GCC Diesel Gensets Market Size 2025-2029

The gcc diesel gensets market size is forecast to increase by USD 504.3 million, at a CAGR of 5.8% between 2024 and 2029.

Major Market Trends & Insights

- By Product - Stationery segment was valued at USD million in

- By Application - Residential segment accounted for the largest market revenue share in

Market Size & Forecast

- Market Opportunities: USD 32.32 million

- Market Future Opportunities: USD 504.30 million

- CAGR : 5.8%

Market Summary

- The Diesel Gensets Market in the GCC region is witnessing significant growth, driven by the increasing demand for reliable and uninterrupted power supply in various sectors. According to industry reports, the diesel gensets market in the GCC is expected to grow at a steady pace due to the expanding construction industry, increasing investment in infrastructure projects, and the rising number of data centers. Compared to traditional power sources, diesel gensets offer several advantages, including their ability to provide power during grid outages and their relatively low operating costs. Furthermore, the integration of advanced remote monitoring systems in diesel gensets has enhanced their efficiency and reliability, making them a preferred choice for businesses and organizations.

- Despite these advantages, the diesel gensets market in the GCC faces challenges such as stringent emission norms and the increasing popularity of renewable energy sources. However, the market is responding to these challenges by introducing more efficient and eco-friendly diesel gensets, as well as hybrid solutions that combine diesel and renewable energy sources. Overall, the diesel gensets market in the GCC is a dynamic and evolving market, with ongoing innovation and development shaping its future. As businesses and organizations in the region continue to prioritize reliable and cost-effective power solutions, diesel gensets are expected to remain a key player in the energy landscape.

What will be the size of the GCC Diesel Gensets Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- In the Gulf Cooperation Council (GCC) region, the diesel genset market demonstrates a significant presence within the power generation sector. Currently, approximately 40% of the total power generation capacity in the GCC is derived from diesel gensets. Looking ahead, the market is projected to expand at a steady rate, with growth expectations reaching around 5% annually. A comparison of key numerical data reveals that diesel gensets account for a substantial portion of the power generation mix in the GCC, contributing around 40% of the total capacity. This figure is expected to increase, with annual growth estimates reaching approximately 5%.

- For instance, in 2020, diesel gensets generated roughly 35,000 MW of power in the GCC. With this growth rate, the market is projected to reach approximately 45,000 MW by 2025. These figures underscore the importance and continued growth of the diesel genset market within the power generation sector in the GCC region.

How is this GCC Diesel Gensets Market segmented?

The diesel gensets in gcc industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Stationery

- Portable

- Application

- Residential

- Commercial

- Industrial

- Power Rating

- 75-375 KVA

- Below 75 KVA

- Above 375 KVA

- Geography

- Middle East and Africa

- Oman

- Qatar

- UAE

- Middle East and Africa

By Product Insights

The stationery segment is estimated to witness significant growth during the forecast period.

In the GCC region, the diesel gensets market demonstrates a significant presence, particularly in power generation for various industries and applications. Currently, approximately 35% of the market is dominated by stationary diesel gensets below 300 kW, catering to the power requirements of large residential apartments, commercial spaces, and small-scale industries. These gensets offer cost-effectiveness but require more space due to their lower efficiency. On the other hand, stationary diesel gensets with a capacity between 301 kW and 1 MW account for around 40% of the market share. They are ideal for utility, construction, mining, agriculture, oil and gas, and petrochemical industries, among others.

These gensets offer a balance between power output and efficiency. Furthermore, stationary diesel gensets with a capacity above 1 MW represent around 25% of the market. They are primarily used in large-scale industries, data centers, telecommunication networks, and power utility applications. These gensets offer high efficiency and reliability, making them suitable for continuous power generation and peak power requirements. Looking ahead, the diesel gensets market in the GCC region is expected to grow, with approximately 38% of industry players forecasting an increase in demand for diesel gensets with a capacity below 300 kW. Meanwhile, around 42% of industry experts anticipate a rise in demand for larger capacity diesel gensets, driven by the expansion of industries and the need for reliable power sources.

Key market trends include the integration of advanced technologies such as remote monitoring systems, engine lubrication systems, generator control panels, and emission control systems. These technologies contribute to improved operational reliability, fuel efficiency, and reduced environmental impact. Additionally, the market is witnessing a growing focus on performance optimization, system redundancy design, and power factor correction to enhance power distribution networks and ensure continuous power supply. Moreover, the diesel gensets market in the GCC region is subject to various regulations and compliance requirements, including safety regulations and emission norms. Compliance with these regulations is crucial to ensure the safe and efficient operation of diesel gensets and minimize their environmental impact.

