Dermatology Diagnostic Devices Market Size 2024-2028

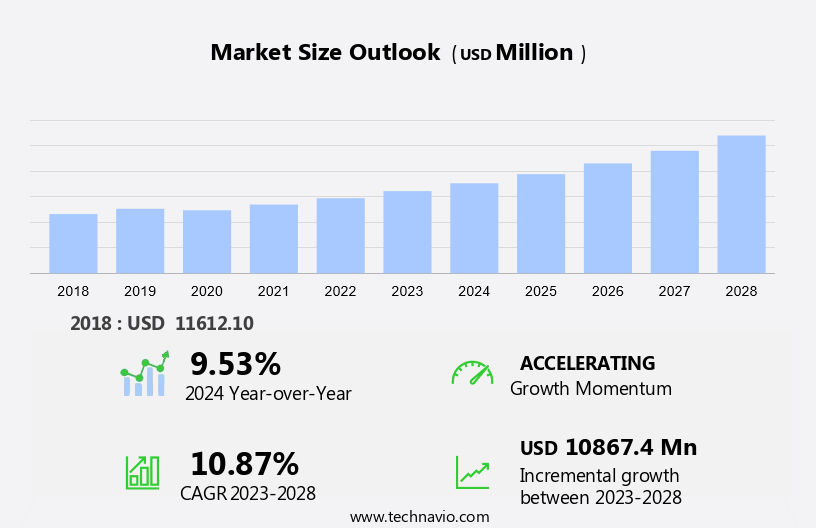

The dermatology diagnostic devices market size is forecast to increase by USD 10.87 billion at a CAGR of 10.87% between 2023 and 2028. The market is experiencing significant advancements, driven by the increasing prevalence of skin diseases such as melanoma and autoimmune conditions. To address the lack of accurate diagnosis and the shortage of skilled technicians, innovative technologies like augmented reality (AR) and virtual reality (VR) are being integrated into diagnostic tools. Spatial computing, which combines AR and VR, enables more precise analysis and diagnosis. Wearable devices, such as smartwatches, patches, and smart clothing equipped with trackers and sensors, are also gaining popularity for the early detection and monitoring of skin conditions. Battery life remains a crucial factor in the adoption of these devices, as prolonged usage is essential for effective monitoring. The integration of these advanced technologies into dermatology diagnostic devices is revolutionizing the industry and improving patient outcomes.

The market is witnessing significant growth due to the increasing prevalence of skin disorders and the growing preference for non-invasive diagnostic methods. Dermatologists are increasingly relying on advanced technologies to provide accurate diagnoses and develop effective treatment plans for their patients. Several technology advancements are driving the growth of the market. Infrared imaging, ultrasound, and optical coherence tomography are some of the technologies that are revolutionizing the diagnosis and treatment of various skin conditions. These technologies enable early detection and diagnosis of skin disorders, leading to better treatment outcomes.

Furthermore, demographic trends, such as an aging population and rising awareness of skin health, are also fueling the demand for dermatology diagnostic devices. According to the American Academy of Dermatology, over 90% of Americans will develop a skin condition at some point in their lives. Moreover, the increasing prevalence of chronic diseases and lifestyle-related disorders, such as cardiovascular diseases and diabetes, are leading to an increased focus on preventive healthcare and early diagnosis. Smartphone-based healthcare devices are gaining popularity in the market due to their convenience and affordability. These devices use wireless connectivity to transmit patient data to healthcare providers, enabling remote diagnosis and consultation.

Moreover, lifestyle management tools, such as fitness tracking capabilities, wearable activity monitors, and activity trackers, are also being integrated into these devices to provide a holistic approach to patient care. Patient preference for non-invasive diagnostic methods is another factor driving the growth of the market. Non-invasive diagnostic methods, such as infrared imaging and optical coherence tomography, offer several advantages over traditional diagnostic methods, including minimal discomfort, faster results, and improved accuracy. The use of biosensors and mHealth intelligence is also gaining momentum in the market.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

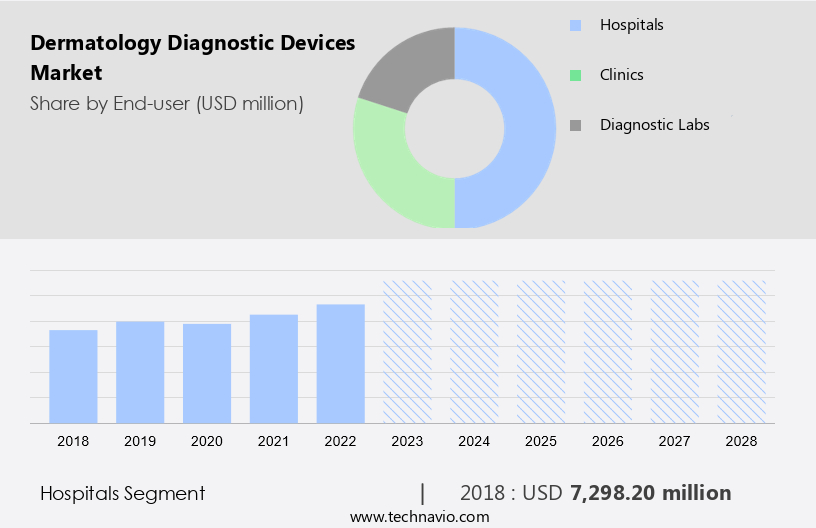

- End-user

- Hospitals

- Clinics

- Diagnostic labs

- Type

- Imaging devices

- Microscopes

- Immunoassays

- Molecular diagnostics

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period. In the market, hospitals are projected to experience notable growth in terms of annual expansion rate compared to clinics and diagnostic labs. These devices offer numerous advantages to hospitals and clinics, including enhanced patient care and satisfaction, streamlined operations at the point of care, and cost savings through improved operational efficiency. In 2023, hospitals emerged as the primary revenue drivers for the market due to the increasing prevalence of skin diseases and the availability of specialized professionals. Consumer-grade and clinical-grade dermatology diagnostic devices are increasingly being adopted for remote patient monitoring and home healthcare applications. MHealth intelligence, activity trackers, and other digital health technologies are transforming the diagnosis and management of chronic diseases and lifestyle-related disorders.

Moreover, hospitals are integrating these advanced tools into their care delivery models to provide personalized and convenient care to patients. The market in North America is expected to expand significantly due to the increasing burden of chronic diseases, growing awareness of early disease detection, and the adoption of digital health technologies. The market is also driven by the presence of major market players, advanced healthcare infrastructure, and favorable reimbursement policies. The market is experiencing steady growth due to the increasing prevalence of skin diseases, the adoption of digital health technologies, and the integration of remote patient monitoring and home healthcare applications.

Furthermore, hospitals are the major revenue contributors to the market due to their ability to provide specialized care and the availability of skilled professionals. In North America, the market is expected to expand significantly due to the increasing burden of chronic diseases, favorable reimbursement policies, and the presence of major market players.

Get a glance at the market share of various segments Request Free Sample

The Hospitals segment was valued at USD 7.29 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

