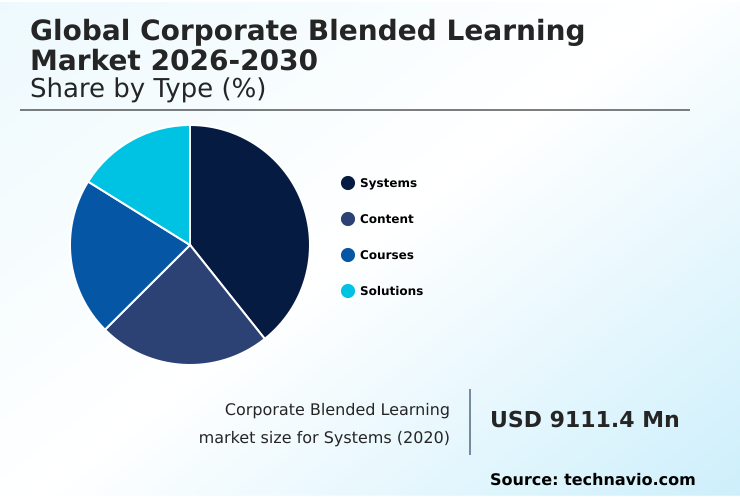

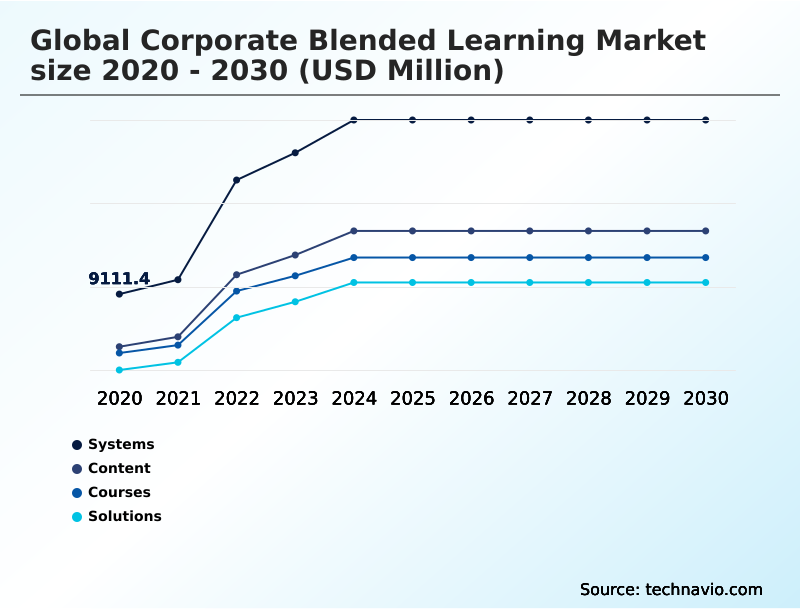

- By Type - Systems segment was valued at USD 21.43 billion in 2024

- By End-user - Automotive industry segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 116.29 billion

- Market Future Opportunities 2025-2030: USD 74.64 billion

- CAGR from 2025 to 2030 : 16.6%

Market Summary

- The corporate blended learning market is defined by a strategic pivot toward performance-driven training, with organizations reporting a 30% improvement in employee engagement when learning is tied to career development. The adoption of AI-first architectures is a primary driver, enabling the shift from static content libraries to dynamic, hyper-personalized skill acquisition at scale.

- For instance, a multinational manufacturing firm can deploy a blended program using virtual reality for hands-on safety training and AI-powered modules for theory, reducing on-site accidents by 15%. However, this progress is challenged by the technical debt of legacy systems, which creates data silos that hinder the effectiveness of advanced analytics and AI.

- Enterprises are thus prioritizing the consolidation of fragmented learning tools into unified ecosystems to unlock the full potential of data-driven professional development.

What will be the Size of the Corporate Blended Learning Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Corporate Blended Learning Market Segmented?

