Direct Air Capture Market Size 2025-2029

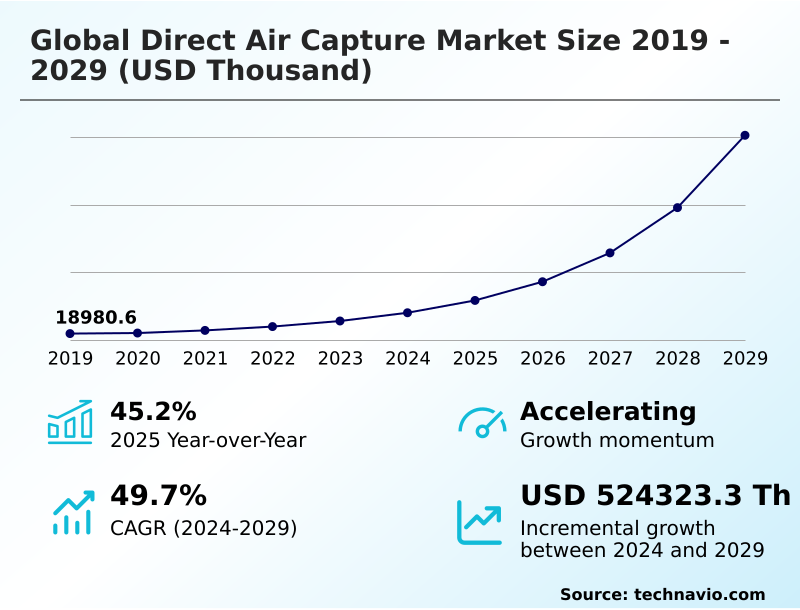

The direct air capture market size is valued to increase by USD 524.32 million, at a CAGR of 49.7% from 2024 to 2029. Increasing corporate net-zero commitments will drive the direct air capture market.

Major Market Trends & Insights

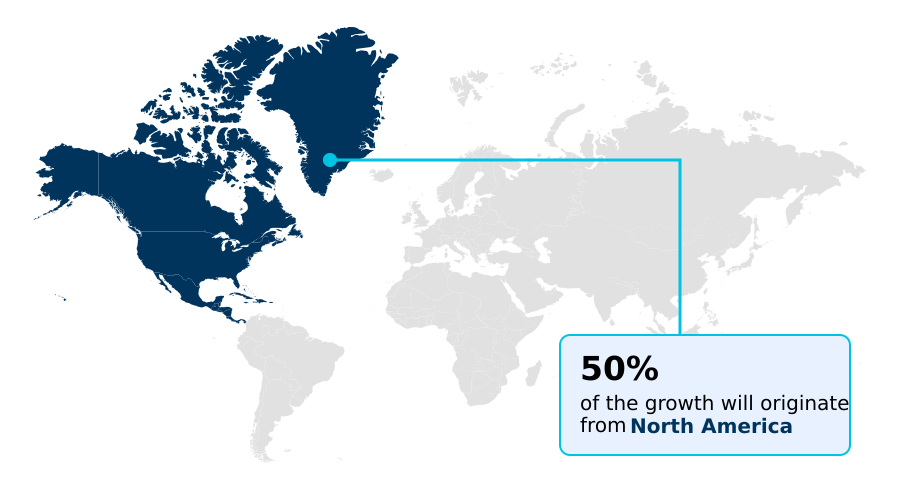

- North America dominated the market and accounted for a 49.7% growth during the forecast period.

