Metal Additive Manufacturing Market Size 2026-2030

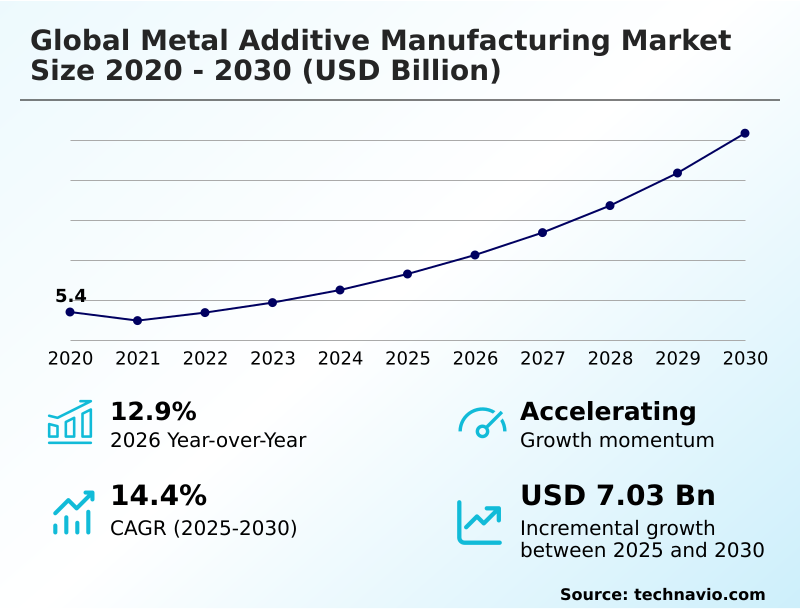

The metal additive manufacturing market size is valued to increase by USD 7.03 billion, at a CAGR of 14.4% from 2025 to 2030. Industrialization of production-scale metal additive manufacturing in aerospace and defense will drive the metal additive manufacturing market.

Major Market Trends & Insights

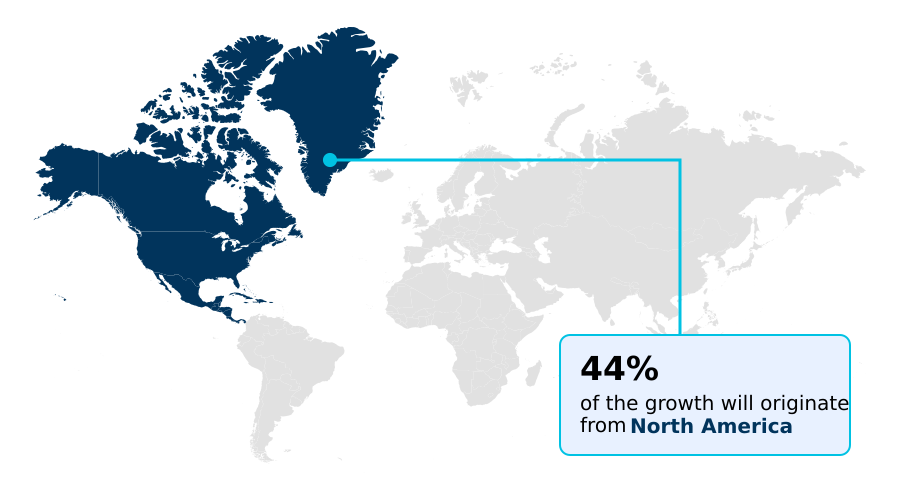

- North America dominated the market and accounted for a 43.7% growth during the forecast period.