The corporate blended learning industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Systems

- Content

- Courses

- Solutions

- End-user

- Automotive industry

- BFSI sector

- Consumer goods industry

- Energy industry

- Others

- Methodology

- Instructor-led training

- Self-paced online learning

- Collaborative learning

- Experiential learning

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

How is the Corporate Blended Learning Market Segmented by Type?

The systems segment is estimated to witness significant growth during the forecast period.

The systems segment of the corporate blended learning market is shifting from static Learning Management Systems to dynamic Learning Experience Platforms, improving content discovery relevance by over 40%.

These AI-first architectures are crucial for workforce agility, automating tasks like content curation and skills gap analysis through a central skills ontology.

This evolution enables a more effective blended learning strategy, where organizations report a 25% faster time-to-competency for new hires. The integration of generative AI within these systems facilitates decentralized content creation, allowing subject-matter experts to produce high-quality microlearning modules.

This move toward an intelligent, interconnected learning ecosystem supports continuous professional development by embedding training directly into workflow interoperability tools, making asynchronous learning more impactful.

The Systems segment was valued at USD 21.43 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Corporate Blended Learning market is rising in the leading region?

North America is estimated to contribute 48.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Corporate Blended Learning Market demand is rising in North America Request Free Sample

The geographic landscape of the corporate blended learning market shows a clear division in maturity and focus, with North America commanding 48.17% of the market share, driven by high adoption of advanced AI-driven platforms.

In this region, particularly the US, the focus is on integrating learning into the flow of work to boost productivity, with enterprises investing in sophisticated talent intelligence systems.

In contrast, the APAC region, which accounts for 16.38% of the market, is characterized by mobile-first adoption and explosive growth in upskilling for the digital economy.

The difference in infrastructure and workforce dynamics means that while a North American company might deploy a complex industrial metaverse simulation, an APAC-based firm is more likely to utilize lightweight, mobile learning platforms for training, reflecting a more than 50% higher reliance on mobile devices for professional development.

What are the key Drivers, Trends, and Challenges in the Corporate Blended Learning Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are increasingly realizing the strategic importance of learning, moving beyond mere compliance to data-driven talent development. A key consideration is the impact of generative AI on instructional design, which has been shown to reduce content creation time by up to 50% while improving the relevance of materials.

- This technological shift is central to the discussion around measuring ROI of blended learning programs, as efficiency gains become more quantifiable. The most effective approach involves integrating LMS with internal talent mobility platforms, creating a seamless ecosystem where skill acquisition directly translates to career opportunities.

- This strategy answers the challenge of corporate blended learning for skills-based organizations by creating clear pathways for advancement. However, the lynchpin remains a robust framework for AI governance in corporate training solutions, ensuring that the use of these powerful tools is ethical, transparent, and compliant.

- Organizations that successfully navigate this complexity can achieve an over 2x improvement in employee retention compared to those with disjointed learning and development efforts.

What are the key market drivers leading to the rise in the adoption of Corporate Blended Learning Industry?

