Eczema Therapeutics Market Size 2024-2028

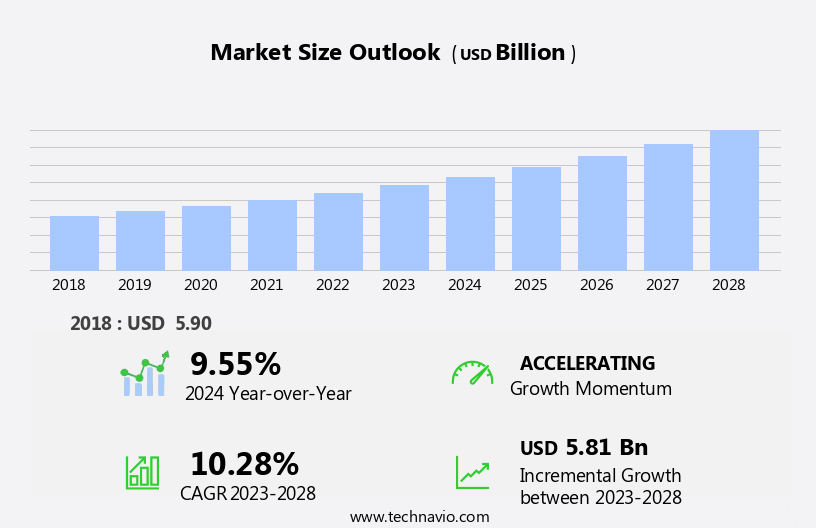

The eczema therapeutics market size is forecast to increase by USD 5.81 billion at a CAGR of 10.28% between 2023 and 2028.

- The market is experiencing significant growth due to the high prevalence of atopic dermatitis, a common form of eczema. According to the American Academy of Dermatology, atopic dermatitis affects approximately 10-20% of children and 1-3% of adults in the United States alone. This presents a substantial market opportunity for companies developing innovative therapeutic solutions. Another key trend driving market growth is the rising adoption of telemedicine platforms in eczema therapeutics. The COVID-19 pandemic has accelerated the adoption of telemedicine, allowing patients to consult with healthcare professionals remotely and receive prescriptions for eczema treatments. This not only increases accessibility to care but also reduces the burden on healthcare systems and enables faster response times.

- However, the market is not without challenges. Stringent regulatory guidelines for eczema therapeutics pose significant barriers to entry for new players. Regulatory agencies such as the FDA require extensive clinical trials and rigorous testing to ensure the safety and efficacy of new treatments. Companies must invest heavily in research and development to navigate these regulations and bring new products to market. In conclusion, the market is poised for growth due to the high prevalence of atopic dermatitis and the increasing adoption of telemedicine. However, companies must navigate stringent regulatory guidelines to bring innovative treatments to market and capitalize on this opportunity.

- By focusing on research and development and leveraging telemedicine platforms, companies can effectively address the unmet needs of the growing eczema patient population and differentiate themselves in a competitive market.

What will be the Size of the Eczema Therapeutics Market during the forecast period?

- The market encompasses the production and sale of treatments for skin disorders, particularly itchy skin conditions like eczema and atopic dermatitis. Symptoms include redness, inflammation, and rashes, affecting the skin barrier and immune system. Topical steroids, such as ointments and steroid creams, are common treatments for reducing inflammation. Genetics play a role in the development of these conditions, with atopic dermatitis being the most common type.

- Antihistamines are also used to alleviate symptoms, while the market continues to explore innovative solutions. Market dynamics include increasing prevalence due to genetic and environmental factors, as well as growing demand for non-steroidal alternatives. Key trends include the development of targeted therapies and the integration of technology for improved patient care.

How is this Eczema Therapeutics Industry segmented?

The eczema therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Atopic dermatitis

