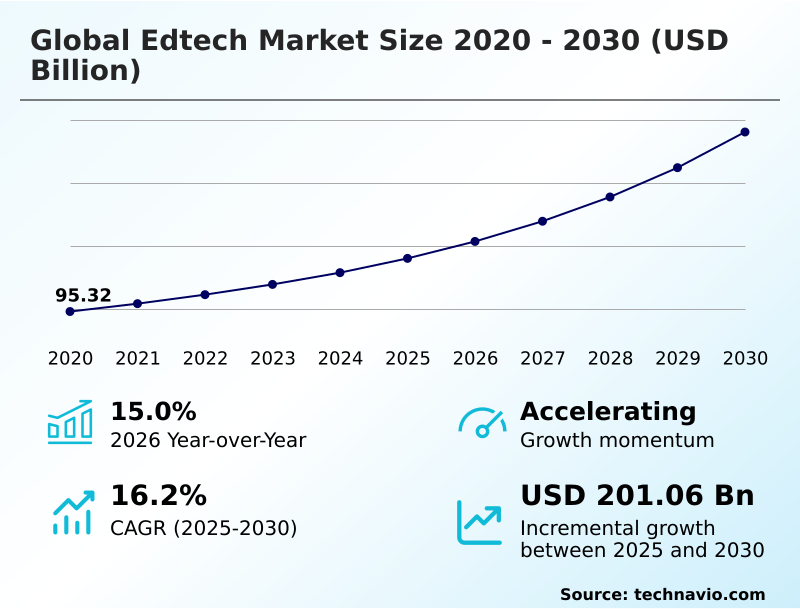

Edtech Market Size 2026-2030

The edtech market size is valued to increase by USD 201.06 billion, at a CAGR of 16.2% from 2025 to 2030. Integration of ML language in technical educational systems will drive the edtech market.

Major Market Trends & Insights

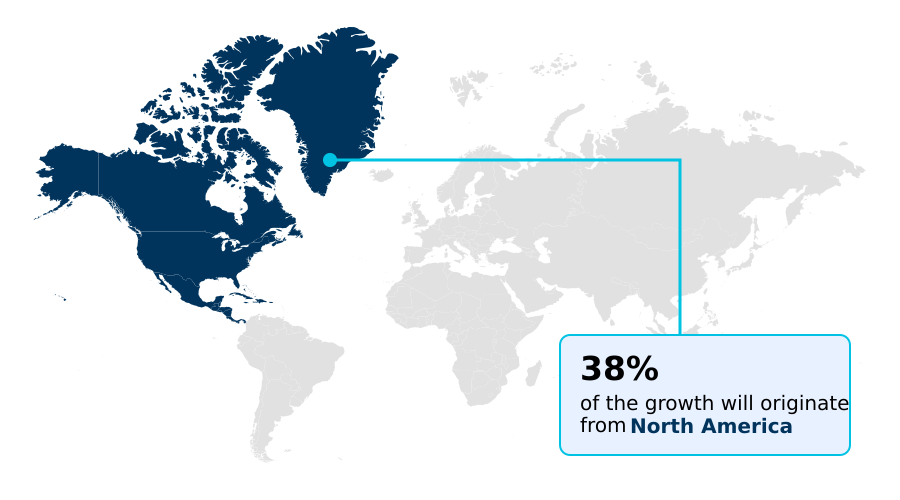

- North America dominated the market and accounted for a 37.5% growth during the forecast period.

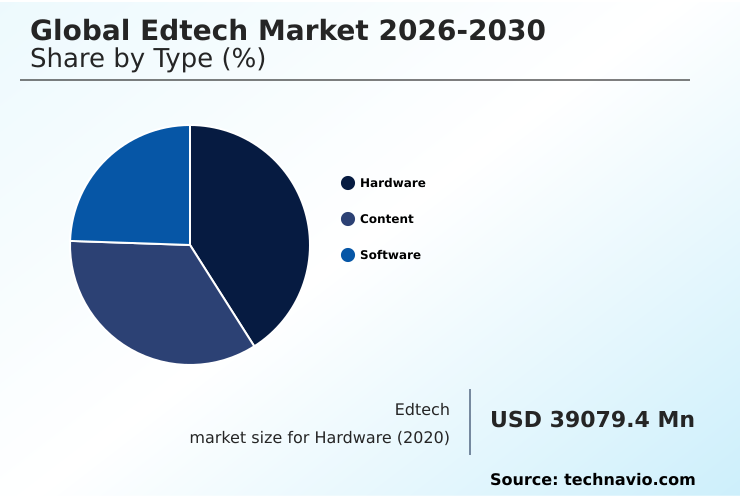

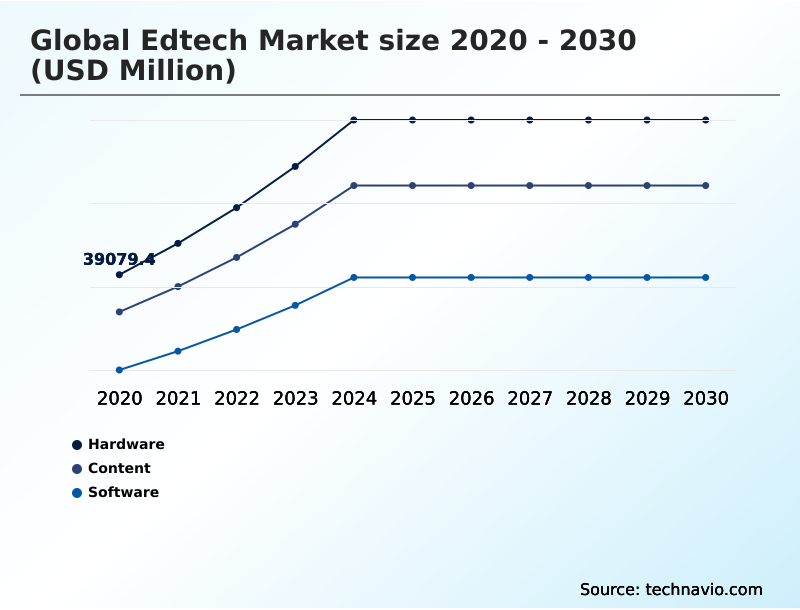

- By Type - Hardware segment was valued at USD 64.67 billion in 2024

- By Sector - K-12 segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 285.58 billion

- Market Future Opportunities: USD 201.06 billion

- CAGR from 2025 to 2030 : 16.2%

Market Summary

- The edtech market is fundamentally transforming how knowledge is delivered and acquired, moving beyond traditional classroom structures to create more accessible, personalized, and efficient learning ecosystems. This evolution is propelled by the integration of technologies like machine learning and cloud computing, which enable adaptive learning platforms to tailor content to individual student needs.

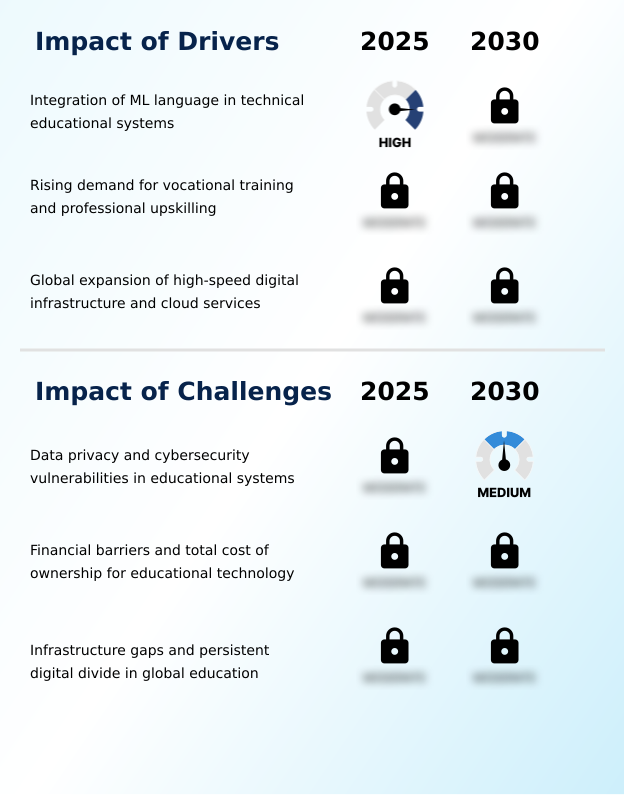

- The rising demand for continuous vocational training and professional upskilling is a major driver, as the modern workforce requires constant skill enhancement. Consequently, professional upskilling platforms are proliferating. Key trends include the adoption of generative AI for hyper-personalized learning and AI-driven content creation, alongside the use of extended reality for immersive simulations in technical fields.