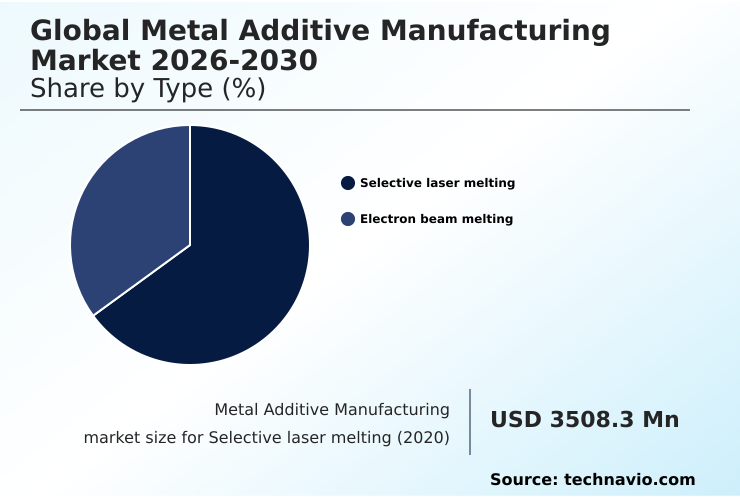

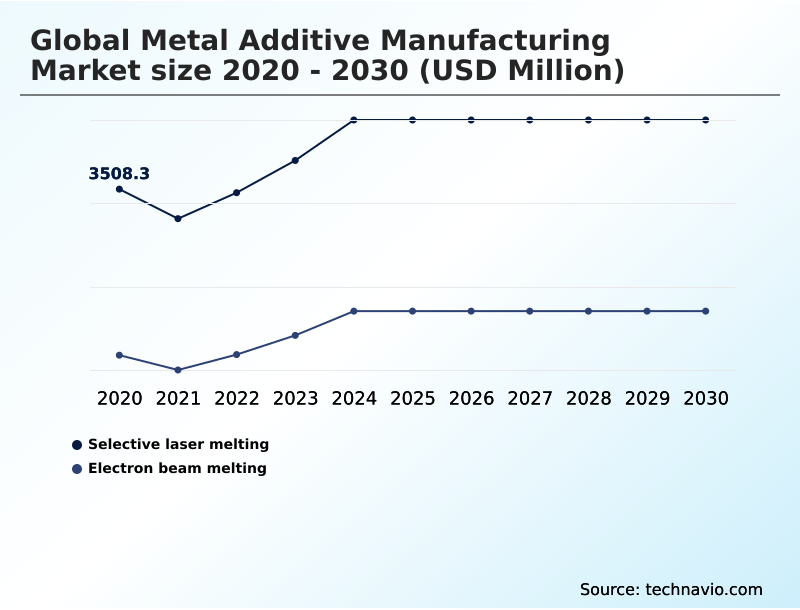

- By Type - Selective laser melting segment was valued at USD 4.18 billion in 2024

- By Application - Aerospace segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 8.94 billion

- Market Future Opportunities: USD 7.03 billion

- CAGR from 2025 to 2030 : 14.4%

Market Summary

- The metal additive manufacturing market is shifting from prototyping to industrialized production, driven by demand for high-performance components. This evolution is defined by advancements in core technologies like powder bed fusion and directed energy deposition, which enable the creation of parts with complex internal geometries previously unachievable.

- Key sectors such as aerospace and healthcare are leveraging these capabilities for lightweighting structural parts and producing 3d printed orthopedic devices. For instance, in a medical supply chain scenario, point-of-care manufacturing allows hospitals to produce patient-specific implants on-demand, drastically reducing lead times and inventory costs associated with traditional implant distribution.

- The integration of digital twin simulation and in-situ process monitoring addresses challenges related to part qualification standards and repeatability. As the industry matures, the focus on sustainable manufacturing practices, including metal powder feedstock recycling, and cost per part reduction will continue to shape its trajectory, making it a viable alternative to conventional methods like metal injection molding.

What will be the Size of the Metal Additive Manufacturing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Metal Additive Manufacturing Market Segmented?

The metal additive manufacturing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Selective laser melting

- Electron beam melting

- Application

- Aerospace

- Healthcare

- Tools and mold

- Automobile

- Others

- Material

- Stainless steel

- Titanium and alloys

- Nickel alloys

- Aluminum alloys

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- South Korea

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- South Africa

- Saudi Arabia

- Rest of World (ROW)

- North America

By Type Insights

The selective laser melting segment is estimated to witness significant growth during the forecast period.

