Custom Procedure Packs Market Size 2024-2028

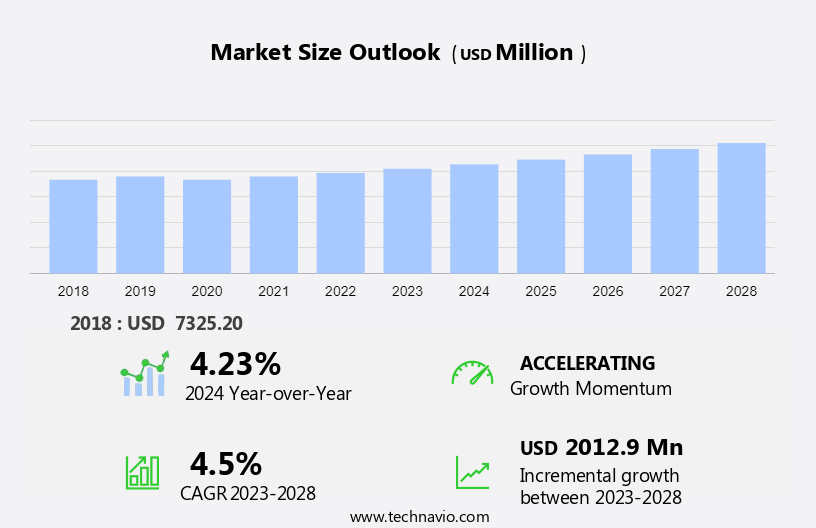

The custom procedure packs market size is forecast to increase by USD 2.01 billion, at a CAGR of 4.5% between 2023 and 2028. Custom procedure packs have gained significant importance in the healthcare industry due to the increasing demand for surgical procedures and the rising number of organ transplants. These packs are meticulously designed to include all the necessary instruments, supplies, and sterilization materials required for a specific surgical procedure. By using custom procedure packs, healthcare facilities can ensure standardization, sterility, and efficiency in their surgical processes. Moreover, these packs help reduce the risk of surgical site infections, minimize the chances of cross-contamination, and lower the overall cost of surgical procedures. The benefits of custom procedure packs extend to patients as well, who can expect improved safety, better outcomes, and reduced recovery time. In summary, custom procedure packs are an essential tool for healthcare providers, enabling them to deliver high-quality, cost-effective, and safe surgical care to their patients. The market report provides market size, historical data and future projections, all presented in terms of value in USD billion for each of the mentioned segments.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Request Free Sample

Market Dynamic and Customer Landscape

The market is a significant segment in the healthcare industry, catering to the specific needs of various medical specialties. These packs are used in healthcare settings, including hospitals, emergency centers, and homecare, to manage chronic diseases such as cardiovascular conditions, neurovascular conditions, ophthalmic conditions, and orthopedic conditions. The market comprises disposable and reusable procedure kits, used for inventory management and cross-contamination prevention. The market encompasses a wide range of products, including surgical drapes, wound dressings, surgical blades, cardiac catheters, implants, and surgical trays. Healthcare suppliers provide these packs to meet the demands of healthcare infrastructure and the increasing use of breakthrough medicines. Medical waste generated from these packs is a concern, leading to the development of more sustainable solutions. Surgical tools and instruments, such as cardiac catheters, implants, and surgical blades, are essential components of procedure packs. Effective inventory management is crucial to ensure the availability of these supplies in healthcare facilities. Reusable procedure packs are gaining popularity due to cost savings and reduced environmental impact. However, the risk of cross-contamination is a concern with reusable packs, leading to the continued use of disposable options in certain applications.