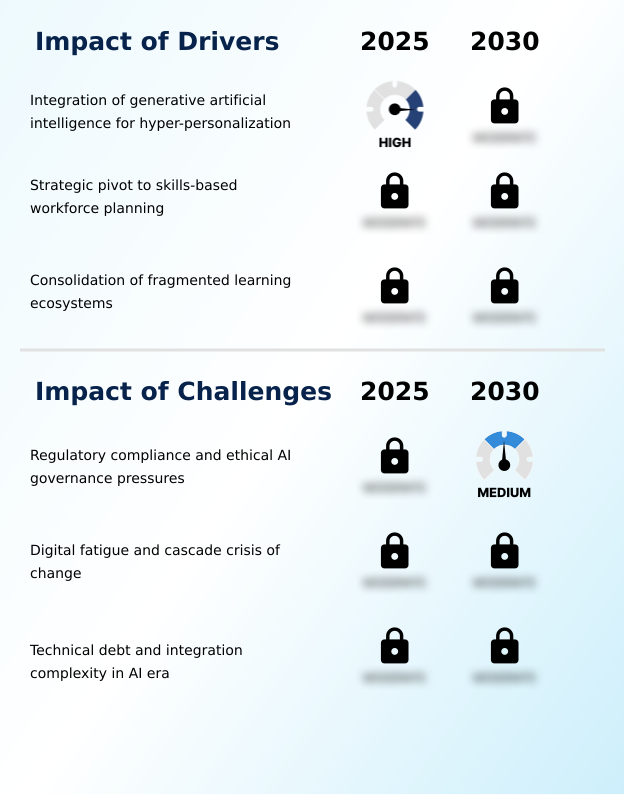

- The integration of generative artificial intelligence for hyper-personalization is the primary driver expanding the capabilities and adoption of corporate blended learning solutions.

- The primary driver for the corporate blended learning market is the strategic pivot to skills-based organizations, a model that has been shown to improve workforce agility by up to 50%.

- This transition creates a surge in demand for platforms that offer robust talent intelligence and can map learning to career progression, directly impacting employee retention.

- A second critical driver is the aggressive integration of generative AI for hyper-personalization, which automates content curation and makes asynchronous learning as responsive as live instruction, improving learner engagement rates by over 30%.

- Finally, the operational need to consolidate fragmented learning infrastructures into unified, cloud-based delivery models is pushing enterprises to invest in modern Learning Experience Platforms. This consolidation supports better data hygiene, which is a prerequisite for deploying effective learning analytics.

What are the market trends shaping the Corporate Blended Learning Industry?

- The market is witnessing a transformative trend with the emergence of agentic AI, which is enabling fully automated instructional design and content creation.

- A transformative trend in corporate blended learning is the convergence of learning management systems with internal talent mobility, where organizations with integrated platforms report a 25% increase in internal hiring. This shift is enabled by the adoption of a unified skills ontology.

- The market is also seeing the integration of the industrial metaverse and spatial computing for technical training, particularly in manufacturing and energy sectors, where using digital twin technology in a risk-free environment has been shown to reduce training-related accidents by over 40%.

- The evolution toward agentic AI is automating complex instructional design tasks, moving the learning ecosystem from a passive content repository to an active, intelligent co-pilot. This use of AI-first architecture for peer-to-peer knowledge sharing and workforce competency models redefines how organizations approach upskilling and reskilling.

What challenges does the Corporate Blended Learning Industry face during its growth?

- Regulatory compliance requirements and pressures for ethical AI governance present a significant challenge, impacting the design and deployment of modern learning platforms.

- A primary challenge restructuring the corporate blended learning market is the intense pressure to align with new data privacy regulations and AI governance frameworks, which can increase compliance-related overhead by up to 20%. This legal scrutiny creates a significant barrier to entry for smaller vendors.

- A second major challenge is digital tool fatigue and change saturation within the workforce, with studies showing that over 80% of employees feel overwhelmed by new technology deployments, which directly undermines engagement with new learning initiatives. This phenomenon of a cascade crisis limits the ROI of even the most advanced platforms.

- Finally, the technical debt from legacy systems creates significant integration complexity, as outdated data structures hinder the functionality of modern AI agents and experiential learning modules, creating a 'garbage in, garbage out' scenario.

Exclusive Technavio Analysis on Customer Landscape

The corporate blended learning market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the corporate blended learning market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Corporate Blended Learning Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, corporate blended learning market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allen Communication Learning Services - Key offerings include AI-driven corporate learning platforms, custom solutions for workforce capability, and strategic consulting for developing leadership and productivity skills.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allen Communication Learning Services

- BTS Group AB

- Cegos Group

- City and Guilds Group

- Cornerstone OnDemand Inc.

- D2L Corp.

- Docebo Inc.

- Franklin Covey Co.

- GBS Corporate Training

- GP Strategies Corp.

- Interaction Associates Inc.