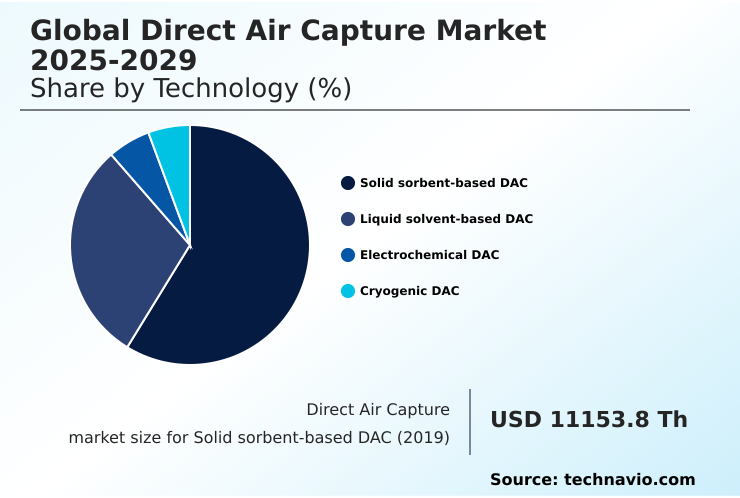

- By Technology - Solid sorbent-based DAC segment was valued at USD 32.94 million in 2023

- By Source - Electricity segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 524.32 million

- CAGR from 2024 to 2029 : 49.7%

Market Summary

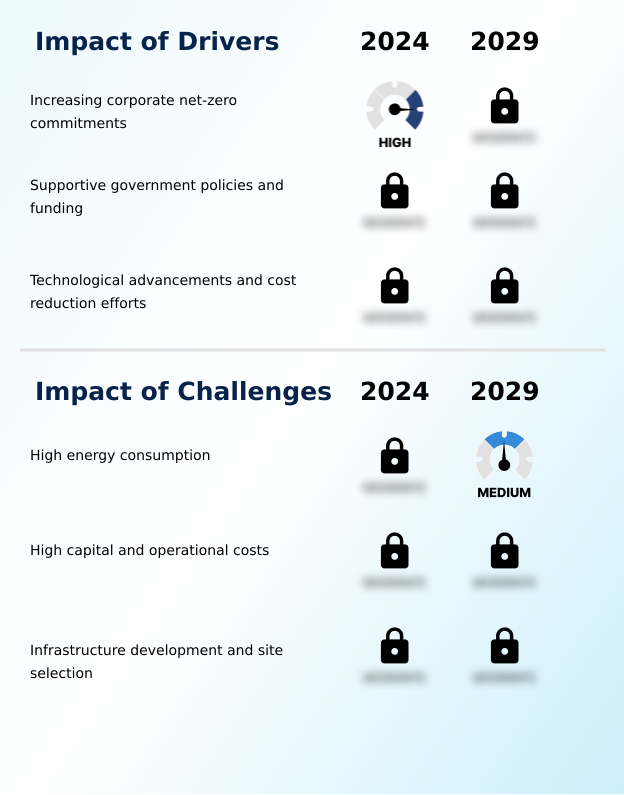

- The direct air capture market is a critical component of global decarbonization strategies, focusing on technologies engineered for atmospheric carbon dioxide removal. This field is defined by several technological pathways, including solid sorbent-based dac, liquid solvent-based dac, and emerging electrochemical dac systems. Growth is fueled by increasing corporate net-zero commitments and supportive government policies providing financial incentives.

- However, the industry contends with significant hurdles, notably the high energy consumption per ton co2 captured and the substantial capital expenditure required for deployment. A key trend involves the integration of dac facilities with renewable energy sources to ensure the carbon removal process is genuinely net-negative.

- For instance, an industrial conglomerate might deploy modular dac systems powered by a dedicated solar farm, using the captured CO2 as a feedstock to produce carbon-neutral synthetic fuels, thereby creating a circular carbon economy and fulfilling its ESG mandates. This scenario highlights the strategic convergence of climate action and economic innovation, where carbon removal credits become a valuable asset.

- The continuous drive for technological advancements, such as improving sorbent regeneration cycles, is essential for reducing costs and scaling this vital net-zero emissions technology.

What will be the Size of the Direct Air Capture Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Direct Air Capture Market Segmented?

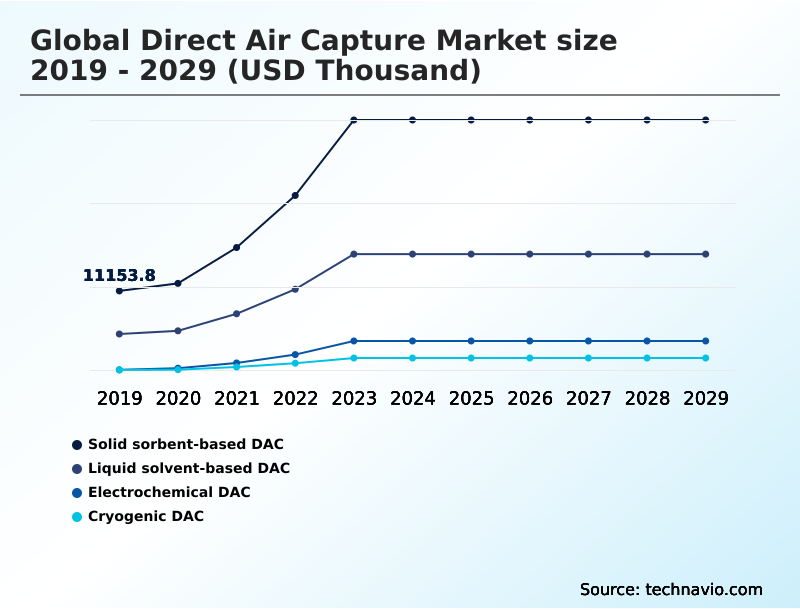

The direct air capture industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Technology

- Solid sorbent-based DAC

- Liquid solvent-based DAC

- Electrochemical DAC

- Cryogenic DAC

- Source

- Electricity

- Heat

- Application

- Carbon capture and storage

- Carbon capture utilization and storage

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Technology Insights

The solid sorbent-based dac segment is estimated to witness significant growth during the forecast period.

The direct air capture market is segmented by technology, with solid sorbent-based DAC representing a prominent pathway. This method utilizes solid materials, such as those enabling CO2 mineralization, to adsorb carbon dioxide from ambient air.

Air is drawn through a CO2 air contactor where the sorbent binds to CO2 molecules. The sorbent is then regenerated, often through temperature swing adsorption, to release a concentrated CO2 stream for geological CO2 storage or carbon dioxide utilization.

Innovations in this segment focus on enhancing sorbent capacity and longevity to reduce operational costs, with advanced systems improving regeneration efficiency by over 15%.

This approach's modularity is a key advantage, facilitating scalable deployment for atmospheric carbon dioxide removal and the generation of carbon removal credits.

The Solid sorbent-based DAC segment was valued at USD 32.94 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 49.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Direct Air Capture Market Demand is Rising in North America Get Free Sample

The geographic landscape of the direct air capture market is led by North America, which benefits from robust policy support and significant private investment.

This region is projected to exhibit an expansion rate of 50.3%, driven largely by initiatives in the United States and Canada. Europe is another key region, with an expected growth of 48.6%, focusing on renewable energy integration and industrial decarbonization.

However, the APAC region is forecast to expand at the fastest rate of 50.5%, with nations increasingly investing in net-zero emissions technology.

The development of CO2 transport infrastructure is a critical factor across all regions, enabling the connection between capture sites and locations for saline aquifer storage.

The advancement of passive direct air capture and moisture swing regeneration techniques is particularly relevant for diverse global climates, influencing regional technology adoption and decarbonization strategy.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the direct air capture market hinges on a nuanced understanding of competing technologies and their economic implications. A critical evaluation of solid sorbent vs liquid solvent dac efficiency reveals differing trade-offs in energy consumption and scalability, impacting long-term operational costs.

- The continuous push for cost reduction in direct air capture technology is a central theme, with advancements in areas like moisture swing regeneration and amine-based sorbents for co2 capture showing promise. Integrating dac with renewable energy sources is now a baseline requirement for sustainable projects, directly influencing site selection and infrastructure planning.