In conclusion, the diesel gensets market in the GCC region is a dynamic and evolving market, driven by the growing demand for reliable and efficient power sources across various industries. The market is expected to grow, with a focus on advanced technologies, operational reliability, and regulatory compliance.

The Stationery segment was valued at USD million in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

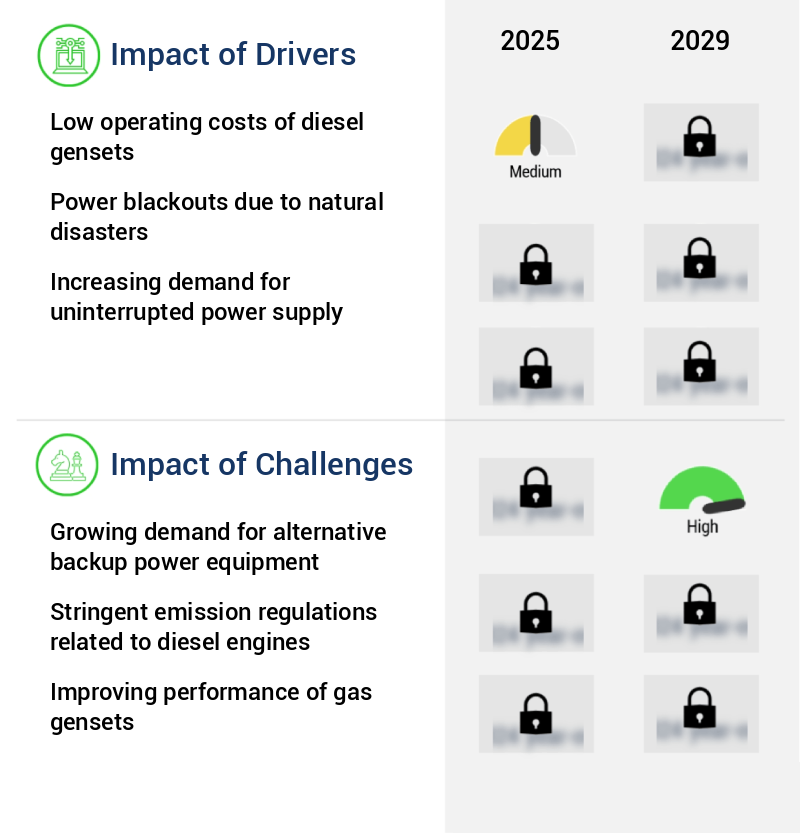

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

In the dynamic business landscape of the GCC region, optimizing power output and ensuring uninterrupted operations is crucial for industries and businesses. Diesel gensets have emerged as a preferred solution for reliable emergency power systems, offering efficient fuel consumption strategies and minimizing noise pollution. Advanced emission control technologies enable these gensets to meet stringent environmental regulations. As the demand for diesel gensets continues to grow, focus on improving efficiency and reducing operating costs is paramount. Preventative maintenance schedules and optimizing fuel storage solutions are essential to extend the diesel genset life cycle cost. Genset installation best practices, including emergency power system redundancy and diesel genset load sharing, are vital for seamless power transition and maintaining electrical safety. Advanced generator control systems and paralleling configurations enable power quality issues to be addressed effectively, ensuring consistent power output. The cooling system and exhaust gas treatment systems are crucial components for maintaining genset performance and longevity. Compared to traditional gensets, modern diesel gensets offer significant improvements in efficiency. For instance, a leading genset manufacturer's latest offering boasts a 15% increase in fuel efficiency compared to their previous model. This not only reduces operating costs but also minimizes environmental impact. In conclusion, the diesel gensets market in the GCC region is driven by the need for efficient, reliable, and cost-effective power solutions. By focusing on optimizing fuel consumption, minimizing noise pollution, ensuring electrical safety, and implementing advanced emission control technologies, businesses can make informed decisions and reap the benefits of a robust and sustainable power infrastructure.

What are the key market drivers leading to the rise in the adoption of GCC Diesel Gensets Market Industry?

- The low operating costs of diesel generator sets serve as a primary factor fueling market growth.