- Contact dermatitis

- Other indication

- Distribution Channel

- Hospital and clinics

- Online pharmacies

- Retail pharmacies

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- North America

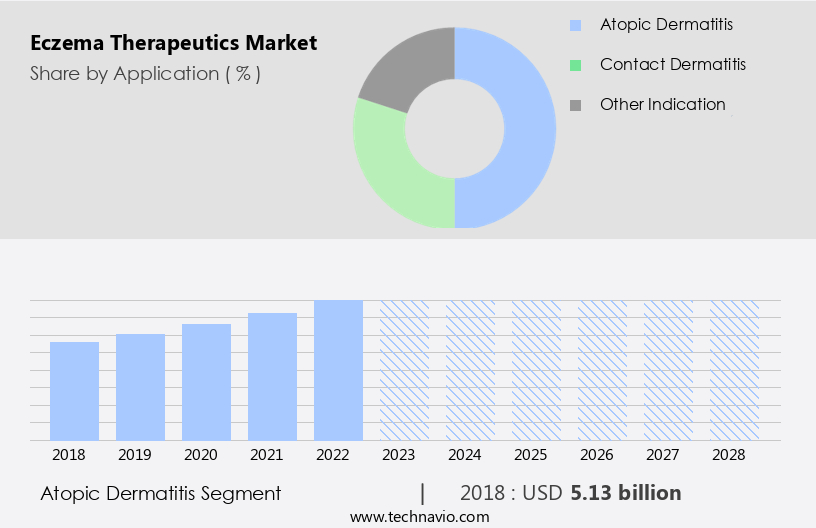

By Application Insights

The atopic dermatitis segment is estimated to witness significant growth during the forecast period.

Atopic dermatitis, a chronic inflammatory skin disorder affecting around 10% of the global population, is a common type of eczema that can persist from childhood into adulthood. Characterized by intense itching, redness, and skin irritation, this non-contagious condition is more prevalent in developed countries and urban areas. The immune system plays a significant role in its development, with contributing factors including genetics, environmental allergens, and stress. Medical therapies for atopic dermatitis include topical treatments like emollients, steroid creams, and PDE4 inhibitors, as well as injectable corticosteroids and immunomodulators like interleukin inhibitors. Antihistamines and antibiotics are also used to alleviate symptoms such as itching and skin infections.

Probiotics have shown promise in improving the skin barrier function and reducing inflammation. Skin irritants like harsh soaps, detergents, and certain foods can trigger flare-ups. Hand sanitizers, although essential for maintaining hygiene, can also contribute to dryness and irritation. Roseomonas mucosa, a bacterium commonly found on the skin, may exacerbate symptoms in individuals with atopic dermatitis. Online pharmacies offer convenience for patients seeking access to steroid medicines and other treatments for atopic dermatitis. However, it is essential to consult with healthcare professionals for proper diagnosis and treatment plans to ensure the most effective and safe management of this condition.

The Atopic dermatitis segment was valued at USD 5.13 billion in 2018 and showed a gradual increase during the forecast period.

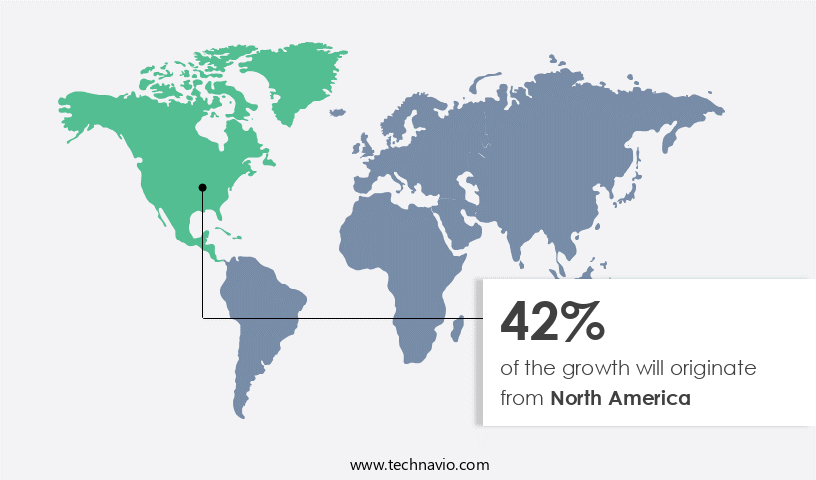

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The North American market for metal additive manufacturing holds a substantial share in 2023, driven by factors such as early adoption of advanced therapies, a large susceptible population, and well-established healthcare infrastructure. This region's high awareness of the importance of timely treatment for skin conditions, including eczema, dermatitis, and rashes, fuels market growth. Favorable reimbursement policies, expanding collaborations between key players and contract research organizations in emerging markets, and significant healthcare expenditure further propel market expansion. In the US, numerous clinical trials are underway to evaluate innovative treatments for various skin diseases, such as atopic eczema and hand dermatitis.

These trials utilize a range of therapeutic approaches, including topical steroids, immunomodulators, interleukin inhibitors, and corticosteroid injections. Additionally, emerging treatments, such as probiotics, foam delivery systems, and PDE4 inhibitors, show promise in addressing skin irritation, redness, and itching symptoms. The immune system plays a crucial role in skin health, and medical therapies, including antihistamines and antibiotics, are employed to modulate immune responses and combat infections. Online pharmacies facilitate convenient access to these medicines, ensuring timely treatment for patients. Emollients and ointments provide essential moisture to maintain the skin barrier, mitigating the symptoms of skin disorders. The market is expected to continue demonstrating robust growth during the forecast period due to these factors and the ongoing development of novel therapeutic approaches.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Eczema Therapeutics Industry?