Key Market Driver

Growing need for surgical procedures is notably driving market growth. The global healthcare industry is experiencing a significant surge in the demand for medical supplies due to the increasing prevalence of chronic diseases, such as diabetes, obesity, and cardiovascular diseases. According to the International Diabetes Federation (IDF), approximately 537 million adults worldwide were living with diabetes in 2021, and this number is projected to reach 643 million by 2030 and 783 million by 2045. In response to this trend, healthcare suppliers are focusing on providing customized solutions to meet the specific needs of healthcare facilities, particularly in emergency centers and healthcare infrastructure. Two types of medical supplies that have gained popularity in recent years are Disposable Procedure Kits and Reusable Procedure Kits. Disposable Procedure Kits offer the advantage of eliminating the risk of cross contamination, making them ideal for use in emergency situations.

Besides, Reusable Procedure Packs are cost-effective and environmentally friendly, making them a preferred choice for routine procedures in healthcare facilities. However, proper sterilization procedures are essential to prevent the risk of infection. Healthcare suppliers are investing in research and development to create innovative solutions to address the unique requirements of healthcare facilities. For instance, they are developing reusable packs with advanced materials that can withstand multiple sterilization cycles without compromising the quality of the pack or the sterility of the contents. These developments are expected to drive the growth of the Custom Procedure Packs Market in the coming years. Thus, such factors are driving the growth of the market during the forecast period.

Significant Market Trends

Growing number of ambulatory surgery centers (ASCs) is the key trend in the market. In developed countries such as the US, Canada, the UK, France, and Germany, healthcare infrastructure includes a significant number of Ambulatory Surgery Centers (ASCs), which provide cost-effective, same-day surgical care. These centers offer patients access to fully equipped operating rooms for surgeries that do not necessitate hospitalization. According to Medicare data, ASCs are predominantly utilized for procedures in specialties like gastrointestinal, ophthalmology, neurology, orthopedic, urology, and dermatology. This trend is also emerging in developing countries like India and China, where ASCs are being implemented to alleviate the burden on physician clinics and hospitals.

Further, reusable Procedure Packs and Disposable Procedure Kits are essential components in ASCs to maintain hygiene and prevent cross-contamination. Reusable Procedure Kits undergo rigorous sterilization processes before and after use, ensuring patient safety. In contrast, Disposable Procedure Kits are used once and then discarded, eliminating the risk of reusing contaminated equipment. Overall, ASCs contribute significantly to the efficiency and affordability of healthcare services. Thus, such trends will shape the growth of the market during the forecast period.

Major Market Challenge

High cost of healthcare is the major challenge that affects the growth of the market. The global custom procedure packs market is experiencing significant growth due to the increasing demand for sterile and efficient medical supplies in healthcare institutions. However, the high costs associated with healthcare in developed nations, such as the US, Canada, and the UK, may pose a challenge to market growth during the forecast period. In 2019, the US had the most expensive healthcare system among these countries, with a per capita expenditure of USD 10,948.

Furthermore, other European nations, including Switzerland, Norway, Germany, the Netherlands, Austria, Denmark, Sweden, Ireland, France, Belgium, and Luxembourg, also had high per capita healthcare expenditures, ranging from USD 6,731 in Germany to USD 7,138 in Switzerland. This high cost can make reusable procedure packs and disposable procedure kits less economically viable for healthcare suppliers. Cross contamination is another concern in the use of reusable packs, which can increase the risk of infection and require additional resources for sterilization. Therefore, the demand for disposable procedure kits is increasing in emergency centers and healthcare infrastructure to mitigate these risks. Hence, the above factors will impede the growth of the market during the forecast period

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

3M Co.: The company offers custom procedure trays which is reliable and cost effective.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- B.Braun SE

- Cardinal Health Inc.

- Kimal Group

- Hubei Medlink Healthcare Co. Ltd.

- Med-italia Biomedica Srl

- Multigate Medical Products Pty Ltd.

- Medtronic Plc

- Molnlycke Health Care AB

- Owens and Minor Inc.

- Priontex

- Thermo Fisher Scientific Inc.

- Unisurge International Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

By Type

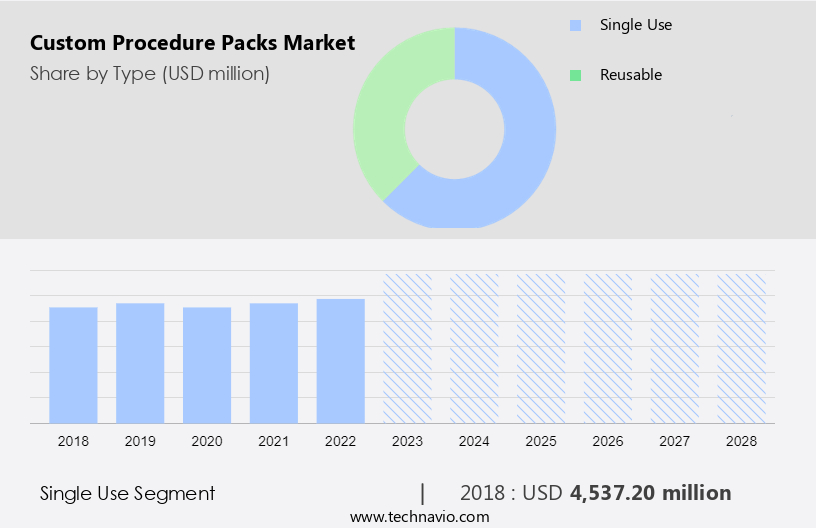

The single use segment is estimated to witness significant growth during the forecast period. In the healthcare industry, custom procedure packs have gained significant importance in managing chronic diseases, particularly in cardiovascular and neurovascular conditions, ophthalmic diseases, orthopedic conditions, and wound management. These packs consist of surgical tools, trays, disposables, and reusable kits, ensuring efficient inventory management and adherence to infection control protocols. Dental practices also utilize custom procedure packs with surgical gowns, personal protective equipment, and surgical swabs, sutures, drapes, and wound dressings. The orthopedic segment, including bone diseases and the geriatric population, benefits from minimally invasive and noninvasive procedures.

Get a glance at the market share of various regions Download the PDF Sample

The single use segment accounted for USD 4.54 billion in 2018. Hospitals and ambulatory surgical centers use these packs in surgical involvement, involving surgical waste management, surgical team preparation, and utilization of surgical blades, surgical swabs, sutures, drapes, wound dressings, surgical blades, cardiac catheters, and implants. Medical tourism has further fueled the demand for custom procedure packs, ensuring standardization and sterility in healthcare delivery. Custom procedure packs play a crucial role in infection control, especially in chronic cardiovascular diseases and the aged population. Surgical waste management is essential to minimize contamination risks, and hospitals and surgical centers prioritize this aspect. The surgical team relies on these packs for optimal performance and patient safety during procedures.

Regional Analysis

For more insights on the market share of various regions Download PDF Sample now!

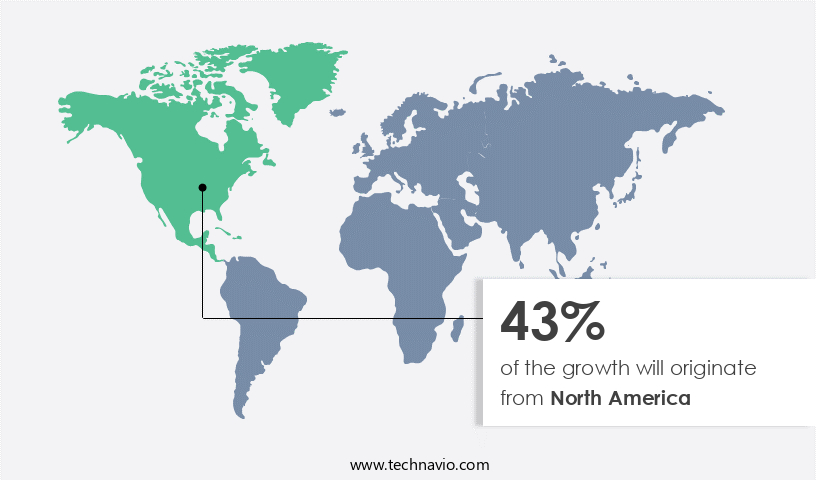

North America is estimated to contribute 43% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The market caters to various chronic diseases and conditions, including cardiovascular and neurovascular diseases, ophthalmic conditions, orthopedic disorders, and wound management. In healthcare settings, custom procedure packs are essential for homecare, dental practices, and surgical facilities. These packs include surgical tools, trays, disposables, and reusable kits. Inventory management is crucial in healthcare to ensure the availability of essential supplies during surgical procedures. Breakthrough medicines and medical tourism have increased the demand for custom procedure packs in hospitals and ambulatory surgical centers.

Further, minimally invasive and noninvasive procedures require precise surgical involvement, and custom procedure packs facilitate efficient execution. Surgical waste management is a critical aspect of healthcare, with hospitals generating substantial waste during surgical procedures. Custom procedure packs help minimize surgical waste by ensuring the use of necessary supplies only. Surgical gowns, surgical swabs, sutures, drapes, wound dressings, surgical blades, cardiac catheters, and implants are some of the essential components of these packs. Surgical teams rely on custom procedure packs to maintain sterility and reduce the risk of cross-contamination during surgeries.

Segment Overview

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million " for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type Outlook

- Single use

- Reusable

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also interested in below market reports

Market Analyst Overview:

Custom Procedure Packs (CPPs) have become an integral part of the healthcare industry, particularly in medical settings where chronic diseases such as cardiovascular conditions and neurovascular conditions are prevalent. These packs consist of essential surgical tools, trays, disposables, and reusable kits required for various procedures, including homecare settings, dental practices, and hospitals. The market is vast and diverse, catering to various medical specialties such as orthopedics, ophthalmology, and wound management. The orthopedic segment, in particular, is expected to witness significant growth due to the increasing prevalence of bone diseases in the geriatric population and the rise in minimally invasive procedures. In healthcare facilities, CPPs play a crucial role in infection control protocols, ensuring the surgical team is well-equipped with personal protective equipment (PPE), surgical gowns, surgical swabs, sutures, drapes, and wound dressings.

Moreover, the adoption of breakthrough medicines and medical tourism has further fueled the demand for custom procedure packs. The market for Custom Procedure Packs is segmented based on the type of procedures, including surgical and noninvasive. Surgical procedures involve the use of surgical tools, trays, implants, cardiac catheters, and disposables. In contrast, noninvasive procedures require fewer supplies, primarily consisting of PPE and disposables. Hospitals and ambulatory surgical centers are the primary consumers of custom procedure packs. The increasing surgical involvement in chronic cardiovascular diseases and the aged population further boosts the demand for these packs. Additionally, the adoption of infection control protocols and the rise in minimally invasive procedures have led to an increase in the usage of custom procedure packs in healthcare settings. In conclusion, the market for Custom Procedure Packs is expected to grow significantly due to the increasing prevalence of chronic diseases, the aging population, and the adoption of minimally invasive procedures. The market is highly competitive, with key players including Stryker, Medtronic, and Ethicon, among others, competing on the basis of product innovation, pricing, and distribution networks.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

131 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 2.01 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

4.23 |

|

Regional analysis |

North America, Asia, Europe, and Rest of World (ROW) |

|

Performing market contribution |

North America at 43% |

|

Key countries |

US, China, UK, Canada, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

3M Co., B.Braun SE, Cardinal Health Inc., Kimal Group, Hubei Medlink Healthcare Co. Ltd., Med-italia Biomedica Srl, Multigate Medical Products Pty Ltd., Medtronic Plc, Molnlycke Health Care AB, Owens and Minor Inc., Priontex, Thermo Fisher Scientific Inc., and Unisurge International Ltd |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behavior

- Growth of the market across North America, Asia, Europe, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

RIA -

RIA -