Dairy Alternative Plant Milk Beverages Market Size 2024-2028

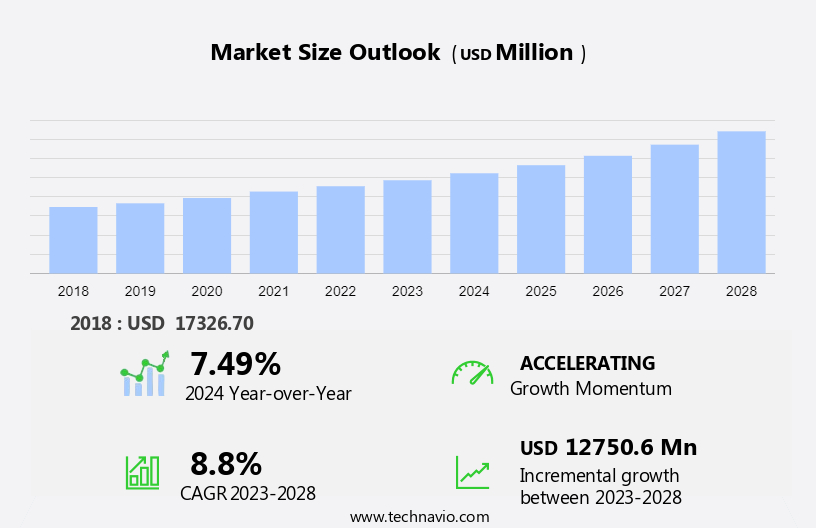

The dairy alternative plant milk beverages market size is forecast to increase by USD 12.75 billion at a CAGR of 8.8% between 2023 and 2028.

- The market is witnessing growth due to the increasing demand for plant-based milk as an alternative to traditional dairy products. This trend is driven by the rising health consciousness among consumers and the growing number of lactose intolerant and vegan populations. Furthermore, frequent product innovation and the launch of new flavors and varieties are also fueling market growth. However, the market faces challenges such as the presence of allergens in plant-based sources like soy, almond, and coconut, which may limit its consumer base. To mitigate this challenge, companies are focusing on producing allergen-free plant-based milk beverages using alternative sources like organic rice, oat, and hemp. Overall, the market is expected to continue its growth trajectory due to these factors.

What will the size of the market be during the forecast period?

- Dairy alternatives have gained significant popularity in recent years due to various health, ethical, and environmental concerns. These plant-based milk beverages cater to individuals with lactose intolerance, vegetarian and flexitarian diets, and those following veganism. Cholesterol concerns, personal health, animal welfare, and environmental issues are key drivers for the market's growth. Almond milk, one popular alternative, is free from cholesterol and suitable for those with nut allergies, but its production has high carbon and greenhouse gas emissions.

- Soy milk, another common alternative, is rich in proteins and can cause allergic reactions in some individuals due to soy lecithin and soybean oil. Moreover, proactive measures are being taken to address food allergens and sensitivities, ensuring the production of safe and high-quality dairy alternatives. Despite these challenges, the market for dairy alternatives continues to expand, driven by the growing number of individuals seeking healthier and more sustainable options.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

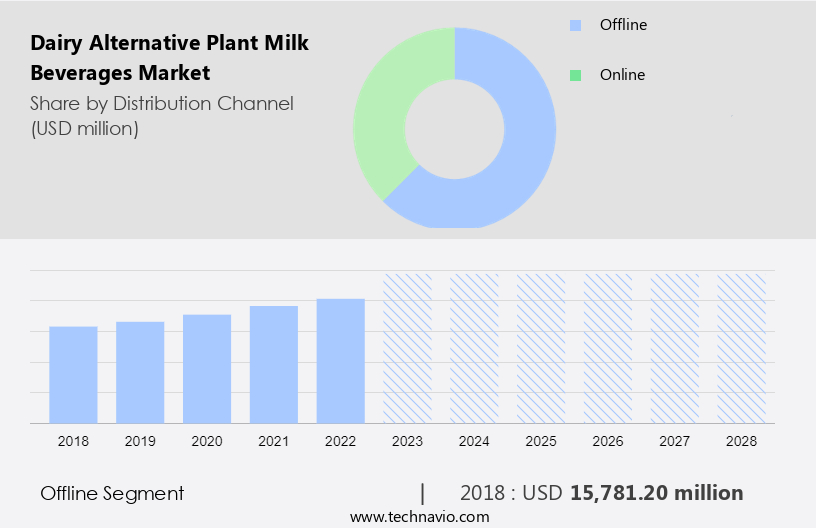

- Distribution Channel

- Offline

- Online

- Source

- Almond milk

- Soy milk

- Rice milk

- Coconut milk

- Others

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- UK

- North America

- US

- South America

- Middle East and Africa

- APAC

By Distribution Channel Insights

- The offline segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to increasing health consciousness and dietary preferences. Consumers are increasingly turning to plant-based milk beverages as alternatives to dairy products for various reasons, including lactose intolerance, cholesterol concerns, and ethical considerations such as vegetarian and flexitarian diets, as well as veganism. These beverages offer solutions for individuals with food allergies or sensitivities to dairy, nuts, soy, or other common food allergens. Environmental concerns, such as carbon emissions and greenhouse gas emissions from animal agriculture, also contribute to the market's growth. Plant-based milk beverages, particularly those derived from almonds, rice, and other sources, offer nutritional value with essential nutrients like calcium, casein, proteins, and phytochemicals.

Moreover, isoflavones, found in soy milk, have been linked to heart disease prevention and breast cancer recurrence. The offline segment holds the largest market share due to consumers' preference for checking product quality and specifications before purchasing. Offline distribution channels include hypermarkets, supermarkets, convenience stores, and other discount stores. companies are expanding their product reach by collaborating with retailers to showcase innovative plant-based milk beverages.

Get a glance at the market report of share of various segments Request Free Sample

The offline segment was valued at USD 15.78 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

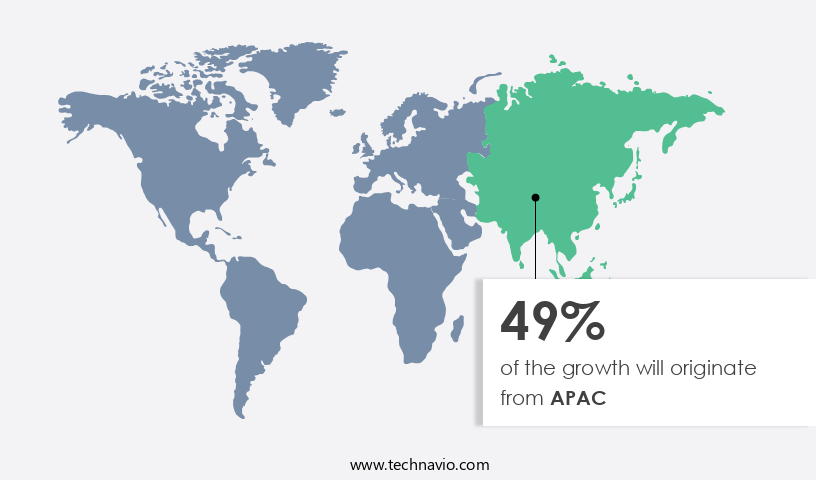

- APAC is estimated to contribute 49% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Plant milk beverages, a popular alternative to traditional dairy products, are increasingly gaining traction in online stores. These non-dairy options cater to various dietary preferences and intolerances, including lactose intolerance, veganism, and those seeking a healthier choice. Online retailers offer a wide array of plant milk beverages derived from sources such as soy, almond, oat, rice, and coconut. Consumers can easily access and purchase these beverages from the comfort of their homes, with options for quick delivery and subscription services. The convenience and accessibility of online stores have contributed significantly to the growth of the plant milk beverages market.

Additionally, the growing awareness of the environmental impact of the dairy industry, including greenhouse gas emissions and water usage, has led to a trend towards more sustainable plant-based milk beverages. These alternatives are not only preferred for their health benefits but also for their versatility. Plant-based milk beverages are rich in essential nutrients such as fiber, protein, vitamins, and minerals like iron and magnesium. They are also suitable for various dietary needs, including those following a ketogenic or vegan diet. Furthermore, plant-based milk is used in various food and beverage applications, as well as in skin care products. Manufacturers of plant-based milk beverages are focusing on ethical practices and transparency in their production processes.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Dairy Alternative Plant Milk Beverages Market ?

Strong demand for plant-based milk is the key driver of the market.

- The preference for dairy alternative beverages, specifically plant-based milk, has witnessed significant growth in recent years. Consumers are increasingly aware of their dietary choices and the environmental consequences of animal agriculture, leading them to explore options beyond traditional cow's milk. Individuals with lactose intolerance or dairy allergies find solace in plant-based milk as a viable substitute. Moreover, the health benefits associated with these beverages, such as lower saturated fat and cholesterol levels, attract those seeking to minimize their consumption of animal products. Environmental concerns, including the environmental footprint of animal agriculture, have influenced many to adopt plant-based milk. These beverages often contain essential minerals like phosphorus, zinc, copper, and manganese, as well as vitamins such as Vitamin E and Vitamin D.

