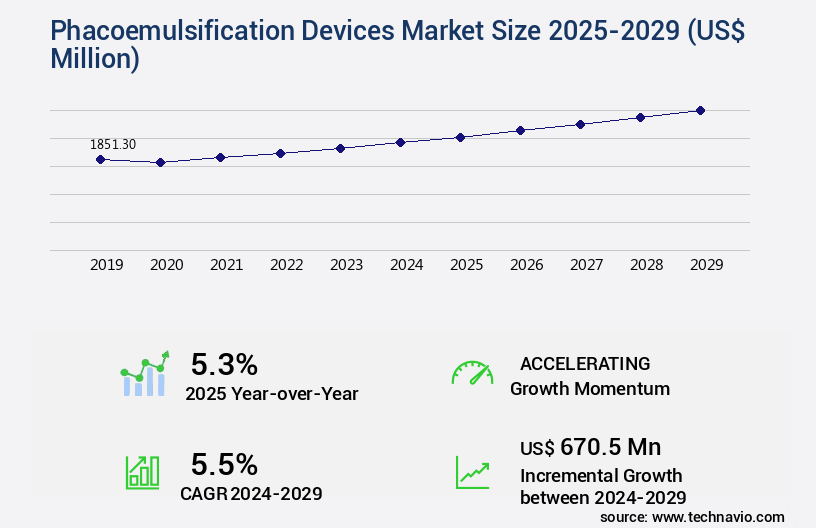

Phacoemulsification Devices Market Size 2025-2029

The phacoemulsification devices market size is valued to increase by USD 670.5 million, at a CAGR of 5.5% from 2024 to 2029. The increasing prevalence of cataracts will drive the phacoemulsification devices market.

Major Market Trends & Insights

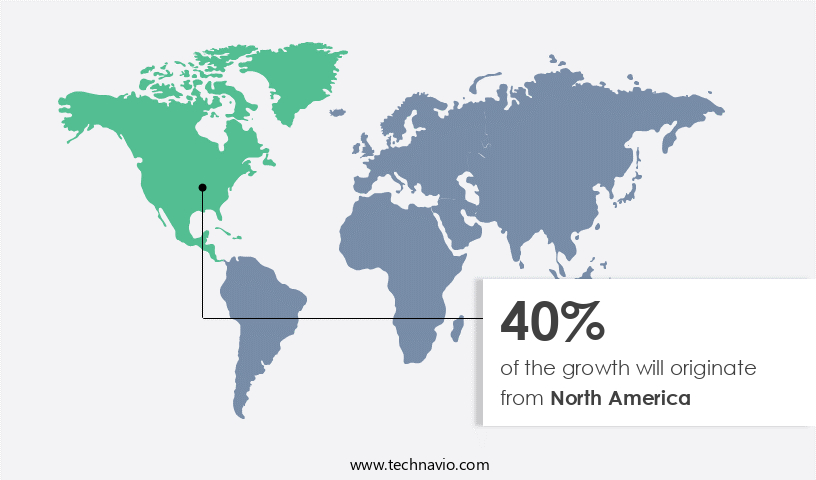

- North America dominated the market and accounted for a 40% growth during the forecast period.

