Esports Market Size 2026-2030

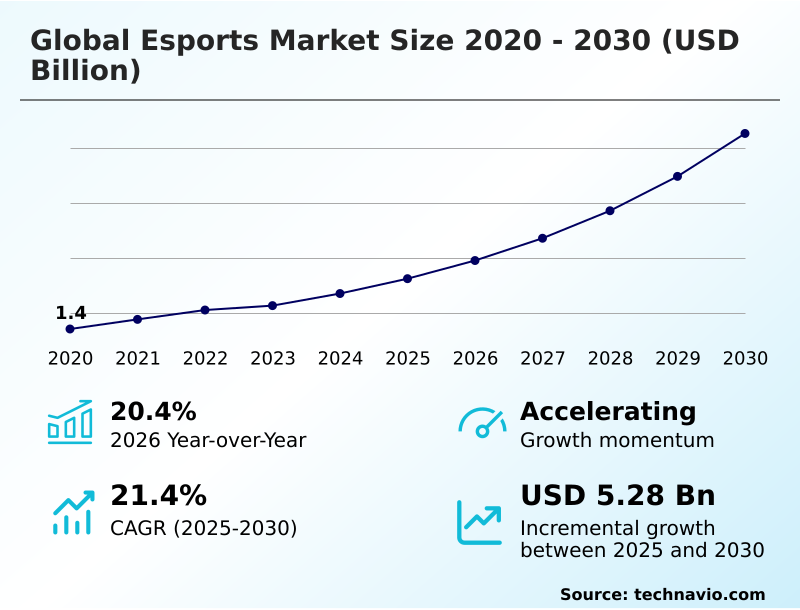

The esports market size is valued to increase by USD 5.28 billion, at a CAGR of 21.4% from 2025 to 2030. Proliferation of strategic brand sponsorships and commercial partnerships will drive the esports market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 42.1% growth during the forecast period.

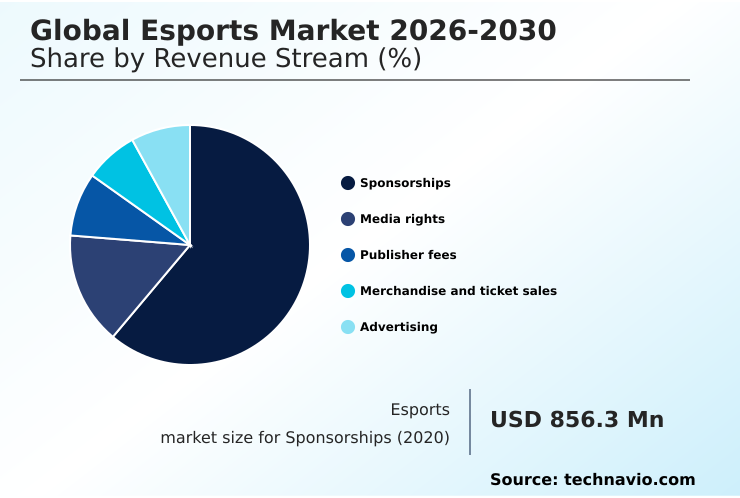

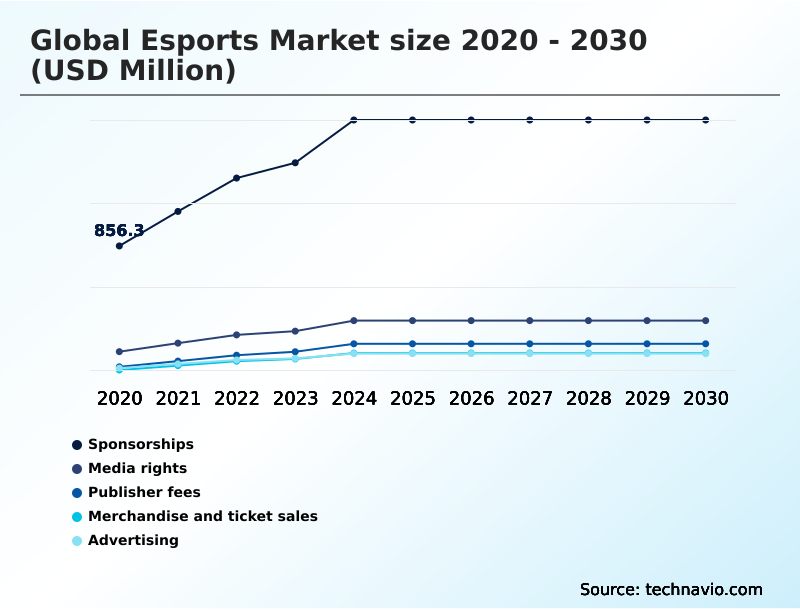

- By Revenue Stream - Sponsorships segment was valued at USD 1.62 billion in 2024

- By Genre - MOBA segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 7.11 billion

- Market Future Opportunities: USD 5.28 billion

- CAGR from 2025 to 2030 : 21.4%

Market Summary

- The esports market is undergoing a period of rapid professionalization and commercial expansion, transitioning from a niche hobby into a mainstream entertainment industry. This growth is propelled by increasing institutional investment from non-endemic brands, the formalization of media rights agreements, and continuous advancements in streaming technology.

- The ecosystem is now a complex interplay of game publishers, who control the intellectual property; professional team organizations managing high-performance training facilities; and tournament organizers staging large-scale live events. A core dynamic involves balancing the interests of these stakeholders.

- For instance, a game publisher must manage game updates to maintain competitive integrity and viewer interest, which directly impacts professional player contracts and team strategies, all while creating opportunities for sponsorship activation and digital content creation.

- Challenges such as player salary inflation and the need for sustainable fan monetization models persist, requiring innovative business strategies to ensure long-term viability for the entire competitive gaming ecosystem.

What will be the Size of the Esports Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Esports Market Segmented?

The esports industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Revenue stream

- Sponsorships

- Media rights

- Publisher fees

- Merchandise and ticket sales

- Advertising

- Genre

- MOBA

- FPS

- RTS

- Others

- Device

- Smart phone and smart TV

- Gaming console

- Desktop/laptop/tablets

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- APAC

By Revenue Stream Insights

The sponsorships segment is estimated to witness significant growth during the forecast period.

The sponsorships segment is a foundational revenue stream, evolving from simple logo placement to complex, multifaceted campaigns. Sophisticated sponsorship activation now involves bespoke digital content, co-branded products, and experiential marketing at live events.

The segment's appeal lies in reaching a young, digitally native audience that is often elusive through traditional media. Data analytics are crucial, with organizations leveraging detailed viewer engagement metrics to demonstrate clear ROI, justifying premium fees and fostering strategic partnerships.

This influx of capital from non-endemic brands is critical for financial stability, supporting everything from high-performance training facilities to larger tournament prize pools.

As a result of such integrated strategies, some teams have seen fan merchandise sales increase by over 25% following a new sponsorship announcement.

The Sponsorships segment was valued at USD 1.62 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 42.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Esports Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the global esports market is diversifying, with APAC poised to contribute 42.1% of the total incremental growth.

This region's competitive gaming ecosystem is heavily influenced by mobile-first battle royale and team-based strategic combat titles, reflecting unique audience demographics and preferences.

In North America, the market is characterized by mature, franchise-based professional leagues for sports simulation games and first-person shooters, which attract substantial media rights deals.

Europe shows a fragmented but passionate market, with strong national leagues and a thriving grassroots competition scene. The growth in these key regions is underpinned by a global trend toward professionalization.

For example, organizations adopting structured collegiate esports programs report a 15% higher rate of securing top-tier talent from grassroots levels, solidifying the global talent pipeline.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A critical examination of the global esports market 2026-2030 reveals nuanced strategic questions that extend beyond surface-level growth metrics. Stakeholders are increasingly focused on the long-term ROI of non-endemic brand sponsorship in esports, seeking data-driven proof of value.

- Concurrently, the debate over publisher control versus third-party tournament organizers intensifies as the ecosystem matures, raising questions about competitive balance and revenue distribution. The industry is also exploring optimal monetization strategies for mobile esports titles, which command massive audiences but often have lower per-user revenue compared to their PC counterparts.

- A significant area of innovation is the impact of AI on professional player performance, with teams using analytics to gain a competitive edge. This has led to the development of new legal frameworks for international player contracts that account for data rights and performance metrics.

- Another key area is comparing franchised vs open tournament circuits, as organizations weigh financial stability against competitive dynamism. The role of cloud gaming in esports accessibility is reshaping infrastructure planning, while educational institutions are focused on building a sustainable collegiate esports program to create a formal talent pipeline.

- Finally, the evolution of fan engagement models in team-based strategic combat games and understanding new revenue streams from virtual goods in battle royale games are central to achieving long-term profitability.

What are the key market drivers leading to the rise in the adoption of Esports Industry?

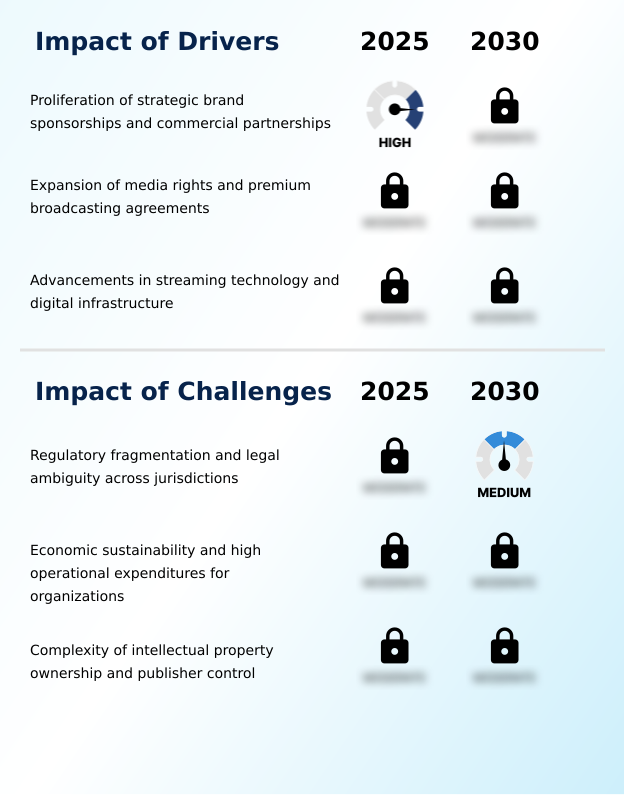

- The proliferation of strategic brand sponsorships and commercial partnerships from non-endemic companies is a primary driver fueling the market's commercialization and professional growth.

- The market's rapid commercialization is fueled by several key drivers, most notably the influx of non-endemic brands executing sophisticated sponsorship activation strategies.

- These brand partnerships extend beyond simple logo placement, integrating into digital content creation and leveraging broadcasting services for maximum reach.

- The formalization of media rights agreements with major digital streaming platforms is creating a stable, high-value revenue stream, with exclusive deals increasing a platform's subscriber base by up to 15% during a tournament season.

- Furthermore, continuous advancements in streaming technology are enhancing the viewer experience and expanding accessibility.

- The adoption of new compression technologies has reduced data usage for mobile viewers by 30%, broadening the addressable audience in data-sensitive markets and reinforcing the value proposition for advertisers and sponsors.

What are the market trends shaping the Esports Industry?

- The expansion of mobile esports, propelled by significant regional infrastructure development in emerging markets, is reshaping the competitive landscape and audience demographics.

- Key trends are reshaping the competitive landscape, led by the expansion of mobile esports and the requisite build-out of regional infrastructure. This shift democratizes access and creates new avenues for fan monetization, where tailored virtual goods sales in mobile-first markets have increased average revenue per user by 15%.

- Simultaneously, the integration of AI and advanced data analytics is revolutionizing both performance and consumption. Teams are using these tools to refine strategies, improving win rates in specific matchups by up to 10%.

- On the broadcast side, AI-driven viewer engagement metrics provide real-time feedback that allows platforms to personalize content, which has proven to extend average watch times by over 20%. This data-centric approach is becoming a cornerstone of the industry's evolution.

What challenges does the Esports Industry face during its growth?

- Regulatory fragmentation and persistent legal ambiguity across key international jurisdictions present a primary challenge to scalable, global operations and investment stability.

- The market faces significant structural challenges that temper its growth trajectory. The primary issue is the lack of a unified regulatory framework, creating legal ambiguity in areas like professional player contracts and cross-border operations. This regulatory fragmentation increases compliance costs by an estimated 20% for organizations operating globally.

- Another critical challenge is achieving economic sustainability amid high operational expenditures and rampant player salary inflation. Many teams struggle to diversify beyond brand sponsorships, with over 60% of revenue for mid-tier organizations still coming from this single source.

- Finally, the absolute intellectual property ownership and control wielded by game publishers create inherent market instability, as they can unilaterally alter a game's competitive ecosystem, risking the investments of all other stakeholders.

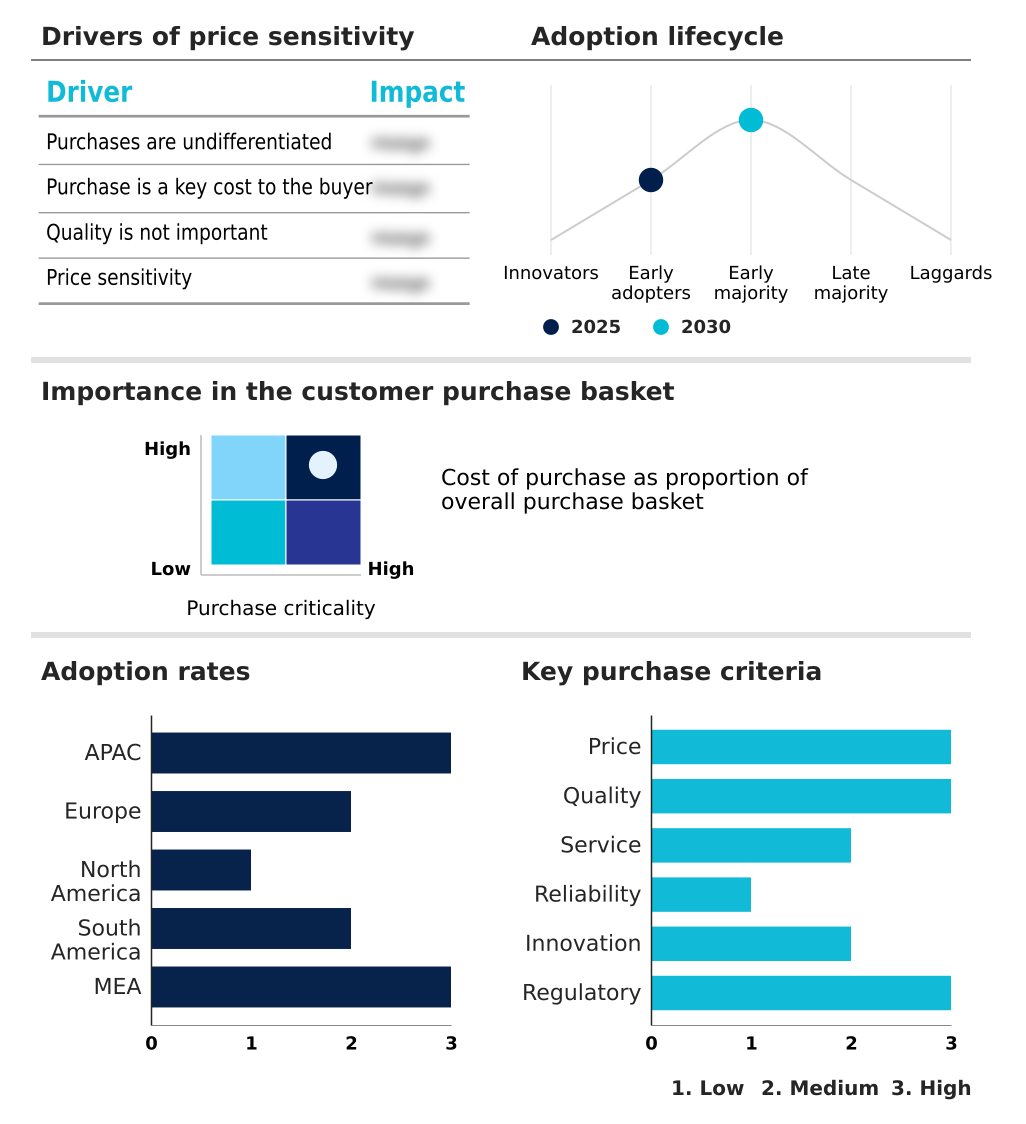

Exclusive Technavio Analysis on Customer Landscape

The esports market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the esports market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Esports Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, esports market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

100 Thieves LLC - The company provides a portfolio of premier esports leagues and competitive gaming tournaments, operating key franchises that are central to the professional competitive ecosystem.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 100 Thieves LLC

- Activision Blizzard Inc.

- BLAST ApS

- Cloud9 Esports Inc

- DreamHack AB

- Electronic Arts Inc.

- Epic Games Inc.

- ESL FACEIT Group

- FaZe Holdings Inc

- Fnatic Ltd.

- G2 Esports GmbH

- Garena

- Krafton Inc.

- Logitech International SA

- Nintendo Co. Ltd.

- Riot Games Inc.

- Team Liquid

- TSM FTX Inc

- Ubisoft Entertainment SA

- Valve Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Esports market

- In March 2025, the Esports World Cup Foundation expanded its Club Partner Program, committing an additional $20 million to support team development and fan engagement initiatives.

- In March 2025, Activision Blizzard Inc. announced a strategic overhaul for its main franchise league, shifting to an open, tournament-based circuit to reduce financial burdens on teams and improve viewership.

- In January 2025, Riot Games Inc. adjusted its global partnership policies, officially permitting its partnered teams in major leagues to secure sponsorships from approved betting companies to enhance team financial sustainability.

- In January 2025, the German Federal Ministry for Digital and Transport launched a $50 million fund to upgrade municipal arenas with fiber optic technology, bolstering the nation's esports infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Esports Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.4% |

| Market growth 2026-2030 | USD 5282.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, South Africa, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The esports market is defined by a highly structured competitive gaming ecosystem, where franchise-based leagues and major tournament prize pools are becoming standard. This professionalization is underpinned by sophisticated live event production and advancements in streaming technology, which facilitate a richer viewer experience through enhanced data analytics.

- The integration of non-endemic brands via complex sponsorship activation has become a crucial revenue stream, though it necessitates careful management of intellectual property ownership and publisher control. A key boardroom consideration is the high operational cost, including player salary inflation and investments in high-performance training facilities, which must be balanced against revenue from media rights agreements and in-game monetization.

- Organizations that successfully leverage digital content creation and fan monetization strategies see higher engagement. For instance, teams integrating direct-to-fan virtual goods sales have achieved a 30% increase in ancillary revenue per fan. Success hinges on navigating this complex environment, from managing professional player contracts to fostering grassroots competition and exploring ancillary markets like esports betting.

What are the Key Data Covered in this Esports Market Research and Growth Report?

-

What is the expected growth of the Esports Market between 2026 and 2030?

-

USD 5.28 billion, at a CAGR of 21.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Revenue Stream (Sponsorships, Media rights, Publisher fees, Merchandise and ticket sales, and Advertising), Genre (MOBA, FPS, RTS, and Others), Device (Smart phone and smart TV, Gaming console, and Desktop/laptop/tablets) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of strategic brand sponsorships and commercial partnerships, Regulatory fragmentation and legal ambiguity across jurisdictions

-

-

Who are the major players in the Esports Market?

-

100 Thieves LLC, Activision Blizzard Inc., BLAST ApS, Cloud9 Esports Inc, DreamHack AB, Electronic Arts Inc., Epic Games Inc., ESL FACEIT Group, FaZe Holdings Inc, Fnatic Ltd., G2 Esports GmbH, Garena, Krafton Inc., Logitech International SA, Nintendo Co. Ltd., Riot Games Inc., Team Liquid, TSM FTX Inc, Ubisoft Entertainment SA and Valve Corp.

-

Market Research Insights

- Market dynamics are defined by a push toward sustainable monetization strategies and enhanced viewer engagement. The reliance on brand sponsorships is diversifying, with professional leagues now generating significant revenue from media rights, where exclusive broadcast deals have shown to increase platform-specific viewership by up to 40%.

- Concurrently, data-driven insights are optimizing brand partnerships, improving activation ROI by over 25% through precise audience analytics. However, a key tension exists between publisher relations and team organizations over revenue sharing from virtual items and franchised league fees.

- This competitive landscape requires organizations to innovate fan engagement models beyond traditional methods, exploring new avenues to secure long-term financial health in a rapidly professionalizing industry.

We can help! Our analysts can customize this esports market research report to meet your requirements.

RIA -

RIA -