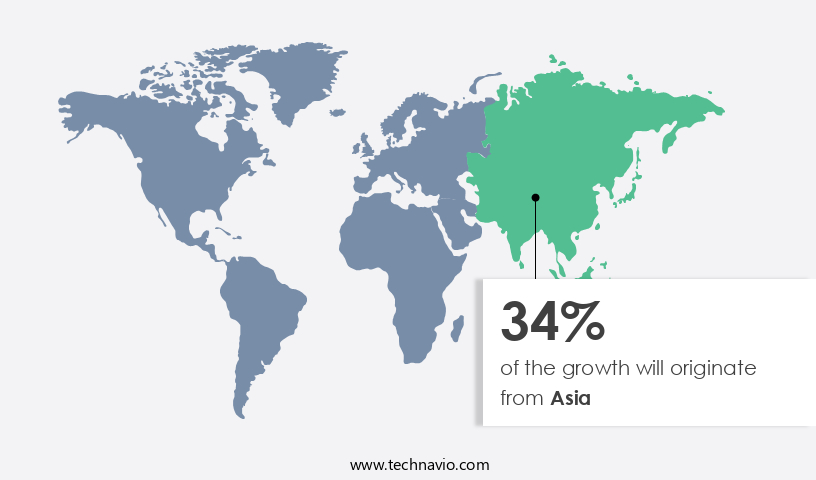

Asia is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the market is experiencing notable expansion due to several factors. The geriatric population is a significant contributor to this growth, as the prevalence of chronic and infectious skin diseases is higher among older adults. In the United States, in particular, there is a growing awareness of the importance of dermatology diagnostic tests among this demographic. Furthermore, the geriatric population is more susceptible to skin cancers, which increases the demand for advanced diagnostic tools Dermatologists rely on advanced technologies, such as infrared imaging, ultrasound, and optical coherence tomography, to provide accurate diagnosis and treatment plans for their patients. Technology advancements continue to shape the market, with patient preference playing a crucial role in driving innovation.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The increasing prevalence of melanoma and autoimmune skin diseases is the key driver of the market. The prevalence of skin disorders and abnormalities is on the rise, leading to an increased demand for accurate and efficient diagnostic tools in the field of dermatology. Skin issues are among the most common health concerns worldwide, surpassing conditions like hypertension, cancer, and obesity in prevalence. Autoimmune skin disorders, which result from the body's abnormal immune response to foreign substances, are a significant contributor to this trend. For instance, psoriasis, an autoimmune skin condition, affects over 3% of the adult population in the United States. Moreover, the rise in aesthetic procedures and the increasing awareness of skin cancers have further fueled the adoption of dermatology diagnostic devices.

Furthermore, tropical countries and regions with high UV radiations exposure are particularly susceptible to skin disorders and skin cancers. Additionally, the advent of smartphone-based healthcare devices is revolutionizing the industry, offering convenience and accessibility to patients.

Market Trends

The emergence of teledermatology in mobile applications is the upcoming trend in the market. Dermatology diagnostic devices have evolved significantly with the integration of advanced technologies such as augmented reality (AR), virtual reality (VR), and spatial computing. These technologies enable more accurate and efficient diagnosis of skin conditions. For instance, AR and VR can provide a more great experience for both doctors and patients, allowing for a more precise analysis of skin lesions. Additionally, battery life, trackers, smartwatches, patches, and smart clothing are essential components of these devices, ensuring continuous monitoring and real-time data transmission. In the US market, teledermatology has gained traction as an alternative to traditional in-person consultations, particularly in underserved areas.

Furthermore, Mobile applications that allow individuals to interact with doctors and share images of their skin conditions have become increasingly popular. The integration of these advanced technologies into dermatology diagnostic devices is set to transform the industry and improve patient outcomes.

Market Challenge

Lack of accurate diagnosis and shortage of skilled technicians is a key challenge affecting the market growth. The diagnostic accuracy of skin diseases poses a significant challenge for healthcare professionals, with many relying on clinical symptoms and physical examinations for diagnoses. While devices such as reflectance confocal microscopy and dermatoscopes have shown improvements in specificity and sensitivity, their reliability is not absolute. For instance, studies have shown that malignant melanomas misdiagnosed by reflectance confocal microscopy were correctly identified by dermatoscopes. This inconsistency in diagnosis results in a low referral rate to specialists and an increased need for more accurate methods. Advancements in computer vision (CV) algorithms have shown promise in categorizing skin lesions with greater accuracy than human dermatologists.

