Farro Market Size 2024-2028

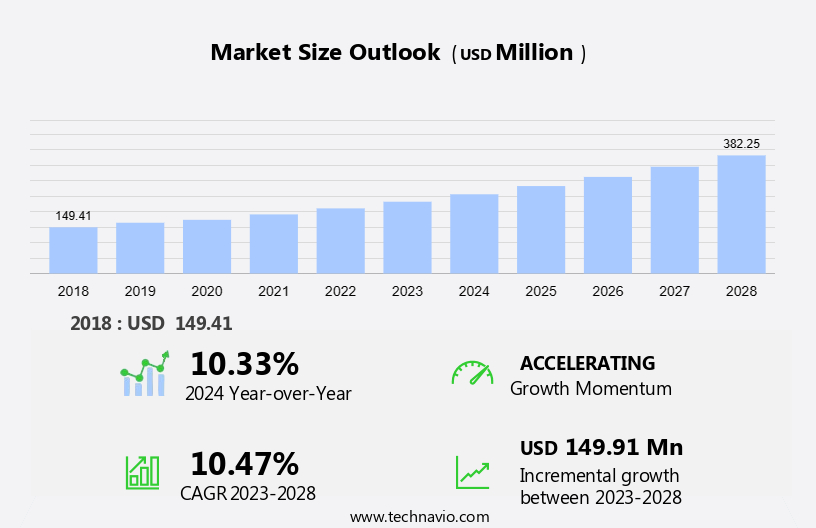

The farro market size is projected to increase by USD 149.91 million, at a CAGR of 10.47% between 2023 and 2028. Major contributors to the market include the UK, Germany, France, Spain, Italy, and the Russian Federation, with notable companies such as Waitrose and Poggio operating in the region. Growing consumer demand for ancient grains like farro, spelled, Kamut, and oats is evident, driven by their associated health benefits. These grains, particularly farro, are increasingly utilized in food product innovations within the European food and beverages industry, offering enhanced nutritional value compared to alternatives. This surge in demand has led to increased farro imports into Europe for both direct consumption and incorporation into various food and beverage applications. Agribosco SRL is a key player, offering organic pearled emmer (farro perlato bio), emphasizing 100% organic content that can be stored in a cool, dry place away from heat sources. Such factors are expected to drive the regional market growth during the forecast period.

Market Overview

To get additional information about the market report, Request Free Sample

Market Dynamics

The market is propelled by increasing consumer interest in nutritional profile and health-conscious eating. Both conventional and organic farro varieties are gaining popularity due to their high protein, fiber, and mineral content. Consumers' preference for non-GMO & pesticide-free grown products drives demand in supermarkets & hypermarkets and on brand websites. However, challenges include competition from refined grains and consumer education about farro's benefits. As the market embraces plant-based diets, farro, along with related products like muesli and oats, is set to thrive amidst changing consumer preferences and dietary trends.

Key Market Driver

Increased use of farro as an ingredient in muesli is notably driving the market development. Farro is a healthier alternative to white rice and other refined grains due to its high nutritional value. It has a rich nutritional profile of protein, fiber, magnesium, zinc, and B vitamins and, therefore, witnesses significant demand as a nutritional ingredient in breakfast food options, especially in muesli. Muesli is a mixture of oats, cereals, grains, nuts, and dry fruits, and its consumption is high globally. The premiumization of packaged breakfast cereals, due to their high-quality ingredients, is expected to propel the market trends and analysis of the muesli market globally.

As a result, several vendors operating in the market offer muesli products with farro as a nutritional ingredient. For instance, Poggio del Farro srl offers ORGANIC biscuits with flakes, in which whole-grain farro flour and flakes are used as sources of protein and fiber. Similarly, the company also offers organic farro crunchy with chestnut flour, which contains farro flakes as a nutritional ingredient. Hence, the increasing use of farro as a nutritional ingredient in muesli is expected to propel the growth of the market during the forecast period.

Major Market Trends

The increasing influence of blogs and digital media on farro consumption is an emerging trend shaping the market growth. The adoption of farro as a necessary ingredient has been favorably affected by blogs about its advantages. Bloggers promote the qualities of cereal grains, such as farro, by sharing their expertise and experience with farro consumption. Consumers prefer products that are devoid of chemicals and preservatives. Besides, farro is used in the food and beverages industry and by end consumers as a healthy food products and ingredient in meals. Furthermore, the increased global adoption of cell phones and the internet has contributed to people's reliance on digital media for product information.

Consumers consult blogs on food ingredients and recipes available online to understand the nutritional qualities of farro-based meals. In addition, many blogging web portals promote the consumption and recipes of meals. Therefore, the availability of blogs and information through digital media is expected to increase the consumption of farro, either directly or through food and beverage products, which in turn may fuel the growth of the market during the forecast period.