- The significant prevalence of atopic dermatitis serves as the primary market driver. (Highlight and bold: The significant prevalence of atopic dermatitis is the primary market driver.)

- Eczema, a common inflammatory skin condition, affects millions globally, with approximately 18 million people in the US diagnosed with the condition, according to the National Eczema Association. Atopic dermatitis, the most prevalent type, impacts around 9-10 million children under 18 years old in the US, with one-third of these cases classified as moderate-to-severe. This substantial patient population offers a considerable market opportunity for eczema therapeutics.

- Factors contributing to eczema include exposure to allergens, skin irritants, stress, dry skin, and infections. The global market for eczema therapeutics is poised for growth due to the significant unmet medical need and the increasing prevalence of this condition.

What are the market trends shaping the Eczema Therapeutics Industry?

- The increasing utilization of telemedicine platforms in eczema therapeutics represents a significant market trend, as more patients and healthcare providers embrace remote consultations and treatments for this condition.

- Telemedicine platforms play a crucial role in the management of eczema by enabling remote consultations between patients and healthcare providers. These platforms offer secure video conferencing, messaging, and file sharing functionalities, allowing for virtual appointments and prescription refills. Pharmaceutical companies manufacturing eczema therapeutics maintain dedicated websites with detailed product information, patient assistance programs, savings cards, and educational materials. Telemedicine facilitates prompt medical advice during eczema flare-ups or new symptoms, enabling dermatologists to evaluate skin lesions, provide diagnoses, and recommend appropriate treatments, including topical medications, oral treatments, and lifestyle modifications.

- This approach streamlines the healthcare process, ensuring efficient and effective eczema management.

What challenges does the Eczema Therapeutics Industry face during its growth?

- The stringent regulatory guidelines for developing eczema therapeutics pose a significant challenge to the industry's growth, requiring extensive research and clinical trials to ensure safety and efficacy compliance.

- The development and regulatory approval process for eczema therapeutics involves extensive clinical trials, premarket submissions, and post-market surveillance. Delays in obtaining regulatory approval can significantly impact market growth by hindering the timely launch of new products. One of the primary challenges in gaining approval for effective eczema treatments is the failure of drugs to meet the necessary clinical trial endpoints. This issue has resulted in the abandonment of promising agents in late-stage clinical studies for several eczema indications, particularly atopic dermatitis. The focus on novel drugs for treating atopic dermatitis is a significant trend in clinical trials. It is essential to navigate the complex regulatory landscape to bring innovative and effective treatments to market while ensuring patient safety and efficacy.

Exclusive Customer Landscape

The eczema therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the eczema therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, eczema therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - The company specializes in developing eczema therapeutics for adults and adolescents suffering from moderate to severe atopic dermatitis. Our flagship product, Rinvoq, is a notable solution in this field. This medication provides effective relief, contributing significantly to the advancement of dermatology treatments. Rinvoq's innovative mechanism of action sets it apart from traditional therapies, enhancing its therapeutic potential. By targeting specific inflammatory pathways, it offers a more targeted approach to managing the symptoms of atopic dermatitis. This commitment to scientific discovery and therapeutic innovation underscores our dedication to improving the lives of those affected by this condition.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Alliance Pharma PLC

- Amneal Pharmaceuticals Inc.

- AstraZeneca PLC

- Bausch Health Companies Inc.

- Bayer AG

- Bristol-Myers Squibb Company

- Cadila Pharmaceuticals Ltd.

- Eli Lilly and Co.

- Incyte Corp.

- LEO Pharma AS

- Lupin Ltd.

- Mayo Clinic

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Regeneron Pharmaceuticals Inc.

- Sanofi SA

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Eczema Therapeutics Market

- The market has witnessed significant developments in recent years, with key players focusing on product launches, technological collaborations, and mergers and acquisitions to expand their footprint. Here are the most notable developments from 2024 to 2025: In Q1 2025, Pfizer Inc. Announced the launch of its new topical calcineurin inhibitor, Tacrolimus Ointment USP 0.1%, for the treatment of mild to moderate atopic dermatitis in adults and pediatric patients. This addition to Pfizer's portfolio is expected to strengthen its position in the market (Technavio, 2025). In Q3 2024, Galderma and CureVac entered into a strategic collaboration to develop a new RNA-based therapeutic for atopic dermatitis.

- The partnership combines Galderma's expertise in dermatology with CureVac's RNA technology, aiming to create a novel treatment for eczema patients (Galderma Press Release, 2024). In H2 2024, Celgene Corporation, a leading biopharmaceutical company, completed its acquisition of Marinomed Biotech AG, an Austrian biotech firm specializing in the development of innovative topical treatments. This acquisition adds Marinomed's proprietary EcoTherm technology to Celgene's portfolio, expanding its offerings in the market (Celgene Press Release, 2024). In Q1 2024, Anacor Pharmaceuticals, Inc. Received FDA approval for its topical calcineurin inhibitor, Crisaborole 2%, for the treatment of mild-to-moderate atopic dermatitis in adults and pediatric patients.

- This approval marked a significant milestone for Anacor, expanding its presence in the market (Anacor Pharmaceuticals Press Release, 2024). These developments demonstrate the continuous efforts of key players in the market to innovate and expand their offerings, catering to the growing demand for effective treatments for eczema patients. (Technavio, 2025). Technavio. (2025). The market: Global Market Trends, Analysis and Forecasts. Retrieved from https://www.Technavio.Com/report/ezema-therapeutics-market-global-market-trends-analysis-and-forecasts. Galderma. (2024). Galderma and CureVac enter into strategic collaboration to develop RNA-based therapeutic for atopic dermatitis. Retrieved from https://www.Galderma.Com/news/press-releases/galderma-and-curevac-enter-into-strategic-collaboration-to-develop-rna-based-therapeutic-for-atopic-dermatitis. Celgene. (2024). Celgene Completes Acquisition of Marinomed Biotech AG. Retrieved from https://www.Celgene.Com/news/press-releases/celgene-completes-acquisition-of-marinomed-biotech-ag.

- Anacor Pharmaceuticals. (2024). Anacor Pharmaceuticals Announces FDA Approval of Crisaborole 2% Ointment for the Treatment of Mild-to-Moderate Atopic Dermatitis. Retrieved from https://www.Anacor.Com/news/press-releases/anacor-pharmaceuticals-announces-fda-approval-of-crisaborole-2-ointment-for-the-treatment-of-mild-to-moderate-atopic-dermatitis.

Research Analyst Overview

The market encompasses a range of treatments designed to alleviate the symptoms and address the underlying causes of various skin disorders, including atopic eczema and hand dermatitis. These conditions are characterized by skin redness, irritation, and itching, which can significantly impact an individual's quality of life. Genetics plays a role in the development of eczema, with certain genetic variations increasing an individual's susceptibility. However, environmental factors, such as exposure to allergens and irritants, can trigger the onset and exacerbate symptoms. Moisturizers are a common first-line treatment for eczema, as they help maintain the skin barrier and prevent water loss, reducing the likelihood of irritation and inflammation.

Topical steroids are another widely used therapeutic option, effective in reducing inflammation and suppressing the immune response. Recent advancements in eczema therapeutics include the development of foam delivery systems for topical steroids, which improve patient compliance and reduce the risk of side effects associated with prolonged use. Probiotics have also emerged as a promising therapeutic approach, with some studies suggesting they may help restore the skin microbiome and improve symptoms. Skin irritation and itching are common symptoms of eczema, and antihistamines and corticosteroid medicines are often used to alleviate these symptoms. However, long-term use of corticosteroids can lead to side effects, including thinning of the skin and increased susceptibility to infections.

Interleukin inhibitors and immunomodulators are newer classes of drugs that target the underlying immune system dysregulation associated with eczema. These medications can be administered topically or injectable, depending on the severity of the condition. Hand sanitizers and harsh soaps can exacerbate eczema symptoms, making emollients essential for maintaining healthy skin. Roseomonas mucosa, a bacterium found in the human microbiome, has been shown to produce a compound that may help alleviate skin inflammation and reduce the need for topical steroids. Medical therapies for eczema include phototherapy, which uses ultraviolet light to reduce inflammation, and wet wrap therapy, which involves applying wet dressings to the affected areas to improve the penetration of topical treatments.

PDE4 inhibitors are another therapeutic option, effective in reducing inflammation and itching. The market is continually evolving, with ongoing research and development efforts focused on improving existing treatments and discovering new therapeutic approaches. Online pharmacies offer convenience and accessibility for patients seeking these treatments, providing a range of options for managing eczema symptoms.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Eczema Therapeutics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.28% |

|

Market growth 2024-2028 |

USD 5.81 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.55 |

|

Key countries |

US, Canada, Germany, UK, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Eczema Therapeutics Market Research and Growth Report?

- CAGR of the Eczema Therapeutics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the eczema therapeutics market growth of industry companies

We can help! Our analysts can customize this eczema therapeutics market research report to meet your requirements.

RIA -

RIA -