- The applications of captured co2 in industry are diversifying, moving beyond traditional uses toward high-value products like synthetic fuels and carbon-negative building materials. This shift is essential for improving the economic viability of carbon removal credits. However, significant challenges of scaling direct air capture facilities remain, particularly concerning capital investment and the development of geological storage site selection criteria.

- The role of dac in corporate net-zero commitments is solidifying, with companies increasingly looking for durable carbon removal verification standards. Projects leveraging advanced electrochemical dac system design principles demonstrate a nearly twofold improvement in energy efficiency compared to earlier thermal systems, directly impacting operational planning and financial models.

What are the key market drivers leading to the rise in the adoption of Direct Air Capture Industry?

- The market's growth is primarily driven by the increasing number of corporate net-zero commitments, which necessitate active carbon dioxide removal solutions.

- The primary driver propelling the direct air capture market is the global push toward climate change mitigation, underpinned by increasingly stringent corporate and national net-zero commitments. This has created strong demand for negative emission technology solutions.

- Supportive government policies, offering substantial financial incentives, have de-risked investments and spurred a 40% year-over-year increase in private funding for new projects. Technological advancements are also crucial, with ongoing innovations in sorbent materials and process designs.

- For example, new calcium oxide sorbent formulations have shown a 15% higher CO2 selectivity and durability, reducing operational expenditure.

- Similarly, the development of more efficient electrochemical cells and passive direct air capture systems is lowering the high capital expenditure that has traditionally been a barrier, making the technology more accessible for widespread deployment.

What are the market trends shaping the Direct Air Capture Industry?

- A prominent trend shaping the market is the discernible shift from pilot programs to the scaling up of commercial projects, reflecting growing confidence in the technology's viability for large-scale carbon removal.

- A significant trend in the direct air capture market is the increasing integration of facilities with renewable energy sources to ensure climate-beneficial operations. This synergy is critical for achieving true negative emissions. For instance, projects utilizing dedicated geothermal powered DAC have demonstrated a 90% lower operational carbon footprint compared to grid-powered alternatives.

- This move aligns with a broader decarbonization strategy and enhances the value of carbon credit procurement. Another key development is the diversification of carbon dioxide utilization pathways, with a focus on creating a circular carbon economy.

- The use of captured CO2 in low-carbon concrete and other carbon-negative building materials is gaining traction, with some applications showing a 25% lower lifecycle emission profile. These trends are supported by advancements in technologies like membrane capture medium and cryogenic DAC, which offer different advantages in purity and scalability.

What challenges does the Direct Air Capture Industry face during its growth?

- The industry's growth is significantly challenged by the high energy consumption inherent in direct air capture processes, impacting operational costs and scalability.

- A primary challenge for the direct air capture market is the high energy consumption per ton CO2 captured, which inflates operational costs and complicates efforts to ensure a net-negative carbon footprint. Some systems still require over 2,000 kWh per ton, which is 30% higher than industry targets.

- The substantial capital and operational costs (CapEx and OpEx) remain a significant hurdle, with the initial investment for a megaton-scale facility often exceeding that of comparable renewable energy projects by over 50%. Furthermore, the sorbent degradation rate necessitates periodic replacement, adding to long-term expenses.

- Infrastructure development for CO2 transport and sequestration, including identifying suitable sites for saline aquifer storage and building pipelines, is both capital-intensive and faces regulatory and public acceptance challenges, thus constraining the pace of deployment.

Exclusive Technavio Analysis on Customer Landscape

The direct air capture market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the direct air capture market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Direct Air Capture Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, direct air capture market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aircapture - Provides containerized direct air capture units leveraging a solid capture medium with polymeric amine sorbent, regenerated through temperature and vacuum swing processes for scalable deployment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aircapture

- AirMyne

- Avnos

- Capture6

- Carbon Collect

- CarbonCapture Inc.