However, the gap between CV algorithms and clinical practice is not significant. As technology advances, wireless connectivity and lifestyle management tools, such as home healthcare, fitness tracking capabilities, and wearable activity monitors, are increasingly integrated into dermatology diagnostic devices. These innovations offer opportunities for more accurate and accessible diagnoses, but they also raise concerns regarding consumer privacy and cybersecurity attacks. With the advent of 5G networks, faster and more reliable data transfer is expected to revolutionize the market. In conclusion, the need for accurate and reliable diagnosis of skin diseases remains a critical issue in healthcare. While advances in technology, such as computer vision algorithms and wireless connectivity, offer promising solutions, they also present challenges related to consumer privacy, cybersecurity, and regulatory compliance. As the market for dermatology diagnostic devices continues to evolve, it is essential to prioritize these considerations to ensure the delivery of effective, accessible, and secure diagnostic solutions.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Agfa Gevaert NV: The company offers a dermatology diagnostic device called Skintell, which is a non-invasive imaging technology for visualizing skin morphology.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Agfa Gevaert NV

- AnMo Electronics Corp.

- Baxter International Inc.

- Bayer AG

- Bomtech Electronics Co. Ltd.

- Bruker Corp.

- Caliber Imaging and Diagnostics Inc

- Canfield Scientific Inc.

- Danaher Corp.

- F. Hoffmann La Roche Ltd.

- Firefly Global

- FotoFinder Systems GmbH

- General Electric Co.

- HEINE Optotechnik GmbH and Co. KG

- Keyence Corp.

- KIRCHNER and WILHELM plus GmbH Co. KG

- Michelson Diagnostics Inc.

- Microcurrent Technology Inc.

- Strata Skin Sciences Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to advancements in technology and an increasing preference for non-invasive diagnostic methods. Dermatologists are leveraging innovative technologies like infrared imaging, ultrasound, and optical coherence tomography for early detection and treatment of various skin disorders, including cosmetic procedures and skin cancers. Demographic trends, such as an aging population and the rising prevalence of lifestyle-related disorders, are also driving market growth. Patient preference for home healthcare and wearable technology is transforming the market. Smartphone-based healthcare devices, wireless connectivity, and lifestyle management tools are becoming increasingly popular. Consumer privacy and cybersecurity are key concerns, with 5G networks and spatial computing offering potential solutions.

Technology advancements in the form of augmented reality (AR) and virtual reality (VR) are revolutionizing the way dermatologists diagnose and treat patients. Battery life, trackers, smartwatches, patches, and smart clothing are some of the consumer-grade devices gaining traction. Clinical-grade devices, such as those used in hospitals and research institutions, continue to dominate the market. Remote patient monitoring and home healthcare applications are driving the adoption of advanced diagnostic devices. UV radiation exposure can have a significant impact on general health and fitness, especially when it comes to skin health. To protect against potential harm, tools like HealthPulse TestNow can help individuals monitor and manage their health more effectively. Additionally, protecting personal health data, such as Protected Health Information (PHI), is critical when using these health technologies to ensure privacy and compliance with regulatory standards. Chronic diseases, such as cardiovascular diseases and nonmelanoma cancer, are major indications for these devices. Retail pharmacies and online distribution channels are also expanding the reach of these devices.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2023 |

|

Historic period |

2017-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.87% |

|

Market growth 2024-2028 |

USD 10.87 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.53 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

Asia at 34% |

|

Key countries |

US, China, UK, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Abbott Laboratories, Agfa Gevaert NV, AnMo Electronics Corp., Baxter International Inc., Bayer AG, Bomtech Electronics Co. Ltd., Bruker Corp., Caliber Imaging and Diagnostics Inc, Canfield Scientific Inc., Danaher Corp., F. Hoffmann La Roche Ltd., Firefly Global, FotoFinder Systems GmbH, General Electric Co., HEINE Optotechnik GmbH and Co. KG, Keyence Corp., KIRCHNER and WILHELM plus GmbH Co. KG, Michelson Diagnostics Inc., Microcurrent Technology Inc., and Strata Skin Sciences Inc |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -