Dips and Spreads Market Size 2024-2028

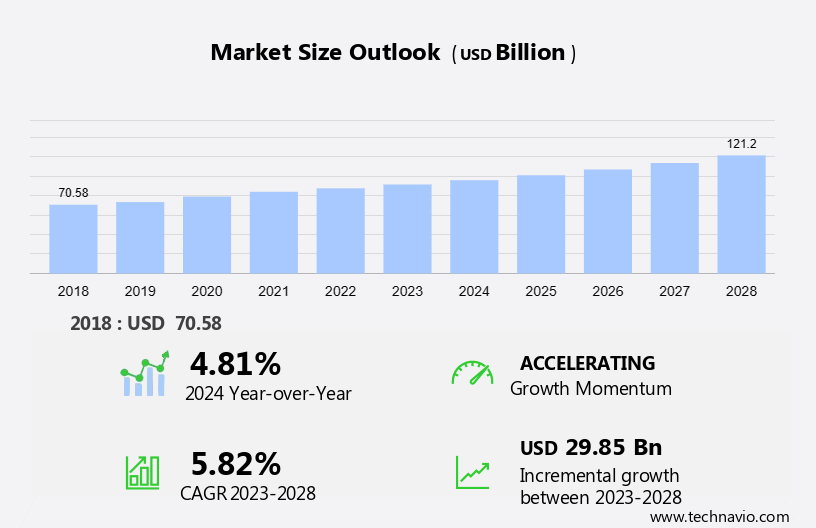

The dips and spreads market size is forecast to increase by USD 29.85 billion at a CAGR of 5.82% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing popularity of appetizers and finger food in the US. Ethnic and international cuisines, such as dumplings, pita bread, and seafood dips, are gaining traction among consumers, driving market expansion. Additionally, there is a growing emphasis on clean-label food products, with consumers preferring dips and spreads made from natural ingredients and free from artificial additives.

- Rise in allergens and dietary restrictions is driving the creation of alternative options, such as dips made from raw vegetables, meat, and plant-based proteins. Common pairings like crackers, fruits, tortilla chips, and potato chips are further contributing to the market's growth.

What will be the Dips and Spreads Market Size During the Forecast Period?

- The market has witnessed significant growth in recent years, with established brands continually expanding their product lines to capture consumer attention. The market encompasses a diverse range of offerings, including thick sauces for Mexican food, natural spreads, and plant-based alternatives catering to the vegan movements. Consumer preferences for dips and spreads are driven by factors such as taste, product quality, and food safety. Brands focus on delivering authentic flavors and textures to meet the evolving demands of consumers. Incorporating high-quality raw materials and ensuring food safety throughout the supply chain is essential for maintaining consumer trust and loyalty. Appetizers, finger foods, and snack foods are popular categories for dips and spreads. Consumers enjoy pairing these items with pita bread, dumplings, seafood, and nachos, or simply using them as a spread on crackers. The versatility of dips and spreads makes them a staple in various culinary applications, from casual gatherings to fine dining experiences. Mexican food, with its vibrant flavors and rich textures, has a substantial presence in the market. Guacamole, salsa, and queso dips are among the most popular choices for consumers.

- Moreover, the market also offers a wide array of nut-based spreads, providing plant-based alternatives for those following vegan diets or seeking healthier options. Restaurants and foodservice establishments are significant contributors to the market. They offer a diverse range of dips and spreads to cater to various tastes and dietary preferences. The convenience and versatility of these products make them an essential component of many restaurant menus, enhancing the overall dining experience for customers. In conclusion, the market continues to grow as consumers seek out authentic, high-quality, and diverse offerings. Brands that prioritize consumer preferences, food safety, and supply chain transparency are well-positioned to succeed in this competitive landscape. The market's continued expansion is driven by trends such as the increasing popularity of plant-based alternatives, the vegan movements, and the versatility of dips and spreads in various culinary applications.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

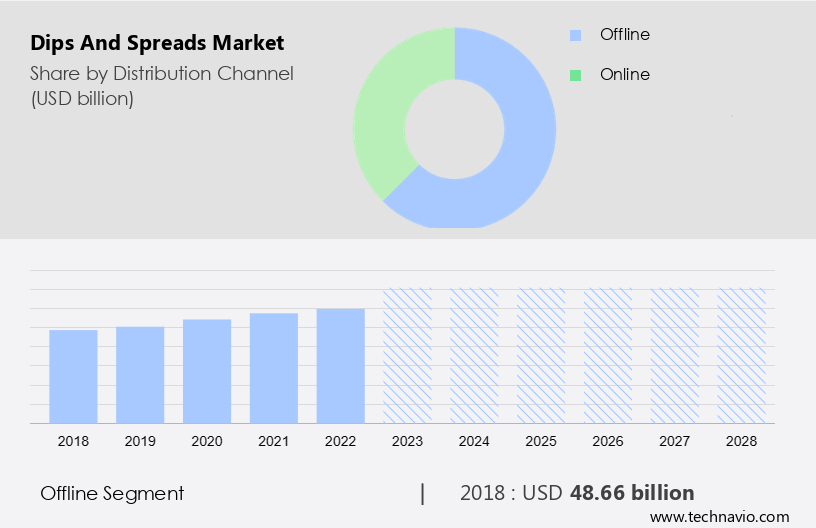

- Distribution Channel

- Offline

- Online

- End-user

- Foodservice industry

- Household

- Geography

- APAC

- North America

- Canada

- US

- Europe

- UK

- France

- South America

- Middle East and Africa

- APAC

By Distribution Channel Insights

- The offline segment is estimated to witness significant growth during the forecast period.