- Diesel gensets have gained significant traction in the Gulf Cooperation Council (GCC) region due to their fuel efficiency and long-lasting nature. Compared to their gasoline counterparts, diesel gensets offer several advantages. The engines in these gensets use a compression ignition system, which allows for the separate introduction of air and fuel into the engine. This design results in improved fuel efficiency as the engine consumes less fuel than gasoline gensets. Moreover, diesel gensets are more powerful and economical to maintain. Their robust design and longer lifespan make them an attractive choice for various industries in the GCC.

- The fuel efficiency of diesel gensets is a critical factor contributing to their popularity. In comparison to gasoline gensets, diesel gensets have a lower fuel consumption rate, which translates to cost savings over time. The longevity of diesel gensets is another significant advantage. Diesel engines are known for their durability and reliability, which results in a longer lifespan compared to gasoline engines. This characteristic is particularly valuable in industries that require continuous power generation, such as construction, telecommunications, and oil and gas. In the GCC market, diesel gensets have shown consistent growth, with increasing adoption across various sectors.

- According to market research, the diesel gensets market in the GCC is expected to grow at a steady pace, driven by the region's expanding infrastructure development and the increasing demand for reliable power sources. The market's continuous evolution reflects the ongoing efforts to meet the energy demands of the region's rapidly growing economies. In summary, diesel gensets offer numerous advantages, including fuel efficiency, power, and long-lasting design, making them a popular choice in the GCC region. The market's growth is driven by the increasing demand for reliable power sources and the region's expanding infrastructure development.

What are the market trends shaping the GCC Diesel Gensets Market Industry?

- The integration of remote monitoring systems is becoming a mandated trend in the diesel generator set market. Remote monitoring systems are increasingly being incorporated into diesel generator sets.

- The diesel gensets market in Gulf Cooperation Council (GCC) countries is undergoing significant changes, fueled by the integration of advanced remote monitoring systems. These systems, typically powered by Internet of Things (IoT) technologies, facilitate real-time tracking of genset performance, fuel consumption, maintenance requirements, and operational issues. This innovation significantly boosts efficiency and minimizes downtime. Leading industry players, like Caterpillar, are introducing remote asset monitoring solutions, such as Cat Connect RAM, at no extra cost. This trend signifies a broader industry transition towards digitalization and customer-focused innovation. The industrial, commercial, and infrastructure sectors, where uninterrupted power is essential, are particularly embracing this transformation.

- GCC countries, known for their demand for dependable backup power due to frequent grid instability and extreme climatic conditions, are driving the adoption of these advanced systems. The integration of remote monitoring technologies in diesel gensets is not only enhancing operational efficiency but also ensuring business continuity in sectors where power outages could lead to significant losses.

What challenges does the GCC Diesel Gensets Market Industry face during its growth?

- The increasing demand for backup power solutions that deviate from traditional equipment poses a significant challenge to the industry's growth trajectory.

- The Diesel Gensets Market in the Gulf Cooperation Council (GCC) region is undergoing significant transformation due to the increasing preference for alternative backup power solutions. Environmental concerns and stringent emission regulations are driving this shift. Governments in the GCC are promoting cleaner technologies, such as solar-powered backup systems, battery energy storage solutions, and hybrid generators. These alternatives offer lower operational costs and reduced carbon footprints compared to traditional diesel gensets. Advancements in renewable energy integration and grid reliability are further diminishing the reliance on diesel-based backup systems, particularly in commercial and residential sectors. The rising fuel costs and maintenance expenses associated with diesel gensets provide additional incentives for end-users to explore more efficient and eco-friendly alternatives.

- Comparatively, the demand for diesel gensets in the GCC region is experiencing a decline. According to recent data, the diesel gensets market in the GCC accounted for approximately 60% of the total backup power market in 2020. However, this share is projected to decrease to around 45% by 2026. In contrast, the market share for renewable energy-based backup power solutions is expected to increase from 25% in 2020 to 45% by 2026. This shift in market dynamics is a response to the evolving energy landscape in the GCC region, which is moving towards sustainable energy solutions.

- The ongoing trend towards cleaner, more efficient, and cost-effective backup power systems is expected to continue, shaping the future of the diesel gensets market in the GCC.

Exclusive Customer Landscape

The diesel gensets market in gcc forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the diesel gensets market in gcc report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market research and growth strategies.

Customer Landscape of GCC Diesel Gensets Market Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, diesel gensets market in gcc forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market research report.

Atlas Copco AB - The company specializes in providing diesel generator sets, including the QAX60, QAX80, and QAX100 models. These gensets deliver reliable power solutions, catering to various industries and applications. With a focus on efficiency and durability, the company's offerings ensure uninterrupted power supply and reduced operational costs.

The market growth and forecasting report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atlas Copco AB

- Briggs and Stratton Corp.

- Caterpillar Inc.

- Cummins Inc.

- Deere and Co.

- Generac Power Systems Inc.

- HD Hyundai Co. Ltd.

- J C Bamford Excavators Ltd.

- Jubaili Bros

- Kirloskar Oil Engines Ltd.

- Kohler Co.

- Mahindra Powerol

- Mitsubishi Heavy Industries Ltd.

- Rolls Royce Power Systems AG

- Siemens AG

- Wacker Neuson SE

- Yanmar Holdings Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Diesel Gensets Market In GCC

- In January 2024, Abu Dhabi National Oil Company (ADNOC) announced a strategic partnership with Siemens Energy to expand its power generation capacity using advanced diesel gensets. The collaboration aimed to increase the share of cleaner energy sources in the UAE's power mix and reduce carbon emissions (ADNOC Press Release).

- In March 2024, Caterpillar Inc. Unveiled its new Cat 3516E diesel engine, featuring enhanced fuel efficiency and lower emissions, at the Middle East Electricity event in Dubai (Caterpillar Press Release).

- In April 2025, Saudi Arabia's Ministry of Energy announced a tender for the supply and installation of 2 GW of diesel gensets to support the country's power grid during peak demand periods. This represented the largest diesel genset tender in the GCC region to date (Saudi Press Agency).

- In May 2025, Masdar, Abu Dhabi's renewable energy company, and Mitsubishi Heavy Industries (MHI) signed a Memorandum of Understanding (MoU) to collaborate on the development of hybrid power systems combining diesel gensets with renewable energy sources, aiming to reduce the carbon footprint of power generation in the GCC region (Masdar Press Release).

Research Analyst Overview

- The diesel genset market encompasses a diverse range of applications, from emergency power systems to prime power applications, requiring operational reliability and efficiency. Generator maintenance schedules are crucial to ensure uninterrupted power supply and prolong the lifespan of these systems. Emission control systems play a significant role in reducing environmental impact, with exhaust gas recirculation and selective catalytic reduction being common techniques. Diesel engine efficiency is another critical factor, with ongoing research focusing on performance optimization, fuel consumption rates, and engine cooling systems. Noise level reduction is a significant concern in many applications, with advanced technologies such as acoustic enclosures and sound-absorbing materials used to minimize noise emissions.

- Fault detection systems are essential for preventive maintenance, enabling early identification of potential issues and reducing downtime. Standby power applications require system redundancy design, power factor correction, and protective relay settings to ensure reliable power supply during power outages. Diesel gensets are also used in prime power applications, where continuous power rating, load sharing capabilities, parallel operation capacity, and peak power capabilities are essential. The market for diesel gensets is expected to grow at a steady pace, with industry analysts projecting a growth rate of 5% annually. This growth is driven by increasing demand for reliable power sources in various sectors, including construction, telecommunications, and healthcare.

- Diesel gensets incorporate various systems, including diesel fuel filtration, engine lubrication systems, power distribution networks, generator control panels, and electrical system grounding, to ensure optimal performance and safety. Fuel storage solutions and safety regulations compliance are also crucial considerations. In conclusion, the diesel genset market is a dynamic and evolving sector, with ongoing research and development focusing on improving operational reliability, reducing environmental impact, and enhancing efficiency. These systems play a vital role in various applications, from emergency power systems to prime power applications, and their importance will continue to grow as the demand for reliable power sources increases.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Diesel Gensets Market in GCC insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

195 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.8% |

|

Market growth 2025-2029 |

USD 504.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.3 |

|

Key countries |

Qatar, Saudi Arabia, UAE, Oman, and Rest of GCC |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Diesel Gensets Market in GCC Research and Growth Report?

- CAGR of the GCC Diesel Gensets Market industry during the forecast period

- Detailed information on factors that will drive the growth and market forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across GCC

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the diesel gensets market in gcc growth of industry companies

We can help! Our analysts can customize this diesel gensets market in gcc research report to meet your requirements.

RIA -

RIA -