- For instance, a global manufacturing firm can deploy a corporate e-learning platform using virtual reality in education to train technicians on complex machinery, reducing equipment downtime and improving safety compliance by over 20%. However, the industry faces challenges related to data privacy and the digital divide, which can limit equitable access to these advanced tools.

- The shift toward skills-based assessment and micro-credentials, often verified using blockchain technology, reflects a move toward more flexible and employment-focused educational pathways.

What will be the Size of the Edtech Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Edtech Market Segmented?

The edtech industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Hardware

- Content

- Software

- Sector

- K-12

- Higher education

- Others

- Deployment

- Cloud

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment provides the physical foundation for the edtech market, encompassing everything from personal devices to interactive displays that facilitate collaborative learning. The growth of smart classroom technology and corporate e-learning platforms is driving demand for specialized hardware.

This includes devices optimized for virtual reality in education, enabling virtual reality training in technical fields.

The expansion of digital infrastructure is critical for supporting mobile learning applications, which now represent over 60% of digital content access points in some emerging markets.

Effective hardware selection and deployment are essential for institutions to deliver high-quality digital experiences and capitalize on software advancements.

The Hardware segment was valued at USD 64.67 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Edtech Market Demand is Rising in North America Get Free Sample

The geographic landscape of the edtech market is characterized by varied adoption rates and investment priorities. North America remains a dominant market, with a mature ecosystem focused on advanced applications like predictive analytics to improve student outcomes.

In contrast, the APAC region is the fastest-growing market, driven by mobile-first adoption and government initiatives supporting K-12 digital curriculum solutions.

The implementation of online assessment tools and student performance dashboards is becoming standard in European universities to support online degree program management.

Across all regions, the use of adaptive learning and generative AI is a key focus, though deployment is often limited by infrastructure readiness.

North America contributes over 37% of the incremental growth, while APAC's market is expanding at a CAGR of 17.7%.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of the edtech market is being defined by the sophisticated application of technology to solve specific educational challenges. The use of generative AI for personalized learning paths is revolutionizing instruction by creating truly individualized curricula, with platforms using AI-powered adaptive learning software for math showing the potential to improve student scores by up to two grade levels.

- However, this increased reliance on data-driven systems amplifies cybersecurity risks in K-12 school districts, making robust protocols for integrating LMS with student information systems non-negotiable. In the professional realm, there is a clear shift toward recognizing granular skills, highlighting the benefits of micro-credentials in corporate training.

- The integrity of these credentials is paramount, which is where blockchain for verifying academic credentials provides a tamper-proof solution. Simultaneously, the impact of extended reality on medical education is profound, allowing for risk-free surgical practice in virtual environments.

- This demand for high-fidelity simulations forces a critical decision between the scalability of cloud computing vs on-premise edtech solutions, as institutions balance performance needs with the total cost of ownership for educational technology.

- Furthermore, using AI to bridge the student skills gap and addressing the challenges of the digital divide in remote learning remain central to ensuring equitable access and opportunity for all learners.

What are the key market drivers leading to the rise in the adoption of Edtech Industry?

- The integration of machine learning language within technical educational systems serves as a key driver for market growth.

- Key drivers are reshaping how educational content is delivered and consumed, with machine learning at the forefront of this transformation.

- The demand for industry-aligned skills fuels the growth of professional upskilling platforms that offer specialized vocational training, with some platforms reporting a 30% faster time-to-competency for learners.

- This is enabled by cloud-based learning management systems that provide scalable and flexible access to resources. Cloud computing also supports the deployment of AI-powered tutoring systems and AI-driven content creation, which helps in developing personalized learning path software.

- Furthermore, the integration of gamification elements has proven to increase learner engagement by as much as 50%, making learning more interactive and effective.

What are the market trends shaping the Edtech Industry?

- The integration of generative AI represents an emerging market trend. This technology enables the delivery of hyper-personalized learning experiences.

- Market trends are shifting toward more individualized and verifiable learning pathways. The adoption of extended reality is creating new opportunities for immersive simulations, particularly in hands-on training where it can reduce errors by up to 40%. Concurrently, AI in education platforms are enabling hyper-personalized learning at scale, moving beyond one-size-fits-all instruction.

- This is complemented by a growing focus on competency-based learning models and the use of micro-credentials for targeted skill development. To ensure the integrity of these achievements, blockchain technology is being implemented for digital credential verification, providing a secure and transparent record. These trends are reshaping blended learning environments and defining the future of education delivery.

What challenges does the Edtech Industry face during its growth?

- Data privacy concerns and cybersecurity vulnerabilities within educational systems present a key challenge to industry growth.

- The rapid digitalization of education introduces significant operational challenges, primarily centered on data privacy and cybersecurity vulnerabilities. Institutions must implement robust student data protection policies as they manage vast amounts of sensitive information across the learning management system and student information system. The increasing reliance on remote learning technologies expands the potential attack surface, making security a paramount concern.

- Integrating education data analytics with higher education ERP systems requires careful management to prevent data breaches. Failure to secure these systems can undermine trust and lead to regulatory non-compliance, with some institutions dedicating over 15% of their IT budgets to mitigating these risks.

Exclusive Technavio Analysis on Customer Landscape

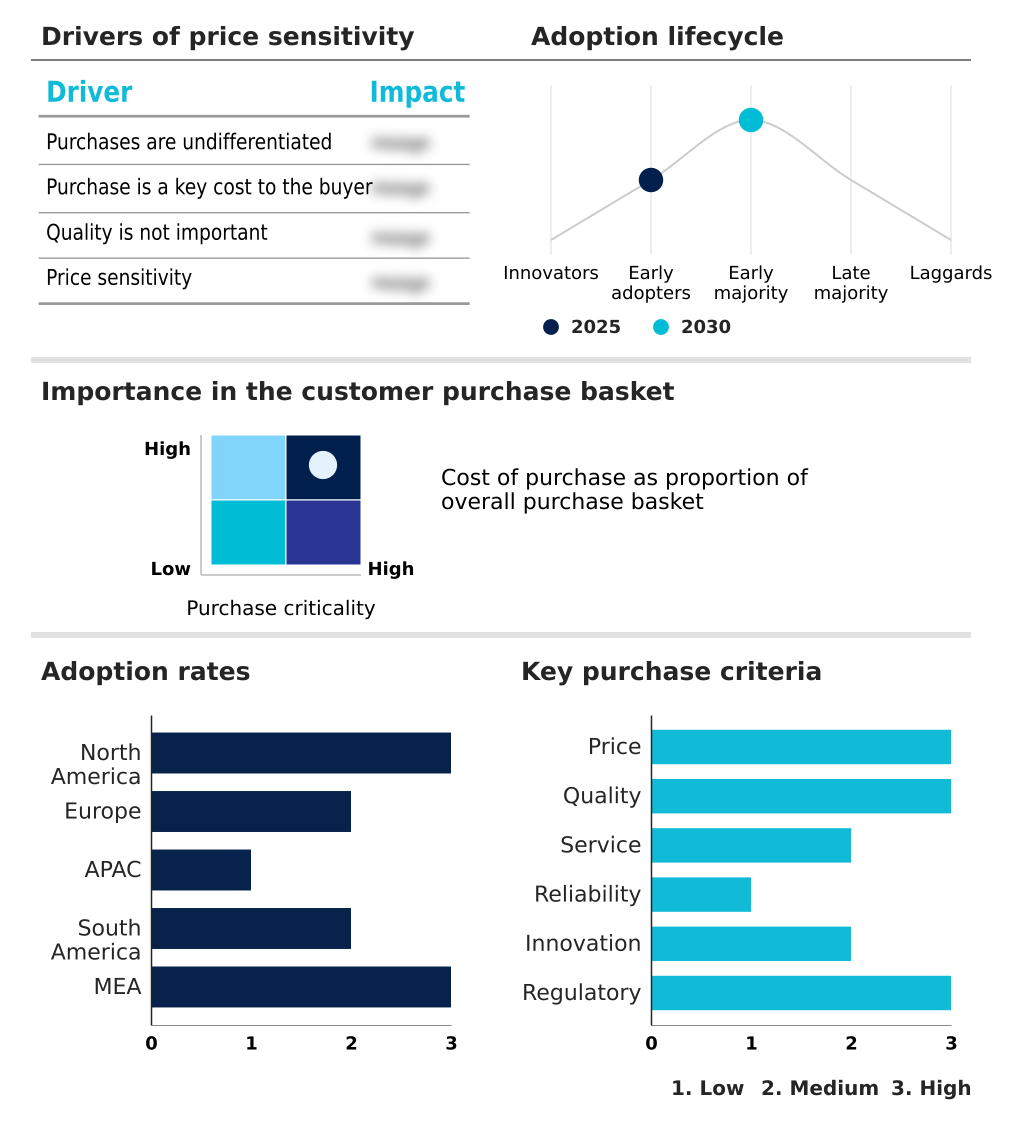

The edtech market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the edtech market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Edtech Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, edtech market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

2U Inc. - Delivering integrated digital platforms and software that manage and enhance education across academic, corporate, and lifelong learning environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 2U Inc.

- Anthology Inc.

- Chegg Inc.

- Cornerstone OnDemand Inc.

- Coursera Inc.

- D2L Corp.

- Discovery Education Inc.

- edX LLC

- Ellucian Co.

- Google LLC

- Instructure Holdings Inc.

- Microsoft Corp.

- Oracle Corp.

- PleIQ Smart Toys Spa

- Promethean World Ltd.

- Think and Learn Pvt. Ltd.

- Udacity Inc.

- UOL EdTech

- upGrad Education Pvt. Ltd.

- Workday Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Edtech market

- In August 2024, Skillsoft introduced a new platform for leadership training that uses interactive simulations to teach management skills to employees in the corporate sector.

- In October 2024, Udacity launched a specialized program for automotive software engineering to address the shortage of skilled workers in the electric vehicle industry.

- In March 2025, OpenAI launched a dedicated educational initiative that provides large language model access to universities for the purpose of developing personalized tutoring bots.

- In May 2025, Meta Platforms announced a partnership with educational institutions in Europe to deploy thousands of quest headsets for use in science and history classes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Edtech Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.2% |

| Market growth 2026-2030 | USD 201057.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- From an analyst perspective, the edtech market is undergoing a strategic pivot from simple content digitization to the creation of intelligent learning ecosystems. The integration of machine learning and generative AI is no longer a niche feature but a core component of competitive platforms, enabling hyper-personalized learning and adaptive learning at an unprecedented scale.

- Boardroom decisions are now centered on leveraging data analytics from the learning management system and student information system to drive retention and operational efficiency. The adoption of extended reality for immersive simulations and virtual reality training offers a clear return on investment, particularly in vocational training.

- Platforms that incorporate gamification elements are demonstrating a 40% increase in user completion rates, validating their effectiveness. The market is also moving toward verifiable outcomes through skills-based assessment and micro-credentials, with blockchain technology ensuring the integrity of this digital curriculum.

- Looking ahead, success will depend on addressing cybersecurity vulnerabilities and ensuring robust digital infrastructure to support these advanced mobile learning applications and AI-powered tutoring systems.

What are the Key Data Covered in this Edtech Market Research and Growth Report?

-

What is the expected growth of the Edtech Market between 2026 and 2030?

-

USD 201.06 billion, at a CAGR of 16.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Hardware, Content, and Software), Sector (K-12, Higher education, and Others), Deployment (Cloud, and On-premises) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of ML language in technical educational systems, Data privacy and cybersecurity vulnerabilities in educational systems

-

-

Who are the major players in the Edtech Market?

-

2U Inc., Anthology Inc., Chegg Inc., Cornerstone OnDemand Inc., Coursera Inc., D2L Corp., Discovery Education Inc., edX LLC, Ellucian Co., Google LLC, Instructure Holdings Inc., Microsoft Corp., Oracle Corp., PleIQ Smart Toys Spa, Promethean World Ltd., Think and Learn Pvt. Ltd., Udacity Inc., UOL EdTech, upGrad Education Pvt. Ltd. and Workday Inc.

-

Market Research Insights

- The edtech market's dynamics are increasingly shaped by the demand for data-driven, skill-focused educational outcomes. AI in education platforms are at the core of this shift, with institutions using student performance dashboards reporting up to a 15% improvement in student retention rates.

- The move toward competency-based learning models is supported by online assessment tools that offer more flexible and accurate evaluations of learner skills. In the corporate sector, the adoption of corporate e-learning platforms has been shown to reduce employee onboarding time by over 30% compared to traditional methods.

- Blended learning environments are becoming standard, combining the best of in-person and digital instruction. The focus is on creating integrated ecosystems where cloud-based learning management and higher education ERP systems work seamlessly to provide a holistic view of the learner's journey.

We can help! Our analysts can customize this edtech market research report to meet your requirements.

RIA -

RIA -