In the United States, offline distribution channels play a crucial role in the expansion of the market. A multitude of retail outlets contribute substantially to the sales and distribution of these products, addressing the diverse demands of various consumer segments. Supermarkets, hypermarkets, and grocery stores are primary channels, providing a vast selection of brands, flavors, and packaging sizes for consumers' convenience. Specialty food stores specialize in gourmet or health-conscious options, stocking a curated range of high-end and unique dips and spreads, catering to consumers seeking premium or specialized products. Popular spreads in the US market include plant-derived options such as jellies, jams, and honey, as well as meat-based spreads like pate and marmite equivalents such as vegemite.

Additionally, flavor-driven spreads like gochujang, chimichurri, and peri peri continue to gain traction. While some spreads offer nutritional benefits, others may contribute to unhealthy snacking habits. Margarine, a common spread, has faced competition from healthier alternatives like olive oil spreads and nut butters. Overall, the US market is characterized by a wide array of offerings, catering to various consumer preferences and dietary needs.

Get a glance at the market report of share of various segments Request Free Sample

The Offline segment was valued at USD 48.66 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

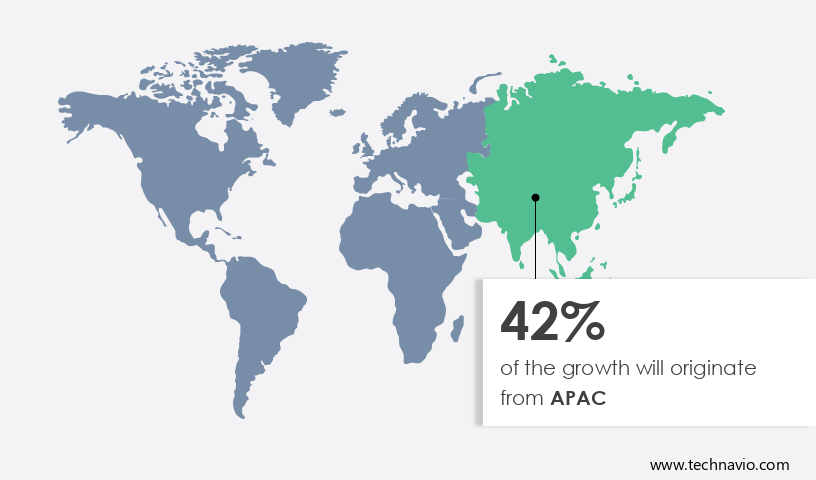

- APAC is estimated to contribute 42% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The Asia Pacific (APAC) region is witnessing a notable expansion in the market for dips and spreads, driven by several factors. Consumer preferences are evolving, leading to a growing demand for convenient and flavorful options. Urbanization and rising disposable incomes are contributing to the increasing popularity of ready-to-eat foods, with dips and spreads serving as ideal accompaniments. The food service industry is also expanding, providing more opportunities for dips and spreads in various settings. In the APAC region, countries like China, India, Japan, South Korea, and Southeast Asian nations are experiencing a significant increase in the consumption of convenience foods and snacks.

This trend is particularly prominent in urban areas, where busy lifestyles and changing demographics are driving demand. Dips and spreads, including thick sauces, Mexican food staples like nachos and salsa, natural spreads, plant-based and vegan options, and nut-based spreads, are gaining popularity. PepsiCo, a leading player in the global food and beverage industry, has recognized this trend and is expanding its offerings in the market. The company's D2C (Direct-to-Consumer) initiatives and partnerships with restaurants and food service providers are aimed at capitalizing on this growth. The cheese segment, a significant contributor to the dips market, is expected to continue its dominance, while vegetable dips and sauces are also gaining traction due to health-conscious consumer preferences.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Dips and Spreads Market?

Increasing influence of ethnic and international cuisines on dips and spreads is the key driver of the market.

- The market is witnessing significant growth due to the increasing consumer interest in ethnic and international cuisines. As globalization broadens cultural connections, consumers in the United States are increasingly seeking authentic and exotic flavors, leading to a heightened demand for dips and spreads inspired by diverse culinary traditions. Brands are responding to this trend by expanding their product offerings to cater to specific regional tastes, such as Mediterranean, Middle Eastern, Latin American, Asian, and African-inspired varieties. Established brands and artisanal producers are focusing on taste, product quality, and food safety to capture consumer attention. The hummus segment, in particular, has gained popularity due to its nutritional value and plant-based protein content.

