Dog Food Market Size 2024-2028

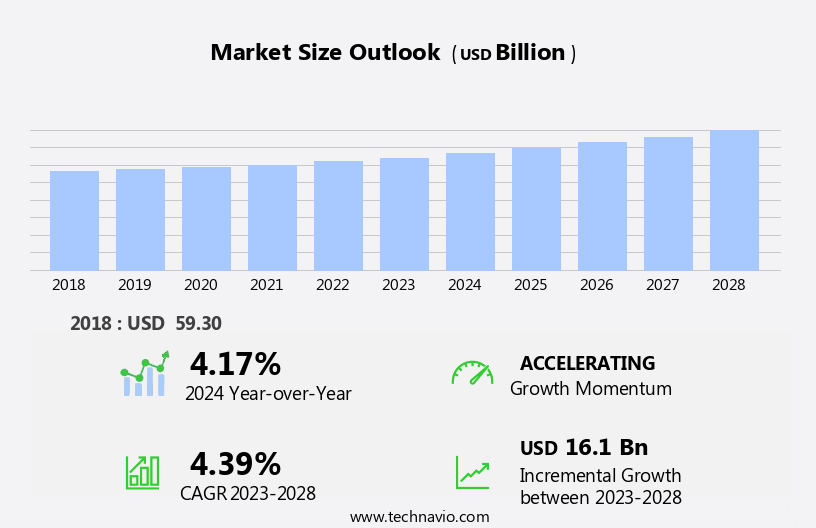

The dog food market size is forecast to increase by USD 16.1 billion, at a CAGR of 4.39% between 2023 and 2028.

- The market is driven by the rising trend of pet health awareness, leading to an increasing demand for premium and nutritious dog food options. Pet adoption rates continue to soar, fueled by the humanization of pets and their integration into families as companions. Additionally, changing lifestyle patterns and the busy work lives of urban populations have resulted in a growing preference for convenient, ready-to-serve dog food solutions. However, the market faces challenges in the form of stringent regulations governing pet food labeling and safety standards.

- Ensuring compliance with these regulations can be a significant obstacle for market entrants. Furthermore, the growing trend of natural and organic pet food may put pressure on companies to source high-quality, sustainable ingredients, increasing production costs. To capitalize on opportunities and navigate these challenges, companies must focus on innovation, sustainability, and transparency in their product offerings and business practices.

What will be the Size of the Dog Food Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, with ongoing innovations in ingredient sourcing, formulation, and processing techniques shaping the industry's landscape. For instance, sodium content levels and calorie density calculation are increasingly important considerations for pet owners seeking to maintain their pets' health. Antioxidant inclusion, mineral fortification, and gut microbiome impact are other key areas of focus. Dry kibble formulation undergoes pet food extrusion, ensuring optimal nutrient retention and palatability. Quality control measures, ingredient interaction, and shelf life extension are crucial aspects of manufacturing, while digestive health support, amino acid analysis, and allergen management are essential for meeting diverse consumer needs.

Food safety protocols, calcium phosphorus ratio, taurine content, crude fiber content, and palatability testing are integral parts of the production process. Canned food processing, meat by-product utilization, moisture content regulation, and pet food digestibility are additional areas of research and development. Prebiotic fiber types, fatty acid profile, protein source identification, probiotic strain selection, vitamin supplementation, and novel protein sources are some of the emerging trends in the market. The AAFCO statement plays a vital role in ensuring standardized nutritional labeling and kibble texture analysis. Industry growth is expected to reach 5% annually, driven by increasing pet ownership, rising consumer awareness, and advancements in pet nutrition technology.

For example, a leading pet food manufacturer reported a 12% increase in sales due to the introduction of a grain-free formulation with improved digestibility and gut health benefits.

How is this Dog Food Industry segmented?

The dog food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Dry dog food

- Dog treats and snacks

- Wet dog food

- Distribution Channel

- Offline

- Online

- Formulation

- Natural/Organic

- Grain-Free

- High-Protein

- Weight Management

- Price Range

- Premium

- Mid-Range

- Economy

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

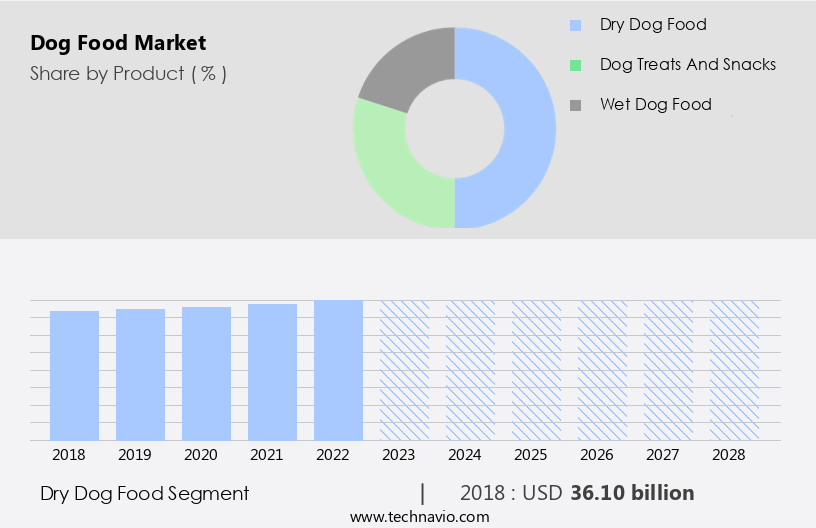

The dry dog food segment is estimated to witness significant growth during the forecast period.

In the dynamic pet food industry, dry kibble remains the dominant product category in 2023, catering to the nutritional needs of dogs with proteins, vitamins, and minerals. Packaging innovations and attractive designs are key trends, boosting sales growth. Manufacturers are expanding their consumer base through strategies like mergers and acquisitions. For instance, Hill's Pet Nutrition's acquisition of Nutriamo's Italian canned pet food manufacturing facility in May 2022. Mineral fortification and antioxidant inclusion are essential aspects of pet food production, ensuring optimal health support for pets. Sodium content levels are carefully managed to maintain a balance between taste and health.

Calorie density calculation is crucial for addressing the varying energy requirements of different dog breeds and sizes. Pet food extrusion and canned food processing techniques ensure the preservation of essential nutrients and palatability. Quality control measures are rigorously implemented to maintain consistency and safety. Probiotic strains and prebiotic fiber types are increasingly being used to support digestive health. Ingredient interaction and allergen management are crucial considerations to ensure the production of safe and effective pet food products. Shelf life extension is a significant concern, with moisture content regulation playing a vital role. Amino acid analysis and protein source identification are essential for ensuring the nutritional value of pet food.

The calcium phosphorus ratio is meticulously maintained to support bone health, while taurine content is included for heart health. Crude fiber content is monitored to ensure proper digestion, and vitamin supplementation is crucial for overall health and well-being. Grain-free formulations cater to the growing demand for alternative dietary needs, while novel protein sources are increasingly being explored to cater to diverse consumer preferences. Nutritional labeling is transparent and clear to help consumers make informed decisions. Kibble texture analysis ensures the right consistency for optimal pet satisfaction. The global pet food market is expected to grow by 5% annually, driven by increasing pet ownership and evolving consumer preferences for premium and nutritious pet food options.

The Dry dog food segment was valued at USD 36.10 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