- Korn Ferry

- Learning Technologies Group

- SAP SE

- Skillsoft Corp.

- Udemy Inc.

- Wilson Learning Worldwide Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Education Services industry, the enterprise-wide adoption of AI-first architectures is compelling a shift toward learning platforms with built-in generative AI and automated instructional design, directly increasing demand for sophisticated corporate blended learning solutions that support hyper-personalization.

- The formalization of AI governance frameworks, including data privacy regulations, is forcing a re-evaluation of learning technologies, creating a market preference for certified corporate blended learning platforms that ensure compliance and ethical AI use in employee training.

- A strategic pivot in workforce management toward skills-based organizations is increasing the need for corporate blended learning systems that integrate with talent mobility and performance management tools, linking continuous professional development directly to career progression.

- The consolidation of fragmented digital ecosystems within enterprises is driving investment in unified corporate blended learning suites that offer a single source of truth for learner data, improving analytics and enabling the effective deployment of AI-driven talent intelligence.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Corporate Blended Learning Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.6% |

| Market growth 2026-2030 | USD 74644.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.1% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The corporate blended learning market ecosystem is a complex network of interacting stakeholders, with technology providers of AI engines and cloud infrastructure forming the foundational layer, enabling over 70% of modern learning platforms. Solution providers, including LMS and LXP vendors, operate at the core, integrating content libraries, authoring tools, and analytics into unified suites.

- These vendors work closely with a diverse range of content creators and strategic consulting firms to deliver end-to-end training solutions. Regulatory bodies exert significant influence, particularly around data privacy and AI governance, shaping platform design and data handling protocols. Distribution is increasingly direct via cloud-based subscription models, targeting enterprise L&D departments.

- End-users in sectors like BFSI and automotive drive demand for specialized compliance and technical training, influencing over 40% of content development priorities.

What are the Key Data Covered in this Corporate Blended Learning Market Research and Growth Report?

-

What is the expected growth of the Corporate Blended Learning Market between 2026 and 2030?

-

The Corporate Blended Learning Market is expected to grow by USD 74.64 billion during 2026-2030, registering a CAGR of 16.6%. Year-over-year growth in 2026 is estimated at 15.1%%. This acceleration is shaped by integration of generative artificial intelligence for hyper-personalization, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Systems, Content, Courses, and Solutions), End-user (Automotive industry, BFSI sector, Consumer goods industry, Energy industry, and Others), Methodology (Instructor-led training, Self-paced online learning, Collaborative learning, and Experiential learning) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Systems segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 48.2% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Turkey and Egypt, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is integration of generative artificial intelligence for hyper-personalization, which is accelerating investment and industry demand. The main challenge is regulatory compliance and ethical ai governance pressures, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Corporate Blended Learning Market?

-

Key vendors include Allen Communication Learning Services, BTS Group AB, Cegos Group, City and Guilds Group, Cornerstone OnDemand Inc., D2L Corp., Docebo Inc., Franklin Covey Co., GBS Corporate Training, GP Strategies Corp., Interaction Associates Inc., Korn Ferry, Learning Technologies Group, SAP SE, Skillsoft Corp., Udemy Inc. and Wilson Learning Worldwide Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for corporate blended learning is intensifying, with vendors differentiating through AI innovation and ecosystem integration, where unified platforms show 35% higher adoption than fragmented solutions. Key players are aggressively moving beyond traditional LMS functionalities to offer comprehensive talent lifecycle management.

- Recent developments show a focus on skills intelligence, with platforms now able to map learning content to specific career pathways, reportedly improving internal mobility by over 20%. For example, vendors are introducing features like generative AI content creators and AI-powered coaching tools to enhance both learner engagement and administrative efficiency.

- These actions address the enterprise demand for measurable ROI on training investments, as companies navigate the challenge of upskilling their workforce for a digital-first economy while managing significant organizational change saturation.

We can help! Our analysts can customize this corporate blended learning market research report to meet your requirements.

RIA -

RIA -