The selective laser melting segment leads due to its precision and material versatility. This technology uses a high-power laser for fusing metallic powders, enabling complex part production with high density.

Key sectors leverage it for fabricating intricate geometries and lattice structure designs for weight optimization. The move from rapid prototyping to production is enabled by multi-laser systems, which improve build rates and economic viability.

Integrated real-time monitoring enhances process reliability, with some systems achieving build speeds up to 900% faster than standard methods. This powder bed fusion technique is crucial for industrial production scaling.

The focus on cost per part reduction and high-throughput metal printing is expanding its adoption for aerospace-grade components and patient-specific implants.

The Selective laser melting segment was valued at USD 4.18 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metal Additive Manufacturing Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which accounts for over 43% of the market's incremental growth, driven by its advanced aerospace and medical sectors.

In this region, the focus is on industrial production scaling and leveraging technologies like electron beam melting for aerospace-grade components. Europe remains a key innovation hub, with a strong emphasis on part qualification standards and developing hybrid manufacturing systems.

Meanwhile, APAC is the fastest-growing region, with a projected CAGR of 14.9%, fueled by automotive and electronics manufacturing. The region is rapidly adopting binder jetting technology and developing its own metal powder feedstock supply chains to support high-volume production.

This global distribution underscores the technology's adaptability, from on-demand spare part fabrication in mature markets to green additive manufacturing initiatives in emerging economies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global metal additive manufacturing market 2026-2030 is increasingly shaped by how selective laser melting impacts aerospace component design, enabling lighter and stronger parts. Simultaneously, the benefits of electron beam melting for titanium medical implants are becoming more pronounced, offering superior biocompatibility and customization.

- A key enabler of this progress is the role of digital twin technology in metal am process control, which allows for predictive analysis and optimization. However, significant challenges in qualifying additively manufactured parts for defense persist, demanding rigorous validation. In the automotive sector, engineers are using topology optimization for automotive weight reduction, a strategy that pairs well with additive techniques.

- The conformal cooling channels in injection mold tooling benefits provide a clear economic advantage, reducing cycle times by over 40% compared to traditionally machined tools. The cost analysis of powder bed fusion vs traditional casting continues to evolve with advancements in nickel superalloy 3d printing for turbines.

- Techniques such as in-situ monitoring techniques for ensuring part quality and residual stress reduction methods in metal 3d printing are critical for achieving consistency. Implementing a digital thread for metal additive manufacturing is becoming standard, as are sustainability gains from metal powder recycling systems.

- As the industry explores the material properties of 3d printed high-entropy alloys, scaling metal additive manufacturing for serial production is the ultimate goal, where the binder jetting process for mass producing stainless steel parts and wire arc additive manufacturing for large marine components showcase diverse pathways.

What are the key market drivers leading to the rise in the adoption of Metal Additive Manufacturing Industry?

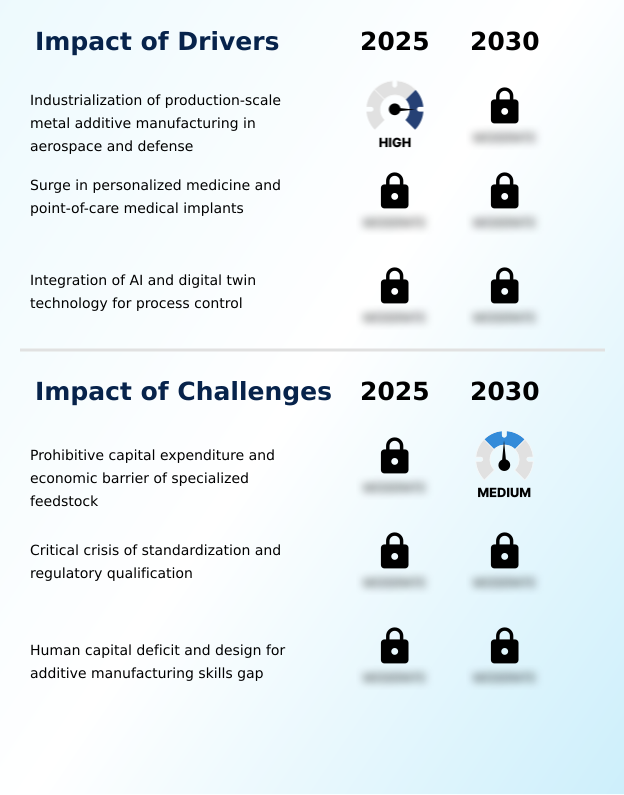

- The industrialization of production-scale metal additive manufacturing, particularly within the aerospace and defense sectors, is a key driver for market expansion.

- Market growth is driven by the increasing demand for lightweighting structural parts and the capability for on-demand spare part fabrication, which enhances supply chain resilience.

- The integration of AI-driven defect detection has improved first-pass yield rates by up to 20%, a critical factor for high-value industries. The ability to create complex internal geometries allows for optimized thermal management solutions in electronics and energy applications.

- In healthcare, point-of-care manufacturing of 3d printed orthopedic devices offers personalized solutions that improve patient outcomes. This is further supported by streamlined processes for regulatory compliance for implants.

- The push for industrial production scaling is also fueled by a continuous focus on cost per part reduction, making the technology economically viable for a broader range of applications.

What are the market trends shaping the Metal Additive Manufacturing Industry?

- The proliferation of industrial-scale, multi-laser systems is a significant market trend. This development indicates a maturation toward mass production capabilities across key industrial sectors.

- Key market trends are centered on the shift from rapid prototyping to production and the maturation of industrial-scale technologies. High-throughput metal printing is becoming a reality as multi-laser systems are more widely adopted, with some platforms demonstrating a 300% increase in build speed. This enables effective part consolidation strategy, which simplifies complex assemblies in aerospace and automotive applications.

- The evolution of advanced metallurgical engineering is expanding the material palette to include high-performance alloy printing. Additionally, the development of orbital manufacturing platforms represents a forward-looking trend focused on in-space production. Sustainable manufacturing practices are also gaining traction, as feedstock recycling systems can recover over 95% of unused powder, significantly reducing material waste and operational costs.

What challenges does the Metal Additive Manufacturing Industry face during its growth?

- Prohibitive capital expenditure, along with the economic barrier of specialized feedstock, presents a key challenge affecting widespread industry adoption and growth.

- The market faces challenges related to standardization and the high initial investment for industrial systems. A significant hurdle is the complex process of functional validation testing, which can be time-consuming and costly, sometimes offsetting the speed advantages of additive manufacturing.

- The skills gap in design for additive manufacturing (DFAM) remains a constraint, as engineers require specialized training to fully leverage the technology. While non-destructive testing methods are advancing, ensuring consistent quality assurance in AM across different machines and materials is still a complex issue.

- The high cost of specialized metal powder feedstock and the operational expenses of automated powder handling systems also present economic barriers for smaller enterprises, limiting broader adoption. The lack of universal part qualification standards creates bottlenecks, particularly in safety-critical sectors.

Exclusive Technavio Analysis on Customer Landscape

The metal additive manufacturing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metal additive manufacturing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Metal Additive Manufacturing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, metal additive manufacturing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - Offers metal additive manufacturing with advanced powder bed fusion systems, featuring integrated software solutions to enhance production workflows and part quality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- Additive Industries BV

- DMG MORI Co. Ltd.

- EOS GmbH

- Eplus 3D

- Hoganas AB

- HP Inc.

- Markforged Holding Corp.

- Nikon Corp.

- Norsk Titanium AS

- Optomec Inc.

- Renishaw Plc

- Sandvik AB

- Sciaky Inc.

- Stratasys Ltd.