- Carbyon

- Climeworks

- Deep Sky

- Heirloom Carbon Technologies

- Mission Zero Technologies

- Noya

- Octavia Carbon

- Origen Carbon

- Parallel Carbon

- Phlair

- RepAir

- Sirona Technologies

- Skytree

- Soletair Power

- Spiritus Technologies

- Ucaneo

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Direct air capture market

- In August, 2024, 1PointFive commenced construction on its Stratos direct air capture plant in Texas, which is projected to become the world's largest DAC facility.

- In September, 2024, Heirloom celebrated the activation of its direct air capture facility in California, which employs a novel limestone-based technology designed for enhanced energy efficiency and lower costs.

- In March, 2025, Mission Zero Technologies entered into a partnership with a cement and concrete producer to explore the utilization of captured carbon dioxide in low-carbon concrete production.

- In May, 2025, CarbonCapture Inc. announced a strategic agreement with clean energy provider Standard Power to explore powering its future direct air capture facilities with dedicated renewable energy.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Direct Air Capture Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 286 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 49.7% |

| Market growth 2025-2029 | USD 524323.3 thousand |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 45.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The direct air capture market is advancing beyond research and development into a phase of early commercialization, defined by a push for industrial-scale deployment. Key technological pathways, including solid sorbent-based DAC, liquid solvent-based DAC, and electrochemical DAC, are being refined to improve efficiency and reduce costs.

- The industry is focused on optimizing every stage, from the CO2 air contactor and sorbent regeneration cycle to final geological CO2 storage. The trend toward scaling up projects presents a critical boardroom decision, requiring significant capital allocation toward technologies like amine-based structured sorbents or hybrid direct air capture systems.

- Success hinges on achieving lower energy consumption through innovations such as temperature swing adsorption and vacuum swing regeneration. As companies scale, they are securing offtake agreements for carbon removal credits, which are essential for project financing.

- Firms adopting advanced sorbent technologies have reported up to a 20% improvement in capture rates, directly influencing their competitive positioning and ability to meet net-zero emissions technology targets through effective atmospheric carbon dioxide removal.

What are the Key Data Covered in this Direct Air Capture Market Research and Growth Report?

-

What is the expected growth of the Direct Air Capture Market between 2025 and 2029?

-

USD 524.32 million, at a CAGR of 49.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Solid sorbent-based DAC, Liquid solvent-based DAC, Electrochemical DAC, and Cryogenic DAC), Source (Electricity, and Heat), Application (Carbon capture and storage, and Carbon capture utilization and storage) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing corporate net-zero commitments, High energy consumption

-

-

Who are the major players in the Direct Air Capture Market?

-

Aircapture, AirMyne, Avnos, Capture6, Carbon Collect, CarbonCapture Inc., Carbyon, Climeworks, Deep Sky, Heirloom Carbon Technologies, Mission Zero Technologies, Noya, Octavia Carbon, Origen Carbon, Parallel Carbon, Phlair, RepAir, Sirona Technologies, Skytree, Soletair Power, Spiritus Technologies and Ucaneo

-

Market Research Insights

- The direct air capture market is characterized by rapid technological evolution and shifting economic drivers. The development of a circular carbon economy is reshaping investment priorities, with a focus on creating value from captured CO2. Innovations in CO2 as a feedstock are enabling new revenue streams, while enhanced oil recovery remains a viable, albeit debated, utilization pathway.

- Companies are achieving notable efficiency gains; for instance, advancements in sorbent materials have improved capture selectivity by up to 15%. Furthermore, process optimizations that integrate with renewable energy sources have demonstrated a potential 20% reduction in operational expenditures, bolstering project viability.

- This progress is critical as the industry moves toward megaton-scale carbon removal, where lifecycle emissions analysis informs both technological choices and policy incentives, driving the market toward more sustainable and economically sound solutions.

We can help! Our analysts can customize this direct air capture market research report to meet your requirements.

RIA -

RIA -