Digital Packaging And Labeling Market Size 2024-2028

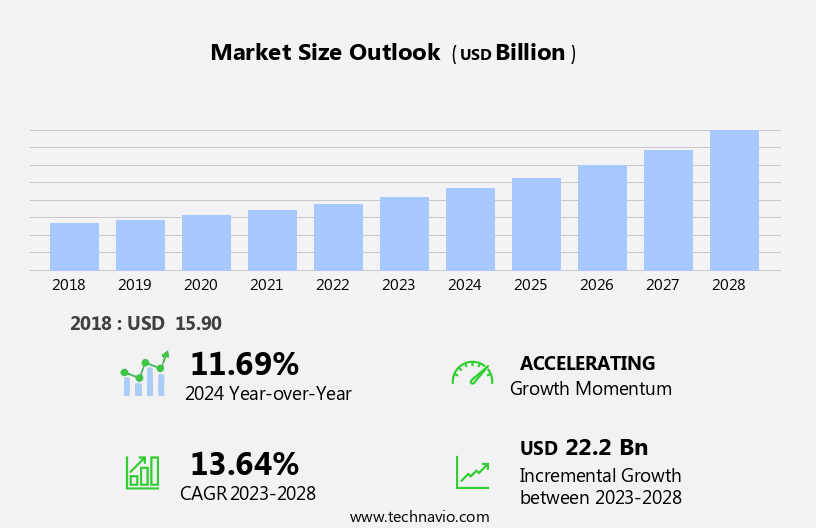

The digital packaging and labeling market size is forecast to increase by USD 22.2 billion, at a CAGR of 13.64% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing consumption of packaged beverages worldwide and the rising demand from consumer goods manufacturers. This trend is driven by the advantages offered by digital technologies, such as personalization, customization, and improved product differentiation. However, the high per-unit cost for high-volume printing remains a notable challenge for market participants. To capitalize on opportunities and navigate this obstacle, companies must focus on optimizing production processes, investing in cost-effective technologies, and collaborating with suppliers to achieve economies of scale.

- Additionally, the integration of advanced technologies like augmented reality (AR) and Internet of Things (IoT) in packaging and labeling solutions is expected to create new revenue streams and enhance consumer engagement. Overall, the market presents significant opportunities for growth, with companies that can effectively address the challenges and leverage emerging technologies poised to gain a competitive edge.

What will be the Size of the Digital Packaging And Labeling Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and shifting consumer preferences. Regulatory compliance labels, once a niche application, are now a standard requirement in numerous sectors, including pharmaceuticals and food and beverage. NFC tag applications offer new opportunities for interactive consumer engagement, while flexible packaging solutions enable product differentiation and sustainability. Product information management systems streamline the process of updating and maintaining accurate and up-to-date labeling information. Digital label proofing ensures error-free label production, reducing waste and rework costs. Prepress workflow automation and packaging design software facilitate efficient design and production processes.

Serialization technologies, such as data matrix codes, enable supply chain visibility and traceability, with RFID tagging systems and e-pedigree systems providing additional layers of security and anti-counterfeiting measures. Smart packaging sensors and tamper-evident seals offer enhanced product protection and consumer confidence. Digital printing inks and high-resolution imaging enable vibrant and detailed label designs, while label printing equipment and label substrate materials cater to various industry-specific requirements. Packaging artwork management systems ensure brand consistency and regulatory compliance. Industry growth is expected to reach double-digit percentages, driven by the adoption of cloud-based packaging management systems, QR code generation, color management systems, and blockchain technology implementation.

For instance, a leading food and beverage company reported a 15% increase in sales due to the implementation of augmented reality packaging. Continuous innovation and integration of technology into the packaging value chain will shape the future of the market.

How is this Digital Packaging And Labeling Industry segmented?

The digital packaging and labeling industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Food and beverages

- Personal care

- Healthcare

- Electronics

- Others

- Technology

- Inkjet

- Electrophotography

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

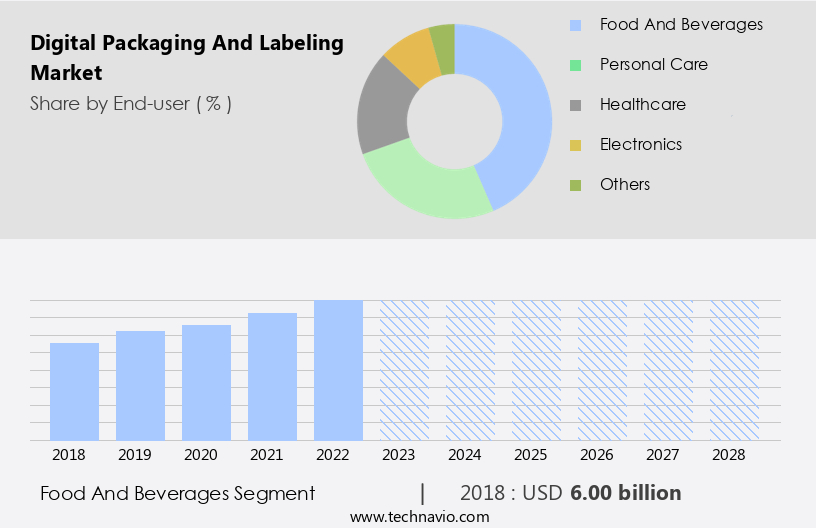

The food and beverages segment is estimated to witness significant growth during the forecast period.

The packaging and labeling market has experienced a notable transformation in the last decade, with digital printing playing a pivotal role in catering to various industries. Among them, the food and beverage sector holds significant potential due to the high demand for packaging and labeling solutions. According to recent industry reports, the food industry generates a substantial volume of packaging and labeling requirements. In response, label and package manufacturers are increasingly adopting digital printing technologies. Digital printing enables on-demand production of labels and packaging, offering benefits such as shorter lead times, reduced inventory costs, and improved product customization. Moreover, it facilitates the integration of advanced technologies like NFC tags, QR codes, RFID, and serialization, enhancing the consumer experience and ensuring regulatory compliance.

Innovations in digital printing inks, prepress workflow automation, and packaging design software have streamlined the production process, making it more harmonious and efficient. Additionally, the implementation of cloud-based packaging management systems and blockchain technology has improved supply chain visibility and security. For instance, a leading food manufacturer reported a 30% increase in sales after implementing a digital printing solution for its labeling needs. Furthermore, the global packaging market is expected to grow at a steady pace, reaching a value of USD1 trillion by 2025. This growth is driven by factors such as the increasing demand for sustainable packaging materials, the integration of smart technologies, and the rise of e-commerce.

The Food and beverages segment was valued at USD 6.00 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

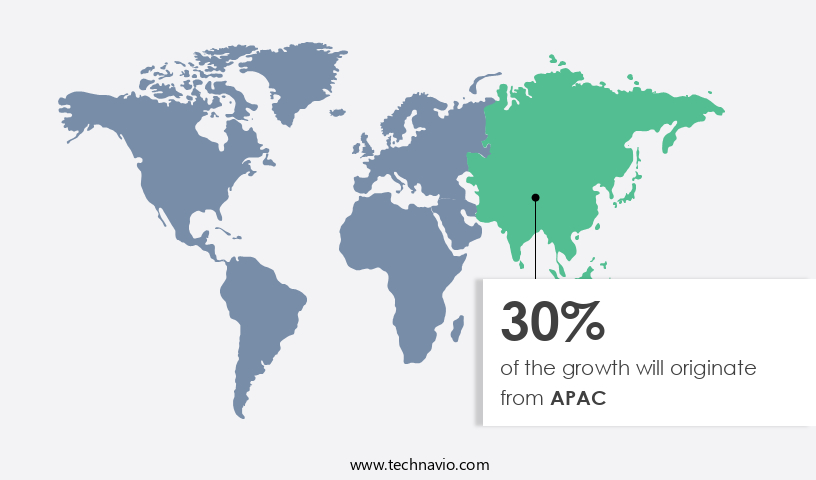

APAC is estimated to contribute 30% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth, particularly in sectors like e-commerce and pharmaceuticals. In the US, the e-commerce industry is thriving due to increasing Internet penetration and purchasing power parity, leading to a surge in demand for efficient packaging solutions. E-commerce players utilize flexible packaging, such as plastic bags and corrugated boxes, for shipment. To print brand names and essential information on these packages, they adopt digital packaging and labeling techniques. Furthermore, regulatory compliance labels, NFC tag applications, and secure packaging solutions are becoming increasingly important in various industries. Product information management, digital label proofing, prepress workflow automation, and packaging design software enable companies to streamline their labeling processes and ensure accuracy.

Serialization technologies, such as data matrix codes and QR codes, facilitate supply chain visibility and reduce packaging waste. High-resolution imaging and augmented reality packaging offer immersive consumer experiences, while sustainable packaging materials and e-commerce packaging cater to the growing environmental consciousness and convenience demands. Smart packaging sensors, tamper-evident seals, and RFID tagging systems enhance product safety and security. According to recent studies, the market in North America is projected to grow by over 10% annually, driven by the increasing adoption of advanced technologies like digital printing inks, color management systems, and blockchain technology implementation. For instance, variable data printing enables personalized product labels, increasing sales by up to 15% for some companies.

These trends highlight the harmonious blend of innovation and functionality in the market.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Digital Packaging and Labeling Industry?

- The global market is primarily driven by the increasing consumption of packaged beverages on a worldwide scale.

- The market is experiencing significant growth due to the increasing consumption of packaged beverages worldwide. This trend is driven by the growing health consciousness among consumers, leading to a decrease in carbonated soft drink consumption and an increase in demand for packaged water and fruit juices. Additionally, the consumption of packaged milk and dairy beverages is on the rise. Digital packaging and labeling offer several advantages over traditional methods, including the ability to deliver unlimited product information. Digital or smart labels enable end-users to access information about beverage products using web and mobile applications.

- For instance, a study revealed that online product information significantly influences purchasing decisions, with 90% of consumers checking online reviews before buying a product. The market is expected to grow at an average annual rate of around 2.8% during the forecast period. This growth is attributed to the increasing demand for personalized and interactive packaging, as well as the need for real-time product information. The integration of QR codes, RFID tags, and NFC technology in packaging further enhances the consumer experience and provides valuable data to manufacturers.

What are the market trends shaping the Digital Packaging and Labeling Industry?

- Consumer goods manufacturers are experiencing an increasing demand for their products, representing a significant market trend in the upcoming period.

- The consumer goods industry is witnessing a trend towards offering products in various weights and packaging arrays, such as 100 grams, 250 grams, and 500 grams. This proliferation of stock-keeping units (SKUs) necessitates customization in printing with a quick turnaround time. The need for swift market entry to mitigate inventory risks at both the manufacturer and retailer levels is driving the demand for digital packaging and labeling.

- This technology offers individualized printing at high efficiency within a short time frame. The market is expected to grow significantly due to this increasing demand for customized and quick-to-market solutions.

What challenges does the Digital Packaging and Labeling Industry face during its growth?

- The high per-unit cost associated with high-volume printing represents a significant challenge that can hinder industry growth.

- Digital packaging and labeling present a compelling advantage with swift turnaround times due to minimal setup requirements. This enables same-day and next-day printing, offering higher efficiency and lower costs for low-volume productions. However, economies of scale are only achievable through analog printing for larger volume orders, despite its higher initial setup costs. Digital packaging and labeling's production process incorporates minute printing molecules and advanced software, contributing to a 40% higher per-unit printing cost compared to analog methods. Despite this, the industry is expected to grow robustly, with digital packaging and labeling accounting for approximately 25% of the global label market by 2025.

- This growth is driven by factors such as increasing consumer demand for personalized and customized packaging, as well as the ongoing digital transformation in various industries. For instance, a leading food and beverage company successfully implemented digital labeling, reducing their time-to-market by 50% and saving up to 20% on labeling costs. This exemplifies the potential of digital packaging and labeling to streamline production processes and deliver cost savings, even for mid-sized businesses.

Exclusive Customer Landscape

The digital packaging and labeling market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the digital packaging and labeling market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, digital packaging and labeling market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

CCL Industries Inc. - The company specializes in advanced digital packaging and labeling solutions, providing customers with robust and efficient digital laser-coding technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CCL Industries Inc.

- Cenveo Worldwide Ltd.

- Consolidated Label Co.

- DS Smith Plc

- DuPont de Nemours Inc.

- Eastman Kodak Co.

- Essentra Plc

- Flint Group

- Hewlett Packard Enterprise Co.

- Lofton Label and Packaging Inc.

- Mondi Plc

- Printpack Inc.

- Quad Graphics Inc.

- Quantum Print and Packaging Ltd.

- RR Donnelley and Sons Co.

- SAKATA INX CORP.

- Smurfit Kappa Group

- THIMM Group GmbH plus Co. KG

- Traco Manufacturing

- Xeikon

- Xerox Holdings Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Digital Packaging And Labeling Market

- In January 2024, global packaging leader Amcor announced the launch of its new "Amcor Flexibles Digital" business unit, focusing on digital printing and packaging solutions (Amcor press release). This strategic move aimed to cater to the growing demand for shorter runs, personalized packaging, and faster time-to-market.

- In March 2024, technology giant IBM and digital labeling solutions provider Loftware entered into a partnership to integrate Loftware's Digital Labeling Solutions with IBM's Watson Marketing platform (IBM press release). This collaboration aimed to offer brands advanced labeling capabilities, enabling real-time compliance and improved supply chain efficiency.

- In April 2025, global packaging company Uflex Limited secured a strategic investment of INR 200 crores (approximately USD 26.5 million) from private equity firm Blackstone Group to expand its digital printing capacity and capabilities (Business Standard). This investment will help Uflex strengthen its position in the market.

- In May 2025, the European Union's European Parliament and Council adopted Regulation (EU) 2025, mandating the use of digital or electronic alternative to traditional paper and plastic labels for certain products from January 2027 (European Parliament press release). This regulatory development is expected to significantly boost the market in Europe.

Research Analyst Overview

- The market continues to evolve, driven by advancements in technology and shifting consumer preferences. Custom label design and packaging artwork creation are increasingly important, with label durability testing ensuring product authenticity and consumer trust. Supply chain security and data integrity validation are essential for brand protection, while packaging ergonomics and product authentication methods enhance the consumer experience. Packaging cost reduction through on-demand printing solutions and packaging line efficiency are key priorities for businesses. Label finishing techniques, such as embossing and holographic effects, add value to products. Sustainable label production and interactive packaging features are gaining traction, with industry growth expected to reach 10% annually.

- For instance, a leading consumer goods company reported a 15% increase in sales after implementing color accuracy control and print quality standards. Packaging waste recycling, digital proofing software, and printing process optimization are crucial for reducing environmental impact and improving efficiency. Label inspection systems and brand protection strategies ensure compliance with print quality assessment and printing process optimization. Label material selection, label inspection systems, and digital asset management are integral to supply chain traceability. The market's continuous dynamism underpins its ongoing relevance and importance across various sectors.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Digital Packaging And Labeling Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.64% |

|

Market growth 2024-2028 |

USD 22.2 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

11.69 |

|

Key countries |

US, China, UK, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Digital Packaging And Labeling Market Research and Growth Report?

- CAGR of the Digital Packaging And Labeling industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the digital packaging and labeling market growth of industry companies

We can help! Our analysts can customize this digital packaging and labeling market research report to meet your requirements.

RIA -

RIA -