- However, consumers are also mindful of saturated fat content and are looking for healthier alternatives. The jars segment of the market is growing, with glass jars becoming a preferred packaging material due to their premium look and appeal. Supply chain and raw material sourcing are crucial considerations for brands, ensuring a steady supply of high-quality ingredients and maintaining transparency in their production processes. Mediterranean cuisine, with its rich and diverse flavors, continues to dominate the market. Consumers are drawn to the authentic taste and health benefits of these products, making them a staple in many households. As the market evolves, brands are focusing on innovation and product development to meet the changing needs and preferences of consumers.

What are the market trends shaping the Dips and Spreads Market?

Increasing emphasis on clean-label food products is the upcoming trend in the market.

- The preference for clean label foods continues to gain traction in the market in the United States, as consumers increasingly prioritize natural and transparent ingredients. This trend is fueled by a heightened awareness and concern regarding the components in the food we consume. As a result, there is a burgeoning demand for dips and spreads with clear labels, devoid of artificial flavors, colors, preservatives, and additives. Consumers are drawn to products featuring recognizable and natural ingredients, such as herbs, spices, vegetables, and whole foods. In response, manufacturers are modifying their formulations to include shorter ingredient lists and eschewing artificial additives.

- Dips and spreads made with seafood, raw vegetables, meat, fruits, tortilla chips, potato chips, pita bread, and dumplings are popular choices among consumers. Spreads like hummus, guacamole, and falafel are favored for their rich textures and flavors, often served with a knife and bread or dishes like pita or tortilla chips.

What challenges does Dips and Spreads Market face during the growth?

Increase in prevalence of allergens and dietary restrictions is a key challenge affecting the market growth.

- The market in the United States is witnessing significant growth due to the increasing demand for gourmet products and natural, nutritious ingredients. Product offerings in this market include hummus, guacamole, salsa, cheese spreads, and vegetable dip, available in various forms such as jars, tubs/tubes, and single-serve packets. However, catering to the diverse dietary needs and restrictions of consumers, including allergies to common ingredients like nuts, dairy, gluten, and soy, as well as veganism and paleo diets, poses a challenge for manufacturers.

- Creating allergen-free or hypoallergenic dips and spreads necessitates careful ingredient sourcing, production processes, and cross-contamination prevention. Proper labeling practices are essential to accurately communicate potential allergens and adhere to regulatory standards, ensuring consumer trust and food safety. The online retail segment, including foodservice and retail stores, plays a crucial role in the distribution of these products. Key players in the market include Hummus Bowl, Sabra, and Newman's Own, among others.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Andros Group

- Arizona Spice Company LLC

- AVT Gavia Foods Pvt. Ltd

- Campbell Soup Co.

- Conagra Brands Inc.

- Cornitos

- Del Monte Pacific Ltd.

- Dr. August Oetker KG

- Euro American Brands LLC

- Ferrero International S.A.

- Hormel Foods Corp.

- McCormick and Co. Inc.

- PepsiCo Inc.

- Renfro Foods

- Sandridge Crafted Foods

- The Hershey Co.

- The Kraft Heinz Co.

- VRB CONSUMER PRODUCTS Pvt. Ltd.

- Wingreens Farms Pvt. Ltd.

- Yihai International Holding Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Dips and spreads have become a popular choice for consumers seeking delicious and nutritious additions to their appetizers, snacks, and meals. Established brands dominate the market with diverse product offerings, catering to various consumer preferences. Taste and product quality are key factors driving consumer attention, with an emphasis on food safety and ethical supply chains. The hummus segment, a staple in Mediterranean cuisine, leads the market due to its nutritious value and plant-based protein content. Consumers prefer jars over tubs/tubes, tubs, or single-serve packets for a premium look and artisanal feel. Packaging materials, such as glass jars, also contribute to the premium image of these products. The online retail segment has seen significant growth due to the convenience it offers. Natural and nutritious ingredients are in high demand, with a focus on reducing unhealthy ingredients like saturated fat, salt, sugar, and unhealthy fats. New product types, such as plant-derived spreads, jellies, jams, and honey, are gaining popularity. Flavor-driven spreads, like gochujang, chimichurri, and peri peri, are influencing consumer buying decisions.

Moreover, the market demand for unrivaled flavors continues to rise, with rapid urbanization and altered eating habits driving sales. Refrigeration and storage are crucial factors in the market, ensuring product freshness and shelf life. Market trends include the influence of vegan movements and the rise of nut-based spreads. The food service industry, including restaurants and foodservice segments, also contributes significantly to the market growth. Thick sauces, like mayonnaise and cheese spreads, and vegetable dips remain popular choices. The cheese segment continues to dominate, with Mexican food and sauces gaining traction. The market also caters to various sectors, including B2B and B2C, and the direct-to-consumer (D2C) channel. The market research report on dips and spreads covers various aspects, including product types, market trends, and consumer preferences. It provides insights into the market's future growth potential and key challenges.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

152 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.82% |

|

Market growth 2024-2028 |

USD 29.85 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.81 |

|

Key countries |

US, Canada, Australia, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -