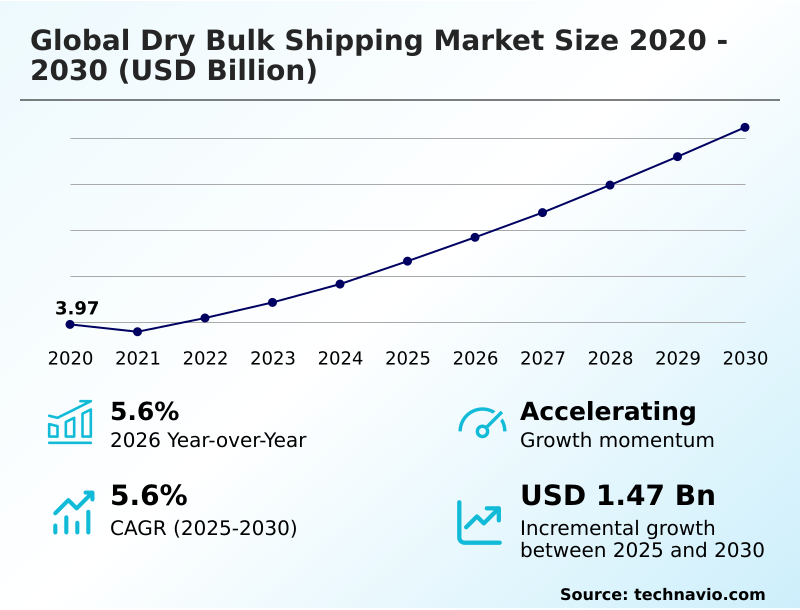

Dry Bulk Shipping Market Size 2026-2030

The dry bulk shipping market size is valued to increase by USD 1.47 billion, at a CAGR of 5.6% from 2025 to 2030. Expansion of global bauxite and aluminum supply chains will drive the dry bulk shipping market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 54.1% growth during the forecast period.

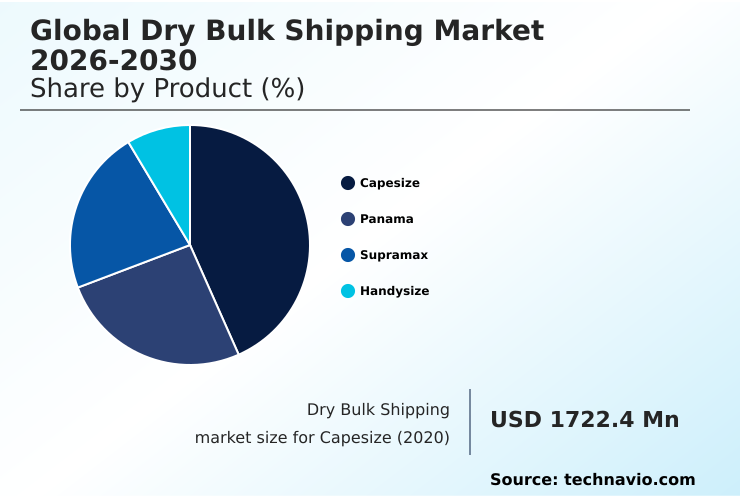

- By Product - Capesize segment was valued at USD 1.92 billion in 2024

- By Type - Iron ore segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.15 billion

- Market Future Opportunities: USD 1.47 billion

- CAGR from 2025 to 2030 : 5.6%

Market Summary

- The Dry Bulk Shipping Market is undergoing a significant structural recalibration, moving beyond its role as a simple barometer of industrial health to become a focal point of technological and regulatory change. The sector remains fundamental to the global economy, facilitating the movement of essential raw materials for manufacturing and agriculture.

- However, its trajectory is now shaped by a complex interplay of forces. The industrial appetite of emerging economies continues to fuel demand, but this is tempered by volatile freight rates and an urgent need for fleet modernization.

- A key scenario is the shipowner's dilemma: investing millions in retrofitting an older vessel to meet new decarbonization mandates, such as the Carbon Intensity Indicator (CII), or commissioning a newbuild with unproven alternative marine fuels technology like ammonia-ready engines. This decision carries immense financial risk, as choosing the wrong path could lead to stranded assets.

- Simultaneously, geopolitical instability is rerouting traditional maritime logistics chains, increasing voyage lengths and tightening vessel supply. This dynamic landscape necessitates a strategic shift toward operational resilience, advanced voyage planning optimization, and investment in technologies that support sustainable shipping practices to maintain profitability.

What will be the Size of the Dry Bulk Shipping Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Dry Bulk Shipping Market Segmented?

The dry bulk shipping industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

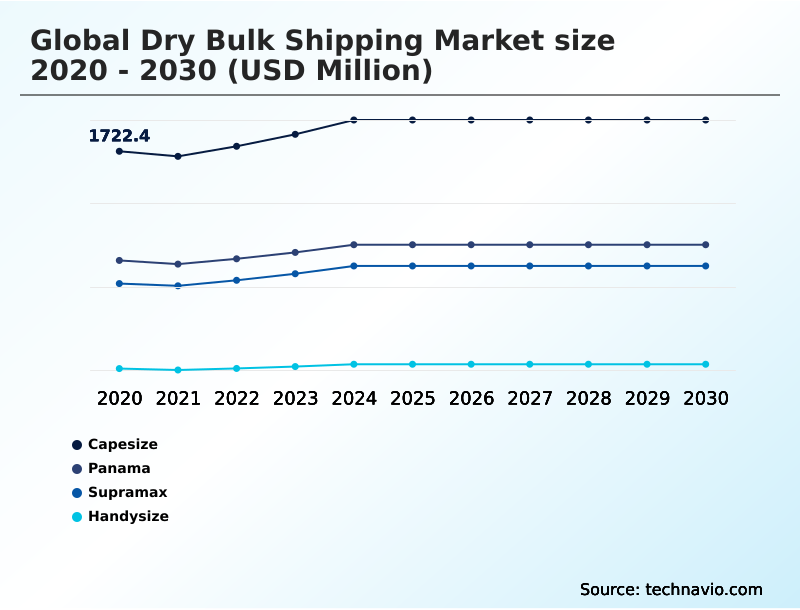

- Product

- Capesize

- Panama

- Supramax

- Handysize

- Type

- Iron ore

- Coal

- Grains

- Bauxite

- Others

- Service type

- Gearless bulk carriers

- Conventional bulkers

- Self-dischargers

- OBO

- Bulker lakers

- Geography

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- The Netherlands

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- APAC

By Product Insights

The capesize segment is estimated to witness significant growth during the forecast period.

The capesize segment, comprising the largest vessels, is pivotal for long-haul trade routes, primarily facilitating iron ore transport. These ships rely on deep-water port facilities, and their demand is shaped by industrial output in major economies.

A critical shift is underway as new mining projects commence, creating new trans-oceanic trade routes that structurally increase tonne-mile demand, providing a long-term catalyst for fleet utilization even amid geopolitical trade disruption.

This evolution reshapes global supply chains and drives port infrastructure modernization. Concurrently, decarbonization mandates are pushing operators to invest in dual-fuel technologies, with smart port technologies enhancing efficiency.

The segment's reliance on a few key commodities, like high-grade ore with over 65% iron content, underscores its strategic importance in global industrial logistics.

The Capesize segment was valued at USD 1.92 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

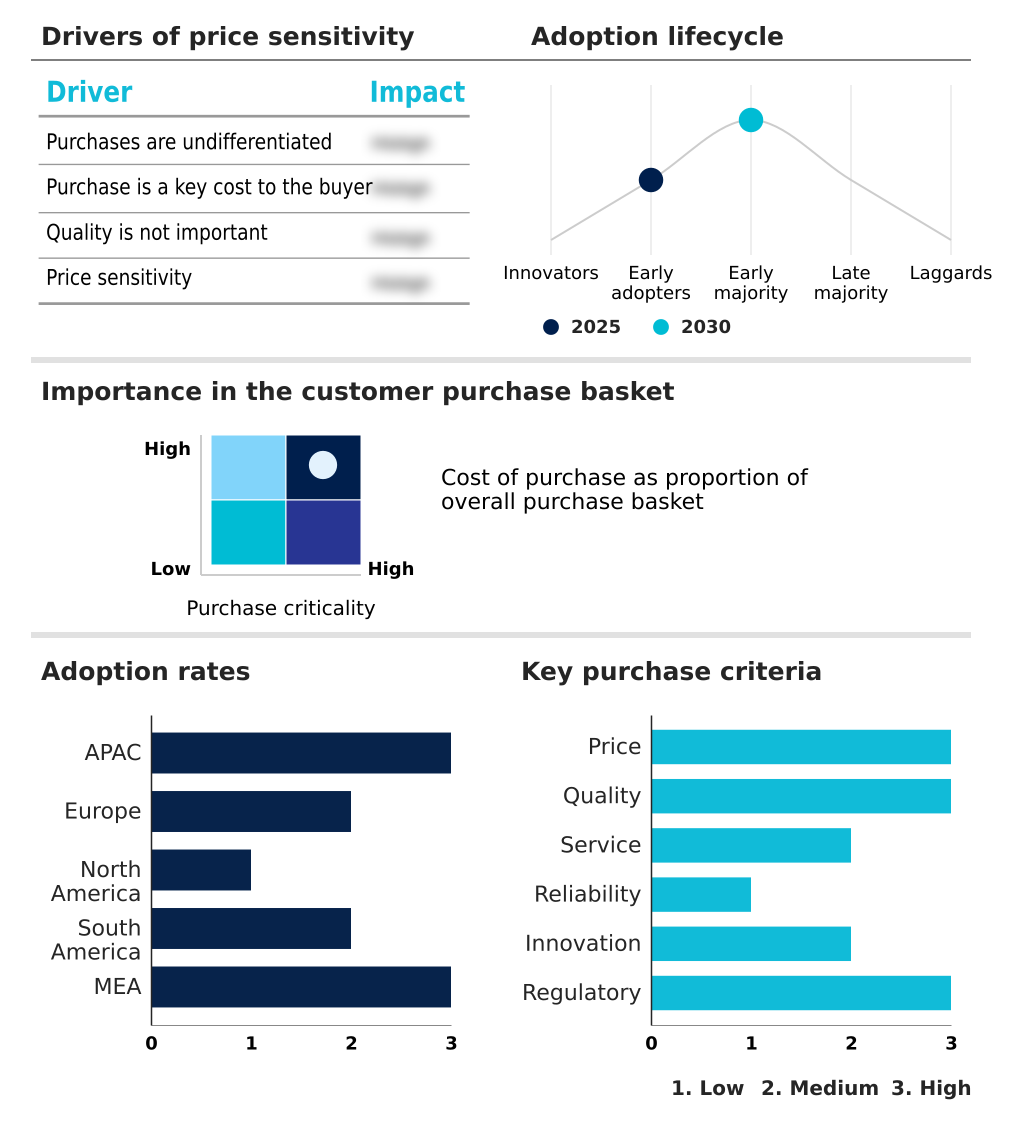

APAC is estimated to contribute 54.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Dry Bulk Shipping Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the dry bulk shipping market is dominated by APAC, which accounts for over 54% of the global opportunity, driven by the vast industrial demand from China and India.

This region's consumption of iron ore and coal sets the tone for the global dry bulk freight market. Europe and North America represent the next significant tiers, contributing approximately 19.7% and 19.6% respectively.

These mature markets are pivotal for grain shipments and specialized bulk carriers, with a strong focus on sustainable shipping practices and adherence to global shipping regulations.

The North American market, in particular, leverages sophisticated inland waterway logistics to connect agricultural heartlands with global seaborne commodity trade routes.

South America and the Middle East and Africa, while smaller, are crucial supply hubs for minerals and are witnessing investment in deep-water port facilities to support long-haul trade routes.

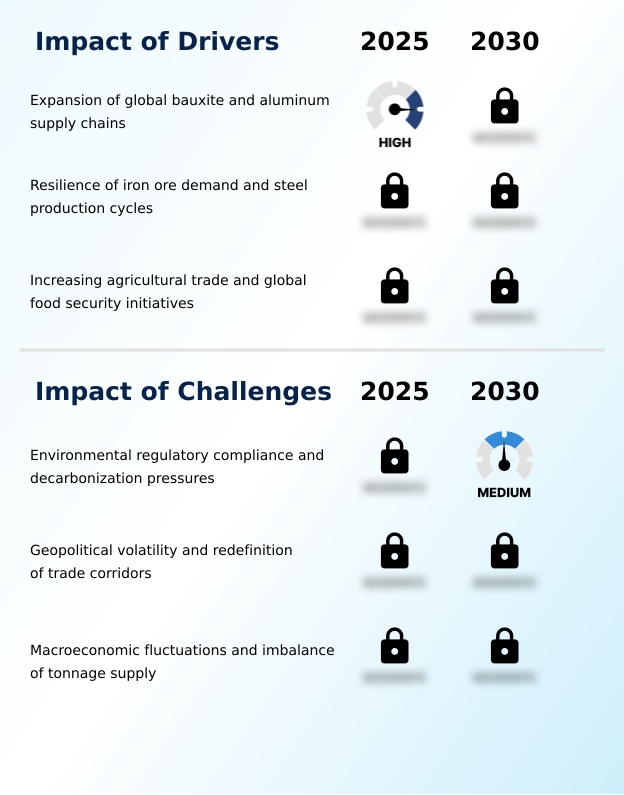

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the modern dry bulk sector requires a deep understanding of interconnected strategic challenges and opportunities. The impact of the simandou project on capesize demand is a clear example, fundamentally altering long-haul trade dynamics and putting pressure on existing port infrastructure.

- At the same time, the industry grapples with the pervasive decarbonization challenges for dry bulk shipping, forcing a reevaluation of vessel design and propulsion systems. This has spurred investment in eco-efficient bulk carriers and accelerated research into LNG as a transition fuel for shipping.

- Technology adoption in port-to-ship coordination is becoming a key differentiator, with many operators integrating digital twins in port operations to reduce turnaround times. Optimizing fleet utilization with AI is no longer a futuristic concept but a present-day necessity for managing freight rate volatility in shipping.

- However, geopolitical risks in maritime trade corridors remain a persistent threat, complicating the future of coal transport in dry bulk and reshaping bauxite shipping routes from guinea to china. The industry also faces the structural challenges of newbuild tonnage oversupply, which can erode profitability.

- In this context, the role of panamax vessels in global grain trade remains a stabilizing force, alongside the impact of agricultural trade on shipping demand. Fleet management now involves complex decisions regarding the effects of imo regulations on vessel design, the strategic deployment of a supramax vessel for minor bulk transport, and a handysize vessel deployment for regional trade.

- Effective maritime supply chain risk mitigation strategies are paramount, as is improving cargo handling with geared bulkers. This complex environment has seen operators face an influx of new capacity, the highest since 2020, making operational efficiency more critical than ever.

What are the key market drivers leading to the rise in the adoption of Dry Bulk Shipping Industry?

- The expansion of global bauxite and aluminum supply chains, driven by demand from green energy and automotive sectors, serves as a primary driver for the market.

- Market growth is propelled by robust demand from key industrial and agricultural sectors, alongside the structural expansion of specific commodity supply chains.

- The seaborne bauxite trade has become a critical driver, with exports from key regions expected to grow by more than 8% annually, fueling the need for specialized bulk carriers on long-haul trade routes.