- The Lincoln Electric Co.

- TRUMPF SE Co. KG

- Velo3D Inc.

- Xact Metal Inc.

- Xjet Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metal additive manufacturing market

- In September 2024, Innospace announced a strategic agreement to supply its INNO AM-X process control system to Hyundai for real-time quality management of metal additive manufacturing processes.

- In January 2025, Hadrian launched its Hadrian Additive division to provide scalable, production-ready metal additive manufacturing capacity for the United States Defense Industrial Base and allied partners.

- In March 2025, The European Union updated its industrial manufacturing guidelines, establishing clearer qualification pathways for 12-kilowatt laser powder bed fusion lines to reduce per-part production costs.

- In April 2025, a Chilean medical startup successfully completed the implantation of several hundred customized titanium craniomaxillofacial devices, demonstrating advanced regional medical manufacturing capabilities.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metal Additive Manufacturing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.4% |

| Market growth 2026-2030 | USD 7032.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.9% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, South Korea, India, Australia, Indonesia, Brazil, Argentina, Colombia, UAE, South Africa, Saudi Arabia, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a strategic transition toward full-scale industrialization, where the focus is on producing born-qualified parts through advanced manufacturing processes. Technologies such as selective laser melting and electron beam melting are foundational, supported by innovations in multi-laser systems and binder jetting technology.

- The development of high-entropy alloy development and refractory metal processing is expanding application possibilities into extreme environments. A key trend impacting boardroom strategy is the integration of a complete digital thread, which combines topology optimization software and digital twin simulation for end-to-end process control.

- This approach not only facilitates the creation of complex lattice structure designs but also addresses critical compliance requirements by ensuring layer-by-layer inspection and traceability. For instance, firms adopting closed-loop feedback control have reported a 20% improvement in part consistency, directly impacting qualification timelines and cost.

- This push for reliability, from metal powder feedstock to post-processing heat treatment, is making metal additive manufacturing a viable alternative for creating patient-specific implants and aerospace-grade components.

What are the Key Data Covered in this Metal Additive Manufacturing Market Research and Growth Report?

-

What is the expected growth of the Metal Additive Manufacturing Market between 2026 and 2030?

-

USD 7.03 billion, at a CAGR of 14.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Selective laser melting, and Electron beam melting), Application (Aerospace, Healthcare, Tools and mold, Automobile, and Others), Material (Stainless steel, Titanium and alloys, Nickel alloys, Aluminum alloys, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Industrialization of production-scale metal additive manufacturing in aerospace and defense, Prohibitive capital expenditure and economic barrier of specialized feedstock

-

-

Who are the major players in the Metal Additive Manufacturing Market?

-

3D Systems Corp., Additive Industries BV, DMG MORI Co. Ltd., EOS GmbH, Eplus 3D, Hoganas AB, HP Inc., Markforged Holding Corp., Nikon Corp., Norsk Titanium AS, Optomec Inc., Renishaw Plc, Sandvik AB, Sciaky Inc., Stratasys Ltd., The Lincoln Electric Co., TRUMPF SE Co. KG, Velo3D Inc., Xact Metal Inc. and Xjet Ltd.

-

Market Research Insights

- The market is defined by a strategic shift from rapid prototyping to production, where advanced metallurgical engineering is enabling high-performance alloy printing. This transition is supported by innovations that directly impact operational efficiency, with some multi-laser systems improving throughput by over 300% compared to single-laser counterparts.

- Furthermore, the use of AI-driven defect detection during layer-by-layer inspection has reduced part rejection rates by up to 25% in critical applications. The implementation of a part consolidation strategy through generative design algorithms allows manufacturers to combine multiple components into a single unit, simplifying assembly and strengthening the metal 3d printing supply chain.

- This focus on process parameter optimization and automated powder handling is essential for achieving the industrial production scaling needed for mainstream adoption.

We can help! Our analysts can customize this metal additive manufacturing market research report to meet your requirements.

RIA -

RIA -