- Some popular plant-based milk options, like rice milk and hemp milk, also provide Vitamin B12, an essential nutrient often lacking in vegan diets. Carbohydrates in plant-based milk contribute to a healthy immune system, while Vitamin E supports healthy skin, hair, and nails. Organic forms of plant-based milk offer additional health benefits, ensuring the absence of synthetic additives. Popular plant-based milk varieties include rice milk, hemp milk, cashew milk, and coconut milk. As consumers continue to prioritize health and sustainability, the demand for these alternatives to dairy milk is expected to persist.

What are the market trends shaping the Dairy Alternative Plant Milk Beverages Market?

Frequent product innovation and launch is the upcoming trend in the market.

- The dairy alternative plant-milk beverage market in the United States is experiencing significant growth due to the increasing preference for ethical and vegan options among the millennial population. This demographic is increasingly concerned about animal welfare and is opting for dairy-free alternatives. In response, companies are introducing new product lines to cater to this demand. For instance, Danone invested USD22 million in new health and wellness initiatives, which included the reformulation of 70% of its plant-based drinks portfolio in October 2022. This trend is expected to continue, with frequent product launches driving market growth during the forecast period. Consumers can easily access these dairy-alternative beverages through various channels, including convenience stores and online stores.

What challenges does Dairy Alternative Plant Milk Beverages Market face during the growth?

Increasing allergies to plant-based sources is a key challenge affecting the market growth.

- Plant milk beverages, derived from sources such as almonds, soy, cashews, hemp, and coconut, have gained significant popularity among consumers seeking dairy alternatives for various reasons. These reasons include dietary needs, ethical considerations, and health benefits. Some consumers prefer these beverages due to their association with strong heart health and strong bones. Others use them for arthritis treatment or weight loss. The older population and breast cancer survivors also find beverage options like almond, soy, and rice milk beneficial. Flavored beverages, such as vanilla or chocolate almond milk, are popular choices for those seeking taste variety. Unflavored and low calorie plant milk beverages are preferred by those looking for plain dairy alternatives.

- Sour creams and regular cheese alternatives made from these plant milks are also available in the market. Hemp milk, cashew milk, and coconut milk are popular choices for desserts. Allergies to soy and tree nuts like almonds are potential limitations to the growth of the plant-based milk industry. Soy allergies occur when the immune system mistakenly identifies the proteins in soy as harmful and produces antibodies to fight them. While severe reactions to soy are rare, individuals with asthma or allergies to other foods, including peanuts, are more susceptible. In conclusion, plant milk beverages offer a range of benefits and cater to diverse consumer preferences.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adisoy Foods and Beverages Pvt. Ltd.

- ALT. MILK

- Arla Foods amba

- Califia Farms LLC

- Campbell Soup Co.

- Celebes Coconut Corp.

- Dairy Farmers of America Inc.

- DANA Dairy Group Ltd.

- Danone SA

- Drupe Foods India Pvt. Ltd.

- Eden Foods Inc.

- Goodmylk

- LEMONCONCENTRATE SLU

- MALK Organics

- Midas Soy Nutritions

- Nestle SA

- SAP Agrotech Pvt. Ltd.

- Soyfoods USA

- SunOpta Inc.

- The Hershey Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Dairy alternatives have gained significant popularity in recent years due to various health, ethical, and environmental concerns. These plant-based milk beverages cater to individuals with lactose intolerance, vegetarian and flexitarian diets, and those following veganism. Cholesterol concerns, food allergies, and sensitivities are major drivers for the shift towards dairy alternatives. Almond milk, for instance, is a popular choice for those with nut allergies, while soy milk is suitable for those with lactose intolerance, provided they do not have soy allergies or sensitivities to soybean oil or lecithin. Environmental issues, including carbon emissions and greenhouse gas emissions, have also contributed to the growth of the dairy alternative market.

Moreover, plant-based milk beverages offer a more sustainable alternative to traditional dairy products. Personal health concerns, such as immune responses, hives, and anaphylaxis, have led consumers to take proactive measures and opt for dairy alternatives. Proteins, calcium, and essential nutrients like isoflavones, genistein, and phytochemicals are present in various dairy alternatives, making them a healthier option for those at risk of heart disease or breast cancer recurrence. Cold climatic conditions may affect the nutritional value of some plant-based milk beverages, but innovations in production and distribution have mitigated these concerns. Overall, the dairy alternative market continues to grow as consumers prioritize their health, ethical concerns, and environmental sustainability.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.8% |

|

Market growth 2024-2028 |

USD 12.75 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.49 |

|

Key countries |

China, US, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -