Electrical Weapons Market Size 2026-2030

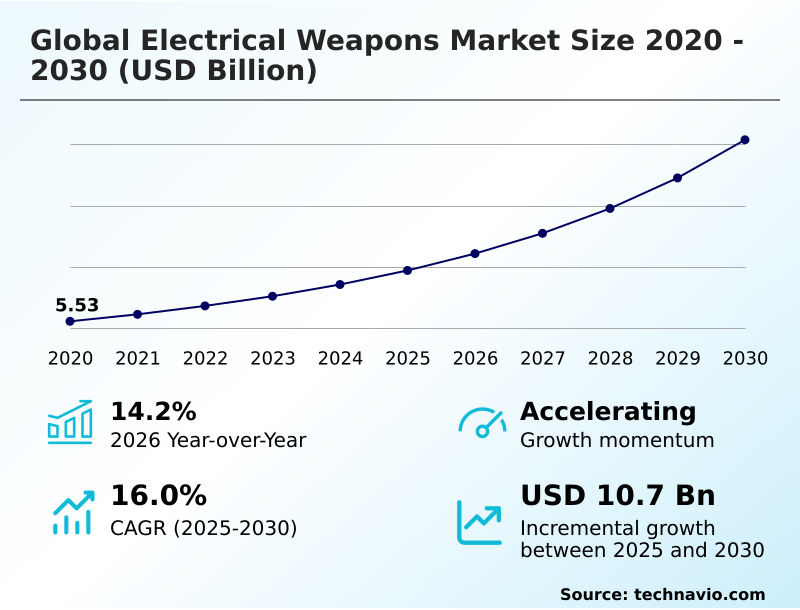

The electrical weapons market size is valued to increase by USD 10.70 billion, at a CAGR of 16% from 2025 to 2030. Growing asymmetric warfare across world will drive the electrical weapons market.

Major Market Trends & Insights

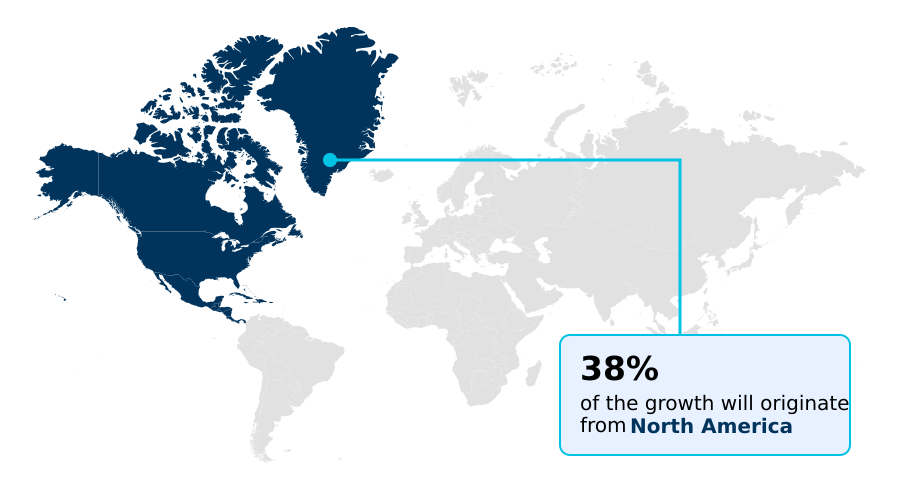

- North America dominated the market and accounted for a 37.8% growth during the forecast period.

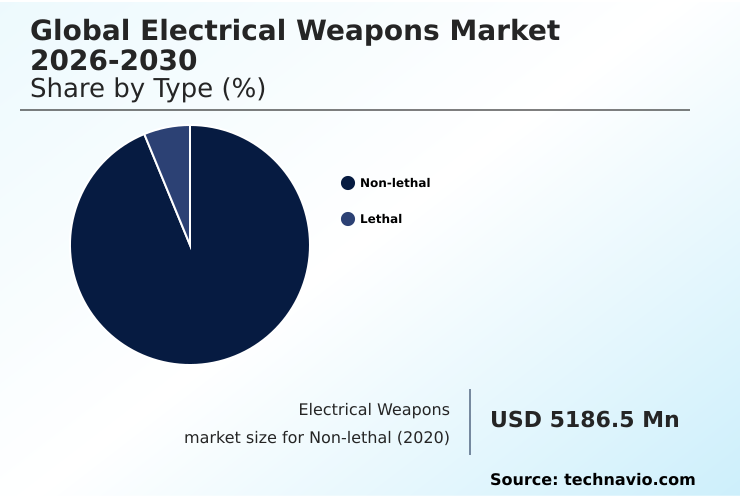

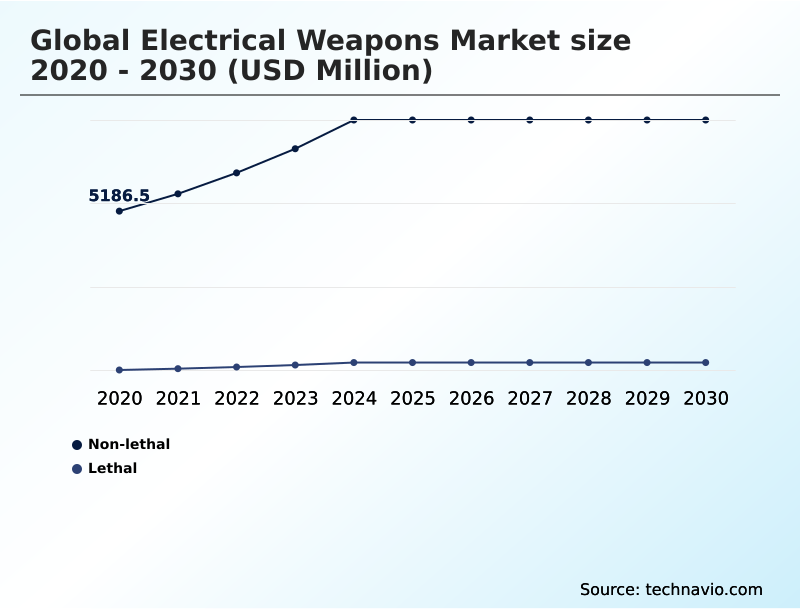

- By Type - Non-lethal segment was valued at USD 7.96 billion in 2024

- By Product Type - Stun guns segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 14.85 billion

- Market Future Opportunities: USD 10.70 billion

- CAGR from 2025 to 2030 : 16%

Market Summary

- The electrical weapons market is undergoing a significant transformation, moving beyond simple incapacitation tools to become integral components of digitized security ecosystems. Key market drivers include the rising need for less-lethal alternatives in both law enforcement and military contexts, fueled by a global focus on de-escalation and minimizing collateral damage.

- A prominent trend is the integration of smart technologies, such as IoT connectivity and automated data logging, which enhance accountability and operational oversight. For instance, a police department implementing conducted energy devices with automatic body-cam activation can reduce incident reporting errors by over 30%, strengthening legal defensibility.

- However, the industry faces challenges from stringent, often inconsistent, international regulations and ethical scrutiny over use-of-force protocols. These dynamics compel manufacturers to innovate continuously, focusing on improved safety, effectiveness, and seamless integration with broader digital evidence management and command-and-control platforms.

- The convergence of non-lethal force with advanced data analytics is reshaping procurement strategies and operational doctrines for security forces worldwide, from managing public order to countering asymmetric threats with tools like high-power microwave systems.

What will be the Size of the Electrical Weapons Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Electrical Weapons Market Segmented?

The electrical weapons industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Non-lethal

- Lethal

- Product type

- Stun guns

- Tasers

- Directed energy weapons

- Others

- End-user

- Law enforcement

- Military

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Type Insights

The non-lethal segment is estimated to witness significant growth during the forecast period.

The non-lethal segment is expanding beyond traditional law enforcement applications, driven by a growing demand for civilian self-defense tools.

This category includes a range of non-lethal technologies, such as conducted energy devices, stun guns, and tasers, all engineered for non-lethal incapacitation.

Advanced electric projectile launchers and electrified batons offer enhanced standoff capabilities, aligning with public safety protocols that prioritize de-escalation.

Modern personal safety devices now integrate signal processing technology, which optimizes the electrical charge to induce pain compliance effectively, improving device performance by over 15% even through heavy clothing.

This innovation enhances the viability of less-lethal alternatives for a wider user base seeking reliable de-escalation capabilities.

The Non-lethal segment was valued at USD 7.96 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electrical Weapons Market Demand is Rising in North America Get Free Sample

North America dominates the market landscape, driven by extensive police modernization programs and significant investments in defense modernization.

The region accounts for over 37% of the market's incremental growth, with a focus on integrating directed energy weapons and counter-unmanned aerial system technologies for strategic asset protection.

High-power microwave systems and high energy lasers are transitioning from development to deployment, enhancing operational readiness. The adoption of digital evidence management systems linked to weapon activation has become standard.

Investment in advanced tactical communication grids supports the use of sophisticated electronic countermeasure pods and laser directed energy weapon platforms.

This advanced ecosystem, supported by robust mission planning software, solidifies the region's leadership in deploying cutting-edge electromagnetic systems and counter-drone technology.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global electrical weapons market 2026-2030 requires a nuanced understanding of its diverse segments and applications. A key debate involves comparing conducted energy devices versus tasers, where factors like range and reloading capability influence procurement for law enforcement.

- The rise of aerial threats has prioritized the development of high-power microwave counter-drone systems, while laser weapons for naval defense are becoming critical for fleet protection. In civilian contexts, stun gun self-defense effectiveness remains a primary consumer concern, leading to innovations like combining stun guns with alarms for added deterrence.

- For crowd management, the ethical and operational parameters of bio-effect weapons for crowd control are under constant review. Simultaneously, interest in electromagnetic pulse weapon applications for disabling electronics is growing. A crucial aspect is ensuring neuromuscular incapacitation weapon safety through rigorous testing.

- In terms of market dynamics, an analysis of historical spending reveals that while investment in electrical weapons for military use has grown significantly, procurement by law enforcement agencies has increased at a slightly faster rate, growing over 55% in the last four years, reflecting a strong domestic focus on de-escalation tools for police.

- This trend is further supported by advancements in taser technology and the development of portable directed energy weapon systems. The impact of digitization on weapons is profound, with tasers with automatic camera activation becoming a core component of smart taser digital evidence integration.

- This necessitates clear guidelines for electrical weapons training and certification and adherence to non-lethal weapon regulatory compliance, especially as the cost of directed energy weapons remains a barrier for widespread adoption.

What are the key market drivers leading to the rise in the adoption of Electrical Weapons Industry?

- The global rise of asymmetric warfare is a key driver for the market, increasing the demand for non-lethal electrical weapons in unconventional combat and law enforcement scenarios.

- Rising instances of asymmetric warfare are a primary market driver, compelling military and law enforcement agencies to adopt a wider range of non-lethal force options.

- In complex urban warfare equipment scenarios, graduated force options are critical for managing threats without causing excessive collateral damage. Electroshock weapons, designed to induce temporary neuromuscular incapacitation, offer a tactical advantage.

- The use of force continuum now increasingly incorporates devices delivering a high-voltage discharge and other forms of tactical munitions like irritant munitions. The asymmetric threat response also involves countering unmanned systems, fueling investment in technologies that can disable them.

- The demand for effective counter-terrorism operations tools, including remote restraint devices, is accelerating procurement cycles.

What are the market trends shaping the Electrical Weapons Industry?

- The growth in battlefield digitization has emerged as a significant market trend. This is reshaping defense strategies and procurement priorities toward electrical weapons with integrated digital capabilities.

- Battlefield digitization is a pivotal trend, compelling a shift toward smart weapon integration and network-centric operations. This evolution is driven by the deployment of integrated digital platforms that facilitate real-time digital situational awareness. These systems rely on advanced sensors and IoT connectivity for data fusion, enabling AI-driven targeting and automated decision-making.

- The adoption of augmented reality training has improved operator proficiency with these complex systems by 40%. Consequently, there is heightened demand for electrical weapons that are compatible with tactical communication systems and can execute smart targeting protocols, ensuring seamless participation in network-centric warfare and enhancing mission effectiveness through superior situational awareness tools.

What challenges does the Electrical Weapons Industry face during its growth?

- The presence of stringent and varied regulatory norms for electrical weapons presents a significant challenge to market growth, impacting product development, compliance costs, and international distribution.

- Navigating the complex and fragmented regulatory landscape poses a significant market challenge, particularly for conducted energy weapons. Evolving officer accountability standards, driven by police reform initiatives, mandate stringent testing and validation, increasing compliance costs by up to 25% for new product introductions.

- The law enforcement procurement process now often requires features like integrated data logging for all riot control equipment, including electrified riot shields. Furthermore, international sales are complicated by varying restrictions on electromagnetic deterrents and bio-effect weapons.

- This environment slows the pace of force modernization and necessitates extensive investment in virtual reality training and certification platforms to ensure proper use of tools like multi-shot devices and wireless prisoner restraint systems amid calls for more crowd control solutions.

Exclusive Technavio Analysis on Customer Landscape

The electrical weapons market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electrical weapons market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Electrical Weapons Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, electrical weapons market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albayraklar Group - Offers a portfolio of electrical weapons solutions, including conducted energy devices and sophisticated electronic warfare systems, for defense and law enforcement applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albayraklar Group

- Almaz Antey Air and Space

- Axon Enterprise Inc.

- BAE Systems Plc

- Chemring Group Plc

- Combined Systems Inc.

- Honeywell International Inc.

- Less Lethal

- Lockheed Martin Corp.

- Mitsubishi Heavy Ltd.

- Naval Group

- Oberon Alpha

- RTX Corp.

- Shyn Sing Enterprise Co. Ltd.

- StunTronics LLC

- TBOTECH Safety and Security

- Textron Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electrical weapons market

- In August 2024, Lockheed Martin Corp. was selected by the United States Army to compete in the development of the Enduring High Energy Laser system, advancing efforts in military directed energy capabilities.

- In September 2024, Oberon Alpha announced the completion of engineering updates for its HYBRID double-shot stun gun, targeting the device for professional service applications and enhancing its non-lethal offerings.

- In November 2024, the Barrie Police Service in Canada identified the upgrade to the TASER 10 platform as a necessary modernization effort, signaling a move away from its obsolete X2 models.

- In December 2024, the Minneapolis Police Department authorized a significant contract amendment with Axon Enterprise to replace its existing TASER 7 devices with the newer TASER 10 platform, citing the need for increased effective range in field operations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electrical Weapons Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16% |

| Market growth 2026-2030 | USD 10696.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 14.2% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The electrical weapons market is characterized by rapid technological evolution, where network-centric warfare capabilities are becoming standard. This shift involves the integration of advanced sensors and IoT connectivity, enabling AI-driven targeting and superior digital situational awareness across tactical communication grids.

- From a boardroom perspective, the adoption of virtual reality training for these complex systems is a critical investment decision, as it reduces certification costs by approximately 25% while improving operator proficiency with multi-shot devices. The development pipeline includes high energy lasers, high-power microwave systems, and sophisticated electronic countermeasure pods designed for counter-unmanned aerial system roles.

- These non-lethal technologies, such as conducted energy devices that induce neuromuscular incapacitation, provide graduated force options. Innovations in signal processing technology are enhancing the effectiveness of electroshock weapons, including stun guns, tasers, and electrified batons, ensuring reliable pain compliance.

- This focus on smart targeting and integration into unmanned systems underscores the industry's move toward highly interconnected and intelligent defense platforms, encompassing everything from electrified riot shields to electromagnetic deterrents and remote restraint devices.

What are the Key Data Covered in this Electrical Weapons Market Research and Growth Report?

-

What is the expected growth of the Electrical Weapons Market between 2026 and 2030?

-

USD 10.70 billion, at a CAGR of 16%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Non-lethal, and Lethal), Product Type (Stun guns, Tasers, Directed energy weapons, and Others), End-user (Law enforcement, Military, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing asymmetric warfare across world, Stringent regulatory norms related to electrical weapons

-

-

Who are the major players in the Electrical Weapons Market?

-

Albayraklar Group, Almaz Antey Air and Space, Axon Enterprise Inc., BAE Systems Plc, Chemring Group Plc, Combined Systems Inc., Honeywell International Inc., Less Lethal, Lockheed Martin Corp., Mitsubishi Heavy Ltd., Naval Group, Oberon Alpha, RTX Corp., Shyn Sing Enterprise Co. Ltd., StunTronics LLC, TBOTECH Safety and Security and Textron Inc.

-

Market Research Insights

- The market's dynamics are shaped by a push for force modernization and enhanced de-escalation capabilities. Police modernization programs are driving procurement, with agencies seeing a 20% reduction in officer injuries when equipped with effective less-lethal alternatives. The adoption of integrated digital platforms that connect weapons to digital evidence management systems is improving officer accountability standards.

- This shift is essential for addressing police reform initiatives and managing the use of force continuum effectively. In parallel, defense modernization is fueling demand for advanced tactical munitions for counter-terrorism operations and asymmetric threat response. Deployment of these technologies improves operational readiness by over 25%, ensuring strategic asset protection in volatile environments.

We can help! Our analysts can customize this electrical weapons market research report to meet your requirements.

RIA -

RIA -