- This is complemented by the resilience of iron ore transport, a foundational component of the dry bulk freight market. Furthermore, expanding global agricultural trade, driven by food security initiatives, ensures steady demand for panamax carriers and supramax vessels.

- Bulk commodity exports from certain North American ports have seen a nearly 6% rise, underscoring the critical role of established logistics hubs.

- This diversified demand underscores the need for ongoing vessel fleet optimization and strategic fleet renewal strategy programs to meet evolving cargo requirements.

What are the market trends shaping the Dry Bulk Shipping Industry?

- A key market trend is the emergence of West African high-grade ore exports. This development is structurally increasing tonne-mile demand, particularly for large-capacity vessels.

- Market dynamics are increasingly shaped by the geographic diversification of commodity sources and the integration of advanced technologies. A primary trend is the development of new high-grade ore projects, which structurally increases tonne-mile demand for capesize vessels as voyages become approximately three times longer than traditional routes.

- This shift, driven by steelmakers seeking ore with over 65% iron content to boost efficiency, supports freight rate stability. Concurrently, the push for operational efficiency is accelerating the adoption of autonomous navigation and real-time port visibility tools. This move toward automation, coupled with the integration of digital twin technology, enhances the predictability of the maritime logistics chain.

- The integration of these systems has been shown to improve arrival time precision, reducing costly time spent at anchor by up to 20% in digitally advanced ports.

What challenges does the Dry Bulk Shipping Industry face during its growth?

- Stringent environmental regulatory compliance and mounting decarbonization pressures present a significant challenge affecting operational costs and investment decisions across the industry.

- The market faces significant headwinds from stringent global shipping regulations and macroeconomic volatility. The intensifying pressure for environmental compliance, particularly the mandate for shipping companies to provide 100% European Union Allowances for emissions on intra-bloc voyages, introduces direct financial burdens and reporting complexities.

- This is compounded by escalating geopolitical volatility, which has contributed to a 12.3% year-on-year increase in shipping corridor stress, forcing costly vessel diversions and increasing maritime risk management costs. Furthermore, a persistent imbalance between vessel supply and demand, exacerbated by a massive influx of newbuild vessel delivery, creates downward pressure on charter rates.

- This vessel oversupply impact is a structural challenge that threatens to erode profitability, forcing operators to focus on efficiency to navigate an increasingly crowded market.

Exclusive Technavio Analysis on Customer Landscape

The dry bulk shipping market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dry bulk shipping market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Dry Bulk Shipping Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, dry bulk shipping market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AP Moller Maersk AS - Provides integrated dry bulk shipping for energy and industrial commodities, complementing its extensive container transport operations and enhancing global supply chain logistics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AP Moller Maersk AS

- Berge Bulk Ltd.

- Cargill Inc.

- COSCO Shipping Ports Ltd.

- Diana Shipping Inc.

- Egon Oldendorff Management GmbH

- Gearbulk Holding AG

- Genco Shipping and Trading Ltd.

- Golden Ocean Group Ltd.

- Grindrod Shipping Holdings Ltd

- Hapag Lloyd AG

- HMM Europe Ltd.

- John Swire and Sons Ltd.

- Kawasaki Kisen Kaisha Ltd.

- Mitsui O.S.K. Lines Ltd.

- Nippon Yusen Kabushiki Kaisha

- Pacific Basin Shipping Ltd.

- Pan Ocean Co. Ltd.

- Precious Shipping Public Co.

- Star Bulk Carriers Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dry bulk shipping market

- In December, 2025, Golden Ocean Group Ltd. merged with CMB.TECH, creating a scaled-up entity focused on decarbonization and future-proof shipping solutions, as reported in industry analyses of maritime consolidation trends.

- In November, 2025, the first commercial cargo from the Simandou project, totaling nearly two hundred thousand tonnes of high-grade iron ore, arrived in China, marking the operational start of a major new trade lane from Guinea, according to commodity trade reports.

- In August, 2025, the United States government officially removed the USD 800 de minimis tax exemption for low-value imports, a policy shift that significantly altered customs documentation and overhead costs for bulk-related maritime logistics services, as outlined in federal trade notices.

- In March, 2025, the finalization of the UK-India Free Trade Agreement catalyzed a surge in demand for gearless bulk carriers, driven by reduced tariffs on industrial raw materials and increased import quotas for Indian steel manufacturers, according to government trade publications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dry Bulk Shipping Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.6% |

| Market growth 2026-2030 | USD 1466.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.6% |

| Key countries | China, Japan, South Korea, India, Indonesia, Australia, Greece, Germany, Norway, UK, The Netherlands, Spain, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, South Africa, UAE, Egypt and Morocco |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The dry bulk shipping market is navigating a period of profound transformation, where operational decisions are increasingly dictated by decarbonization mandates and technological advancements. The core function of facilitating iron ore transport and coal shipments remains, but the methods and associated risks have evolved.

- A central theme is the industry's response to the Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII), which compel a shift toward alternative marine fuels and significant investment in fleet modernization. This includes the adoption of ammonia-ready engines and liquefied natural gas (LNG) propulsion.

- Concurrently, digitalization is reshaping the landscape through autonomous navigation and real-time port visibility, with digital twin technology enabling predictive maintenance and vessel fleet optimization. These tools are crucial for managing persistent freight rate volatility. The expansion of bauxite trade and resilient grain shipments provide diversified demand streams, supported by geared bulk carriers and specialized vessels for minor bulk commodities.

- Boardroom-level strategy is now heavily influenced by maritime risk, with corridor stress metrics increasing by over 12%, forcing a greater focus on ballast water management and port infrastructure modernization to ensure supply chain integrity.

What are the Key Data Covered in this Dry Bulk Shipping Market Research and Growth Report?

-

What is the expected growth of the Dry Bulk Shipping Market between 2026 and 2030?

-

USD 1.47 billion, at a CAGR of 5.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Capesize, Panama, Supramax, and Handysize), Type (Iron ore, Coal, Grains, Bauxite, and Others), Service Type (Gearless bulk carriers, Conventional bulkers, Self-dischargers, OBO, and Bulker lakers) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Expansion of global bauxite and aluminum supply chains, Environmental regulatory compliance and decarbonization pressures

-

-

Who are the major players in the Dry Bulk Shipping Market?

-

AP Moller Maersk AS, Berge Bulk Ltd., Cargill Inc., COSCO Shipping Ports Ltd., Diana Shipping Inc., Egon Oldendorff Management GmbH, Gearbulk Holding AG, Genco Shipping and Trading Ltd., Golden Ocean Group Ltd., Grindrod Shipping Holdings Ltd, Hapag Lloyd AG, HMM Europe Ltd., John Swire and Sons Ltd., Kawasaki Kisen Kaisha Ltd., Mitsui O.S.K. Lines Ltd., Nippon Yusen Kabushiki Kaisha, Pacific Basin Shipping Ltd., Pan Ocean Co. Ltd., Precious Shipping Public Co. and Star Bulk Carriers Corp.

-

Market Research Insights

- The dry bulk shipping market is defined by a dynamic interplay between supply-side pressures and evolving demand patterns. A critical factor is the persistent vessel oversupply impact, which often suppresses earnings, even as operators achieve greater cargo handling efficiency.

- This imbalance is compounded by geopolitical trade disruption, which has led to a 12.3% increase in shipping corridor stress, complicating voyage planning optimization and increasing operational risks. Concurrently, demand is being reshaped by regional trade agreements and a focus on maritime supply chain resilience.

- For instance, enhanced inland waterway logistics in North America have contributed to a 6% rise in bulk commodity exports from key ports, highlighting the importance of integrated transport networks. Operators are responding by accelerating fleet renewal strategy programs and adopting smart port technologies to improve turnaround times and navigate this complex environment.

We can help! Our analysts can customize this dry bulk shipping market research report to meet your requirements.

RIA -

RIA -