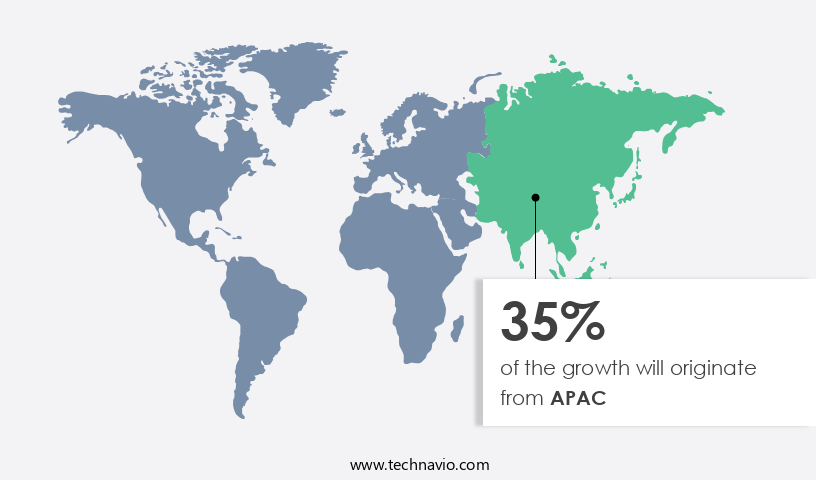

APAC is estimated to contribute 35% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The North American market is experiencing growth due to the convenience and increasing demand for these products. The US and Canada are significant markets for dog food production, with Canada being the leading importer, followed by the Bahamas and Honduras. Manufacturers are responding to consumer awareness by producing clean-label pet food, focusing on transparent ingredient sourcing. Sodium content levels and calorie density are crucial considerations in formulation, while antioxidants are included for health benefits. Dry kibble formulation undergoes pet food extrusion, and mineral fortification ensures proper nutrition. Gut microbiome impact is a key concern, leading to quality control measures and ingredient interaction studies.

Shelf life extension is achieved through various methods, including moisture content regulation and vitamin supplementation. AAFCO statements guide nutritional labeling, and novel protein sources are utilized for allergen management. Prebiotic fiber types and fatty acid profiles are essential for digestive health support, while the calcium phosphorus ratio and taurine content are closely monitored for balanced nutrition. Crude fiber content and palatability testing ensure proper texture and appeal. Canned food processing maintains nutritional value, and meat by-product utilization is a sustainable practice. Industry growth is expected to reach 5% annually, with a focus on food safety protocols and kibble texture analysis.

For instance, a leading manufacturer reduced sodium content by 20% in their dog food line, resulting in a 15% sales increase.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to increasing pet ownership and rising awareness about the importance of proper canine nutrition. One key trend in this market is the focus on advanced nutritional formulations that support gut health and optimize digestibility. Prebiotics, for instance, have gained popularity for their ability to positively impact the gut microbiota of dogs. Protein source is another crucial factor in dog food production. Crude fiber analysis methodology is essential to ensure optimal protein digestibility, as different protein sources may require varying fiber levels for effective digestion. Moreover, the choice of protein source can influence the fatty acid ratios in dog food, which should adhere to optimal levels for canine health. Amino acid balance is another critical aspect of dog food formulation. Vitamin E and antioxidant stabilization are necessary for maintaining the freshness and nutritional value of the food. Mineral supplementation is essential for optimal health, and probiotic strain viability testing guarantees the efficacy of beneficial bacteria in the food. Dry kibble processing parameters and canned food sterilization methods significantly impact the final product's quality. Shelf life prediction modeling and pet food palatability score testing are essential to ensure the food remains appetizing and safe for consumption. Ingredient sourcing sustainability and quality control testing frequency are increasingly important considerations for pet food manufacturers. Nutritional labeling requirements, as outlined by AAFCO nutrient profile guidelines, ensure transparency and consistency in the market. Meat by-product ingredient analysis and novel protein source digestibility testing are also crucial for maintaining the highest standards of safety and efficacy. Kibble texture and density control and calorie density adjustment strategies are essential to cater to various dog breeds and sizes. By focusing on these aspects, dog food manufacturers can create high-quality, nutritious, and appealing products that meet the evolving needs of the global pet food market.

What are the key market drivers leading to the rise in the adoption of Dog Food Industry?

- The significant growth of the market is attributable to the rising awareness and prioritization of pet health.

- The pet industry continues to thrive as pets are increasingly viewed as family members, leading to an increased focus on providing them with a healthy lifestyle. With disposable income on the rise, pet owners are more inclined to invest in premium pet food options. This trend is driving market growth as companies expand their product ranges to cater to the growing concern for pets' health.

- In March 2023, a leading pet food company introduced new multivitamin soft chews for dogs, designed to support their immunity, digestion, and joint health. According to industry reports, the global pet food market is expected to grow by over 5% annually in the coming years, reflecting the significant demand for high-quality pet food products.

What are the market trends shaping the Dog Food Industry?

- The trend in the market involves the adoption of pets and their humanization. Pet adoption and humanization are current market trends.

- The pet food market has experienced significant growth in recent years due to the increasing humanization of pets and rising pet ownership rates. According to the American Pet Products Association, pet ownership in the United States grew by 5% in 2020, with over 160 million pets residing in American households. This trend is expected to continue, with the pet food market projected to grow by 11% in the next five years. The humanization of pets has led to a heightened focus on pet health and well-being, resulting in a surge in demand for premium pet food products. These products often contain natural ingredients and cater to specific dietary needs, such as grain-free, gluten-free, and allergy-friendly options.

- The integration of technology, such as smart feeding systems and personalized nutrition plans, is also driving market growth. Moreover, the increasing adoption of pets in emerging economies, particularly in Asia and South America, is contributing to the robust growth of the pet food market. The COVID-19 pandemic has further accelerated this trend, as people have spent more time at home and have been able to provide better care for their pets.

What challenges does the Dog Food Industry face during its growth?

- The urban population's shifting lifestyle habits and demanding work schedules pose a significant challenge to the industry's growth.

- The global pet ownership trend is on the rise, with an increasing number of working individuals unable to dedicate sufficient time to their pets due to demanding work schedules. According to The World Bank Group, women's labor force participation reached approximately 39% in 2019. This statistic, coupled with the emergence of nuclear families and altered lifestyle patterns, necessitates a solution for pets' dietary needs when their owners are unavailable. The pet food market has responded to this demand by offering convenient and nutritious options, such as premium dry food and wet food in various portion sizes.

- For instance, a leading pet food brand reported a 15% increase in sales of their convenient, portioned wet food line in 2020. Furthermore, the pet food industry is projected to grow by over 5% annually, indicating a robust future for this market.

Exclusive Customer Landscape

The dog food market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dog food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, dog food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bravo LLC - This company specializes in providing a range of high-quality dog food options, including treats, frozen raw diets, and chews, catering to diverse canine nutritional needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bravo LLC

- Canature Processing Ltd.

- Carnivore Meat Co. LLC

- Champion Petfoods Holding Inc.

- Fresh Is Best

- Grandma Lucys LLC

- Hills Pet Nutrition Inc.

- J RETTENMAIER and SOHNE GmbH and Co KG

- Mars Inc.

- Miracle Pet

- Natural Pet Food Group

- Natures Diet

- Nestle SA

- NRG Plus Ltd.

- Primal Pet Foods Inc.

- SCHELL and KAMPETER Inc.

- Stella and Chewys LLC

- Steves Real Food

- The J.M Smucker Co.

- Wellness Pet Co. Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dog Food Market

- In January 2024, Mars, Incorporated, a leading global food company, announced the launch of a new line of grain-free dog food, "Mars Veterinary Diets," in partnership with Banfield Pet Hospital. This collaboration aimed to provide veterinary-recommended options for pets with food sensitivities (Source: Mars, Incorporated Press Release).

- In March 2024, Nestlé Purina PetCare Company, a subsidiary of Swiss multinational food and drink processing conglomerate Nestlé, acquired a significant stake in Open Farm, a Canadian pet food company known for its transparency and sustainable farming practices. The financial terms of the deal were undisclosed (Source: Nestlé Purina PetCare Company Press Release).

- In May 2024, Blue Buffalo, a US-based pet food manufacturer, announced a strategic partnership with The Petco Foundation, a nonprofit organization dedicated to finding lifelong, loving homes for animals. The collaboration focused on supporting pet adoption and animal welfare initiatives (Source: Blue Buffalo Press Release).

- In April 2025, Royal Canin, a French pet food company, received approval from the European Commission for its new production facility in Poland. The ⬠150 million investment will increase the company's European production capacity and support its growth in the European market (Source: Royal Canin Press Release).

Research Analyst Overview

- The market for dog food continues to evolve, with ongoing developments in various sectors shaping its dynamics. Fecal score assessments and dry matter content determination are crucial aspects of food safety regulations, ensuring optimal nutrient absorption and digestive health. Flavor enhancer selection and natural preservative use cater to discerning pet owners' preferences, while regulatory compliance remains a priority. Protein bioavailability and life stage nutrition, including weight management formulas, hypoallergenic recipes, sensitive stomach formulas, puppy growth formulas, senior dog nutrition, dental health chews, and joint health supplements, reflect the diverse needs of the pet population.

- Industry growth is anticipated to reach 6% annually, with significant focus on supply chain management, gut health biomarkers, and digestive enzyme activity. For instance, a leading pet food manufacturer reported a 10% increase in sales due to the introduction of a new, high-fiber source formula.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dog Food Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.39% |

|

Market growth 2024-2028 |

USD 16.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.17 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Dog Food Market Research and Growth Report?

- CAGR of the Dog Food industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the dog food market growth of industry companies

We can help! Our analysts can customize this dog food market research report to meet your requirements.

RIA -

RIA -