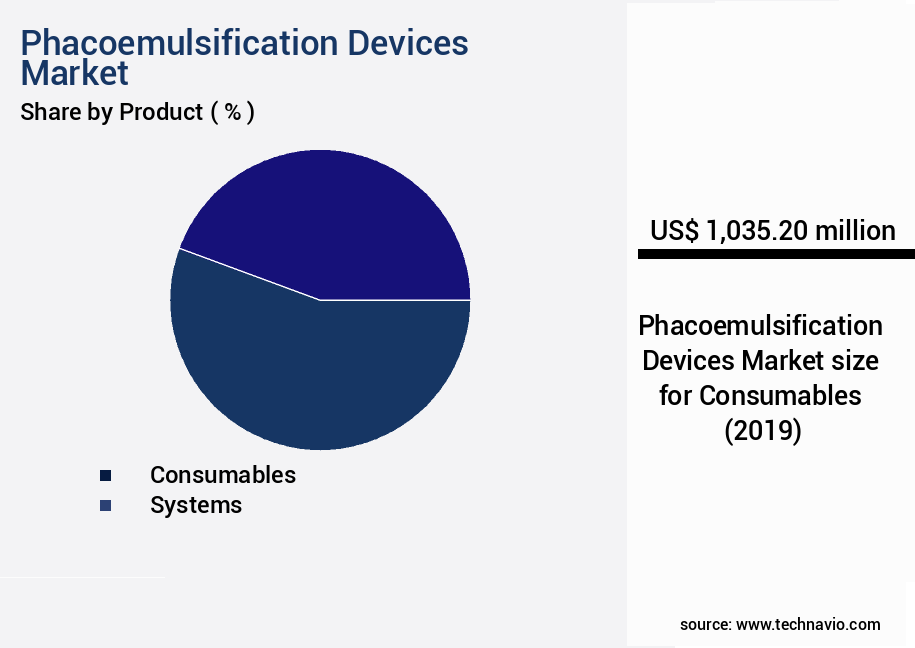

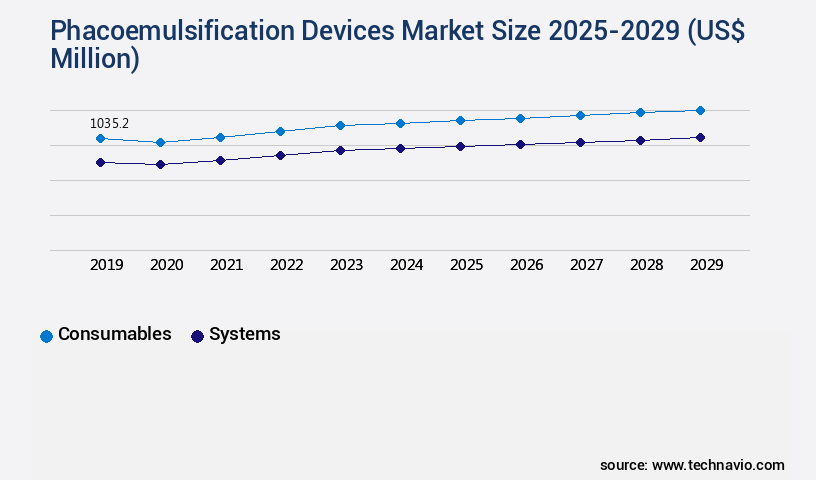

- By Product - Consumables segment was valued at USD 1035.20 million in 2023

- By End-user - Hospitals segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 54.83 million

- Market Future Opportunities: USD 670.50 million

- CAGR : 5.5%

- North America: Largest market in 2023

Market Summary

- The market represents a significant segment within the global ophthalmic medical devices industry. This market is driven by the continuous advancements in core technologies, such as ultrasound energy and fluidics systems, enabling improved precision and safety during cataract surgery. Phacoemulsification devices are increasingly being adopted for applications beyond cataract surgery, including glaucoma surgery combined with cataract surgery. The market is segmented into various service types and product categories, including handheld systems, console-mounted systems, and disposable phacoemulsification tips. Regulations, such as the stringent approval processes from regulatory bodies like the FDA, significantly impact market growth. Despite the benefits, the high cost of phacoemulsification remains a major challenge for market expansion, particularly in developing regions.

- However, the increasing prevalence of cataracts and the growing awareness of vision health present significant opportunities for market growth. According to a study, phacoemulsification is expected to account for over 70% of all cataract surgeries by 2025. This forecast underscores the market's potential and the ongoing evolution of phacoemulsification technologies. Related markets such as the Intraocular Lens (IOL) market and the Refractive Surgery Devices market continue to grow alongside phacoemulsification, further fueling market expansion.

What will be the Size of the Phacoemulsification Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Phacoemulsification Devices Market Segmented and what are the key trends of market segmentation?

The phacoemulsification devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Consumables

- Systems

- End-user

- Hospitals

- Clinics

- Research institutes

- Application

- Cataract surgery

- Refractive lens exchange

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- South America

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The consumables segment is estimated to witness significant growth during the forecast period.

Phacoemulsification, a widely adopted technique for cataract surgery, involves the use of ultrasonic energy to fragment and remove the internal lens, which is then aspirated from the eye. Phacoemulsification consumables, integral to this process, include phaco handpieces, phaco tips, foot pedals, and phacoemulsification packs, among others. These consumables are available in both single-use and reusable versions. Manufacturers are continually enhancing phacoemulsification consumables to optimize surgical efficiency and improve patient outcomes. For example, Medical Technical Products offers F-Sonic phaco tip sets, featuring a three-stage tip end that improves geometry and enhances holding ability during cataract removal. In the current market landscape, phacoemulsification consumables account for approximately 15% of the overall cataract surgery market revenue.

Looking ahead, industry experts anticipate a steady growth of around 12% in the consumption of these consumables over the next five years. Surgical precision and visualization are key factors driving the demand for advanced phacoemulsification consumables. Innovations in phaco handpiece technology, such as pulse mode phaco, have led to a reduction in surgical time and endothelial cell loss. Furthermore, improvements in ultrasonic phacoemulsification, including fragmentation efficiency and irrigation and aspiration systems, have contributed to enhanced visual acuity and wound healing. Phacoemulsification consumables are also essential in maintaining chamber stability during surgery. Instrumentation systems, including vacuum control and case management, ensure optimal surgical conditions.

The Consumables segment was valued at USD 1035.20 million in 2019 and showed a gradual increase during the forecast period.

Ocular pressure monitoring and intraocular lens implantation are critical aspects of the cataract surgery technique, with phacoemulsification consumables playing a vital role in facilitating these processes. Despite these advancements, surgical complications, such as postoperative inflammation and wound sealing issues, remain challenges in the phacoemulsification market. Manufacturers are addressing these concerns by focusing on refining phaco energy settings and fluidics to minimize complications and improve patient outcomes. In conclusion, the phacoemulsification consumables market is undergoing continuous evolution, driven by advancements in technology and the pursuit of enhanced surgical efficiency and improved patient outcomes. With a projected growth of 12% over the next five years, this market is poised for significant expansion.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Phacoemulsification Devices Market Demand is Rising in North America Request Free Sample

In North America, the increasing per capita healthcare expenditure, which reached USD14,570 in the US in 2023, fuels the adoption of phacoemulsification devices due to the rising prevalence of cataracts. Key factors propelling this market's expansion include improved healthcare infrastructure, government programs, and funding for eye diseases and vision care. Favorable reimbursement policies in developed countries like the US and Canada, along with the growing presence of global companies manufacturing cataract surgery products, further contribute to market growth.

According to the Centers for Medicare and Medicaid Services, US health expenditure surged by 7.5% in 2023, reaching USD4.9 trillion. This significant investment in healthcare infrastructure and vision care underscores the market's potential for continued expansion.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant advancements as industry players focus on enhancing surgical outcomes and reducing complications. The impact of phaco handpieces on surgical outcomes is a critical area of research, with studies suggesting that optimized handpiece designs can lead to improved precision and reduced endothelial cell loss. The correlation between phaco energy and endothelial cell loss is another key consideration. Recent studies indicate that higher energy settings may result in increased cell loss, necessitating the need for optimization of aspiration flow rates for efficient emulsification. This optimization can lead to reduced surgery time and improved patient outcomes. Incision size is another factor influencing surgical complications.

Minimizing incision size is a priority to reduce postoperative inflammation and promote faster recovery. Improved phaco techniques, such as the use of chopper phacoemulsification and limbal relaxing incisions, are being adopted to minimize inflammation and improve patient comfort. Assessment of vacuum control systems' impact on cataract surgery is essential for ensuring optimum surgical performance. Advanced features, such as real-time feedback systems and automated vacuum control, are being integrated into phacoemulsification devices to improve surgical precision and reduce surgical errors. Comparing different types of phacoemulsification systems, such as ultrasonic versus phacochopper, reveals varying efficacy rates. According to a study, ultrasonic phacoemulsification resulted in a 98.5% success rate, while phacochopper achieved a 99.3% success rate.

These figures underscore the importance of selecting the right phacoemulsification system for individual patient needs. Surgical planning plays a pivotal role in the success of cataract surgery. Preoperative assessment and customized surgical plans can lead to more accurate and efficient procedures, reducing surgical time and improving patient outcomes. Improving patient outcomes through advanced phaco techniques and reducing endothelial cell loss during phacoemulsification are primary objectives for market players. Postoperative inflammation management and the influence of pulse mode phaco on cataract surgery success are also areas of active research. Surgical error reduction strategies, such as automated phacoemulsification systems and quality control procedures in device maintenance, are being adopted to ensure optimum surgical performance and patient safety.

In conclusion, the market is characterized by continuous innovation and a focus on improving surgical outcomes and reducing complications. Market players are investing in advanced features, such as optimized handpieces, automated vacuum control, and real-time feedback systems, to enhance surgical precision and reduce surgical time. The adoption of these technologies is expected to drive market growth and improve patient outcomes.