Significant Market Challenge

The availability of substitutes for farro is a significant challenge impeding the market development. The availability of numerous substitutes for farro is likely to pose a severe challenge to the growth of the market. The substitutes in the market are available in both conventional and organic forms, offering similar types of nutritional value. These substitutes include teff, quinoa, barley, wheat, Kamut flour, and amaranth flour. These substitutes are witnessing a huge demand in the food and beverages industry for use as ingredients in breakfast food products.

Moreover, the major substitutes for farro are wheat and barley, which have high market shares due to their easy availability and lower price compared to farro. Several food and beverage vendors offer food products where substitutes are used as ingredients. Therefore, the growing consumption of farro substitutes in the food and beverages industry is expected to hamper the growth of the market during the forecast period.

Market Segmentation

By Distribution Channel

Farro is mostly sold through offline distribution channels, which include retail formats such as specialty stores; hypermarkets, supermarkets, and convenience stores; and warehouse clubs or local grain vendors. These retail formats help generate most of the revenue in the global market and account for the major portion of the total market. The major part of the revenue stems from retail formats such as hypermarkets, supermarkets, convenience stores, and warehouse clubs. In addition, consumers find it beneficial to shop from such retail stores owing to the attractive discount offers and schemes. Some key retailers that operate hypermarkets, supermarkets, convenience stores, and warehouse clubs are the following: Walmart Stores Carrefour Target Tesco These developments and factors are expected to augment the demand for the offline segment distribution channel segment globally and, therefore, are expected to drive the growth of the market during the forecast period.

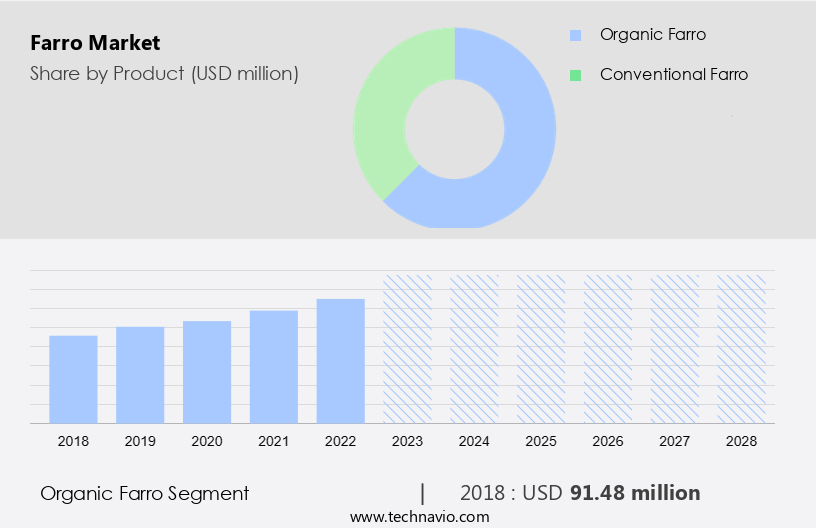

By Product

The market share growth by the organic farro segment will be significant during the forecast period. Farro is often perceived as a nutritious whole grain, rich in fiber, protein, vitamins, and minerals. The increasing awareness of the health benefits associated with whole grains can drive demand among consumers seeking healthier dietary choices. The low price of conventional farro, when compared with organic farro, is one of the major factors that will drive the growth of the segment.

The organic farro was the largest and was valued at USD 91.48 million in 2018

For a detailed summary of the market segments Request for Sample Report

The demand for conventional farro is expected to increase during the forecast period due to the rising awareness among consumers about its various health benefits. Farro is rich in antioxidants, fiber, and various vitamins and minerals. The use of conventional farro as an essential ingredient in many food and beverages will also propel the growth of the segment. Roland Foods LLC (Roland Foods) and Nature Earthly Choice are some of the prominent vendors that offer conventional products. Also, several private label brands offer conventional farro to the food and beverages industry and end-consumers. Thus, the health benefits of conventional farro and its applications in the food and beverages industry will drive the growth of the segment during the forecast period.

By Region

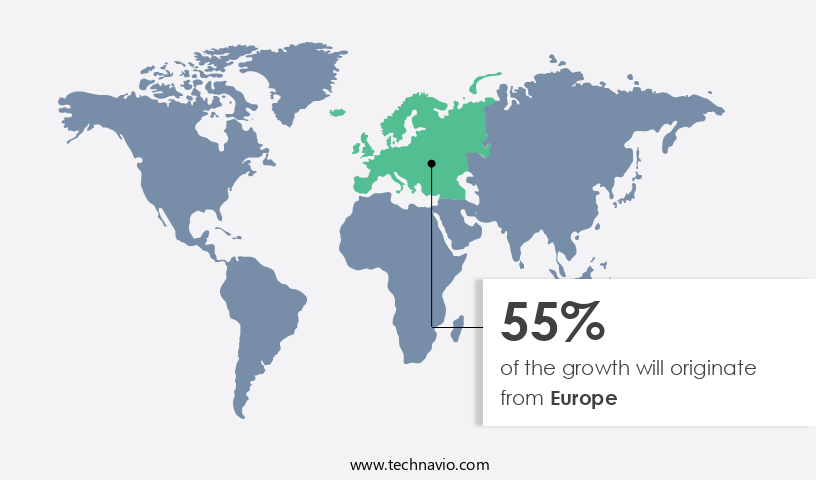

Europe is estimated to contribute 55% to the growth of the global market during the forecast period

Get a glance at the market share of various regions View PDF Sample

Technavio's analysts have provided extensive insight into the market forecasting, detailing the regional trends and drivers influencing the market's trajectory throughout the forecast period. Further, farro crops can be grown in hilly and mountainous regions due to their ability to grow in poor-quality soil and resistance to fungal diseases. Therefore, farro production in the mountainous regions of European countries, such as Switzerland, Italy, and Turkey, will likely increase during the forecast period. In Central Italy, farro is grown as a geographical indication (GI) product and requires no insecticides to control crop diseases.

Additionally, the growing consumer interest in traditional food grains with high nutritional values and increasing adoption of agrobiodiversity conservation for cropping systems among farmers have been fueling the production of organic farro in the mountainous regions of Europe. Therefore, the above factors are likely to increase the production and consumption of farro in the region during the forecast period.

Company Overview

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market forecasting growth and analysis.

- Key Offering- Anson Mills: The company offers slow roasted farro which is used in Italy as a foundation ingredient in soups, stews, salads, and desserts.

- Key Offering- Bluebird Grain Farms: The company offers organic whole grain emmer farro which makes a fabulous pilaf, grain salad, risotto, addition to soup, or sprouted for bread and salads.

The market growth and forecasting report also includes detailed analyses of the competitive landscape of the market and information about 10 market companies, including Agribosco SRL, Anson Mills, Bluebird Grain Farms, Bobs Red Mill Natural Foods Inc., Flourist, Hayden Flour Mill, Hive Brands, Hodmedod Ltd., Italco Food Products Inc., Janies Mill, Molino Bertolo., Molino Peila SpA, Natures Earthly Choice, Poggio del Farro srl, PROMETEO SRL, Roland Foods LLC, SHILOH FARMS, Timeless Seeds Inc., Vigo Importing Co., and Woodland Foods Ltd.

The market analysis and report of qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Segment Overview

The market research and growth report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Million" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments

- Product Outlook

- Organic

- Conventional

- Distribution Channel Outlook

- Offline

- Online

- Region Outlook

- North America

- The U.S.

- Canada

- South America

- Chile

- Brazil

- Argentina

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also interested in the market reports:

-

Grain and Cereal Crop Protection Market: Grain and Cereal Crop Protection Market Analysis APAC, South America, Europe, North America, Middle East and Africa - US, China, India, France, Brazil - Size and Forecast

-

Grain Silos and Ancillary Equipment Market: Grain Silos and Ancillary Equipment Market Analysis North America, Europe, APAC, South America, Middle East and Africa - US, Germany, Canada, UK, China - Size and Forecast

-

Flour Market: Flour Market Analysis APAC,Europe,North America,South America,Middle East and Africa - US,China,India,Germany,France - Size and Forecast

Market Analyst Overview

The market is witnessing significant growth, particularly in the whole grain farro segment, driven by consumers' growing preference for convenience food products and plant-based meals. Farro, classified among staple grains, is gaining traction as a wholesome and organically sourced wholesome grains alternative in on-the-go meals and culinary applications, offering a delightful taste experience.

Furthermore, as consumers prioritize high quality sustainable diets over unhealthy products, demand for farro continues to rise. With a focus on non-GMO & pesticide-free grown products, supermarkets chains & hypermarkets play a crucial role in increasing the visibility and assortment of plant-based products, both in their offline outlets and through online segment like brand websites. As consumer spending reflects a shift towards healthier food choices, the market is poised for continued expansion. The global farro market is seeing an increased yield for farro, with the harvest being prominently labeled in supermarket chains.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

155 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.47% |

|

Market Growth 2024-2028 |

USD 149.91 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.33 |

|

Regional analysis |

Europe, North America, Middle East and Africa, APAC, and South America |

|

Performing market contribution |

Europe at 55% |

|

Key countries |

US, Italy, France, Germany, and Switzerland |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Agribosco SRL, Anson Mills, Bluebird Grain Farms, Bobs Red Mill Natural Foods Inc., Flourist, Hayden Flour Mill, Hive Brands, Hodmedod Ltd., Italco Food Products Inc., Janies Mill, Molino Bertolo., Molino Peila SpA, Natures Earthly Choice, Poggio del Farro srl, PROMETEO SRL, Roland Foods LLC, SHILOH FARMS, Timeless Seeds Inc., Vigo Importing Co., and Woodland Foods Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the market forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

BUY NOW Full Report and Discover more

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market between 2024 and 2028

- Precise estimation of the market size and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across Europe, North America, Middle East and Africa, APAC, and South America

- A thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -