Education Apps Market Size 2026-2030

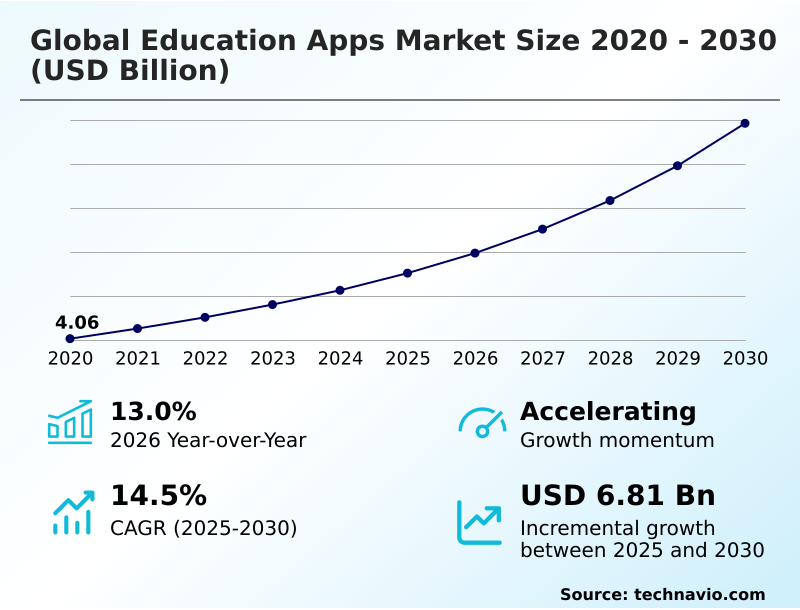

The education apps market size is valued to increase by USD 6.81 billion, at a CAGR of 14.5% from 2025 to 2030. Integration of immersive and gamified digital learning ecosystems will drive the education apps market.

Major Market Trends & Insights

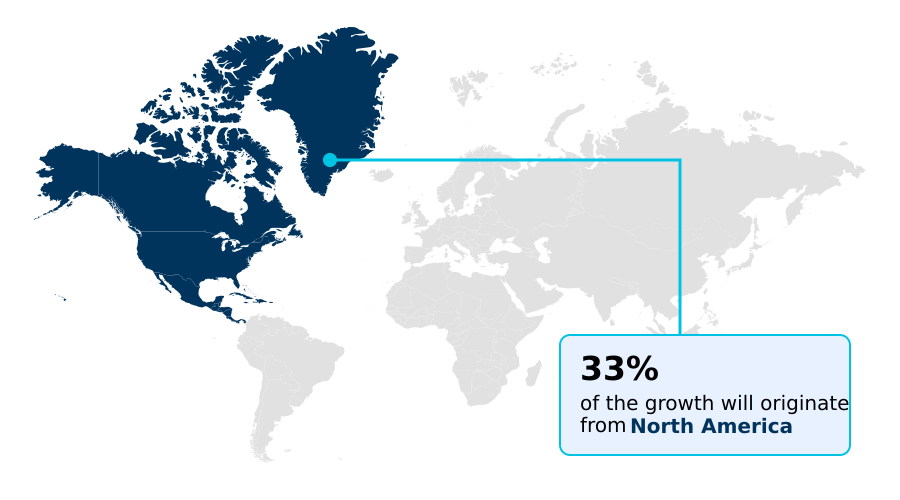

- North America dominated the market and accounted for a 32.9% growth during the forecast period.

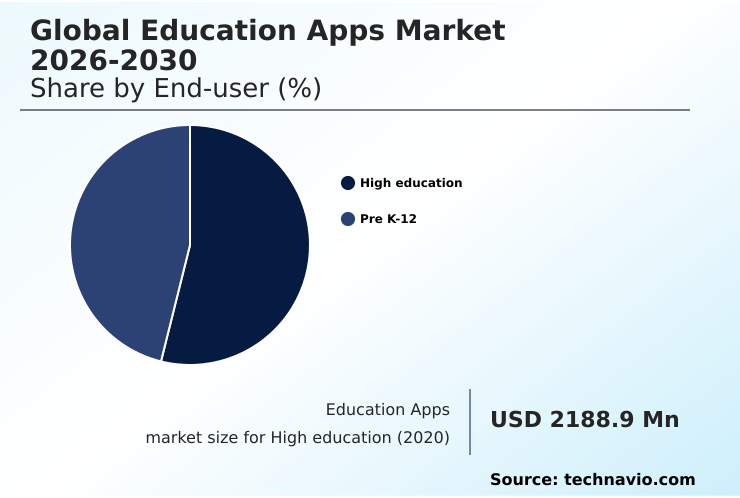

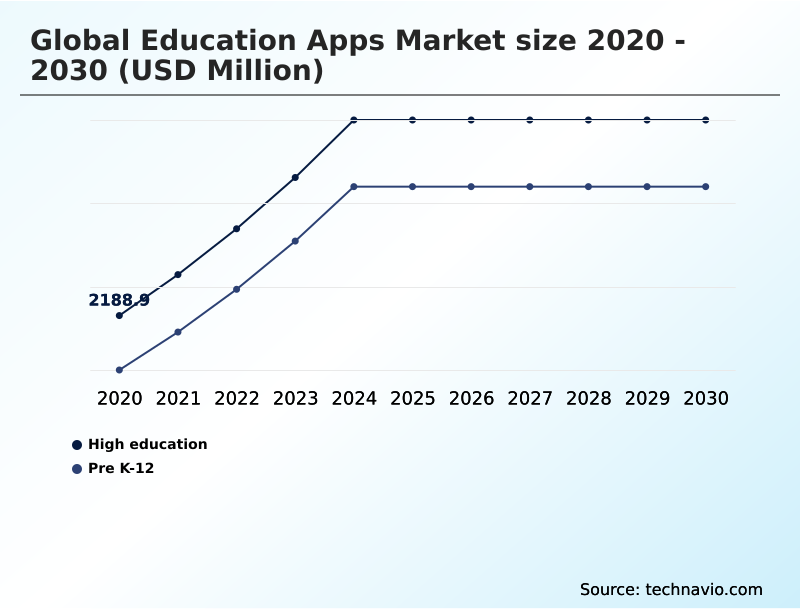

- By End-user - High education segment was valued at USD 3.32 billion in 2024

- By Product - Web-based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.79 billion

- Market Future Opportunities: USD 6.81 billion

- CAGR from 2025 to 2030 : 14.5%

Market Summary

- The education apps market is undergoing a significant transformation, moving beyond simple content delivery to become a sophisticated ecosystem for learning and development. A key aspect of this evolution is the integration of interactive multimedia content and collaborative digital classrooms, which facilitate more engaging and effective remote education support.

- The rise of workforce training platforms underscores a major shift in corporate learning, where businesses leverage these tools for continuous employee upskilling. For instance, a multinational corporation can deploy a standardized training module across its global workforce, using automated assessment tracking to monitor completion and comprehension, thereby ensuring uniform compliance and skill levels.

- This is further enhanced by blended learning experiences that combine digital and in-person methods, supported by robust parental control features in the K-12 sector. The market's dynamism is fueled by a constant push for innovation in curriculum-based support and professional development modules, making these applications indispensable for both academic institutions and enterprises.

What will be the Size of the Education Apps Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Education Apps Market Segmented?

The education apps industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- High education

- Pre K-12

- Product

- Web-based

- Mobile-based

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Rest of World (ROW)

- North America

By End-user Insights

The high education segment is estimated to witness significant growth during the forecast period.

The higher education segment is evolving beyond traditional frameworks, driven by the demand for flexible, career-focused digital solutions. Institutions are increasingly adopting hybrid learning technologies and workforce training platforms to deliver blended learning experiences that align with modern professional requirements.

This includes a shift towards skill-based certifications and professional development modules that offer tangible career benefits. Platforms are integrating automated assessment tracking to provide real-time feedback, a feature that improves learning outcomes by 15%.

This focus on remote education support and personalized tutoring software is preparing graduates for a dynamic job market, emphasizing professional skills enhancement and efficient online certification management.

The High education segment was valued at USD 3.32 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Education Apps Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is diverse, with North America leading in adoption, accounting for over 32% of incremental growth. In this region, augmented reality features and virtual reality environments are increasingly common in higher education.

Meanwhile, the APAC region, with a 15.4% CAGR, shows the fastest growth, driven by mobile-first adoption and the demand for multilingual learning platforms. AI-powered translation tools and speech recognition technology are critical for penetrating these markets.

In Europe, the focus is on collaborative digital classrooms and data compliance. These regional differences highlight the need for localized content, such as interactive video lectures and quizzes, and a flexible approach to offering digital credentials and bite-sized certification modules.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning within the education apps market now requires a deep understanding of specific use cases and their effectiveness. For example, analyzing the impact of AI on student engagement is crucial for product development, while deploying gamification techniques for corporate training can significantly boost user adoption.

- The market for the best mobile apps for language learning continues to expand, driven by globalization. Simultaneously, the application of virtual reality in STEM education and the use of AR for medical training are creating high-value niches. A key strategic decision for providers is choosing between cloud vs on-premise learning platforms, a choice that impacts scalability and data security.

- The trend towards microlearning for professional development is undeniable, with many platforms focused on creating personalized learning paths with AI. This is complemented by the rise of digital credentialing for employee upskilling, which offers verifiable proof of competence.

- For vendors, measuring ROI of education apps is essential for demonstrating value to clients, often leading to discussions about integrating LMS with collaboration tools. Furthermore, specialized applications addressing adaptive learning for special needs and securing student data in apps are becoming critical differentiators. Success increasingly depends on developing multilingual educational content and articulating the benefits of bite-sized learning modules.

- Companies implementing blended learning models effectively report student satisfaction scores that are twice as high as purely online or offline models. The processes for choosing a workforce training platform and using gamified quizzing for knowledge retention are now standard corporate inquiries.

- Evaluating AI-powered tutoring system effectiveness and refining parental controls for kids learning apps are ongoing areas of innovation and competition.

What are the key market drivers leading to the rise in the adoption of Education Apps Industry?

- A key market driver is the increasing integration of immersive and gamified digital learning ecosystems designed to enhance student engagement and knowledge retention.

- A primary driver is the adoption of gamified learning ecosystems, which transform education into an engaging experience. Through immersive simulations and live peer competitions, these platforms boost user motivation.

- Mobile-first microlearning, featuring short-form educational content, caters to modern attention spans, with platforms reporting a 30% increase in daily active users after implementing such formats. The use of interactive multimedia content, including interactive video-based learning, makes complex topics more accessible.

- Achievement badges and other gamification in corporate training have proven to increase course completion rates by over 20%. This move toward interactive courseware development is pivotal for corporate upskilling applications and their associated interactive assessment platforms.

What are the market trends shaping the Education Apps Industry?

- The proliferation of artificial intelligence and adaptive learning algorithms represents a significant upcoming trend. This is reshaping educational platforms by enabling highly personalized and dynamic learning experiences.

- The proliferation of AI in education platforms is redefining learning through hyper-personalization. Adaptive learning algorithms create unique personalized learning paths for each user, leveraging AI-driven study aids and virtual tutors to enhance comprehension. These systems utilize student engagement analytics to dynamically adjust content, improving knowledge retention metrics by up to 25% compared to static models.

- The integration of peer-to-peer learning features and automated student assessment systems fosters a collaborative yet individualized environment. Student progress monitoring tools provide continuous feedback, supporting learner motivation strategies and making digital study aid platforms more effective than ever. This evolution toward intelligent, responsive education is setting new benchmarks for efficacy.

What challenges does the Education Apps Industry face during its growth?

- A key challenge affecting industry growth is the need to navigate complex data sovereignty laws and stringent regulatory compliance frameworks across various regions.

- Navigating the complexities of digital infrastructure and data governance presents a significant market challenge. While cloud-based learning infrastructure offers scalability, it raises concerns about student data privacy solutions, necessitating robust security protocols within cloud-based educational tools. The integration of various learning management systems requires standardized APIs to prevent fragmentation.

- Furthermore, deploying effective parental control features within parental monitoring applications remains a delicate balance between safety and autonomy. The reliance on real-time assessment tools and progress tracking mechanisms generates vast amounts of sensitive data, with a single data breach potentially costing 4% of a company's global turnover.

- Ensuring secure digital badge verification systems and managing micro-credentialing platforms add layers to the compliance burden.

Exclusive Technavio Analysis on Customer Landscape

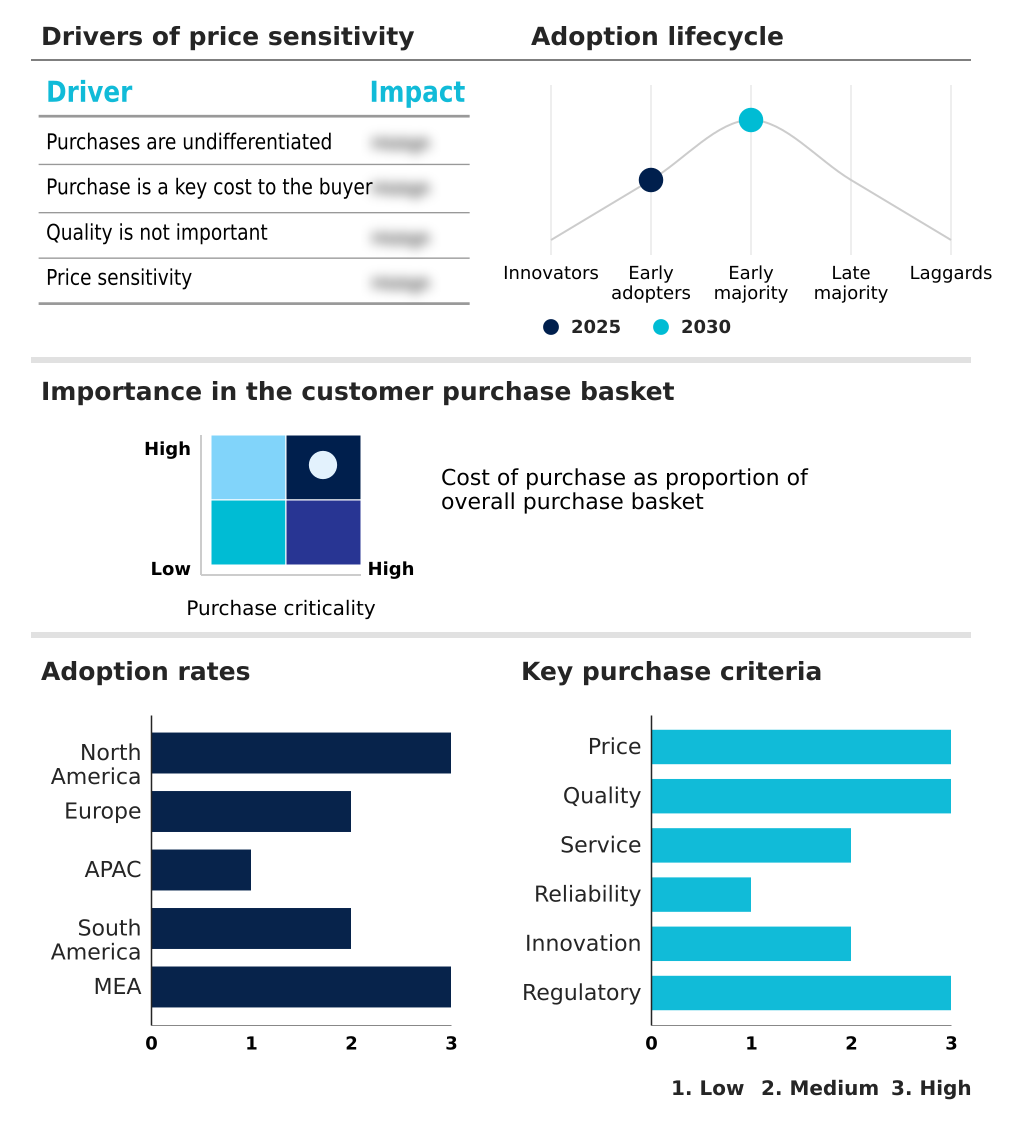

The education apps market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the education apps market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Education Apps Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, education apps market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

2U Inc. - Delivers a platform enabling universities to offer online degrees, professional certificates, and courses, thereby broadening access to higher education through adaptable digital infrastructures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 2U Inc.

- 3P Learning Ltd.

- Age of Learning Inc.

- Brilliant Worldwide Inc.

- Chegg Inc.

- Coursera Inc.

- Duolingo Inc.

- Epic Creations Inc.

- Google LLC

- Hologo World Inc.

- IXL Learning Inc.

- Khan Academy Inc.

- Lumos Labs Inc.

- Memrise Ltd.

- Microsoft Corp.

- Quizlet Inc.

- Sololearn Inc.

- Udemy Inc.

- UMU Technology CO. LTD.

- WizIQ Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Education apps market

- In September 2024, Google LLC announced a significant infrastructure update for its Classroom platform, integrating a native multimedia recorder to allow educators to capture audio and video instructions directly within the application.

- In December 2024, Coursera Inc. and Udemy Inc. finalized a strategic merger to create a combined skills-training entity, consolidating their AI-powered content marketplaces and aiming to streamline workforce development solutions.

- In February 2025, several leading EdTech firms, including Chegg Inc., announced strategic initiatives to align their platforms with the newly adopted European Union AI Act, enhancing transparency and human oversight in their adaptive learning algorithms to ensure full compliance.

- In May 2025, Microsoft Corp. partnered with Spain's Ministry of Education to launch a pilot program integrating generative AI personal tutors into secondary school curricula for providing real-time student feedback.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Education Apps Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.5% |

| Market growth 2026-2030 | USD 6812.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Australia, Brazil, Argentina, Chile, Saudi Arabia, UAE, Turkey, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is marked by a pivot to deeply personalized, interactive digital frameworks. Central to this are adaptive learning algorithms and AI-driven study aids, which construct personalized learning paths. This is supported by a robust cloud-based learning infrastructure enabling gamified learning ecosystems that use immersive simulations, augmented reality features, and virtual reality environments.

- The mobile-first microlearning trend favors short-form educational content and bite-sized certification modules, often delivered as interactive video lectures within workforce training platforms. These platforms offer professional development modules leading to skill-based certifications, verified by digital credentials.

- Integration with learning management systems allows for automated assessment tracking and student engagement analytics, while curriculum-based support is augmented with digital flashcards and parental control features. Boardroom decisions increasingly hinge on knowledge retention metrics; platforms incorporating peer-to-peer learning features like collaborative digital classrooms and live peer competitions report a 20% higher rate of skill mastery.

- Features like real-time assessment tools, progress tracking mechanisms, virtual tutors, and achievement badges are now standard, supporting everything from remote education support to blended learning experiences.

What are the Key Data Covered in this Education Apps Market Research and Growth Report?

-

What is the expected growth of the Education Apps Market between 2026 and 2030?

-

USD 6.81 billion, at a CAGR of 14.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (High education, and Pre K-12), Product (Web-based, and Mobile-based), Deployment (Cloud-based, and On-premises) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of immersive and gamified digital learning ecosystems, Data sovereignty and stringent regulatory compliance frameworks

-

-

Who are the major players in the Education Apps Market?

-

2U Inc., 3P Learning Ltd., Age of Learning Inc., Brilliant Worldwide Inc., Chegg Inc., Coursera Inc., Duolingo Inc., Epic Creations Inc., Google LLC, Hologo World Inc., IXL Learning Inc., Khan Academy Inc., Lumos Labs Inc., Memrise Ltd., Microsoft Corp., Quizlet Inc., Sololearn Inc., Udemy Inc., UMU Technology CO. LTD. and WizIQ Inc.

-

Market Research Insights

- The market's momentum is sustained by a strategic shift towards measurable outcomes. For instance, personalized tutoring software is linked to a 15% improvement in student test scores over traditional methods. The adoption of gamification in corporate training increases engagement by over 40% compared to standard online modules.

- This emphasis on results drives the development of hybrid learning technologies and multilingual learning platforms. As organizations prioritize remote workforce development, the demand for corporate upskilling applications with robust student progress monitoring tools grows.

- The effectiveness of these platforms is validated through data, demonstrating how interactive assessment platforms can reduce grading time for educators by up to 50%, allowing more focus on instruction.

We can help! Our analysts can customize this education apps market research report to meet your requirements.

RIA -

RIA -