Enjoy complimentary customisation on priority with our Enterprise License!

The Data Center Power Market is estimated to grow by USD 20,569.77 million at a CAGR of 11.1% between 2022 and 2027. The primary factors boosting the market growth are the increasing investments, the emergence of mini data centers, and the increasing adoption of intelligent PDUs.

To learn more about this report, Request Free Sample

The emergence of mini data centers is a key factor driving the market growth. Mini data centers are self-contained systems designed to accommodate up to 40 rack enclosures, along with small cooling units, and can handle an IT load of up to 250 kW. These compact centers are commonly used as disaster recovery solutions for branch offices. The growing popularity can be attributed to the need for cost-effective infrastructure, the rise of small and medium enterprises (SMEs), and the efficient management of edge data resources.

The market, valued at USD 1.87 billion in 2016, is projected to reach USD 4.13 billion by 2021, with a CAGR of 17.17%. Companies like Amazon Web Services have introduced mini centers in various cities worldwide to improve cloud service accessibility. As the adoption of mini centers increases, the demand for IT infrastructure, including storage, servers, and networking solutions, will also rise, leading to a greater need for reliable power supply solutions such as UPS and rack PDUs during the forecast period. These advancements are expected to fuel the market growth and trends in the foreseeable future.

An increase in strategic investments and partnerships is a key trend boosting the market. Companies are opting for strategic partnerships and collaborations with market companies, including other component providers, for product development and geographical expansion. It also enables companies to explore new opportunity areas for products and services and generate revenue through sales of their products to operators.

Below are some examples of strategic partnerships and collaborations by companies in the market in focus:

Thus, increasing strategic partnerships and alliances between companies are expected to lead to numerous product-level innovations. They will also accelerate the demand during the forecast period.

Focus on the consolidation of data centers is a major challenge hindering the market. Data center consolidation refers to the process of reducing the size of a single facility or merging multiple facilities to cut down operating expenses. Enterprises undertake consolidation for various reasons, including expanding market shares through acquisitions in different regions. According to the US National Resources Defense Council, data center operators in the US were projected to spend up to USD 13 billion annually on electricity by 2020. However, through consolidation, electricity costs can be reduced by 30%-50%. Consequently, many government agencies worldwide are closing data centers to achieve cost savings. For instance, the US government closed 12,062 data centers in May 2018 and plans to close 1,200 more by 2023, resulting in USD 3.6 billion in savings from cloud consolidation.

Enterprises are also embracing virtualization and Infrastructure as a Service (IaaS) to further consolidate their centers and minimize operational expenses. As a result, some software companies are adopting a common cloud platform to avoid the need for individual centers. These trends are expected to impede the global market in the forecast period.

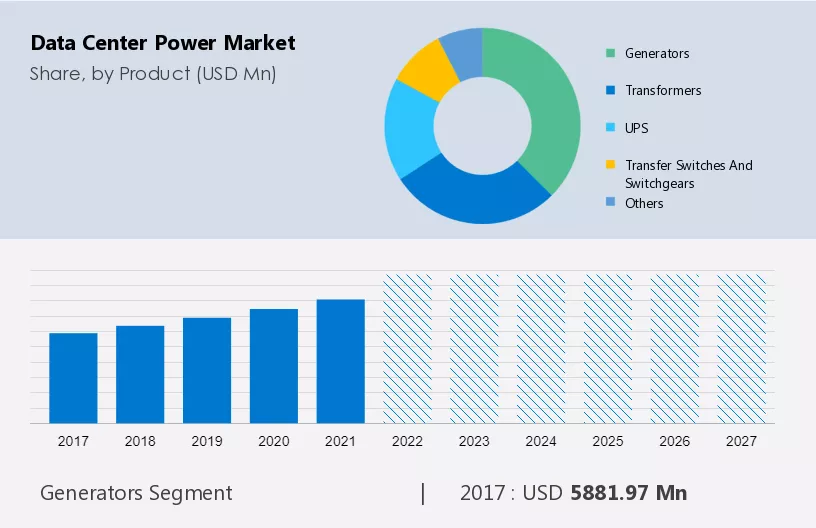

The market share growth by the generators segment will be significant during the forecast period. A generator is a machine that converts mechanical energy into electrical energy to serve as a power source for other machines. In centers, generators are used as backup power supplies when the primary power supply is lost.

Get a glance at the market contribution of various segments Request a PDF Sample

The generators segment showed a gradual increase in market share from USD 5,881.97 million in 2017 and continued to grow by 2021. A generator can be selected based on the backup time and power required for a data center during a power outage. Enterprises should have an in-depth understanding of the power system architecture of their centers before installing a generator at the facility. Based on the fuel source, generators are majorly classified into gas, diesel, and bi-fuel power generators. Enterprises can choose generators based on the fuel option (diesel or gas), which will help them reduce the operating costs associated with generators. A UPS system can act as an alternative option for generators; however, it can supply power for only a few minutes.

Therefore, generators are the ideal deployment option for long backup periods. However, companies are launching UPS systems with more backup time, which is spurring the adoption of UPS over generators, as the former is more cost-effective. Such developments are expected to propel the growth of the market in focus during the forecast period. Furthermore, our report provides a brief analysis of the historical and forecast market share and their segments along with the reasons for growth from 2017 to 2027. The growth of this segment is primarily attributed to the increasing adoption of Power components, which is driven by an increase in the global demand for the industry.

For more insights on the market share of various regions Request PDF Sample now!

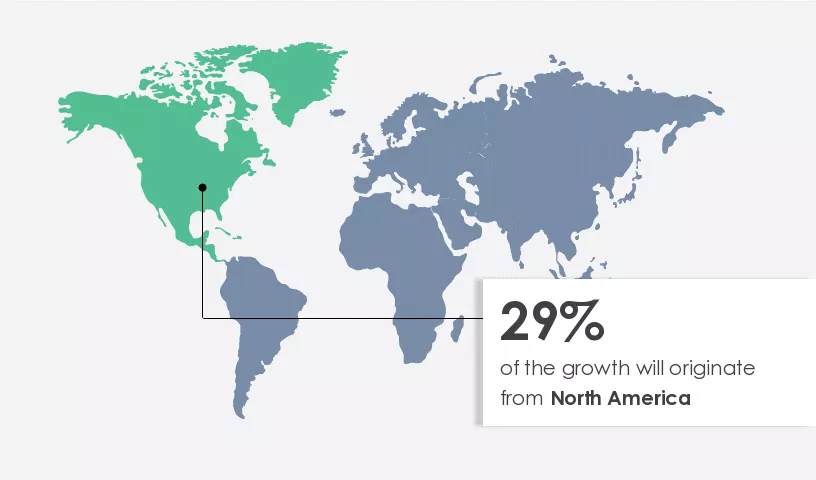

North America is projected to contribute 29% by 2027. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The growing demand for servers in North America is driven by increased investments by hyper-scale cloud providers, colocation service providers, and enterprises. These investments support edge computing, 5G, multi-cloud services, big data analytics, and IoT. The rising adoption of cloud services has also led to an increased demand. Modular UPS is the most popular among all UPS variants due to its high demand. The surge in data traffic from enterprises and consumers, fueled by the implementation of autonomous technologies and AI, has led to the construction of centers in the region. However, concerns over electricity consumption and CO2 emissions are encouraging the use of devices and renewable energy sources like solar and wind energy. These trends are expected to boost the market in the region during the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Active Power - The company offers data center power through the Leansource flywheel. The company designs and manufactures battery-free flywheel uninterruptible power supply (UPS) systems and energy storage products.

The market growth and forecasting report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market research and growth report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Customer Landscape

The Data Center Power Market presents a dynamic landscape driven by the proliferation of mega data centers and hyperscale cloud data centers. With the surge in power-consuming servers and storage devices for cloud computing, operators prioritize greenfield and brownfield facilities with efficient power infrastructure solutions to curb carbon emissions. Hyperscale operators like Cisco and Equinix lead investments in intelligent rack PDU solutions and modular data center deployment. Local benefits include reduced OPEX costs and improved uptime. As demand escalates, vendors like Fujitsu and Tripp Lite by Eaton cater to diverse product categories, emphasizing infrastructure resilience against environmental factors such as shock, vibration, and temperature variations. Mergers and acquisitions reshape the competitive landscape, with Jakarta emerging as a hotspot for International Business Exchange (IBX) data centers and Industrial Gigabit Ethernet switches deployment.

The market growth analysis forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and opportunities from 2017 to 2027.

|

Data Center Power Market Scope |

|

|

Market Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.1% |

|

Market growth 2023-2027 |

USD 20,569.77 million |

|

Market structure |

Fragmented |

|

YoY growth (%) |

9.26 |

|

Regional analysis |

North America, Europe, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 29% |

|

Key countries |

US, China, Australia, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ABB Ltd., Active Power Solutions Ltd., AEG Power Solutions BV, Black Box Corp., Caterpillar Inc., Control Technology Co., Cummins Inc., Cyber Power Systems Inc., Danfoss AS, Delta Electronics Inc., Eaton Corp. Plc, Exide Technologies, Generac Holdings Inc., Legrand SA, Panduit Corp., Rolls Royce Holdings Plc, Schneider Electric SE, Siemens AG, Toshiba Corp., and Vertiv Holdings Co. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period |

|

Customization purview |

If our market trends and analysis report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Product

7 Market Segmentation by End-user

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.