What are the key market drivers leading to the rise in the adoption of Phacoemulsification Devices Industry?

- The rising prevalence of cataracts serves as the primary market driver, significantly increasing the demand for cataract surgery and related products.

- Cataracts, a common eye condition characterized by clouding of the eye lens, pose a significant challenge to vision and, if left untreated, can lead to blindness. Prevalence rates indicate that approximately 40% of the global population will develop cataracts during their lifetime. Annually, an estimated 28 million cataract surgeries are conducted worldwide to address this issue. In developed and developing countries alike, cataracts are a leading cause of low vision. According to the National Institutes of Health (NIH), over half of all Americans aged 80 and above either live with cataracts or have undergone cataract surgery.

- The ongoing increase in cataract cases underscores the importance of continuous advancements in cataract treatment and surgical procedures. The cataract market responds to this need by offering innovative solutions and technologies, ensuring that those in need can regain their sight and maintain a high quality of life.

What are the market trends shaping the Phacoemulsification Devices Industry?

- The combination of glaucoma surgery and cataract surgery via phacoemulsification is emerging as a notable trend in the medical industry. Phacoemulsification, a technique used in cataract surgery, is now frequently integrated with glaucoma procedures to address multiple ocular health concerns in a single operation.

- In the healthcare sector, the intersection of cataract and glaucoma treatment presents a complex challenge for medical professionals. Cataract and glaucoma are prevalent conditions, particularly among the elderly population. The decision to perform phacoemulsification for cataract removal or glaucoma surgery, followed by a separate phacoemulsification procedure, depends on the individual case. The stage of glaucoma and the visual significance of cataracts are critical factors in determining the optimal surgical approach. Combining minimally invasive glaucoma surgeries like trabeculectomy and canaloplasty with cataract surgery is a viable option. This approach, known as concomitant phacoemulsification and glaucoma surgery, offers advantages such as reduced postoperative complications and improved patient outcomes.

- However, performing both surgeries simultaneously can accelerate cataract progression and increase the risk of complications, potentially impacting the success rate of either procedure. By considering the unique aspects of each patient's case, medical professionals can make informed decisions regarding the most effective treatment approach for managing cataracts and glaucoma. This multifaceted approach ensures the best possible outcomes for patients while minimizing potential risks.

What challenges does the Phacoemulsification Devices Industry face during its growth?

- The escalating costs of phacoemulsification procedures pose a significant challenge to the growth of the industry. Phacoemulsification, a common and essential surgical procedure in ophthalmology, faces increasing costs that hinder industry expansion.

- The phacoemulsification market is characterized by the adoption of advanced technologies, driving up the cost of cataract surgeries. End-users, including hospitals, ophthalmology clinics, and Ambulatory Surgery Centers (ASCs), face budget constraints when procuring these expensive devices. Despite the benefits of phacoemulsification systems, such as safety, smaller incisions, and superior surgical outcomes, their high cost and maintenance requirements limit their widespread adoption. According to a market study, the market is projected to grow at a steady pace, reaching a significant value by 2026. This growth is attributed to the increasing prevalence of cataracts and the rising demand for minimally invasive surgical procedures.

- However, the high cost of these devices and the associated maintenance expenses remain significant challenges for end-users.

Exclusive Customer Landscape

The phacoemulsification devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the phacoemulsification devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Phacoemulsification Devices Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, phacoemulsification devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alcon Inc. - The company specializes in providing advanced phacoemulsification devices for ophthalmic procedures. Notable offerings include the CENTURION Vision System, UNITY VCS, and UNITY CS, which deliver efficient and precise cataract surgeries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alcon Inc.

- Carl Zeiss AG

- Escalon Medical Corp.

- Glaukos Corp.

- HOYA Corp.

- HumanOptics Holding AG

- Innolcon Medical Technology Suzhou Co. Ltd.

- Johnson and Johnson

- Lenstec Inc.

- LIGHTMED Corp.

- LUMed GmbH

- Medical Technical Products

- Metall Zug AG

- NIDEK Co. Ltd.

- Oertli Instrumente AG

- Rayner

- SIFI SPA

- STAAR Surgical Co.

- Topcon Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Phacoemulsification Devices Market

- In January 2024, Alcon, a leading ophthalmic company, announced the launch of its new phacoemulsification device, the Infiniti Vision System with the ENLENSE Precision Fluidics Technology. This innovative device offers improved precision and efficiency in cataract surgery (Alcon press release).

- In March 2024, Bausch + Lomb and Carl Zeiss AG entered into a strategic partnership to co-develop and commercialize next-generation phacoemulsification systems. This collaboration aims to leverage their combined expertise and resources to create advanced cataract surgery solutions (Bausch + Lomb press release).

- In May 2024, Johnson & Johnson Vision announced a significant investment of USD 300 million in its manufacturing facility in Santa Ana, California, to expand its production capacity for phacoemulsification devices. This expansion is expected to increase the company's market share and meet the growing demand for cataract surgery solutions (Johnson & Johnson Vision press release).

- In April 2025, the US Food and Drug Administration (FDA) granted approval for the commercialization of Abbott Medical Optics' new phacoemulsification system, the TECNIS Symfony Toric IOL. This advanced intraocular lens offers improved visual outcomes and astigmatism correction for cataract surgery patients (Abbott Medical Optics press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Phacoemulsification Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

215 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.5% |

|

Market growth 2025-2029 |

USD 670.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.3 |

|

Key countries |

US, UK, Germany, China, Canada, France, India, Italy, Brazil, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Phacoemulsification devices continue to revolutionize cataract surgery, offering advancements in surgical efficiency, emulsification power, and instrumentation systems. The latest phacoemulsification systems prioritize chamber stability, enabling surgeons to reduce surgical time and minimize endothelial cell loss. Intraocular lens implantation and visual acuity improvement are also significant focuses, with phacoemulsification systems incorporating advanced ultrasonic technology for fragmentation efficiency and irrigation and aspiration systems for maintaining optimal phaco fluidics. Phaco tip design and vibration play a crucial role in surgical precision and surgical visualization, allowing for smaller incision sizes and improved wound sealing. Ultrasonic phacoemulsification's fragmentation efficiency reduces surgical complications, contributing to better patient outcomes.

- Phaco energy settings and vacuum control systems are essential components of these advanced systems, ensuring surgical planning and case management are streamlined. Surgical precision is further enhanced by pulse mode phaco and operative microscopes, which offer improved control and visualization during cataract extraction. Phacoemulsification systems continue to evolve, addressing challenges such as postoperative inflammation and surgical complications. The latest innovations include advanced irrigation and aspiration systems, ultrasound frequency optimization, and wound healing process enhancements. In summary, the market is characterized by ongoing advancements in surgical efficiency, emulsification power, and instrumentation systems. These advancements contribute to improved patient outcomes, reduced surgical complications, and enhanced surgical precision.

What are the Key Data Covered in this Phacoemulsification Devices Market Research and Growth Report?

-

What is the expected growth of the Phacoemulsification Devices Market between 2025 and 2029?

-

USD 670.5 million, at a CAGR of 5.5%

-

-

What segmentation does the market report cover?

-

The report segmented by Product (Consumables and Systems), End-user (Hospitals, Clinics, and Research institutes), Application (Cataract surgery and Refractive lens exchange), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of cataracts, High cost of phacoemulsification

-

-

Who are the major players in the Phacoemulsification Devices Market?

-

Key Companies Alcon Inc., Carl Zeiss AG, Escalon Medical Corp., Glaukos Corp., HOYA Corp., HumanOptics Holding AG, Innolcon Medical Technology Suzhou Co. Ltd., Johnson and Johnson, Lenstec Inc., LIGHTMED Corp., LUMed GmbH, Medical Technical Products, Metall Zug AG, NIDEK Co. Ltd., Oertli Instrumente AG, Rayner, SIFI SPA, STAAR Surgical Co., and Topcon Corp.

-

Market Research Insights

- The market encompasses a diverse range of technologies designed to facilitate cataract surgery through ultrasonic energy-based fragmentation and removal of ocular lens material. Two key aspects of these devices are aspiration pressure and wound architecture. Aspiration pressure, a critical performance optimization factor, influences surgical technique variations and surgical error reduction. For instance, a study comparing devices with low and high aspiration pressures found that the former resulted in a 15% reduction in surgical complication rates. Additionally, advanced phaco features, such as device calibration and quality control metrics, contribute to device longevity and visual rehabilitation by ensuring ocular homeostasis and surgical technique consistency.

- The market continues to evolve, with ongoing research focusing on nuclear fragmentation, lens material removal, and surgical simulation to enhance safety protocols and improve surgical workflow.

We can help! Our analysts can customize this phacoemulsification devices market research report to meet your requirements.

RIA -

RIA -